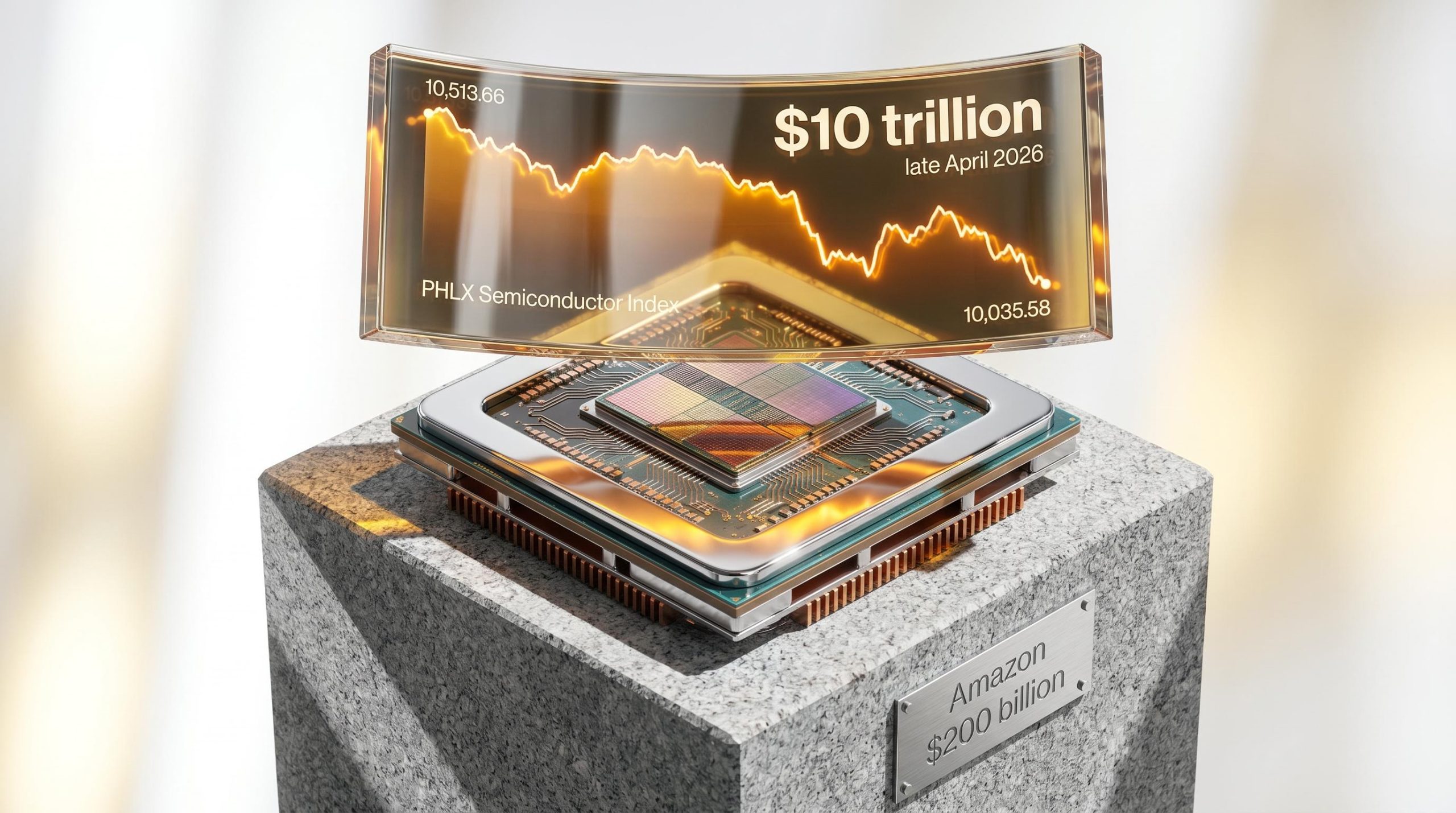

According to market estimates, the upcoming earnings wave for the largest technology conglomerates represents a $10 trillion valuation test for companies that currently command a 17% weighting in the S&P 500 index. As analysts evaluate the AI stock market and its underlying physical infrastructure in late April 2026, derivative pricing remains remarkably calm despite mounting scrutiny over hardware profitability. The gap between the sheer scale of potential valuation shocks and the market’s muted response reveals how current options pricing masks a massive structural vulnerability. This synchronized reporting schedule obscures the severe downside risk facing semiconductor hardware stocks, which remain entirely dependent on hyperscalers sustaining unprecedented capital expenditure levels. Understanding this divergence between derivative market complacency and hardware vulnerability provides a critical framework for measuring systemic equity risks.

The Complacent Pricing in the Derivatives Market

Traders are currently projecting notably subdued post-earnings price swings for major technology conglomerates, contrasting sharply with the massive financial stakes of their reporting week. Options data heading into the final days of April 2026 shows a distinct compression in expected volatility compared to historical averages. This synchronized reporting schedule typically introduces heightened risk for widespread instability across the broader US equities ecosystem.

The structural vulnerabilities tied to megacap tech stock concentration have reached historic levels, with just four companies commanding over 19% of the index and amplifying the potential impact of any single earnings disappointment.

