CSL Has Lost 43%: What the Numbers Say at A$99.76

1 hr ago

Seagate Technology shares have orchestrated a staggering rally over the last twelve months, culminating in aggressive Wall Street upgrades issued today, April 29, 2026. Major financial institutions are hastily revising their valuation models after the hardware manufacturer heavily exceeded third-quarter earnings estimates with unprecedented margin expansion. The sheer scale of this upward trajectory has forced institutional investors to reconsider the fundamental limits of hardware profitability. For analysts issuing a new Seagate price target, historical cyclical precedents no longer apply to the current market environment.

This coverage provides a complete breakdown of the revised analyst valuations and the exact financial metrics that broke Wall Street forecasting models. It also examines the artificial intelligence market mechanics extending this historic hardware supercycle. By analysing both the immediate corporate performance and the underlying structural advantages, investors can understand exactly how a physical product supplier achieves software-like pricing power.

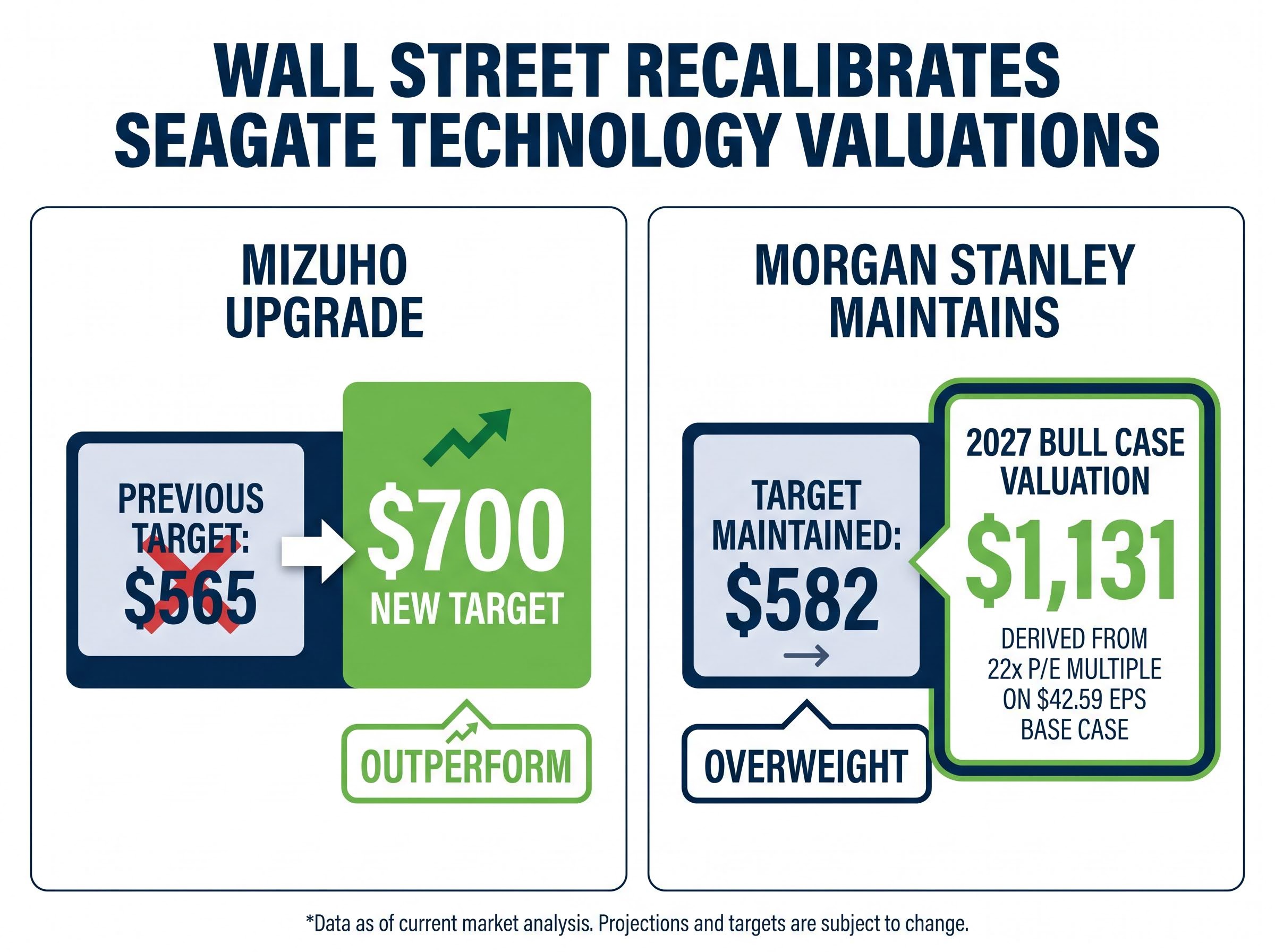

The magnitude of Wednesday morning’s analyst recalibrations reflects a fundamental shift in how Wall Street views the data storage sector. Mizuho immediately issued an aggressive upgrade, raising its target to $700 from $565 while maintaining an Outperform rating. The firm cited exceptionally strong ongoing market demand as the primary driver for the revision.

Despite the overwhelmingly positive financial metrics, the stock experienced a slight aftermarket dip to $565.55. Investors are currently digesting what these structural revaluations mean for the company’s earning power over the next two years. These actions represent complete recalibrations of future cash generation rather than incremental target adjustments.

| Firm | Previous Target | New Target | Current Rating |

|---|---|---|---|

| Morgan Stanley | $582 | $582 | Overweight |

| Mizuho | $565 | $700 | Outperform |

Morgan Stanley’s updated valuation model details a fundamental shift for the hardware manufacturer. The firm reported a new target increase to $582 from $582, maintaining an Overweight rating as its previous bull case scenario effectively became its standard base case expectation.

