Warsh Strips Fed Statement to 130 Words, Drops All Guidance

33 mins ago

Starbucks posted 6.2% global comparable sales growth in its Q2 FY2026 earnings on 28 April 2026, the strongest North American transaction performance in roughly three years. The stock surged to close at $98.67, and within hours, two of Wall Street’s more detailed research operations had revised their multi-year earnings estimates upward. The question for investors is no longer whether the turnaround under CEO Brian Niccol is producing results. It is whether the margin recovery math that Evercore and Wolfe Research are now modelling through FY2028 can withstand the cost pressures still visible in the quarterly numbers. What follows is a breakdown of both analyst frameworks, the specific milestones they are tracking, and the risks that could stall the thesis before it compounds.

The surprise was not that Starbucks grew. It was the magnitude of the acceleration. 6.2% global comparable sales growth arrived against a difficult macro backdrop and ahead of consensus expectations, marking a clear inflection from the trajectory that had defined much of FY2025.

The Q2 FY2026 earnings beat delivered non-GAAP EPS of $0.50, approximately 19% above Wall Street consensus, alongside North America transaction volume growth of 4.4%, the strongest traffic recovery the company had recorded in roughly three years.

Evercore attributed the turnaround signal to a 13 percentage point improvement in North American same-store sales over the prior six quarters, a swing the firm described as the most analytically significant data point in the release.

On the back of these results, Starbucks raised its full-year FY2026 guidance across multiple metrics:

The National Restaurant Association’s 2026 industry outlook identifies a K-shaped consumer spending pattern compressing traffic among lower- and middle-income customers, a dynamic that provides important context for why Starbucks’ comparable sales recovery is analytically significant against the broader sector backdrop.

The guidance raise confirmed that management sees the top-line momentum as durable. The margin compression confirmed that the cost structure has not yet caught up. That gap between revenue recovery and profit recovery is precisely what the two analyst upgrades that followed are attempting to price.

Evercore raised its price target on SBUX to $115 from $110 and maintained its Outperform rating, a move that carries more weight when the underlying margin mechanics are examined.

The centrepiece of Evercore’s revised model is the North America incremental margin trajectory. The firm projects incremental margins of negative 7% in FY2026, turning to above 50% in FY2027.

That swing, from negative 7% to above 50%, is the single most aggressive margin call in the current Starbucks analyst coverage. Evercore attributes it to three converging forces: easing labour reinvestment costs, subsiding coffee-related inflation, and the scaling of Starbucks’ $2 billion productivity savings programme targeting FY2028.

The revised EPS estimates follow accordingly:

| Fiscal Year | Prior Estimate | Revised Estimate | Change |

|---|---|---|---|

| FY2026 | $2.30 | $2.45 | +$0.15 |

| FY2027 | $3.09 | $3.25 | +$0.16 |

| FY2028 | $3.92 | $4.00 | +$0.08 |

For investors assessing whether SBUX at roughly $98-$99 per share represents value, Evercore’s $115 target and the mechanics behind its FY2027 margin call are the most specific directional signal in the current coverage. The question is whether the conditions that produce that inflection actually materialise.

Incremental operating margin measures the proportion of each additional revenue dollar that flows through to operating profit after variable costs. It is a more useful signal than headline operating margin during a recovery because it captures the rate of change in profitability, not just the level.

