AstraZeneca’s £300M UK Investment Reverses 2025 Retreat

11 mins ago

Parsons Corporation shares increased 0.37 percent in intraday trading on 29 April 2026, driven by the defence contractor achieving an unprecedented 10.1 percent profitability margin. The first-quarter financial results comfortably beat Wall Street bottom-line forecasts, shifting investor focus from raw revenue volume to operational precision.

Evaluating Parsons stock as an investment requires looking beyond the immediate surface figures to understand the structural changes within its operations. The contractor managed to generate record efficiency and a massive future work pipeline during the quarter, even while reporting a headline revenue contraction.

The following analysis details the specific mechanics behind the Q1 2026 performance. The data reveals a clear separation between a single contract lifecycle and the underlying demand for the company’s transportation and missile defence services.

The immediate payoff of the quarter came from record margins, establishing that efficiency rather than sheer volume is driving current investor optimism. Parsons reported an adjusted earnings per share of $0.79, comfortably beating the analyst estimate range of $0.66 to $0.68.

The defining achievement of the reporting period was an unprecedented 10.1 percent adjusted EBITDA margin.

The financial data detailed in the official Q1 2026 8-K filing confirms that adjusted EBITDA reached a record $151 million, cementing the contractor’s ability to extract higher profit yields from its existing revenue base.

This metric pushed adjusted EBITDA to a peak. Total net income for the quarter confirmed that the firm is successfully converting operational changes into direct shareholder value.

Management also demonstrated strong capital discipline during the first three months of the year. The operational capital utilised shrank, down significantly from a drain recorded in the same period last year.