The specific mathematics behind this upgrade reveal a massive disparity from broader analyst consensus. According to unconfirmed reports, the firm models a calendar year 2027 earnings per share base case of $42.59, sitting 132% above the current street consensus. According to unconfirmed reports, when applying a 22x price-to-earnings multiple to this future earnings power, the firm’s new bull case valuation stretches to $1,131.

For investors wanting to understand the competitive advantages driving these premium multiples, our detailed coverage of Seagate’s AI storage moat breaks down the HAMR technology lead and the structural shift toward hyperscale data center demand.

The catalyst behind these radical analyst upgrades lies in the raw financial metrics reported on April 28, 2026. Seagate delivered fiscal third-quarter results that demonstrated extraordinary pricing leverage against its enterprise customer base. The company reported total revenue of $3.11 billion, comfortably beating the consensus estimate of $2.95 billion.

Profitability metrics provided the most significant shock to institutional forecasting models. The company achieved a record 47% non-GAAP gross margin, an exceptionally rare achievement for a physical hardware manufacturing operation. This margin expansion drove non-GAAP earnings per share to $4.10, eclipsing the $3.50 expectation and translating to a decade-high free cash flow of $953 million.

Seagate’s fiscal third-quarter supplemental financial information confirms this unprecedented profitability, proving that the hardware supplier successfully executed aggressive price hikes across its enterprise portfolio without suffering volume degradation.

| Metric | Consensus Estimate | Reported Actual / Guidance |

|---|---|---|

| Q3 2026 Revenue | $2.95 billion | $3.11 billion |

| Q3 2026 EPS | $3.50 | $4.10 |

| Q4 2026 Revenue | $3.16 billion | $3.45 billion (± $100M) |

| Q4 2026 EPS | $3.96 | $5.00 (± $0.20) |

These figures prove to the market that recent institutional upgrades are backed by concrete cash generation rather than speculative future promises. The strong June quarter guidance cements the continuation of this financial momentum into the second half of the year. Management projects fourth-quarter revenue of $3.45 billion alongside projected earnings per share of $5.00.