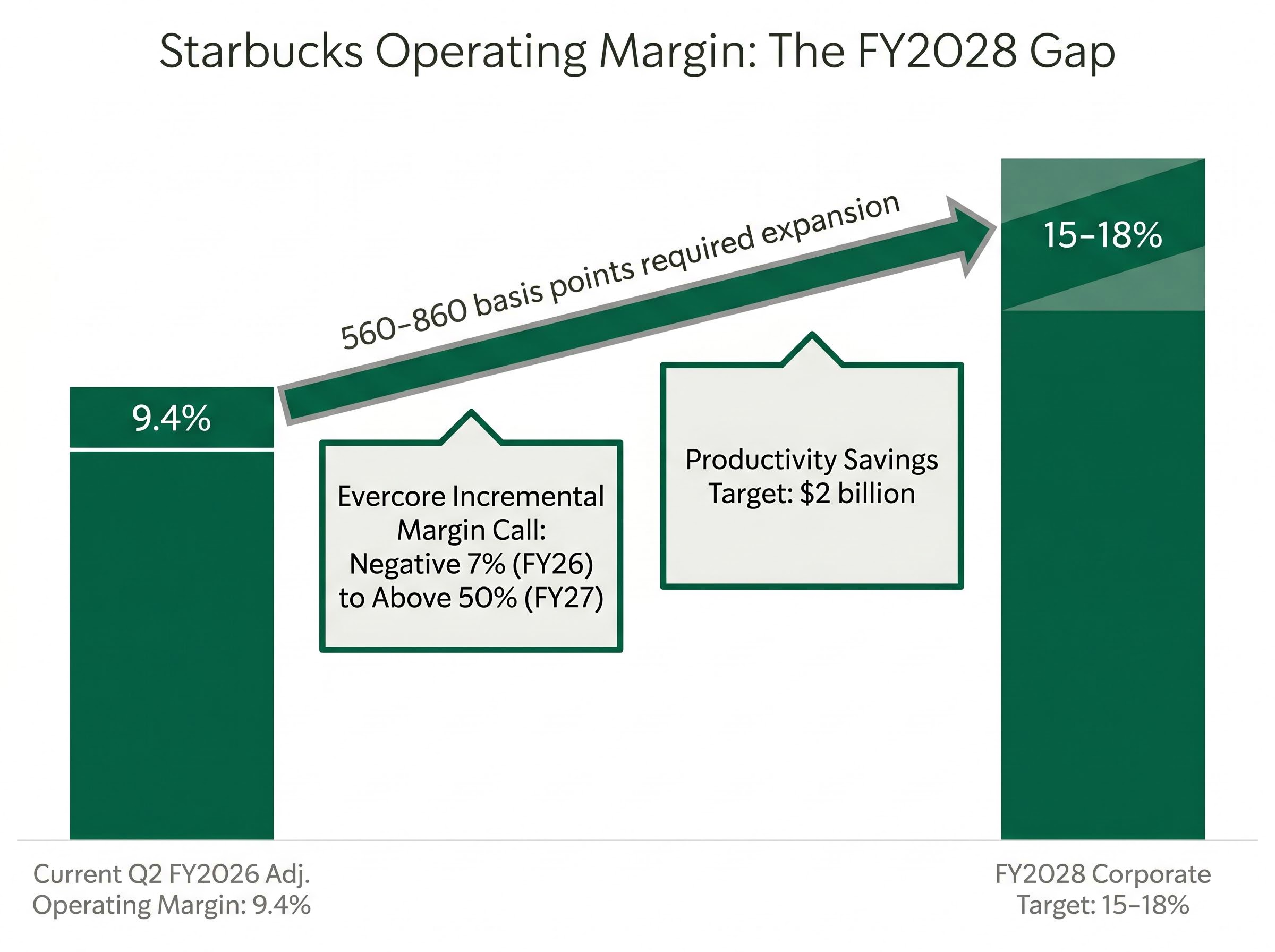

A company can show improving incremental margins while its reported operating margin remains compressed. This happens when new revenue is being converted to profit at higher rates than the existing base, even though the absolute margin figure has not yet recovered. For investors reading Starbucks’ 9.4% adjusted operating margin and concluding the profit story is weak, incremental margin analysis offers a different lens.

The conditions required for Starbucks’ projected inflection are specific:

The operating margin expansion required to close the gap between the current 9.4% adjusted figure and the 15-18% corporate target by FY2028 rests on a specific sequence: fixed labour costs becoming a smaller share of rising revenue, commodity normalisation arriving on schedule, and the productivity savings programme delivering at the pace modelled.

The largest structural cost in the current model is the permanent labour investment underpinning the customer experience strategy. Unlike temporary promotional spending, these costs do not recede when growth slows.

Commodity price volatility sits as the key variable input. If coffee-related inflation eases as Evercore projects, the incremental margin swing becomes plausible. If it does not, the $2 billion productivity savings target by FY2028 must carry more of the bridge between the current 9.4% operating margin and the corporate target of 15-18% by FY2028.

The forward P/E of approximately 27x and EV/EBITDA of approximately 15.2x suggest the market is pricing in some margin recovery. Whether it is pricing in the full extent of Evercore’s FY2027 inflection is the valuation question.

Where Evercore leads with margin mechanics, Wolfe Research anchors its thesis on the consumer-facing catalysts that would drive top-line acceleration. The distinction matters because the two firms are building the same bull case from different foundations.

