Goldman Warns CPI Print Could Reprice an Overvalued Market

2 hrs ago

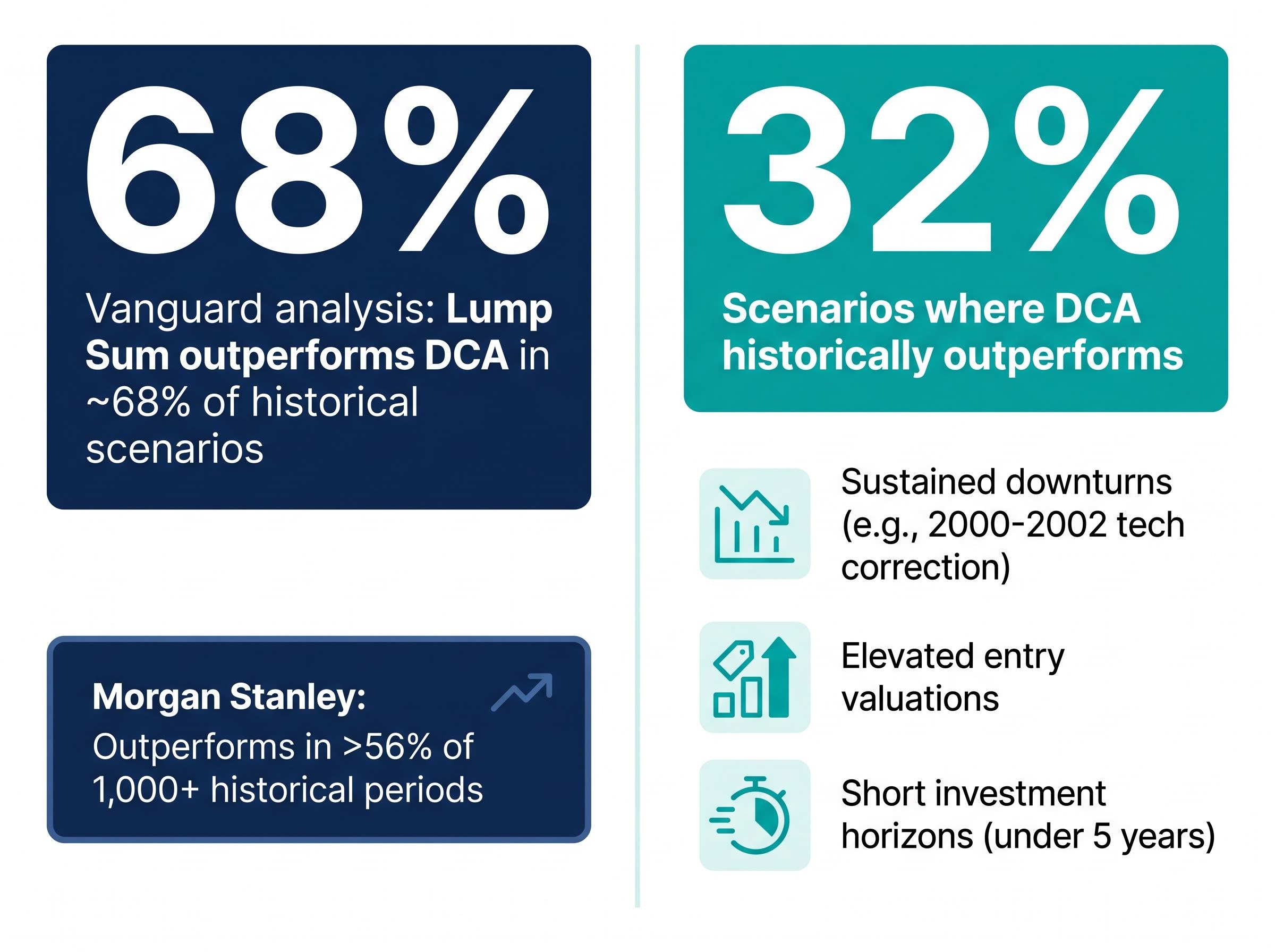

Vanguard’s research across Australian, US, and UK markets found that lump sum investing outperforms dollar cost averaging in roughly 68% of historical scenarios. Yet millions of Australian investors choose DCA anyway, and many of them are making the right call.

With the ASX 200 sitting around 8,622 points in late April 2026 and retail investors increasingly adopting automated, systematic investing strategies, the question of how to deploy capital has become more practically urgent than ever. A $50,000 inheritance, a property sale windfall, or years of accumulated savings all force the same decision: all in now, or spread it out?