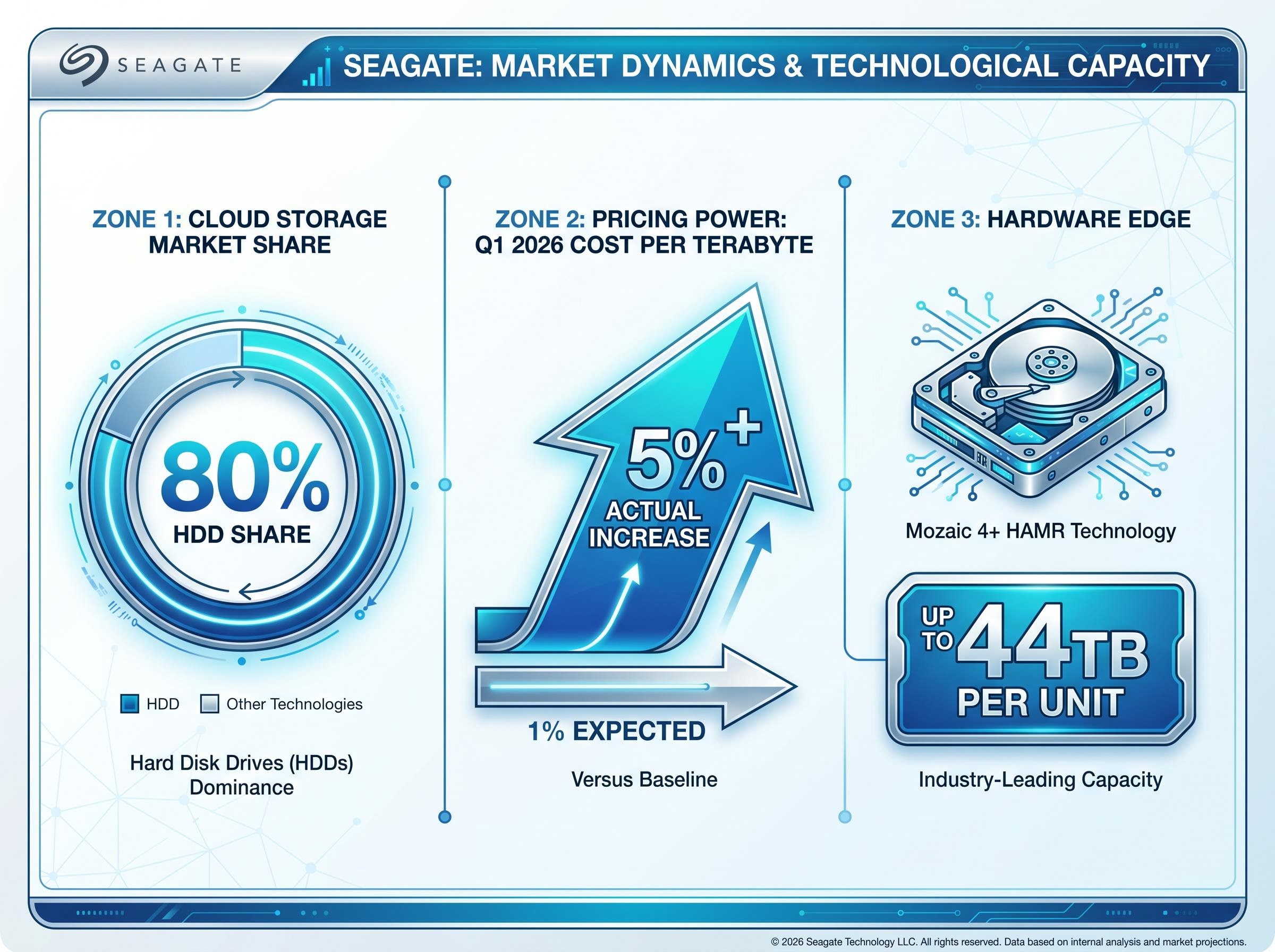

This margin expansion is not purely a function of rising demand, but rather the result of a highly concentrated market structure. The hard disk drive sector currently operates as a rational oligopoly. A small number of major suppliers exercise disciplined output controls, creating a deliberate supply shortfall relative to market needs.

