Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

An Australian investor sits on $50,000 from an inheritance, a property settlement, or a redundancy payout. The brokerage account is open. The money is cleared. And the cursor hovers between “invest all” and “set up a recurring purchase.” It is one of the most common decisions in personal investing, and one of the most emotionally charged.

In April 2026, the question carries particular weight. The ASX 200 has traded through a volatile first half of the year, the Reserve Bank of Australia has hiked rates twice in Q1 2026, and a further increase remains the market’s base case. More Australians than ever have access to automated investing platforms that make both strategies mechanically simple. What remains difficult is choosing between them.

This guide provides a structured, step-by-step framework for assessing which approach fits a reader’s individual circumstances. It covers risk tolerance, investment horizon, capital gains tax implications, superannuation contribution options, and a hybrid path for investors who find neither pure strategy convincing. By the end, the reader will hold a personal answer rather than a list of considerations.

Dollar-cost averaging (DCA) involves committing a fixed dollar amount at consistent intervals, regardless of market price. An investor directing $1,000 on the first of each month into an ASX 200 ETF, for example, purchases more units when prices are low and fewer when prices are high, producing an averaged entry cost across multiple transactions. According to Betashares senior investment strategist Cameron Gleeson, writing in March 2026, this approach can be fully automated through platform features such as Betashares Direct Auto Invest, which offers zero brokerage on recurring purchases of up to five Betashares ETFs.

Lump sum investing deploys all available capital in a single transaction. A $50,000 windfall directed into a diversified ETF portfolio on one day means the full amount is exposed to market movements from that point forward.

The mechanical difference is a trade-off, not a right-versus-wrong choice. Lump sum maximises time in market. DCA averages the entry price. Each is a deliberate bet on a different variable.

| Attribute | DCA | Lump sum |

|---|---|---|

| Capital deployment timing | Staged across weeks or months | Immediate, single transaction |

| Entry price | Averaged across multiple purchase dates | Single price point on deployment date |

| Cash holding period | Extended; uninvested cash held between tranches | None; full capital deployed from day one |

| Automation potential | High; platforms enable recurring scheduled purchases | Low; single manual decision |

| Complexity | Multiple parcels require ongoing record-keeping | One parcel, one cost base |

Understanding that DCA is a deliberate deployment strategy, not a reflection of limited capital, prevents the rest of this framework from being misapplied.

The DCA mechanics for ASX investors carry nuances that the global research does not fully capture, particularly around how the 50% CGT discount interacts with multiple purchase parcels held across different tax years and the specific ETF structures available on Australian platforms.