This guide explains how both dollar cost averaging and lump sum investing work, what the historical data actually shows, why the data does not tell the whole story, and how Australian investors can match the right approach to their own financial situation, risk tolerance, and behavioural profile.

Before weighing performance data or behavioural arguments, it is worth establishing exactly what each strategy does. The mechanical difference is simple. The decision it produces is not.

Both approaches can be applied to the same underlying assets, whether that is an ASX 200 ETF, a diversified global portfolio, or a single sector fund. The comparison is purely about timing and deployment method, not asset selection.

DCA involves deploying a fixed dollar amount at regular intervals regardless of price. An investor contributing $1,000 on the first day of each calendar month into an ASX 200 ETF will buy more units when the price falls and fewer units when it rises. Over time, this produces a weighted average entry price that smooths out short-term volatility.

Automation makes DCA a systematic habit rather than an active decision. Platforms such as Betashares Direct offer an Auto Invest feature allowing automated periodic contributions into up to 5 Betashares ETFs with zero brokerage, removing the friction of manual monthly purchases.

Lump sum investing deploys all available capital in a single transaction. A $50,000 windfall invested directly into a diversified ETF portfolio means the full amount begins compounding from day one, with no portion sitting idle in cash.

For superannuation, lump sum contributions can also be made as non-concessional contributions within ATO limits, then allocated to growth assets within the fund.

The table below summarises the structural differences:

| Attribute | Dollar cost averaging | Lump sum |

|---|---|---|

| Contribution method | Fixed amount at regular intervals | Full amount in one transaction |

| Market exposure timing | Gradual, over months | Immediate, from day one |

| Unit price averaging | Yes, smooths entry price | No, single entry point |

| Automation availability | Widely supported on Australian platforms | Single manual transaction |

The performance evidence is directionally clear, and it favours lump sum. The question is how much weight to place on that evidence given the scenarios where it does not hold.

Vanguard’s historical analysis across Australian, US, and UK markets found that lump sum investing outperforms dollar cost averaging approximately 68% of the time.

That figure has become the most cited data point in this debate, and it holds up under scrutiny. Morgan Stanley’s analysis, covering more than 1,000 historical periods, found lump sum holds an edge in more than 56% of scenarios. A 2026 Betashares analysis confirmed the same directional finding: lump sum outperforms in rising markets due to longer market exposure.

Vanguard’s lump sum versus DCA research examined historical return sequences across Australian, US, and UK markets and found the performance edge for immediate deployment holds consistently across all three geographies, driven by the simple fact that equity markets spend more time rising than falling over multi-year periods.

The mechanism is straightforward. Equity markets rise more often than they fall over meaningful time horizons. Deploying capital earlier captures more of that upward drift. Every month that a portion of capital sits in cash waiting for its next scheduled deployment is a month that portion is not compounding.

Long-term compounding in equity markets has produced approximately 9.43% annually across 150 years of S&P 500 data with dividends reinvested, which is why the central argument for lump sum investing rests not on predicting near-term direction but on capturing as much of that upward drift as possible from the earliest date.

That leaves the other 32% of historical scenarios. DCA has historically outperformed lump sum under three specific conditions:

The data makes a strong case for lump sum as the statistically superior strategy. It does not make the case that lump sum is the right strategy for every investor.

A theoretically optimal strategy that an investor cannot psychologically sustain is not actually optimal for that investor. The performance data assumes the investor stays fully invested through every drawdown, and that assumption breaks down more often than the models suggest.

Behavioural research consistently finds that losses register approximately twice as intensely as equivalent gains, a phenomenon known as loss aversion.

This asymmetry matters because a lump sum deployment followed by a 15-20% correction does not just reduce portfolio value; it triggers a disproportionate emotional response. The investor who deploys $50,000 on a Monday and watches it become $42,500 by Friday is not weighing long-term compounding probabilities. They are experiencing regret at twice the intensity they would experience satisfaction from an equivalent gain.

Kahneman and Tversky’s loss aversion findings, which form the foundation of prospect theory, established that the psychological pain of a financial loss is roughly twice the intensity of pleasure from an equivalent gain, a ratio that holds across a wide range of experimental and real-world settings.

Market timing anxiety compounds the problem. The reluctance to invest at what might be a market peak leads many investors to defer deployment indefinitely, waiting for a correction that may not arrive for years. Research consistently shows this indefinite deferral is the worst outcome of all, worse than either DCA or lump sum.

