A $200 million AI contract collapsed in January 2026, and within weeks the Pentagon had signed deals with multiple technology firms, expanded its vendor coalition, and made clear that no single company would dictate how the United States military deploys artificial intelligence. The speed of the response, and the breadth of the companies now inside the defence AI procurement pipeline, signals something larger than a contract dispute. For investors tracking the intersection of AI spending and defence budgets, the Anthropic fallout has become the organising event of 2026: a clarifying moment that revealed which firms the Pentagon will work with, on what terms, and why the companies willing to operate without use-policy constraints now hold a structural advantage in one of the fastest-growing procurement markets in the world. This analysis maps the confirmed contract awards, assesses what the vendor coalition means for Nvidia, Microsoft, Amazon Web Services, and Reflection AI, and examines the broader investment implications of a defence establishment that has made permissive AI adoption its stated doctrine.

What the Pentagon and Anthropic actually fought over

The breakdown was not abstract. Two specific use cases sat at the centre of the dispute: the Pentagon’s demand that Anthropic‘s Claude AI be used for mass domestic surveillance of unclassified bulk data on U.S. citizens (including geolocation and web browsing data), and its deployment in fully autonomous lethal weapons systems.

Anthropic was not refusing all classified work. The company had indicated willingness to allow NSA use of Claude on classified material. Its objections were targeted, not blanket. The Pentagon rejected that distinction entirely.

Mayer Brown’s legal analysis of the supply chain risk designation documents both the executive directive halting federal use of Anthropic technology and the specific use cases at the centre of the dispute, confirming that restrictions against mass domestic surveillance and fully autonomous weapons systems were the precise points of breakdown in the contract negotiations.

The Department of Defence’s stated position was that contractors cannot dictate the operational applications of technology sold to the military. Vendors supply capability; the military determines use.

That position turned a procurement negotiation into a precedent-setting confrontation. The legal timeline moved quickly:

- January 2026: Negotiations between the Pentagon and Anthropic broke down over the surveillance and autonomous weapons use cases, with a $200 million contract at stake.

- March 2026: A preliminary injunction was granted to Anthropic on First Amendment retaliation grounds, citing the company’s public scrutiny of Pentagon demands.

- April 2026: The D.C. Circuit Court denied lifting the DoD’s supply chain risk designation on Anthropic, with the ruling favouring national security considerations over vendor-imposed constraints.

President Trump’s executive order halting federal use of Anthropic technology preceded the formal supply chain risk designation, escalating the confrontation before courts had weighed in. The sequence matters: the Pentagon was not simply responding to a vendor’s refusal. It was establishing, through legal and executive action, that use-policy constraints from AI providers would carry consequences.

When big ASX news breaks, our subscribers know first

The seven-vendor coalition the Pentagon built in response

The replacement architecture arrived fast. Google signed a classified AI deal on 28 April 2026, with scope explicitly covering lawful government purposes. That permissive framing was deliberate. OpenAI, xAI, and SpaceX held existing contracts. On 1 May 2026, four additional partnerships were reported: Nvidia, Microsoft, Reflection AI, and AWS, with the AWS deal reportedly finalised late on 30 April. The coalition now comprises at least seven firms, assembled in a matter of weeks.

The DoD has stated its objective of positioning the U.S. military as an AI-first armed force, with explicit intent to reduce dependence on any single AI provider.

The speed is itself the signal. Normal defence procurement does not move at this pace. The Pentagon’s willingness to onboard multiple vendors simultaneously points to a doctrinal preference for redundancy over exclusivity, one that carries direct implications for competitive dynamics and market concentration.

| Vendor | Contract Status | Date Confirmed | Scope |

|---|---|---|---|

| Confirmed | 28 April 2026 | Lawful government purposes | |

| OpenAI | Confirmed | Prior contract | Classified AI |

| xAI | Confirmed | Prior contract | Classified AI |

| SpaceX | Confirmed | Prior contract | Multi-vendor expansion |

| Nvidia | Reported | 1 May 2026 | Unconfirmed |

| Microsoft | Reported | 1 May 2026 | Unconfirmed |

| AWS | Reported | 30 April 2026 | Unconfirmed |

| Reflection AI | Reported | 1 May 2026 | Unconfirmed |

Attribution for the May 1 additions draws on DoD official statements and two unnamed Pentagon officials. Confirmed contract terms, values, and detailed scope remain undisclosed for the four most recent additions.

