BCA Research’s chief strategist Juan Correa declared on 1 May 2026 that hyperscalers had collectively deployed more than $400 billion into data centre infrastructure over the prior 12 months, a figure he characterised as the primary engine of the current economic cycle. The statement accompanied a suite of allocation changes: an upgrade of U.S. equities to neutral, an elevation of Communication Services to overweight, and explicit naming of Meta and Alphabet as the firm’s preferred AI plays. For investors tracking institutional AI investment strategy, the moves represent a concrete repositioning by a research house that had maintained a sceptical stance on hyperscaler spending, now aligning tactically with a capex cycle it views as self-sustaining. What follows unpacks BCA’s rationale, the data behind its conviction, the specific stock-level logic, and the geopolitical risk shaping the regional calls.

Why BCA sees infrastructure spending, not the consumer, as the cycle’s true engine

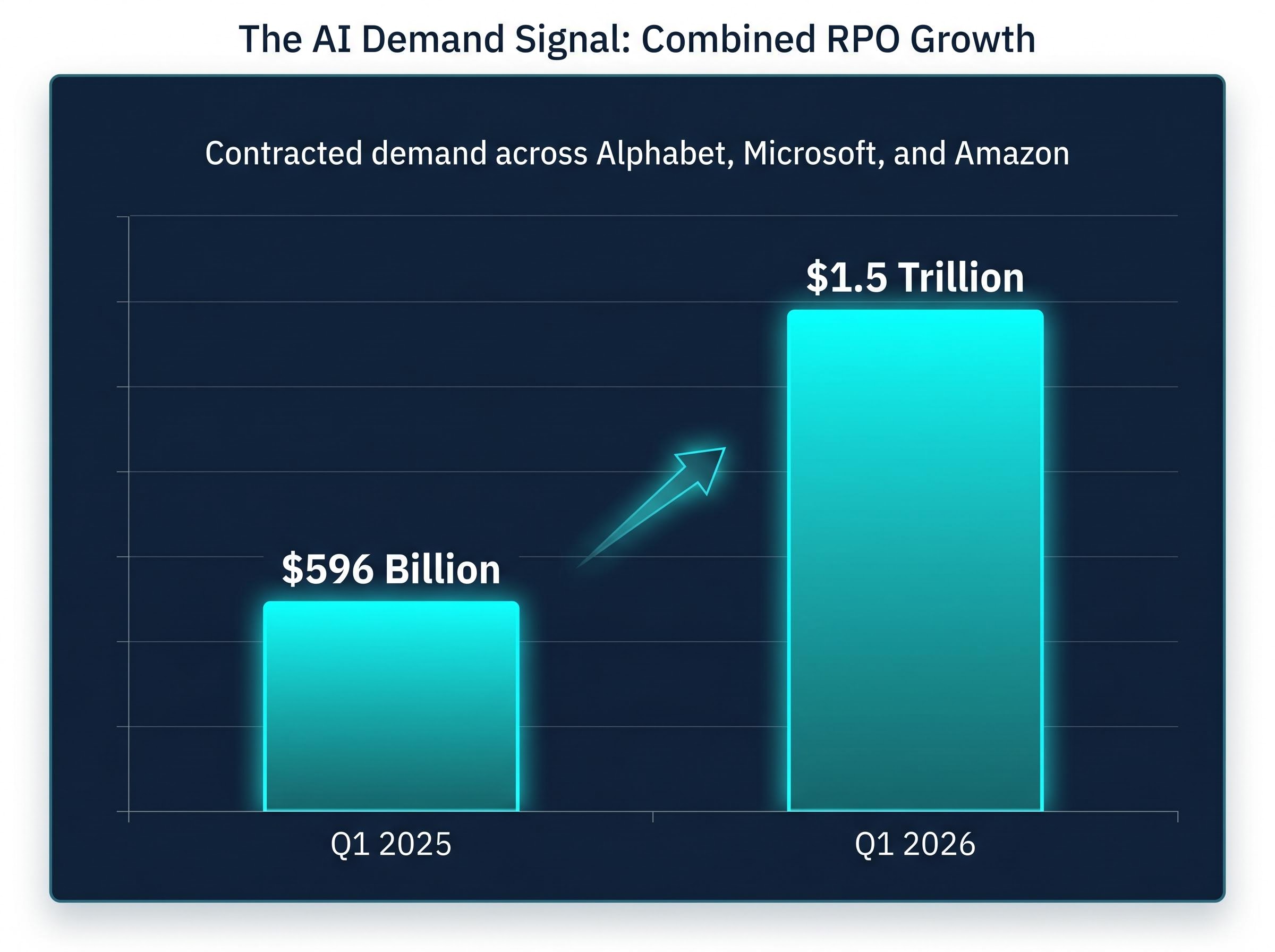

The numbers arrived first: more than $400 billion in trailing 12-month data centre spending from the hyperscaler group, and a combined remaining performance obligations (RPO) figure that had ballooned across the three largest cloud providers.

