The latest Generac earnings report, released this morning, reveals a striking contrast in the company’s financial momentum. The home consumer division, once the primary driver of revenue, posted a modest growth rate. In stark comparison, the commercial segment surged, signalling a definitive shift in the manufacturer’s operational focus.

The 29 April 2026 financial release represents more than a standard quarterly update. It marks a defining pivot toward powering large-scale computing and server farms. What follows is a clear breakdown of how strategic acquisitions and pending technology sector authorisations are driving the company’s upgraded annual forecasts.

These operational shifts contextualise the widely reported minor fluctuations (around +0.48%) observed in early pre-market trading. For financial readers, this disclosure isolates exactly how the company plans to capitalise on widespread power grid constraints.

Commercial Power Surges Past Consumer Segments

The first quarter financial results comfortably surpassed Wall Street consensus estimates across all major metrics. Net sales reached $1.06 billion, representing a 12% year-over-year increase that beat the $1.04 billion expectation. Adjusted earnings per share climbed to $1.80, well ahead of the $1.33 consensus.

This top-line outperformance obscures a dramatic divergence beneath the surface. The growth engine has officially shifted from suburban driveways to industrial parks.

| Metric | Wall Street Consensus | Q1 2026 Actual |

|---|---|---|

| Net Sales | $1.04 billion | $1.06 billion |

| Adjusted EPS | $1.33 | $1.80 |

Commercial and Industrial segment revenues marked an expansion. In contrast, the consumer home division reflected a stagnant growth rate. Early market reactions reflected this shift, with widespread reports of a +0.48% pre-market equity surge as investors digested the commercial momentum.

Examining the Segment Divergence

High interest rates and stabilised residential power grids have temporarily softened demand for home backup units. Consumers are deferring large capital expenditures on residential generators.

This deferral of major residential purchases aligns with underlying economic strain, as declining personal savings rates force many households to severely curtail their discretionary spending.

Simultaneously, accelerated demand in the commercial sector is absorbing the slack. Heavy industrial users are securing independent power generation at record rates, entirely offsetting the consumer slowdown. Investors can now see exactly where the revenue outperformance originates.

When big ASX news breaks, our subscribers know first

The Hyperscale Catalyst Reshaping Generac Strategy

The current earnings beat is likely just the beginning of a larger structural contract pipeline with the largest players in the technology industry. Generac is aggressively expanding into the highly lucrative data centre infrastructure market.

This strategic push is rapidly translating into an expanded product backlog for commercial-grade equipment. Management confirmed they are in the final stages of securing vendor approvals with multiple hyperscale customers.

The expanding backlog allows the manufacturer to capture a direct slice of the massive AI infrastructure investment currently being deployed by major technology companies to build out their computing networks.

“We continue to execute strongly in the data centre market, and we are in the final stages of vendor authorisation with several hyperscale customers,” said Aaron Jagdfeld, Chief Executive Officer.

These pending authorisations act as the primary catalyst for future growth. Securing approval from hyperscalers signals a significant acceleration in the manufacturer’s entry into the large-scale server farm industry. For investors, this reveals the forward-looking strategy. The focus has moved from selling individual units to securing massive, multi-year infrastructure contracts.

Understanding the Power Economics of Server Farms

The optimism surrounding the new commercial strategy relies heavily on the physical realities of modern power consumption. Hyperscalers and large-scale computing centres require absolute, uninterrupted industrial power to function.

Official EIA electricity demand forecasts project the strongest four-year growth trajectory in over two decades, driven heavily by the massive consumption requirements of these new computing facilities.

Widespread utility grid constraints are increasingly unable to guarantee this level of stability. This forces data centre operators to secure massive, independent backup generation facilities on-site.

Three main factors drive the necessity for dedicated commercial power infrastructure at server farms:

The immense energy draw of high-density computing clusters requires industrial-scale generation that exceeds standard commercial capabilities. Ageing regional utility grids frequently face capacity limits and load-shedding events, posing unacceptable risks to mission-critical operations. * Stringent uptime guarantees written into client contracts mandate zero-interruption power redundancies.

In this highly regulated space, vendor authorisation is a rigorous technical vetting process. It confirms a supplier’s equipment can handle the extreme demands of uninterrupted server operation. Achieving this status proves the company manufactures hardware capable of meeting strict enterprise-grade specifications.

Strategic Buyouts Accelerate the Industrial Pipeline

Securing hyperscale contracts requires the physical manufacturing capacity to deliver heavy industrial equipment. The company successfully integrated two major acquisitions in the first half of 2026 to build this exact infrastructure.