| Financial Metric | Q1 2026 Actual | Wall Street Estimate | Variance / Note |

|---|---|---|---|

| Adjusted EPS | $0.79 | $0.66 to $0.68 | Strong Beat |

| Total Sales | $1.5 billion | N/A | Slight Miss |

| Adjusted EBITDA Margin | 10.1% | N/A | Record High |

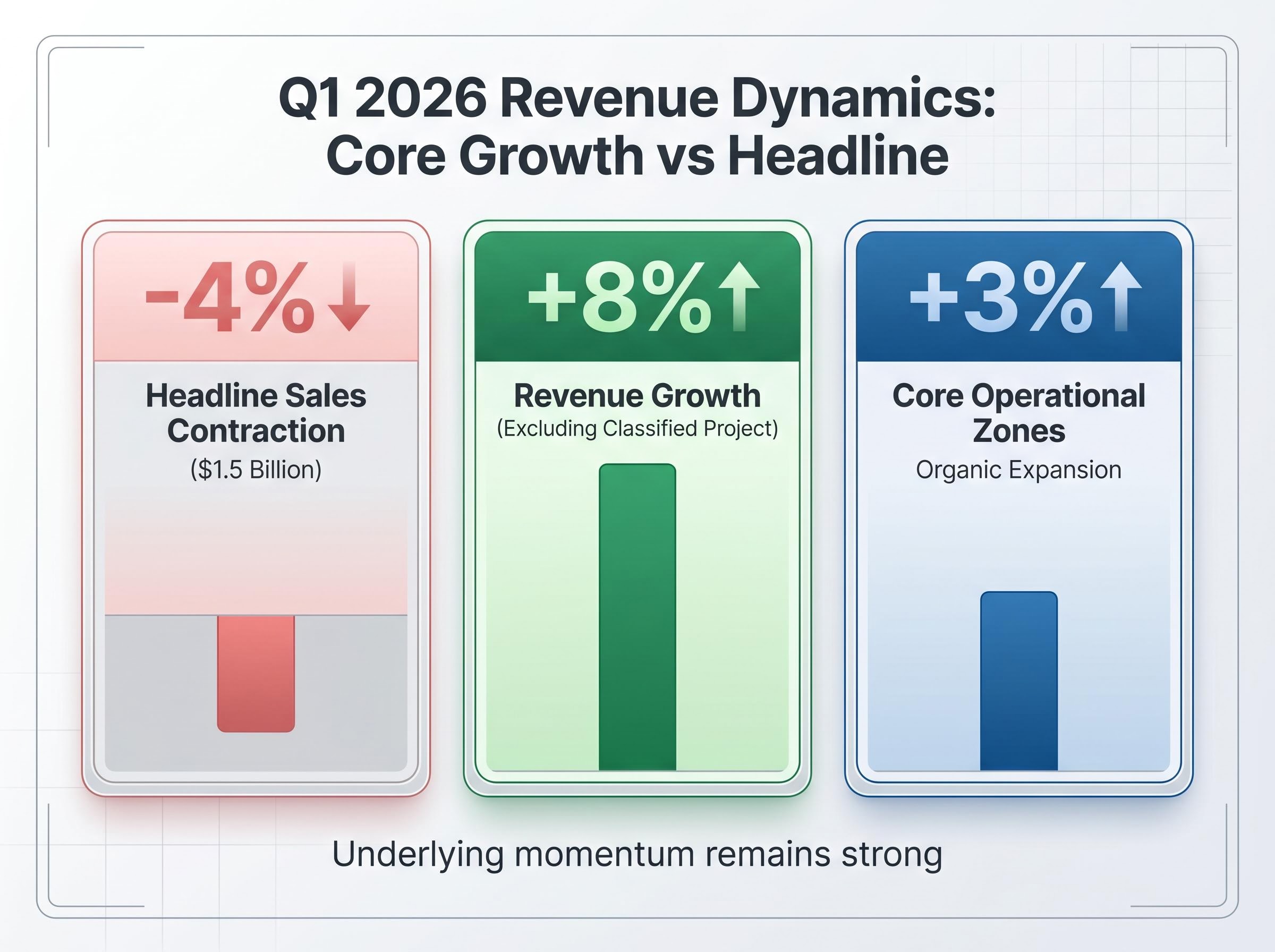

Surface-level declines in the earnings report mask a story of resilient core operations. Total sales declined for the quarter, representing an annual drop that initially drew scrutiny from market participants.

This top-line contraction was entirely driven by lower volume on a single fixed-price confidential contract. When this specific undisclosed project is removed from the calculations, the underlying growth metrics reveal sustained momentum across the broader portfolio.

The core business lines, particularly transportation and missile defence, demonstrated clear expansion during the quarter.

Total headline sales contracted by 4 percent year-over-year to $1.5 billion. Overall revenue grew by 8 percent when excluding the specific classified project. * Core operational zones achieved a 3 percent organic expansion rate.

This separation prevents investors from misinterpreting a single contract’s natural lifecycle as a broader demand issue.

Investors exploring how strategic acquisitions shape these secure operations will find our detailed coverage of Parsons stock analysis, which examines how the Altamira Technologies integration bolstered high-margin classified intelligence capabilities.

Understanding forward-looking defence metrics is necessary to properly evaluate why current quarter revenue dips are often secondary to pipeline expansion. The book-to-bill ratio serves as a primary health indicator in the sector, measuring the ratio of orders received to units billed and shipped.

Analyzing funded backlog metrics alongside total obligations helps investors gauge the genuine financial commitment backing these massive future pipelines.

A ratio above 1.0 indicates that a company is generating new contracts faster than it is fulfilling existing ones. Parsons achieved a strong book-to-bill ratio across both of its operational divisions in Q1 2026, signalling strong future revenue potential.

Classified and fixed-price contracts create natural lumpiness in quarterly revenue recognition. A growing backlog functions as a vital buffer against these short-term revenue fluctuations, moving the analytical focus from past performance to future guaranteed cash flows.