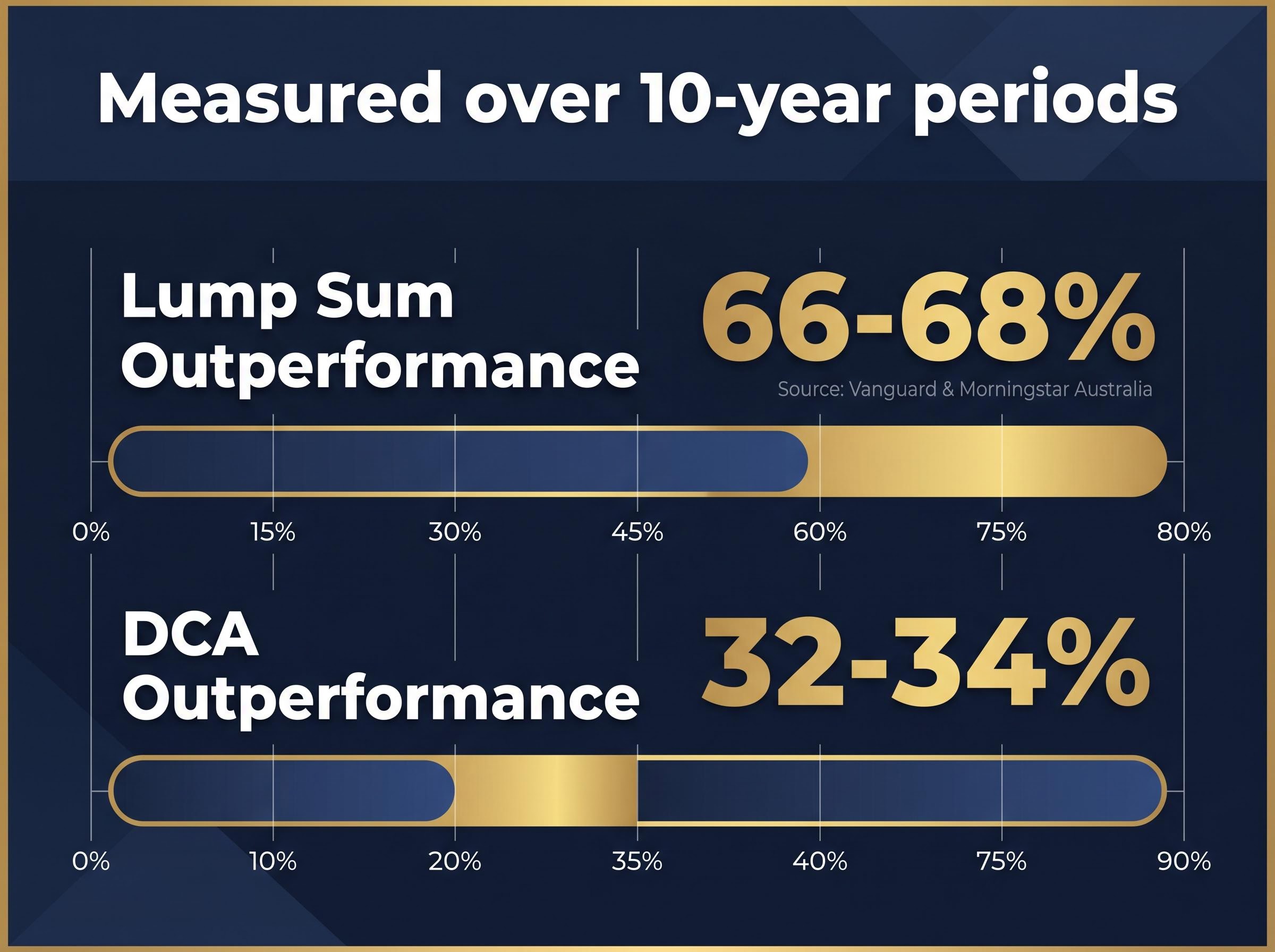

The headline finding is clear. Lump sum investing has historically outperformed DCA in approximately 66-68% of scenarios over 10-year periods, according to Vanguard’s research paper “Cost Averaging: Invest Now or Temporarily Hold Your Cash?” and corroborated by Morningstar Australia analyses published in August 2024 and updated in February 2026.

Lump sum investing outperforms DCA approximately 66-68% of the time across equity markets, a finding consistent in both US and Australian market contexts (Vanguard; Morningstar Australia).

The mathematical reasoning is straightforward. Equity markets trend upward over long periods. Capital deployed earlier participates in more of that growth. A February 2026 report from Hudson Financial Planning confirmed stronger long-term lump sum results in the Australian context specifically.

That still leaves 32-34% of historical periods where DCA delivered the better outcome. Those periods share recognisable characteristics:

Staying invested through volatility is not a passive default but an active performance decision: Australian superannuation members who switched to cash during the March 2026 ASX decline locked in losses and then missed a 1.1% single-session recovery, a sequence that illustrates exactly why the choice to hold is as consequential as the choice of how to deploy capital in the first place.

The 2026 Australian market environment carries several of those characteristics simultaneously. The ASX 200 dropped 0.34% to 8,948 on 16 April 2026, part of broader Q1-Q2 2026 volatility driven by macroeconomic and geopolitical pressures. The RBA implemented two rate hikes in February and March 2026, and as of mid-April, ASX 30 Day Interbank Cash Rate Futures implied a 74% probability of a further increase.

The ASX RBA Rate Tracker derives implied rate change probabilities from 30 Day Interbank Cash Rate Futures, providing a live market-based reading of where institutional participants expect the cash rate to move, which is the data source underlying the 74% further-hike probability cited for mid-April 2026.

Rising rates create a genuine tension for the DCA decision. On one hand, rate-driven equity volatility strengthens the case for staged entry. On the other, higher cash rates increase the opportunity cost of holding uninvested funds during a DCA deployment window. Neither factor resolves the question alone, which is why the personal assessment in subsequent sections carries more weight than the historical averages.

Lump sum investing’s statistical edge depends on the investor staying invested. If a 20% drawdown in month one triggers a panic sale, the theoretical advantage disappears entirely. Psychological sustainability is not a soft consideration; it is a genuine performance variable.

The DCA versus lump sum choice activates several well-documented behavioural barriers:

The correct framing is not “which strategy maximises expected returns” but “which strategy maximises the probability of staying invested through a full market cycle.” As Gleeson put it, a sub-optimal strategy executed consistently outperforms an optimal strategy that is never initiated or abandoned after the first drawdown.

That reframing does not make DCA the default answer. It makes honest self-assessment a required step before choosing.

Australian investors operate within a tax and superannuation system that materially alters the DCA versus lump sum comparison. Three factors deserve specific attention.

CGT parcel tracking is the first. A lump sum purchase creates one parcel with one cost base and one acquisition date. A 12-month DCA programme creates 12 separate parcels, each requiring individual record-keeping. The additional complexity is manageable through platform tracking tools or tax software, and it carries a strategic advantage at disposal. The ATO recognises three parcel identification methods:

DCA investors who maintain accurate records can use specific identification or the minimisation method to manage their CGT position with precision that a single lump sum parcel does not allow.

