Imugene Posts 81% Response Rate and Lands Two FDA Fast Track Tags

1 hr ago

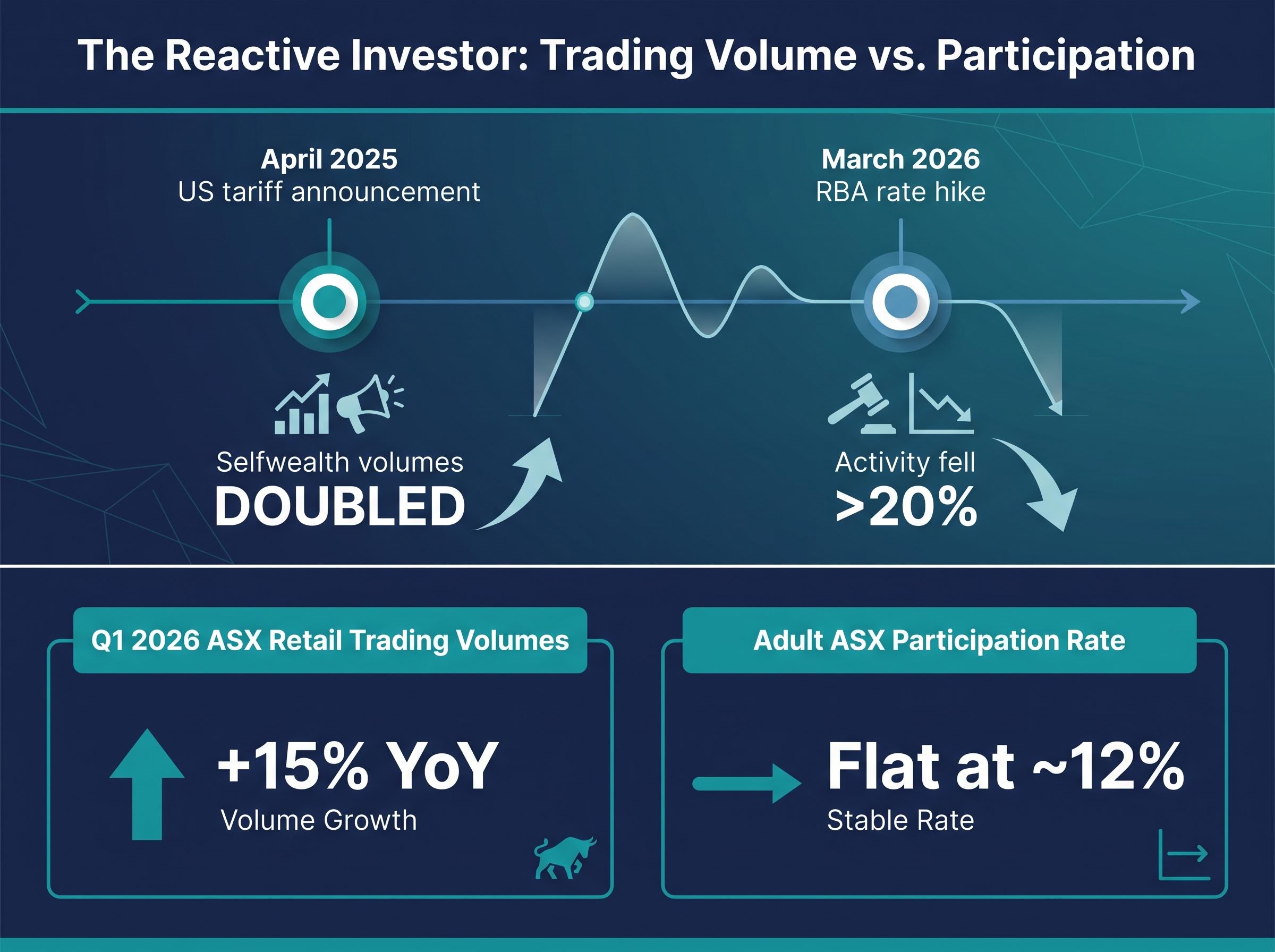

Trading volumes on the Selfwealth by Syfe platform doubled in a single week when the US tariff announcement landed in April 2025. That is not a sign of informed conviction. It is a signal of mass reactivity, and new Q1 2026 data shows the pattern has not reversed. Australian retail investors are trading more actively than at any point in recent memory, yet ASX participation rates have held flat at roughly 12% of adults. The volume surge is coming from existing investors trading more often, not from a wave of new entrants. Against a backdrop of elevated interest rates, persistent inflation, and geopolitical shocks, the speed at which market-moving news is now priced into behaviour has created both an efficiency gain and a new category of risk. This analysis unpacks what the latest platform data reveals about reactive investing among Australian retail investors, why the gold demand cycle offers the clearest case study of sentiment-driven behaviour in recent months, and what disciplined investors can do differently.

ASX data shows overall retail trading volumes rose 15% year-over-year in Q1 2026, with spikes concentrated around macroeconomic events. On the surface, that looks like growing market engagement. The participation rate tells a different story: it held stable at approximately 12% of Australian adults, meaning the surge is not evidence of a broader democratisation of investing. It is the same cohort trading faster.

The behavioural pattern sharpens when platform-level data fills in the detail:

Selfwealth Q1 2026 Investor Pulse: Trading volumes on the platform doubled during the April 2025 US tariff announcement, the sharpest single-event spike recorded in the platform’s recent history.

The volume doubling during the tariff announcement, followed by a 20% drop after the RBA rate hike, traces the outline of a reactive investor base that surges on fear and retreats on disappointment. The problem is not that more Australians are in the market. The problem is that those already in it are becoming more reactive to headlines.

Markets have always priced in new information, but the speed at which that pricing now occurs has changed structurally. Digital platforms, algorithmic trading systems, and real-time financial information access have compressed a process that once took days or weeks into hours or minutes. Selfwealth’s Q1 2026 analysis observed that macroeconomic events now drive near-immediate price incorporation, closing arbitrage windows and reducing persistent mispricings.

The structural basis for instant retail reaction to macro events lies partly in the algorithmic recalibration that now propagates through platforms within minutes of a policy announcement, creating a feedback loop where retail sentiment and price movement reinforce each other before any fundamental analysis has occurred.

For long-term market quality, this is a genuine improvement. Prices that reflect available information faster produce more efficient capital allocation and reduce the windows in which institutional information advantages distort outcomes.

The same speed that improves efficiency shortens the decision window for retail investors. When a tariff announcement or rate decision moves prices within minutes, the pressure to act arrives before the analysis does.

The consequences split in two directions:

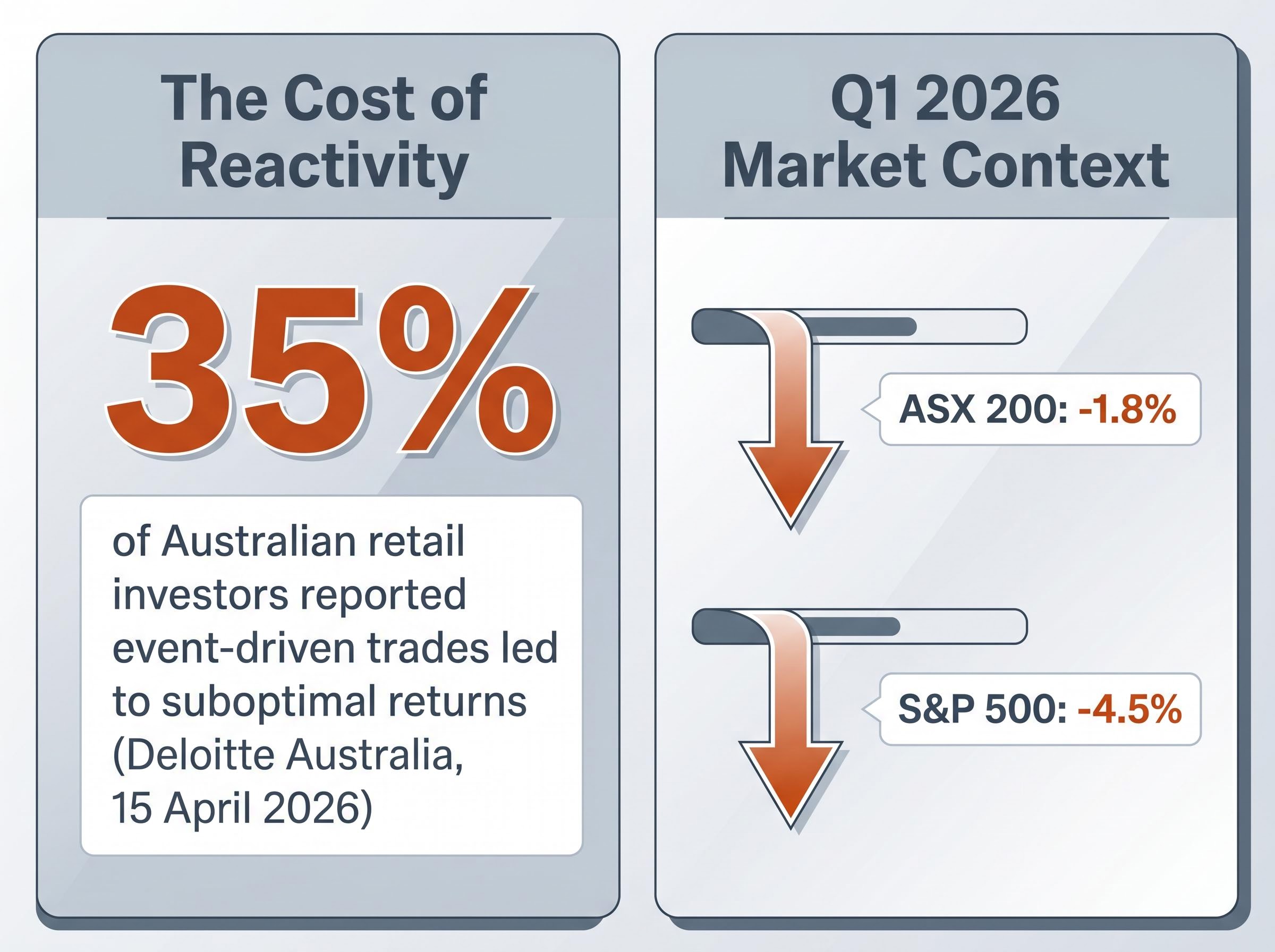

According to a Deloitte Australia report published 15 April 2026, 35% of Australian retail investors reported that event-driven trades led to suboptimal returns. The researchers identified the recency effect, a cognitive bias where recent dramatic events are overweighted relative to longer-term fundamentals, as a primary driver of reactive decisions during periods of macro volatility. The mechanism is not that faster markets are bad. The mechanism is that faster markets demand more discipline from the participants inside them.

Gold’s demand trajectory across late 2025 and into Q1 2026 offers the clearest illustration of how sentiment drives capital in and out of an asset class. The pattern is concrete, data-grounded, and familiar to anyone who has watched a safe-haven trade build and unwind.

In late 2025, elevated geopolitical uncertainty and persistent high interest rates pushed investors toward defensive positioning. Gold buying surged as the preferred expression of that caution. By Q1 2026, investor confidence had partially returned, and the appetite shifted. Gold buying activity fell below 70% of total gold-related trades on the Selfwealth platform, with capital rotating toward financial sector stocks and growth-focused assets.