The specific discrepancy between currently expected volatility and trailing twelve-quarter averages highlights the potential for sudden valuation shocks. Derivative contracts for Amazon indicate an expected post-announcement price swing of nearly 6.5%. Similarly, options pricing predicts a 7.1% adjustment for Meta.

For Amazon options carrying a May 1 expiry date, the implied volatility rests at approximately 98%. Options expiring April 29 price in an expected move of plus or minus $9.76, reflecting a market that appears largely unconcerned about the potential for material guidance downgrades. This collective underpricing of risk creates an immediate, actionable view into how heavily traders are underestimating the potential for an earnings-driven correction across the technology sector.

| Reporting Company | Current Implied Options Move | Trailing 12-Quarter Average Move |

|---|---|---|

| Amazon | nearly 6.5% | Not Available |

| Meta | 7.1% | Not Available |

| Alphabet | 7.0% | Not Available |

When big ASX news breaks, our subscribers know first

Decoding the Multi-Billion Dollar Infrastructure Mandate

The foundational relationship between generative model capabilities and continuous data centre expansion explains why hyperscalers have no choice but to commit historic levels of capital. Training and operating advanced models requires an absolute baseline of physical computing infrastructure that must scale linearly with processing demands. This dynamic has forced the largest technology companies to mandate unprecedented capital expenditures for the fiscal year 2026.

These extreme spending commitments represent a fundamental transition in how technology companies allocate their resources. Industry analysis shows hardware spending transitioning to a significantly larger share of operating cash flow. This financial trajectory demystifies the underlying mechanics of the broader technology equity boom, demonstrating the extreme pressure building beneath the surface just to maintain current operational capacities.