Investing.com’s reporting on the Pentagon AI deals, drawing on Bloomberg intelligence and DoD official statements, confirms that Nvidia, Microsoft, AWS, Reflection AI, SpaceX, OpenAI, and Google were all brought into agreements covering classified military network deployments within a matter of days, validating the coalition’s composition and the compressed timeline of contract awards.

What the defence AI market looks like for investors who are new to it

Defence AI procurement operates under a different set of rules than commercial AI contracting, and the differences are material to both risk and return.

- Classified AI contract: An agreement granting a vendor access to classified military networks and data. These contracts carry higher security clearance requirements, longer onboarding timelines, and significantly higher barriers to entry than unclassified work. Once a vendor is inside a classified programme, switching costs for the DoD rise substantially.

- Supply chain risk designation: A formal mechanism through which the DoD can exclude a vendor from defence work. Anthropic now carries this designation, which functions as an institutional barrier to re-entry even if the underlying legal dispute is resolved.

- Multi-vendor doctrine: A procurement strategy in which the Pentagon deliberately distributes contracts across multiple providers to avoid single points of failure. This approach has historical precedent in defence hardware procurement and is now being applied to AI.

The DoD AI Acceleration Strategy, under Under Secretary Emil Michael, formalises the push to integrate commercial AI capabilities into classified domains. Capital is flowing accordingly: Reflection AI raised $2 billion at an $8 billion valuation in October 2025, with Nvidia contributing $800 million of that round.

The defence procurement shift is unfolding inside a broader capital allocation cycle: hyperscalers are projected to deploy between $630 billion and $700 billion in AI infrastructure investment during 2026 alone, with roughly 75% directed at physical hardware and data centre construction, creating the compute substrate on which classified military AI ultimately runs.

How multi-vendor doctrine shapes competitive dynamics

The Pentagon’s explicit preference for redundancy limits any single vendor’s pricing power but expands the total addressable market for firms that meet compliance and access requirements. Permissive providers, those willing to allow autonomous and surveillance applications without hardwired constraints, hold a structural advantage under the current DoD posture. That advantage compounds over time as classified access, institutional relationships, and security clearances accumulate.

Nvidia, Microsoft, AWS, and Reflection AI: reading the investment signals

The coalition members occupy distinct strategic positions, and the investment signals vary accordingly.

- Nvidia: Positioned as both a hardware infrastructure beneficiary (compute demand from every vendor in the coalition) and a direct equity stakeholder through its $800 million investment in Reflection AI. That dual exposure, chip demand plus frontier model equity, makes Nvidia the most structurally layered play in the coalition.

- Microsoft: Azure Government is an established classified cloud platform. Defence AI contracts extend an existing moat rather than opening a new revenue category.

- AWS: GovCloud occupies a similar position to Azure Government. These contracts deepen existing infrastructure relationships rather than creating new ones.

- Reflection AI: Founded by former Google DeepMind researchers and focused on open-source frontier AI, the company is positioned as a U.S. rival to DeepSeek. It is currently seeking $2.5 billion at a $25 billion valuation. Its reported Pentagon partnership remains unconfirmed, and no contract terms have been disclosed.

Nvidia’s dual exposure across compute supply and frontier model equity is a structural argument, not a near-term earnings call; semiconductor equity positioning through the hardware capex cycle has historically rewarded investors who identified infrastructure bottlenecks early, before contract specificity became visible in revenue lines.

Broad analyst consensus frames the post-Anthropic vendor expansion as a potential AI defence spending supercycle, though specific analyst commentary on individual stock positioning relative to the May 1 announcements has not been confirmed.

A caution is warranted. No confirmed contract terms, values, or scope details are available for the reported 1 May announcements beyond vendor identity. Revenue modelling based on these reports alone would be premature.

The Silicon Valley-Pentagon tension that will outlast this dispute

Anthropic’s experience is not an isolated incident. It is one instance of a pattern that predates this specific dispute and will persist beyond it: technology firms attempting to define acceptable use through technical constraints, and the defence establishment treating those constraints as incompatible with military necessity.