According to Selfwealth’s Q1 2026 data, gold buying activity fell below 70% of total gold-related trades on the platform, marking a measurable cooling from the late-2025 surge.

| Period | Market environment | Investor sentiment signal | Platform behaviour observed |

|---|---|---|---|

| Late 2025 | Elevated geopolitical uncertainty; high interest rates | Defensive positioning; risk aversion | Gold buying surged as dominant trade |

| Q1 2026 | Partial confidence recovery; diversification shift | Cautious optimism; rotation toward growth | Gold buying fell below 70% of gold-related trades |

Gold’s demand cycle functions as a mirror of collective sentiment. When investors rush in at peak fear and rotate out as conditions stabilise, they demonstrate the buy-high-sell-low dynamic that headline-driven trading produces. The asset itself is not the issue. The timing of the entries and exits is.

Sovereign and central bank gold demand adds a structural layer beneath the retail sentiment cycle: while Australian platform investors were rotating out of gold in Q1 2026, central banks were projecting 850 tonnes of accumulation for the full year, a divergence that illustrates how the same asset can simultaneously serve as a retail fear gauge and a long-term institutional reserve instrument.

World Gold Council Q1 2026 demand data recorded global bar and coin demand rising 42% year-on-year to 474 tonnes, confirming that the retail safe-haven surge observed on Australian platforms was part of a broader international pattern rather than a localised response to domestic conditions.

Not all Q1 2026 activity was impulsive. International ETFs overtook domestic funds as the most purchased ETF category on the Selfwealth platform, a structural shift rather than a one-off event. This represents the more considered response to the same macroeconomic environment that drove the reactive trading documented above.

The generational data on ETF adoption reinforces this. Platform-based investing has converged across cohorts around a similar core strategy, challenging the assumption that younger investors are inherently more erratic.

| Generation | Approximate ETF allocation | Individual stock allocation | Notable characteristic |

|---|---|---|---|

| Gen Z | ~50% | ~50% | Mirrors Gen X split between ETFs and stocks |

| Millennials | ~70% | ~30% | Heaviest ETF weighting across all cohorts |

| Gen X | ~50% | ~50% | Balanced allocation; similar profile to Gen Z |

| Baby Boomers | Progressively adding | Majority | Remain more stock-focused but increasing ETF exposure |

Several contextual factors are driving broader ETF adoption across these cohorts:

The cross-generational convergence toward ETF-heavy, geographically diversified portfolios suggests a maturing retail investor base. The move away from home-market concentration also reduces the specific risk of overexposure to ASX-correlated sectors like iron ore and financials.

The structural case against ASX home bias is reinforced by the sector composition of the index itself: an investor holding a market-weighted Australian portfolio carries outsized exposure to iron ore prices and the major banks, two inputs that respond to Chinese demand cycles and RBA policy rather than to the global technology and healthcare growth themes dominating international ETF inflows.

Deloitte Australia, April 2026: 35% of Australian retail investors reported that event-driven trades led to suboptimal returns, with the recency effect identified as a primary cognitive bias amplifying reactive decisions during macro volatility.

That figure is not an abstract warning. It represents more than one in three retail investors making decisions they themselves later identified as suboptimal. The cost of reactivity is measurable, and it compounds through three specific mechanisms:

Selfwealth’s Q1 2026 analysis corroborates this pattern, finding that overtrading erodes returns and creates anxiety-driven portfolio disruption. The broader market context adds perspective: the ASX 200 declined 1.8% in Q1 2026, but this represented relative outperformance compared to the S&P 500, which fell 4.5% over the same period. Investors who sold Australian holdings in reaction to global headlines may have exited the comparatively stronger market.

Dollar-cost averaging removes the timing decision that headline-driven behaviour exploits. By investing a fixed amount at regular intervals, regardless of market conditions, the strategy automates the discipline that reactive environments erode. The Selfwealth platform’s auto-invest feature supports daily, weekly, biweekly, or monthly recurring purchases of existing holdings, institutionalising this approach without requiring manual execution during volatile news cycles.