Demand signal: Combined remaining performance obligations for Alphabet, Microsoft, and Amazon grew from $596 billion in Q1 2025 to $1.5 trillion in Q1 2026, a figure BCA treats as the clearest forward indicator of structural AI adoption.

BCA’s thesis rests on a specific claim: that corporate AI infrastructure investment, not consumer spending, is functioning as the endogenous growth engine of the current economic cycle. The firm’s language is deliberate. “Endogenous” signals that this spending is self-sustaining, driven by contracted demand rather than consumer confidence or monetary stimulus.

Two data points anchor the argument:

- Hyperscalers collectively deployed more than $400 billion into data centre infrastructure over the prior 12 months.

- RPOs across Alphabet, Microsoft, and Amazon expanded from $596 billion to $1.5 trillion in a single year.

Correa added a secondary factor: the current administration’s demonstrated sensitivity to falling equity markets, which BCA reads as an asymmetric upside tilt. If policymakers treat equity declines as politically intolerable, the probability distribution of returns skews positive for U.S. stocks even in a weakening consumer environment.

When big ASX news breaks, our subscribers know first

What the $400 billion figure actually measures: hyperscaler capex and the AI demand signal

The $400 billion figure captures physical spending on data centre construction, server procurement, networking equipment, and supporting infrastructure. It is a backward-looking measure of capital already deployed. What makes it forward-looking is the RPO figure sitting behind it.

Remaining performance obligations represent the total value of contracted but not yet recognised revenue across cloud and AI services agreements. When a hyperscaler signs a multi-year enterprise AI contract, the full contract value enters the RPO balance. The growth from $596 billion to $1.5 trillion in 12 months signals that enterprises are not merely experimenting with AI services; they are locking in multi-year commitments at a pace that justifies the infrastructure buildout.

Goldman Sachs projects AI companies will invest more than $500 billion in 2026 alone, a figure that captures the acceleration BCA is now positioning around.