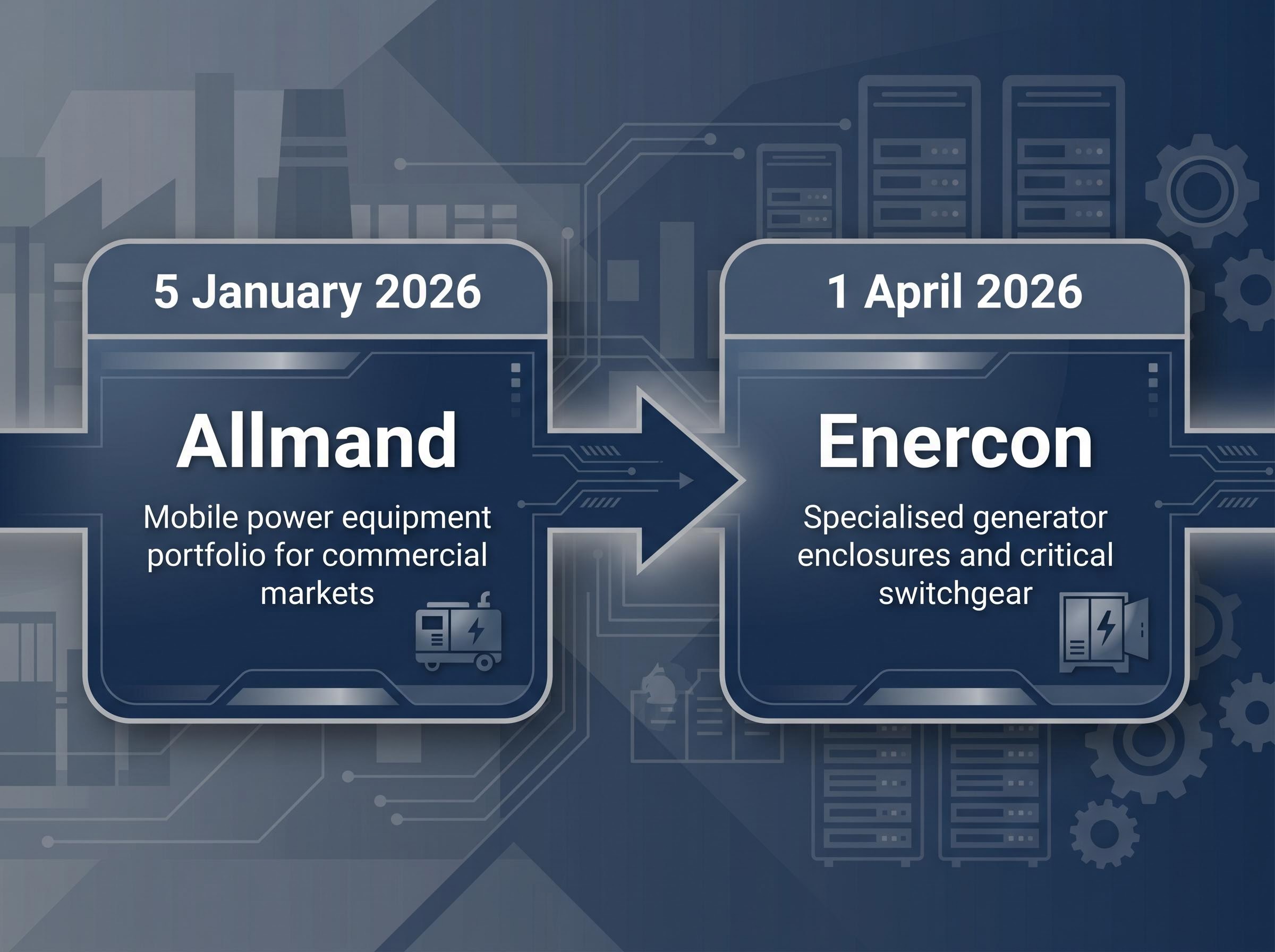

On 5 January 2026, the manufacturer completed the acquisition of Allmand, significantly expanding its mobile power equipment portfolio for commercial markets. Leadership specifically cited these recent buyouts as primary catalysts for their upgraded financial projections. By linking this corporate activity to the hyperscale contract news, the strategic roadmap becomes clear. The company now possesses the necessary manufacturing capabilities to deliver on its new technology sector promises.

The Enercon Capabilities

The most critical piece of the data centre puzzle arrived with the Enercon acquisition, finalised on 1 April 2026. This purchase brings specialised generator enclosures and critical switchgear directly into the product line.

These specific technical components are mandatory for large-scale computing facilities. The addition of custom switchgear allows the company to offer complete, integrated power management systems rather than standalone generators, fundamentally elevating their technical offering for hyperscalers.

Wall Street Reacts to Upgraded 2026 Forecasts

The operational wins in the commercial sector have mathematically altered the company’s financial trajectory for the remainder of the year. The upgraded commercial sales forecast now serves as the anchor for significantly improved profit margins.

Prior to the earnings release, Wall Street maintained a mixed outlook. Pre-earnings analyst price targets established a baseline expectation, with Canaccord Genuity setting a $300 target, Needham at $277, and Barclays at $228.

Driven by the data centre momentum, management raised their full-year guidance across three critical metrics.

| Metric | Previous 2026 Guidance | Upgraded 2026 Guidance |

|---|---|---|

| Net Sales Growth | Mid-teens percentage | Mid-to-high teens percentage |

| Adjusted EBITDA Margin | 18.0% to 19.0% | 18.5% to 19.5% |

| Commercial Sales Growth | Low-to-mid 20% range | Mid-to-high 20% range |

These revised benchmarks translate the narrative strategy back into hard numbers. The anticipated commercial expansion provides the volume necessary to push the Adjusted EBITDA margin into the higher target window.

Generac is not the only infrastructure provider benefiting from this structural shift; accelerating hyperscale data centre demand is triggering similar earnings upgrades across the global critical infrastructure sector.

A Permanent Shift in Corporate Identity

The first quarter results confirm a permanent evolution for the manufacturer. The business has transitioned from a residential backup provider into a critical infrastructure partner for the global computing sector.

The successful integration of Enercon and Allmand provides the physical engines necessary to drive the newly upgraded 2026 financial forecasts. These acquisitions ensure the company can physically manufacture the specialised switchgear and enclosures that major technology clients demand.

Looking ahead, the market awaits the formal announcement of hyperscale contracts expected later this year.

Investors exploring the broader financial impact of this corporate spending shift will find our detailed coverage of how AI capital expenditure drives hardware markets, which outlines the multi-year timelines required to monetise these heavy industrial investments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.