DCA resolves both problems. It allows investors to act without requiring conviction about market direction at a specific moment. The following three scenarios describe where DCA is the functionally superior choice, even if it is not the statistically optimal one:

Event-driven trading patterns among Australian retail investors are well-documented in 2026 platform data, with volumes on major platforms doubling during the April 2025 US tariff announcement and falling sharply after the March 2026 RBA rate decision, a pattern that illustrates precisely the behavioural vulnerability that DCA is designed to neutralise.

According to Hudson Financial Planning’s 2026 analysis, lump sum delivers higher average returns over long periods, but DCA reduces emotional and behavioural risk for investors who struggle to deploy large sums at once. The distinction is between average outcomes and individual outcomes, and most investors are individuals.

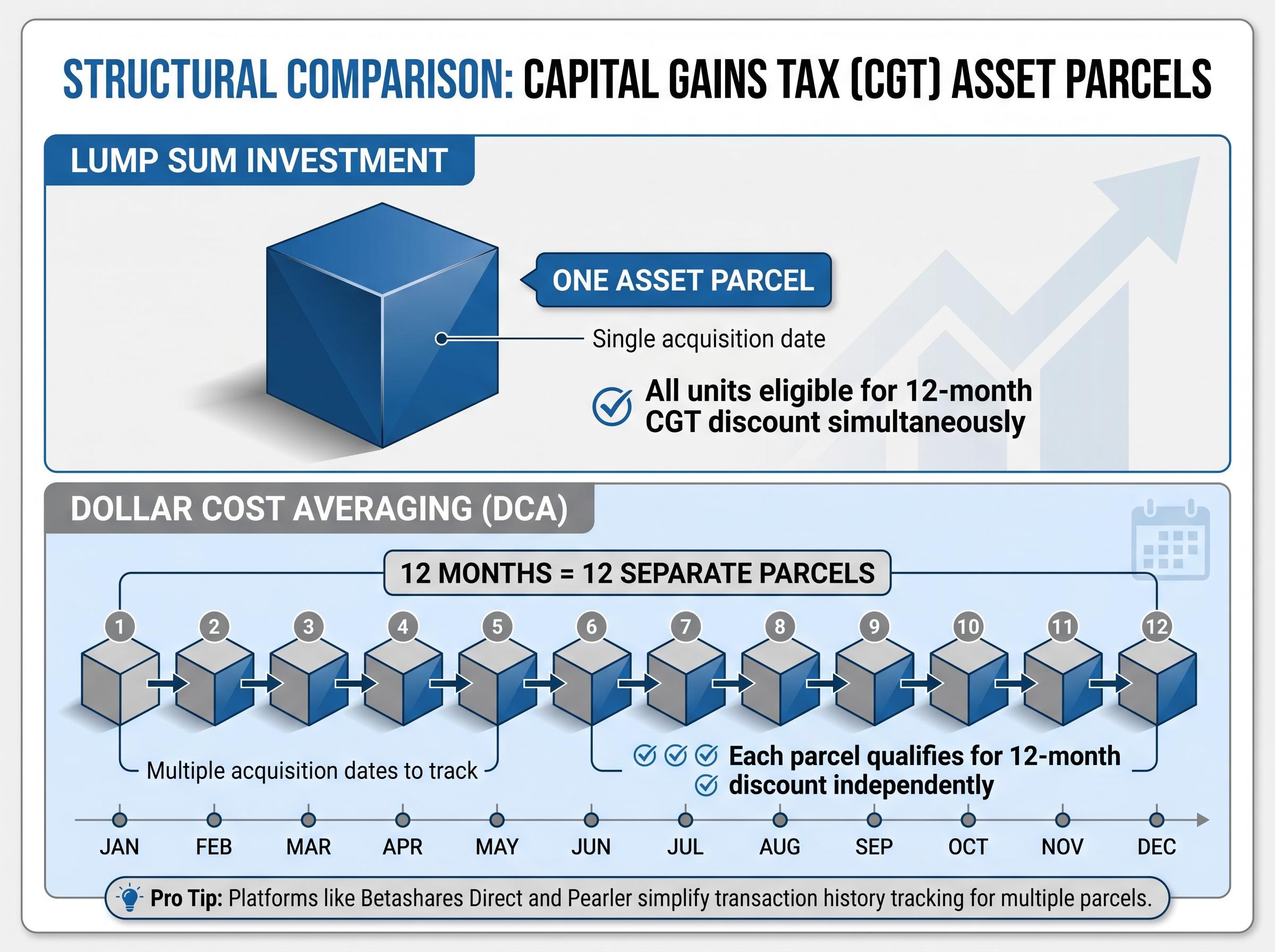

One dimension that most comparison articles overlook is the tax treatment of each approach under Australian rules. Both strategies face identical capital gains tax (CGT) rates under ATO rules, so neither carries a tax rate advantage. The structural difference lies in how each strategy creates asset parcels.