Individual hyperscaler spending in Q1 2026

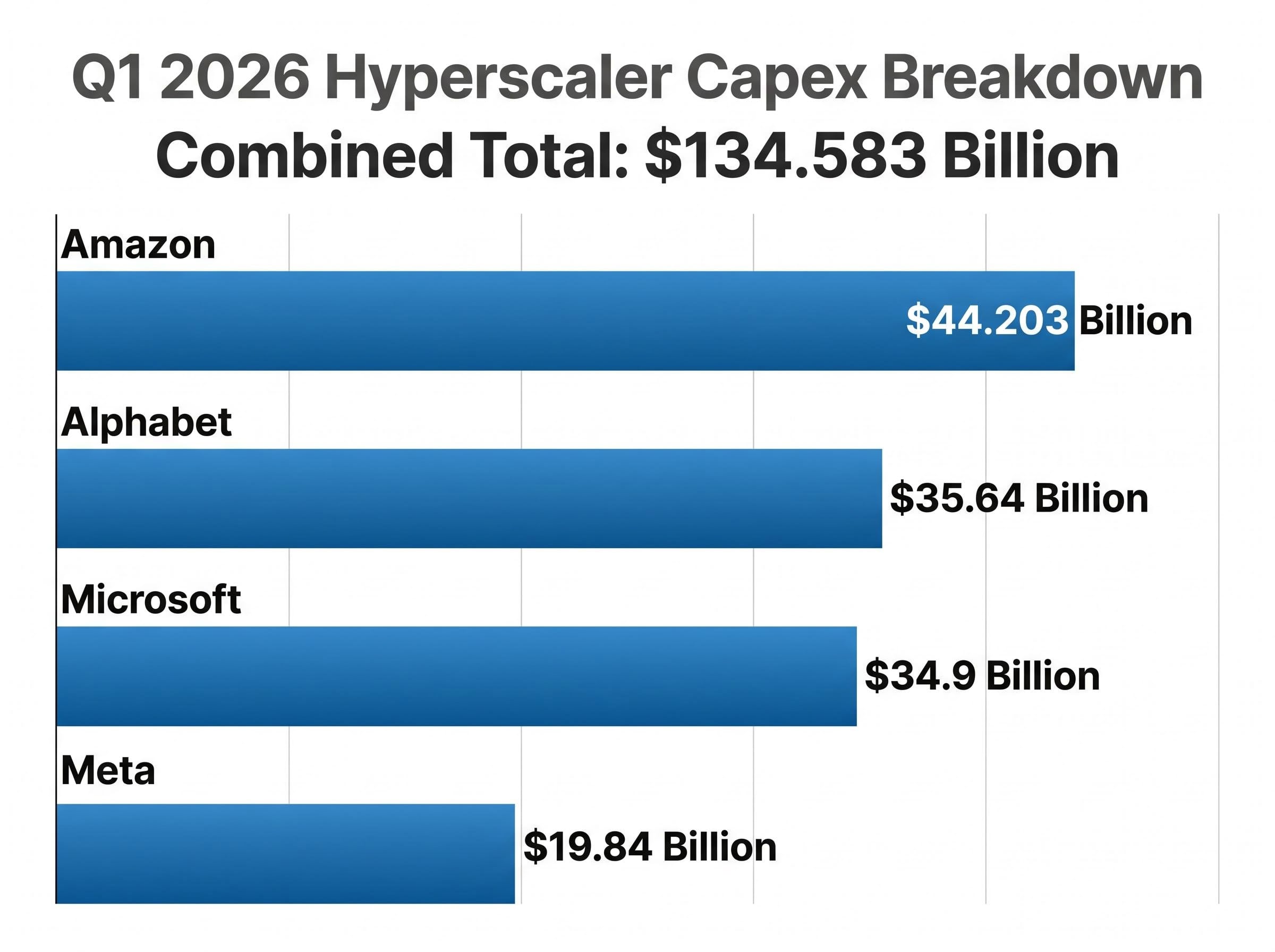

The four largest hyperscalers reported a combined $134.583 billion in capital expenditure during Q1 2026, establishing the current quarterly run-rate underpinning BCA’s trailing figure.

The Q1 2026 earnings season concentrated roughly 44% of S&P 500 market capitalisation into a single reporting week, making the capex disclosures from Microsoft, Amazon, Alphabet, and Meta the most watched data points in a period where forward guidance carried more market weight than backward-looking results.

| Company | Q1 2026 Capex | Full-Year 2026 Outlook |

|---|---|---|

| Alphabet | $35.64 billion | Not formally guided |

| Microsoft | $34.9 billion | Not formally guided |

| Amazon | $44.203 billion | ~$200 billion (Evercore, Mark Mahaney) |

| Meta | $19.84 billion | $125-145 billion (+$10B raise) |

Two forward signals stand out. Meta raised its full-year 2026 capex outlook by $10 billion, to $125-145 billion, a decision that drew an after-hours share price decline but signalled management’s conviction that capacity investment will yield returns. Amazon’s full-year framework of approximately $200 billion, corroborated by Evercore’s Mark Mahaney, represents the single largest annual infrastructure commitment from any technology company in history.

The allocation moves: U.S. equities upgraded, Communication Services elevated

BCA announced four concrete rating changes on 1 May 2026:

- U.S. equities raised to neutral

- Communication Services raised from neutral to overweight

- EU equities lowered from overweight to underweight

- Australian equities reduced from overweight to neutral

The U.S. equity upgrade is a tactical call, not an absolute bull case. BCA reads reduced investor positioning since the onset of the Strait of Hormuz conflict as a wall of worry creating upside optionality. Investors pulled back exposure during the disruption; if AI capex continues at current pace and geopolitical conditions stabilise, the re-entry dynamic could amplify returns.

BCA’s Juan Correa framed the positioning gap as the source of asymmetric upside: reduced investor exposure since the Hormuz conflict, combined with the administration’s sensitivity to equity market declines, creates a return distribution tilted to the positive side for U.S. equities specifically.

The EU downgrade reflects a different calculus. European economies face disproportionate exposure to Hormuz-driven energy disruption, which BCA views as compressing consumer purchasing power and removing easy monetary policy as a viable response. The U.S. upgrade is coherent precisely because of the EU downgrade; it is a relative call anchored to the AI capex differential and lower geopolitical energy risk.

Meta and Google as the preferred vehicles: why BCA picked these two

Juan Correa named Meta and Alphabet as BCA’s explicitly preferred plays within the Communication Services overweight. The logic is not generic “AI winner” designation. Both companies sit at the intersection of massive infrastructure deployment and existing monetisation platforms, giving them dual exposure: efficiency gains from AI integration into advertising and content systems, and revenue growth from cloud and enterprise AI services.

Alphabet’s cloud monetisation signal

Alphabet advanced following Q1 2026 earnings on signals that its cloud division is beginning to exhibit monetisation patterns resembling those of Amazon Web Services in its high-growth phase. The cloud segment’s trajectory suggests that years of infrastructure investment are translating into contracted revenue at an accelerating rate.