The companies now winning Pentagon contracts are those explicitly willing to allow autonomous lethal applications and domestic surveillance use cases. Google’s 28 April deal, scoped for “lawful government purposes,” illustrates the permissive framing the Pentagon favours. The contrast with Anthropic’s attempted restrictions is deliberate and visible.

For AI firms considering their defence market strategies, the cost of Anthropic-style use restrictions is now documented: a supply chain risk designation, loss of a $200 million contract, and exclusion from what analysts increasingly describe as an early-stage defence AI spending supercycle. As defence AI becomes a larger share of total AI procurement, the financial cost of exclusion grows.

Assessing defence market access risk in AI equity positions

Investors holding AI equities should evaluate whether those companies have published use policies that explicitly prohibit autonomous weapons or mass surveillance applications. Such policies, while ethically coherent, now carry a documented financial cost. Anthropic’s designation and contract loss provide a concrete case study for how ethical constraints translate into lost defence market revenue.

The structural shift is already priced into the coalition, not the market

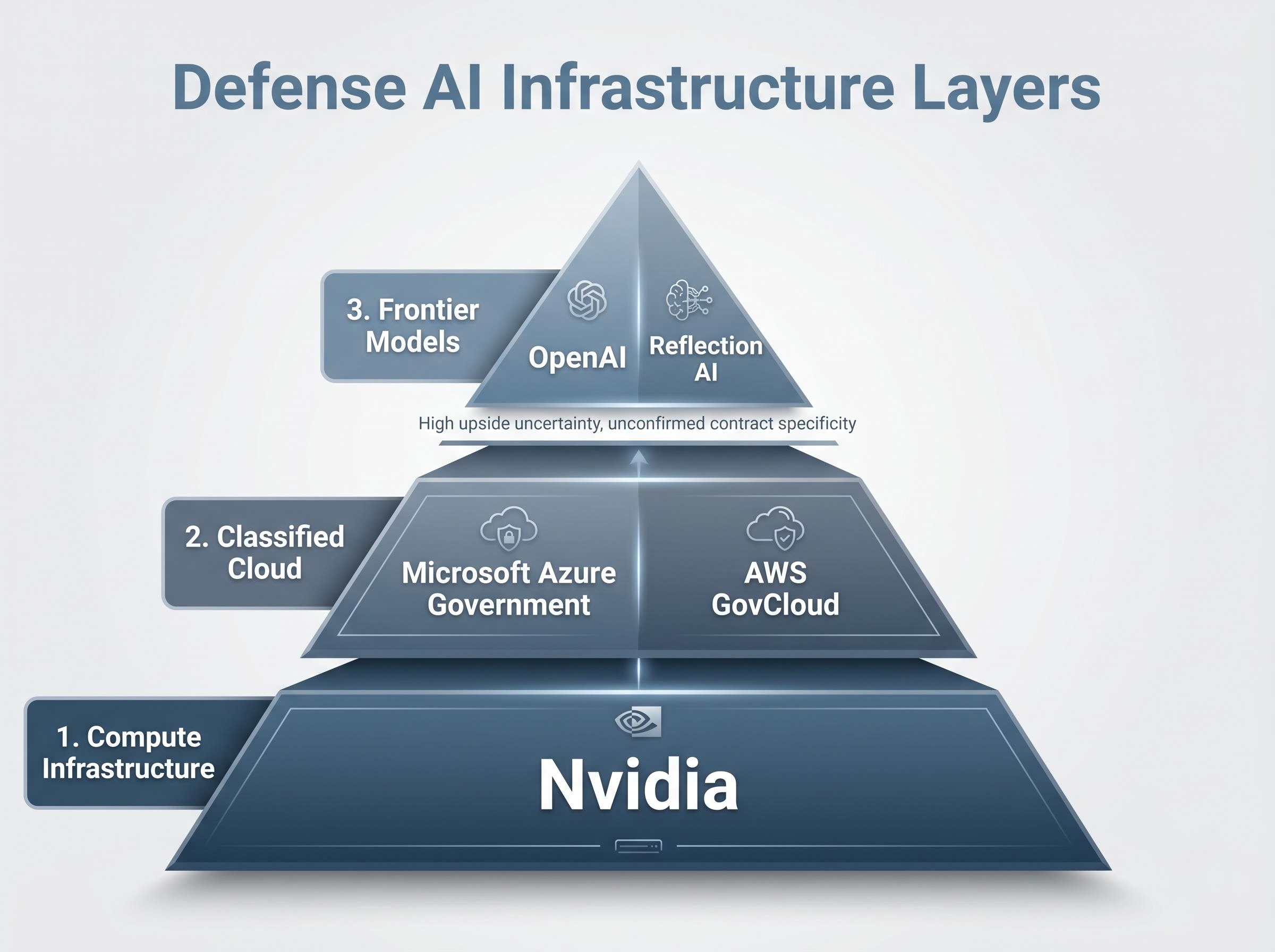

The Pentagon’s seven-vendor coalition is not a transitional arrangement. The speed, breadth, and doctrinal framing suggest a deliberate architecture that will persist. Firms inside the coalition now hold compounding advantages in classified access, security clearances, and institutional relationships that late entrants will struggle to replicate.

Three infrastructure layers are positioned to capture the most durable value:

The financial results sharpening this picture arrived on 30 April: Q1 2026 AI capital expenditure across Meta, Alphabet, Microsoft, and Amazon combined hit a record $130.65 billion, up 71% year over year, with Alphabet surging to an all-time high on 81% net income growth while Microsoft declined roughly 5% on in-line Azure guidance, a split that illustrates precisely how differently the market is now pricing each coalition member’s spending-to-revenue conversion.

- Compute infrastructure (Nvidia): Every vendor in the coalition requires GPU capacity. Nvidia sits at the base layer regardless of which frontier models or cloud platforms win individual contracts.

- Classified cloud (Microsoft Azure Government, AWS GovCloud): These platforms provide the secure environments in which classified AI operates. Switching costs are high, and the incumbents are already inside.