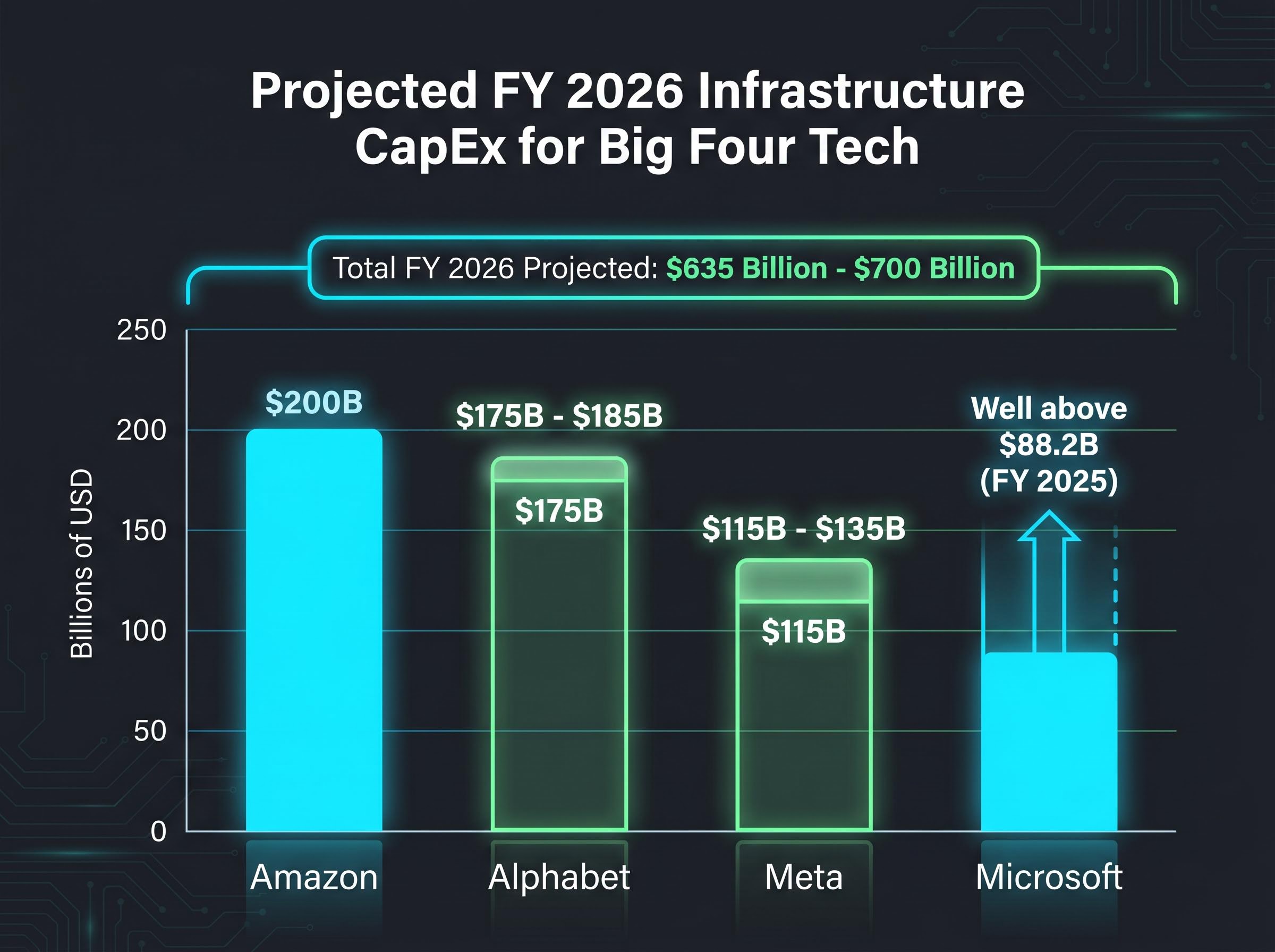

Combined fiscal year 2026 infrastructure capital expenditures for the Big Four tech firms are projected to reach between $635 billion and $700 billion. This capital deployment is heavily weighted toward processor acquisition and facility construction.

The Financial Times infrastructure spending data confirms this historic physical expansion, highlighting that such extreme financial commitments are beginning to reignite broader market debates regarding a potential technology hardware bubble.

Amazon: Allocating approximately $200 billion, primarily directed toward expanding data centre footprints. Alphabet: Projected to deploy between $175 billion and $185 billion on computing infrastructure. Meta: Targeting capital expenditures ranging from $115 billion to $135 billion. Microsoft: Expected to land well above its $88.2 billion spend recorded in fiscal year 2025.

By grasping the sheer volume of capital required to sustain these systems, investors can better appreciate why the current spending pipeline cannot absorb any meaningful deceleration in top-line revenue growth.