A lump sum investment produces one asset parcel with one acquisition date and one cost base. A DCA approach produces multiple parcels, each with its own cost base and its own holding period. An investor contributing monthly into an ETF over 12 months will accumulate 12 separate parcels.

This distinction matters at the point of sale. Multiple parcels provide strategic flexibility: an investor can choose which specific parcels to sell, potentially realising lower-gain or higher-cost-base parcels first to manage CGT outcomes in a given financial year. Each parcel independently qualifies for the 12-month CGT discount once held for at least a year.

The trade-off is record-keeping complexity. Platforms such as Betashares Direct and Pearler often generate downloadable transaction histories that simplify cost base tracking for DCA investors, but the administrative burden remains higher than a single-parcel lump sum approach.

The reactive trading costs that accumulate when investors override systematic strategies are not limited to missed compounding; Australian CGT rules add a structural tax penalty, with investors who sell within 12 months forfeiting the 50% CGT discount and paying full marginal rates on any realised gain, a consequence that compounds the behavioural drag beyond what US-focused studies typically capture.

| CGT attribute | Lump sum | Dollar cost averaging |

|---|---|---|

| Number of parcels | One | Multiple (one per contribution) |

| Acquisition date complexity | Single date | Multiple dates to track |

| CGT discount eligibility timing | All units eligible after 12 months | Each parcel eligible 12 months after its own purchase date |

The evidence, the behavioural research, and the tax considerations all point toward the same conclusion: the right strategy depends on the investor, not the market. What follows is a framework for matching circumstances to approach.

Lump sum investing aligns with investors who meet most of the following criteria:

DCA aligns with investors who recognise any of the following in their own profile:

Systematic investing strategies that combine dollar-cost averaging into diversified index products with automated platform execution have attracted $6.9 billion in global equity ETF inflows among Australian investors in Q1 2026 alone, a figure that reflects growing recognition that removing human timing decisions from the process produces more consistent participation across market cycles.

A hybrid approach deploys a portion of available capital immediately and spreads the remainder over a defined window. This is not a compromise; it is a legitimate primary strategy that balances the mathematical case for lump sum against the psychological benefits of gradual entry.

Every reviewed source, from Vanguard to Morningstar Australia to Hudson Financial Planning, converges on one point: both DCA and lump sum are preferable to remaining in cash. The opportunity cost of waiting for a better entry point consistently exceeds the risk of a suboptimal one.

The most important insight from the data is not that lump sum wins 68% of the time. It is that both strategies outperform the alternative most investors actually default to: doing nothing.

Every day capital sits in cash is a day it is not compounding. Indefinitely delaying investment while searching for the perfect entry point or the optimal deployment strategy is, historically, the worst outcome of all. Lump sum wins more often statistically. DCA wins for behavioural sustainability. The hybrid approach resolves the tension for most investors. All three beat hesitation.

The practical next step is a three-part sequence:

The debate between dollar cost averaging and lump sum investing is worth understanding. It is not worth waiting on.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

—

Dollar cost averaging (DCA) is an investment strategy where you invest a fixed dollar amount at regular intervals regardless of market price, buying more units when prices are low and fewer when prices are high, which smooths out your average entry price over time.

Vanguard's research across Australian, US, and UK markets found lump sum investing outperforms dollar cost averaging in approximately 68% of historical scenarios, primarily because equity markets spend more time rising than falling, rewarding earlier full deployment.

DCA tends to be the better practical choice for investors who are sensitive to short-term volatility, are deploying a large sum for the first time, or have a history of panic selling during drawdowns, as it reduces the emotional risk of a poorly timed single entry.

Each DCA contribution creates a separate asset parcel with its own cost base and acquisition date, giving investors the flexibility to choose which parcels to sell in order to manage CGT outcomes, with each parcel independently qualifying for the 50% CGT discount after 12 months.

A hybrid approach invests a portion of capital immediately as a lump sum and spreads the remainder over a defined period, typically 3-6 months; Vanguard and Betashares both cite this as a widely recommended middle ground that balances the mathematical case for lump sum against the psychological benefits of gradual entry.