For readers evaluating hardware manufacturing cycles, this structure explains exactly why Seagate possesses the leverage to raise prices without losing market share to competitors. According to industry estimates, hard disk drives continue to command roughly 80% of all cloud storage demand across the technology sector. When suppliers refuse to overproduce, cloud infrastructure providers have no choice but to absorb price increases.

This dynamic directly influences the rising cost per terabyte recorded across the industry. According to market estimates, during the first quarter of calendar year 2026, the cost per terabyte rose 5% quarter over quarter, significantly beating the anticipated 1% increase. The current market cycle is defined by three main characteristics:

This structural pricing power is further insulated by the significant total cost of ownership advantage that hard disk drives maintain over solid state alternatives for high-capacity cloud deployments.

Disciplined production caps enforced among the major hardware suppliers Sustained supply constraints relative to expanding cloud infrastructure needs * Unprecedented pricing leverage for premium, high-capacity storage tiers

The evolution of artificial intelligence is fundamentally altering the demand curve for physical storage products. Agentic AI platforms operate autonomously to solve complex problems, generating exponentially larger data sets that require immediate and long-term retention. This specific demand vector bridges the gap between software platform hype and physical hardware realities.

Seagate has positioned itself to capture this enterprise demand through its Mozaic 4+ HAMR technology. The Heat-Assisted Magnetic Recording drives offer up to 44TB per unit and are currently generating shipping revenue from major cloud providers. This technological advantage allows data centre operators to maximise their physical footprints, extending the traditional hardware upcycle beyond historical norms.

The published next-generation Mozaic 4+ technical specifications validate this density breakthrough, showing how hyperscale data centres can drastically multiply their storage capabilities within existing physical infrastructure footprints.

Chief Executive Officer William Mosley highlighted this exact dynamic during the third-quarter earnings presentation. He noted that the shift toward autonomous enterprise workflows is creating an entirely new category of physical storage requirements.

“Agentic AI applications can drive enormous data sets, referencing large data for conclusions and creating new data that needs storage.”

Investors can now trace exactly how artificial intelligence adoption translates into physical storage sales. As enterprise clients deploy these advanced models, the physical infrastructure required to support them mandates continuous, high-margin hardware investment.

The immediate market reaction captures a unique alignment of disciplined market supply, exploding data storage demand, and flawless corporate execution. Major Wall Street firms have been forced to move their previous bull case scenarios directly into their base case expectations. The sheer scale of the third-quarter earnings beat validates this aggressive institutional recalibration.

To justify this newly assigned premium valuation, Seagate must now clear significant execution hurdles in the upcoming June quarter. Delivering on the projected $3.45 billion revenue target will require seamless scaling of its high-capacity product lines. The hardware resurgence is well underway, but the company must maintain its strict pricing discipline to sustain these historic operating margins.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Wall Street analysts raised the Seagate price target following the company's strong third-quarter earnings report, which showcased unprecedented margin expansion and better-than-expected revenue. Firms like Mizuho and Morgan Stanley recalibrated their valuation models based on these results and future growth prospects.

Seagate's record 47% non-GAAP gross margins are largely driven by a highly concentrated hard disk drive market, which operates as a rational oligopoly. This allows major suppliers to enforce disciplined production controls, creating supply shortfalls and unprecedented pricing leverage for high-capacity storage tiers.

Agentic AI platforms operate autonomously, generating exponentially larger datasets that require immediate and long-term retention, fundamentally altering the demand curve for physical storage products. Seagate's Mozaic 4+ HAMR technology is positioned to meet this growing enterprise demand for high-capacity drives.

For Q3 2026, Seagate reported $3.11 billion in revenue and $4.10 non-GAAP earnings per share, both exceeding consensus estimates. The company also achieved a record 47% non-GAAP gross margin and generated $953 million in free cash flow.