BCA appears to view this as validation of the thesis that capex deployed today is generating durable, recurring revenue streams rather than speculative capacity overhang.

Meta’s capex raise as a long-term bet

Meta declined in after-hours trading after announcing the $10 billion capex raise to $125-145 billion for 2026. The market’s immediate reaction reflected spending discipline concerns. BCA’s read-through differs. The firm appears to interpret the raise as an investment in future monetisation capacity, positioning Meta to capture AI-driven advertising revenue improvements and enterprise AI demand.

- Alphabet’s case: Cloud monetisation acceleration, AWS-like revenue scaling, and post-earnings price advance as confirmation of the investment thesis.

- Meta’s case: Near-term capex concern as noise obscuring long-term AI positioning; the $10 billion raise signals management conviction in AI-driven revenue growth.

BCA characterises the current moment as potentially the early stage of a sharp, accelerating AI equity rally, with these two names as the leading-edge beneficiaries.

The geopolitical overlay: why Hormuz risk is reshaping the regional map alongside AI

The Strait of Hormuz disruption is not a separate story from the AI thesis. It is the structural force that makes BCA’s regional calls coherent.

BCA’s assessment holds that the Hormuz closure is depleting energy inventories and compressing consumer purchasing power globally. The inflationary pressure removes easy monetary policy as a response tool, a constraint that affects all regions but not equally.

Markets process geopolitical disruptions as probability-adjusted earnings inputs rather than proportional headline shocks, which explains why the S&P 500 closed near record levels on 29 April 2026 despite active Hormuz disruption; the mechanism BCA is exploiting with its wall-of-worry framing is precisely this gap between perceived risk and actual earnings impact.

- EU equities rated at underweight: the eurozone faces disproportionately larger negative impact from the disruption due to higher energy import dependence, which is the primary differentiating factor versus the U.S.

- U.S. equities rated at neutral: the AI capex engine provides a domestic growth offset that Europe lacks, and reduced investor positioning since the conflict creates re-entry optionality.

- Australian equities reduced from overweight to neutral: a partial unwinding of a prior conflict-era upgrade, reflecting BCA’s view that the initial commodity-linked upside has been captured.

The wall of worry BCA cites is not abstract. Investors reduced U.S. equity exposure during the Hormuz conflict. If capex-driven earnings continue to deliver and geopolitical conditions do not deteriorate further, that positioning gap narrows from below, generating price appreciation.

BCA’s bet on AI’s staying power, and what could prove it wrong

BCA’s overall position is now a tactical upgrade driven by three layers: AI capex as the cycle engine, Communication Services as the sector vehicle, and Meta and Alphabet as the stock-level expression. The firm’s prior scepticism makes the shift notable; this is not a research house that arrived at AI optimism by default.

The broader institutional consensus supports sustained spending:

- Goldman Sachs projects AI companies will invest more than $500 billion in 2026.

- Morgan Stanley frames a $2.9 trillion AI-related investment opportunity.

- McKinsey projects up to $7 trillion globally in data centre infrastructure by 2030.

The Goldman Sachs AI spending projections for 2026 place total sector investment above $527 billion, a figure that aligns closely with BCA’s characterisation of the capex cycle as self-sustaining and provides institutional consensus backing for the firm’s tactical repositioning.

BCA is now tactically aligning with this backdrop despite having previously warned of boom-to-bust dynamics. The alignment is conditional. Correa has identified the signal that would indicate the thesis has run its course.

The Buffett Indicator at historic extremes, sitting at 223.6% as of 1 May 2026 and approximately 2.4 standard deviations above its long-run trend, represents the structural counterargument to BCA’s tactical upgrade; the firm’s call is explicitly conditional and short-duration, which is a meaningful distinction when broader valuation frameworks are signalling a market priced well beyond historical norms.

Key risk signal: BCA has flagged deteriorating free cash flow among hyperscalers as the reversal indicator to monitor. Even if nominal profits remain strong, declining free cash flow would signal that capex is consuming returns rather than generating them, marking the point at which the spending cycle transitions from growth engine to capital destruction.

Free cash flow compression is already measurable across the hyperscaler group, with Alphabet among the companies facing the most acute reductions as capital expenditure consumes an increasing share of operating cash generation; BCA’s reversal signal is not hypothetical but is visible in balance sheets today.

Readers tracking these positions may find the free cash flow metric the most useful ongoing monitoring tool. BCA’s thesis holds as long as hyperscaler capital deployment generates contracted revenue faster than it consumes cash. The moment that relationship inverts, the tactical upgrade unwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including institutional projections for AI spending and market positioning, are subject to change based on market developments and company performance.