The Hidden Crisis of Escalating Inference Costs

The massive capital deployment outlined above appears increasingly precarious when analysing the stark difference between training a model and the ongoing costs of model inference. While training requires a singular, massive injection of computing power, inference represents the continuous processing cost incurred every time an end-user queries the system. These escalating inference costs are severely threatening the profitability of generative applications across the entire software ecosystem.

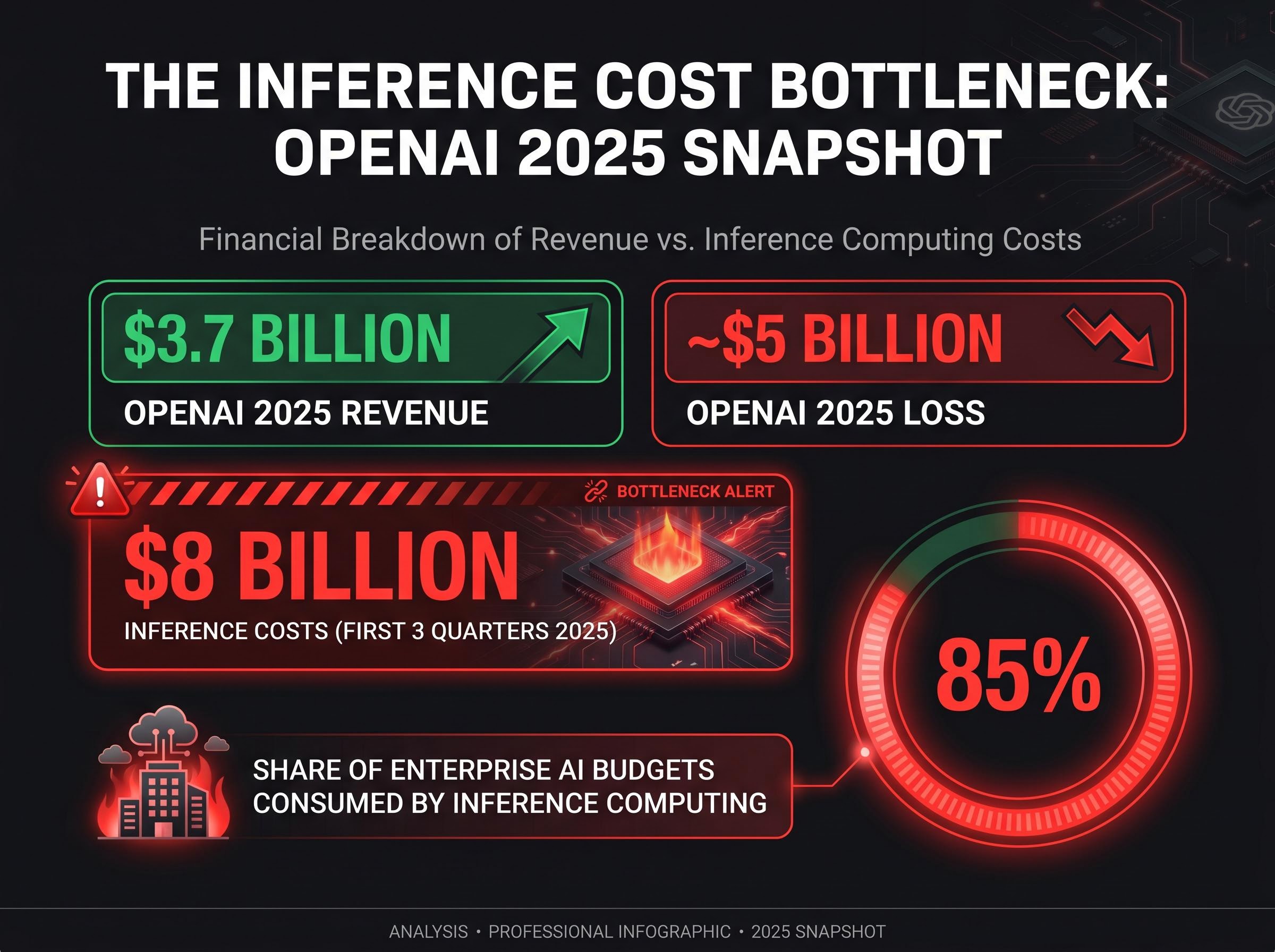

Virtually all major generative developers are currently losing money despite achieving massive commercial scale, creating a structural bottleneck for the broader technology sector. OpenAI, for instance, reported a loss of approximately $5 billion on $3.7 billion in revenue during 2025. The primary driver of this deficit was operational computing requirements, with inference costs accounting for $8 billion of the company’s expenses in just the first three quarters of 2025.