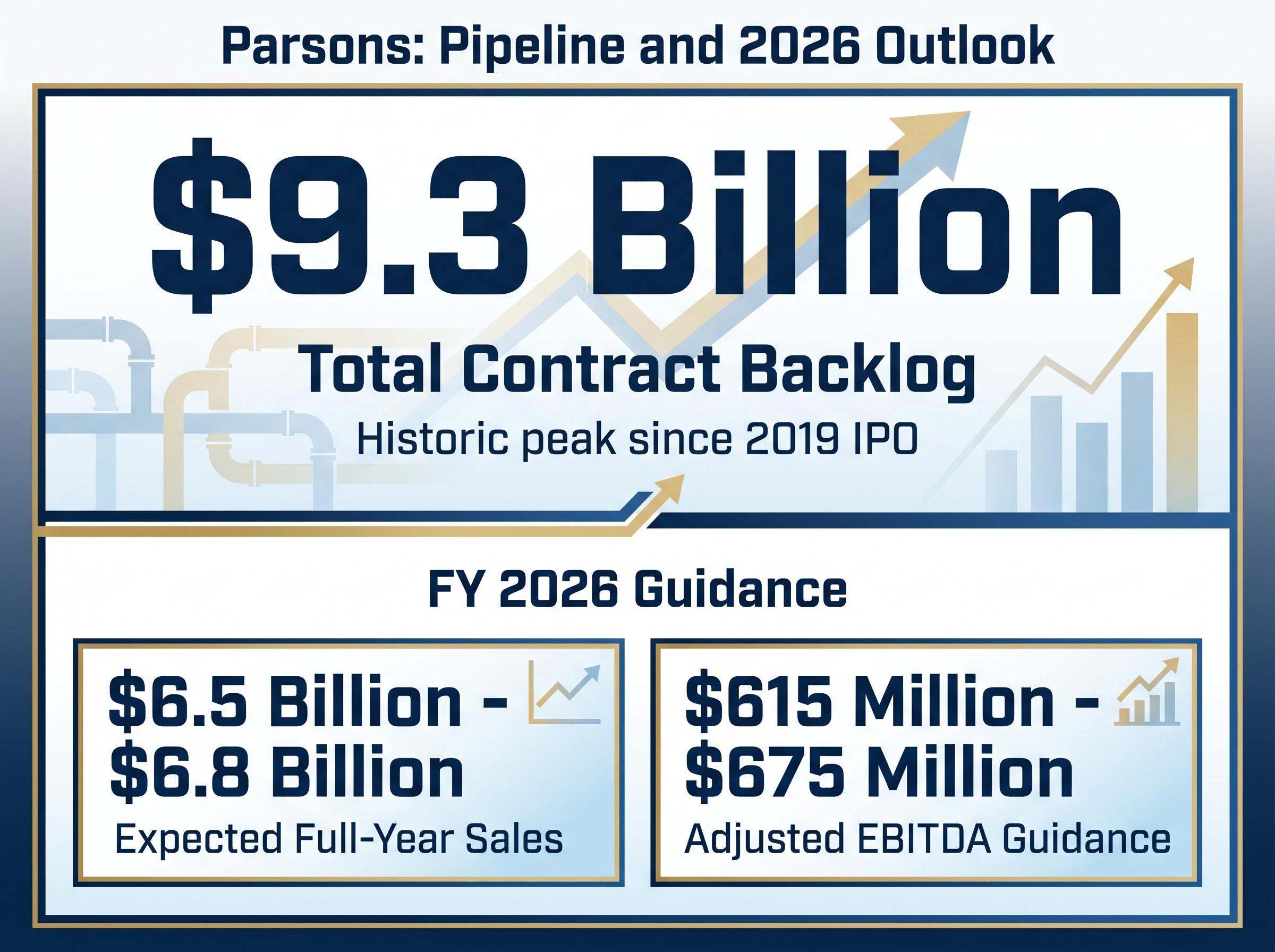

The sheer volume of new contract acquisitions secured during the first three months of the year amplifies the scale of the company’s future security. The total volume of unfinished contractual obligations reached $9.3 billion, marking a historic peak for the enterprise since its 2019 initial public offering.

Stability is further reinforced by the financially backed portion of this future work. The firm acquired fresh agreements during the first quarter alone, demonstrating sustained procurement momentum.

This sustained order flow reflects a broader defence procurement recovery following prior government funding delays, a trend currently driving accelerated purchasing across the sector.

CEO Commentary “Our record backlog and sustained margin expansion demonstrate the resilience of our core operations, positioning the enterprise for disciplined growth through the remainder of the fiscal year,” said Carey Smith, Chief Executive Officer.

The first quarter pipeline expansion was anchored by the achievement of landing four distinct single-award contracts, each valued at over $100 million. Single-award frameworks provide significantly more predictable revenue streams than multiple-award contracts, as they eliminate subsequent bidding requirements for individual task orders.

Comparing these financial metrics against heavyweight peers positions the unique profitability as a standout feature in the current defence sector environment. Major industry competitors like Lockheed Martin typically operate with margins in the 10 percent to 11 percent range.

Recent sector analyses show Lockheed Martin’s operating profit margin testing the 11.7 percent mark, which contextualises just how competitive Parsons has become relative to the industry’s most established heavyweights.

Matching these industry-leading efficiency levels allows a mid-tier contractor to compete aggressively for high-value procurement programmes. Wall Street analysts have largely looked past the top-line volume concerns, focusing instead on the $9.3 billion backlog and the expanding Department of Defence pipeline.

Post-earnings commentary from major investment banks highlights a dual narrative of margin strength outweighing the isolated revenue contraction. Analysts maintained a strong buy consensus following the earnings print, with no immediate downward price target revisions.

The current Wall Street mean price target sits at $74.80. Based on current trading levels, this indicates a potential upside of approximately 45 percent for the equity.

The market steadily digested the earnings call details throughout the trading session. As of mid-afternoon trading on 29 April 2026, the intraday stock price reached $51.69, up 0.37 percent as volume stabilised.

Corporate leadership maintained all previously established sales projections for the 2026 operational year. Expected full-year sales remain projected between $6.5 billion and $6.8 billion, while adjusted EBITDA guidance holds steady between $615 million and $675 million.

The combination of record margins and a massive contractual pipeline positions the firm to execute its fiscal year strategy with minimal reliance on new short-term volume.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Parsons Corporation's stock increased due to achieving an unprecedented 10.1 percent adjusted EBITDA margin, comfortably beating Wall Street's earnings per share forecasts. This strong profitability and record backlog offset a revenue contraction caused by a specific contract.

The top-line revenue contraction was attributed entirely to lower volume on a single fixed-price confidential contract, masking an 8 percent growth in core business lines when that project is excluded. The company's underlying transportation and missile defense services actually expanded.

Parsons' record $9.3 billion backlog, the highest since its 2019 IPO, signifies substantial future revenue potential and stability, buffering against short-term revenue fluctuations. This robust pipeline, including four major single-award contracts, reinforces the company's long-term growth prospects.

Parsons' 10.1 percent adjusted EBITDA margin is competitive with major industry players like Lockheed Martin, which typically operates in the 10 percent to 11 percent range. This strong efficiency allows Parsons, a mid-tier contractor, to compete for high-value procurement programs effectively.