Franking credits create a lump sum advantage for investors targeting Australian dividend-paying shares or ETFs. Earlier full deployment captures franking credit entitlements sooner. In high-yield domestic equity contexts, this income advantage amplifies the time-in-market argument for lump sum.

The ATO contributions caps guidance confirms the non-concessional cap at $120,000 for 2025-26 and outlines bring-forward arrangement eligibility, which directly shapes how much of a windfall can be directed into superannuation in a single financial year without incurring excess contributions tax.

Australia’s superannuation system embeds compulsory DCA into the financial life of virtually every working Australian. Employer Superannuation Guarantee Contribution (SGC) payments, currently 11.5% and rising to 12% from 1 July 2025, are made per payroll cycle. Most Australians are already practising DCA inside super, whether they frame it that way or not.

The strategic question, then, is primarily about voluntary contributions and non-super investment decisions. An investor with a $50,000 windfall faces a choice: deploy into a taxable brokerage account with no contribution cap, or direct some or all into superannuation as a non-concessional contribution, subject to ATO annual and bring-forward caps. The super option offers a concessional tax environment but locks funds away until preservation age, which affects the calculation for investors who may need liquidity before retirement.

Non-concessional contribution caps change periodically. Readers considering a lump sum super contribution should verify current limits directly at ato.gov.au/individuals-and-families/super before committing capital.

For investors weighing a lump sum super contribution as part of their windfall deployment, our full explainer on structural costs inside super funds details the pooled CGT drag, swap-based financing spreads, and franking credit allocation gaps that sit outside headline fee disclosures, covering what to look for in a Product Disclosure Statement before committing capital to a specific fund.

Everything above, the data, the psychology, the Australian-specific variables, converges on a four-step self-assessment that produces a personal answer. Run through each step against individual circumstances.

The best strategy is the one the investor will maintain through a full market cycle, including the parts that are uncomfortable.

For investors whose self-assessment lands somewhere in the middle, a hybrid approach offers a legitimate third path. The structure is straightforward: deploy a specified percentage immediately, commonly 50%, and schedule the remainder across a fixed DCA period of 6-12 months.

This suits investors with a windfall, moderate risk tolerance, and a time horizon long enough to benefit from partial early deployment but not enough conviction to go all-in on day one. The DCA portion should be automated through a platform’s recurring purchase feature to remove the temptation to time the remaining tranches based on short-term market moves.

The hybrid approach is not a compromise born of indecision. It is a calibrated allocation of capital that balances time-in-market advantage with psychological manageability.

Lump sum investing’s historical edge is real. In roughly two-thirds of past scenarios, deploying capital immediately produced the stronger outcome. That statistic deserves respect. It does not, however, override the specific circumstances of an individual investor operating in an Australian market environment where Q1-Q2 2026 conditions, a volatile ASX, an active RBA hiking cycle, and elevated rate uncertainty, more closely resemble the 32-34% scenario where DCA has historically outperformed.

The Australian-specific factors that deserve weight in the final decision include CGT parcel strategy, superannuation contribution caps, franking credit timing, and the availability of platform automation for systematic investing.

ASX home bias among Australian investors has historically skewed windfall deployments toward domestic equity ETFs, but Q1 2026 platform data shows international ETFs overtaking domestic funds as the most purchased category, a structural shift that carries direct implications for which index a DCA or lump sum programme should target.

Three immediate next steps:

For investors dealing with a significant windfall, consulting a licensed financial adviser before deploying provides an additional layer of confidence that the chosen strategy accounts for individual tax, estate, and superannuation considerations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Dollar-cost averaging (DCA) involves investing a fixed amount at regular intervals, spreading your entry price over time, while lump sum investing deploys all available capital in a single transaction for maximum time in the market from day one.

Yes, historically lump sum investing has outperformed DCA in approximately 66-68% of scenarios over 10-year periods, according to Vanguard research and Morningstar Australia analyses, though current Q1-Q2 2026 ASX volatility and RBA rate hikes more closely resemble the minority of periods where DCA has historically delivered better outcomes.

A lump sum purchase creates one parcel with a single cost base, while a 12-month DCA programme creates 12 separate parcels, each with its own acquisition date, enabling investors to use specific identification or the minimisation method to manage their CGT position with greater precision at the time of disposal.

The hybrid strategy involves deploying a set percentage of your windfall immediately, commonly 50%, and scheduling the remainder via automated DCA over 6-12 months, making it suitable for investors with moderate risk tolerance who want partial time-in-market exposure without the full psychological weight of an immediate lump sum commitment.

The choice depends on your liquidity needs and tax position: superannuation offers a concessional tax environment but locks funds until preservation age, while a taxable brokerage account has no contribution cap and preserves access; the ATO non-concessional cap for 2025-26 is $120,000, so verifying current limits at ato.gov.au before committing is recommended.