This unprofitable reality translates directly into fragility for the broader hardware supply chain. Inference computing now consumes approximately 85% of enterprise artificial intelligence budgets, leaving very little capital for application development or software innovation. If the end-product remains fundamentally unprofitable to operate, the massive budgets funding the entire hardware sector could abruptly collapse.

Financial Analyst Warning “The current trajectory of inference computing expenses fundamentally alters the profitability equation for software developers, creating a scenario where scaling user adoption actively accelerates capital destruction rather than generating margin expansion.”

The Downstream Shockwave Approaching Semiconductor Stocks

The extreme downside risk for processor manufacturing entities correlates directly with the mounting earnings pressure facing their largest Big Tech customers. Hardware providers have enjoyed soaring valuations based on the assumption that hyperscaler capital expenditure will grow perpetually, leaving them highly exposed to any deceleration in top-level infrastructure spending. To fund continuous chip purchases, technology companies are making highly consequential workforce and resource trade-offs that industry experts warn are deeply regrettable and ultimately unsustainable.

The persistent semiconductor supply chain constraints have temporarily insulated hardware manufacturers from these downstream pressures, but this dynamic is shifting as hyperscalers demand clearer paths to cloud software monetization.

If generative developers cannot resolve their profitability constraints, the reliance on chipmakers to supply the hardware becomes a critical vulnerability for equity portfolios. This structural threat is already manifesting in the price action of major processor manufacturers.

Recent Market Contractions and Warning Signs

The PHLX Semiconductor Index has recorded a 47% overall increase since April 2025, but the sector exhibited severe volatility leading into the final week of April 2026. The index dropped notably amid mounting rumours regarding revenue and adoption shortfalls at prominent generative developers. The benchmark fell from 10,513.66 on April 24 down to 10,035.58 by April 28, signalling that institutional capital is beginning to price in the fundamental risks of hardware overcapacity.

This volatility demonstrates that the market is already exhibiting signs of stress. Current analyses point to three primary vulnerability vectors for chipmakers:

- Inference cost crises that make software deployment fundamentally unprofitable.

- Earnings pressure stemming from broad slowdowns in commercial technology adoption.

- Structural enterprise bottlenecks created by the unsustainable diversion of operational budgets toward hardware procurement.

Assessing the Breaking Point for Hardware Valuations

The prevailing complacency in derivative markets stands in direct contradiction to the highly vulnerable, multi-billion dollar hardware spending pipeline. Historical market data indicates that shareholder tolerance for delayed profitability is severely limited, typically lasting only a few quarters to one year maximum before valuation multiples compress. While options traders currently project subdued volatility for upcoming earnings, the structural unprofitability of inference computing suggests the underlying ecosystem is rapidly approaching a critical breaking point.

Investors holding semiconductor and hardware equities must now look beyond the immediate quarter’s revenue figures. The primary metric to monitor is the forward guidance language from hyperscalers regarding their 2027 capital deployment plans. Any indication that Microsoft, Amazon, Alphabet, or Meta plan to taper their data centre expansion will likely trigger an immediate revaluation of the entire processor supply chain.

For readers wanting to contextualize this hardware vulnerability within the wider macroeconomic landscape, our detailed coverage of broader market risk factors examines how elevated geopolitical tensions and inflation pressures are further compounding these fundamental equity threats.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and forward-looking statements regarding capital expenditures are subject to market conditions, technological changes, and various risk factors.