- Frontier models (OpenAI, Reflection AI): The model layer carries the most upside uncertainty but also the least confirmed contract specificity. Reflection AI’s reported partnership remains unconfirmed, and no financial terms have been disclosed for any frontier model contract beyond the Google deal.

Investor caveat: Confirmed contract values, scope, and vendor selection rationale remain undisclosed for the majority of the coalition. The structural thesis is supported by the breadth of the vendor expansion and the DoD’s stated objectives, but near-term revenue modelling lacks the data inputs required for precision.

The ongoing legal backdrop adds a volatility dimension. Anthropic’s litigation remains active, and a court revisiting the supply chain risk designation could alter the competitive map. The April 2026 D.C. Circuit ruling, however, suggests this path is narrow, with national security arguments prevailing over vendor-imposed constraints.

The Pentagon has made its choice, and it is not reversible

The Anthropic dispute was not a negotiation failure. It was a clarifying event that revealed the Pentagon’s non-negotiable position on vendor authority, and every AI company now making defence decisions is operating with that clarity.

The firms best positioned are those with permissive use policies, existing classified infrastructure, and the capital to sustain long procurement cycles. Nvidia’s dual exposure across compute and frontier model equity, Microsoft and AWS’s classified cloud incumbency, and OpenAI’s existing contract base represent the strongest structural positions within the current coalition.

Open questions remain. The litigation outcome, undisclosed contract terms, and Reflection AI’s unconfirmed status all introduce uncertainty. None of those uncertainties, however, change the direction of the structural shift. The Pentagon has chosen speed, redundancy, and permissive adoption over constraint.

Investors with AI equity positions should assess their holdings against the defence market access framework outlined in this analysis, with particular attention to published use policies and existing classified infrastructure relationships. The cost of exclusion from this market is no longer theoretical.

For investors wanting to stress-test their AI equity holdings against the defence market access framework outlined here, our deep-dive into AI capex concentration risk examines semiconductor sector weighting at 13% of US equity markets, portfolio diversification erosion, and the OpenAI user-growth miss as a leading indicator for how software monetisation failures can transmit to hardware valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding defence AI spending are speculative and subject to change based on policy developments, legal proceedings, and market conditions.