Vanguard’s dollar-cost averaging research compared DCA against lump-sum investing across multiple markets and historical periods, finding that while lump-sum investing outperforms in rising markets on average, DCA delivers its clearest advantage in volatile, event-driven environments where timing risk is highest, precisely the conditions Australian retail investors faced through the April 2025 tariff shock and the subsequent RBA-driven period.

When the next tariff announcement or rate decision arrives, a scheduled purchase proceeds on its predetermined date. The urgency to act dissolves because the action has already been decided.

For investors wanting to move from the principle to the mechanics, our dedicated guide to dollar-cost averaging covers the specific implementation steps for Australian platforms, the record-keeping requirements for CGT compliance across automated purchase schedules, and the mathematical effect of fixed-amount investing on average entry costs over a full market cycle.

The Q1 2026 shift toward international ETFs demonstrates that a substantial cohort of Australian investors is already moving in this direction. Diversification across asset classes, sectors, and geographies reduces the portfolio’s sensitivity to any single headline, whether it originates from the RBA, Washington, or commodity markets. In an ASX context shaped by iron ore and financial sector cycles, reducing home-market concentration is a structural risk-reduction measure.

A disciplined investor framework, grounded in the Q1 2026 data, follows three steps:

Selfwealth’s Q1 2026 Investor Pulse offers a direct recommendation on this point: focus on fundamentals over short-term reactions. The investors building more defensible portfolios are not ignoring the news. They are refusing to let the news make their decisions for them.

The data assembles into a single clear conclusion. Australian retail investors are more engaged than at any point in recent memory. Markets are faster, information is more accessible, and platforms have reduced the friction between a headline and a trade to near zero. None of that is producing better outcomes unless it is anchored to a durable framework.

Selfwealth, “Five Themes Defining Markets in 2026” (March 2026): Late-2025 resilience is transitioning to a more turbulent 2026 phase, with geopolitical and technological shocks widening winner-loser gaps across asset classes.

The cross-generational convergence around ETF-heavy, geographically diversified portfolios is the data signal that a maturing cohort exists within the Australian retail investor base. That cohort treated the gold surge, the tariff shock, and the RBA rate hike as context to understand rather than instructions to act on. The distinction between those two responses is the practical takeaway the Q1 2026 data supports, and it is the distinction that will separate portfolio outcomes as ongoing geopolitical tensions, inflation concerns, and high interest rates persist through the remainder of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Reactive investing occurs when investors make buy or sell decisions based on news headlines or emotional urgency rather than fundamental analysis. For Australian retail investors, this pattern has been linked to suboptimal returns, with a Deloitte Australia report from April 2026 finding that 35% of retail investors identified event-driven trades as leading to worse outcomes.

The US tariff announcement in April 2025 triggered a fear-driven surge in activity on platforms like Selfwealth by Syfe, where trading volumes doubled in a single week. This spike reflects the recency effect, a cognitive bias where dramatic recent events are overweighted relative to longer-term fundamentals, causing investors to act before completing any considered analysis.

Dollar-cost averaging involves investing a fixed amount at regular intervals regardless of market conditions, which removes the timing decision that reactive behaviour exploits. Platforms like Selfwealth support automated recurring purchases on daily, weekly, biweekly, or monthly schedules, so a scheduled buy proceeds on its predetermined date even when a tariff announcement or rate decision creates pressure to act immediately.

In late 2025, elevated geopolitical uncertainty drove a surge in gold buying among Australian retail investors as a defensive trade. By Q1 2026, partial confidence recovery prompted a rotation away from gold, with buying activity falling below 70% of total gold-related trades on the Selfwealth platform, illustrating a classic sentiment-driven buy-high-sell-low cycle.

Platform data from Q1 2026 challenges this assumption, showing that ETF allocation strategies have converged across generations. Millennials held the heaviest ETF weighting at around 70%, while Gen Z and Gen X both split allocations roughly 50-50 between ETFs and individual stocks, suggesting younger investors are not inherently more erratic than older cohorts.