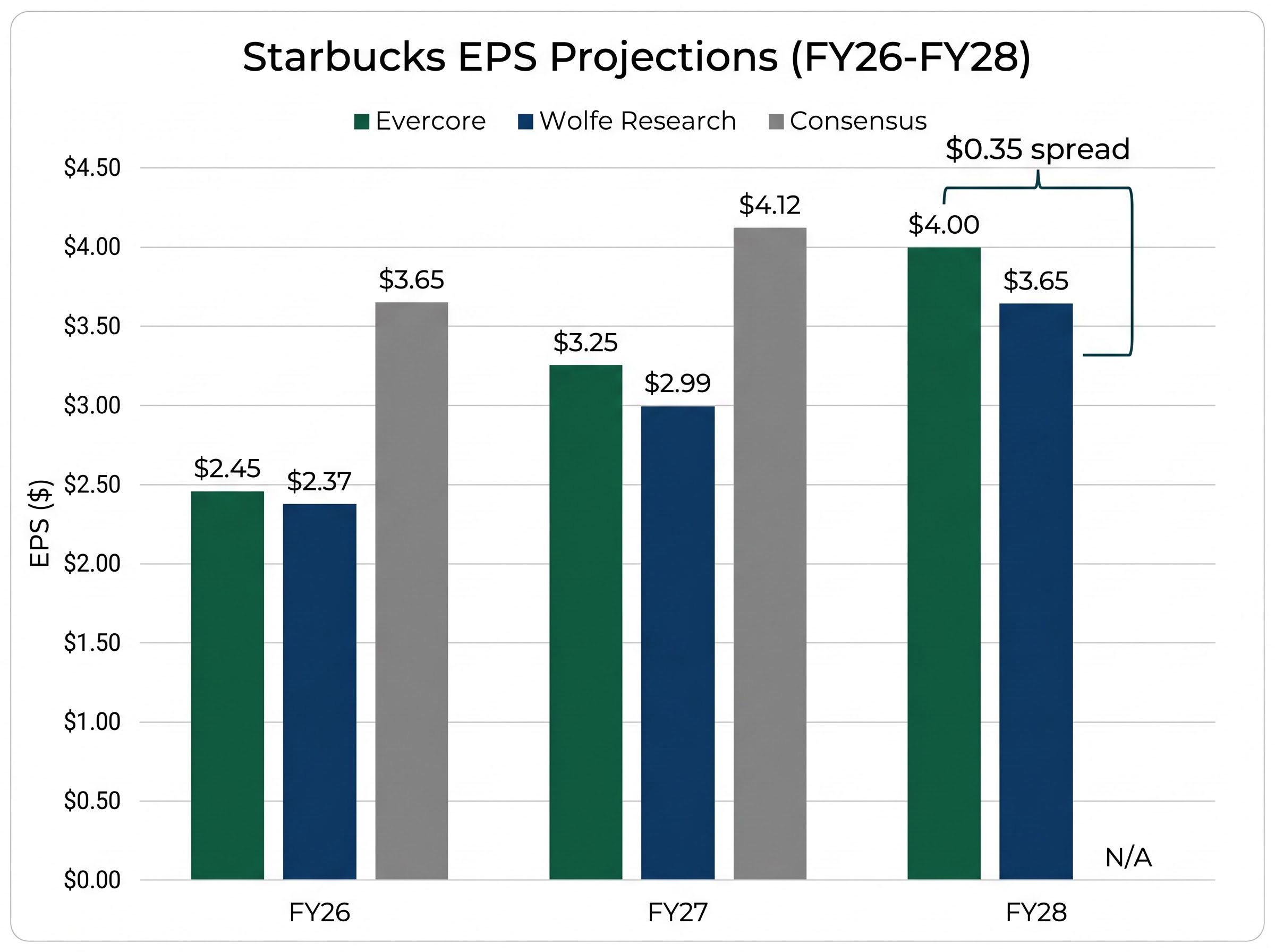

Wolfe’s revised EPS estimates sit below Evercore’s at every point in the forecast horizon:

| Fiscal Year | Evercore | Wolfe Research | Consensus |

|---|---|---|---|

| FY2026 | $2.45 | $2.37 | $3.65 |

| FY2027 | $3.25 | $2.99 | $4.12 |

| FY2028 | $4.00 | $3.65 | N/A |

The gap between Wolfe’s $3.65 FY2028 EPS estimate and Evercore’s $4.00 reflects genuine uncertainty about the pace of cost normalisation and initiative execution. That $0.35 spread is the range investors should stress-test.

Wolfe’s specific focus is on two product and programme catalysts:

The broader consensus reflects the balanced positioning: an average price target of approximately $102.77, with a Hold rating distribution of 12 Buy, 14 Hold, and 1 Sell.

The analyst projections from Evercore and Wolfe rest on assumptions that remain unproven. Each assumption carries a specific failure mode.

Structural competitive pressure from Dutch Bros and McDonald’s McCafe has contributed to Starbucks’ U.S. market share declining to approximately 48% from 52% in 2023, a headwind that sits alongside the cost-side risks and could constrain the top-line growth rate that Evercore’s margin model depends on.

The distance between the current 9.4% adjusted operating margin and the 15-18% FY2028 corporate target illustrates the scale of execution required. That gap represents 560-860 basis points of margin expansion in roughly two years.

The consensus Hold rating, with the average target of approximately $102.77 sitting only modestly above the $98.67 close, reflects a market that sees the turnaround as plausible but far from certain.

Evercore’s $115 price target represents approximately 16% upside from the 28 April close. That target is built on an FY2028 EPS of $4.00 and the assumption that incremental margins inflect sharply in FY2027.

Wolfe’s more conservative FY2028 estimate of $3.65 implies more modest upside at current valuation multiples. The broader analyst range extends from JP Morgan’s $100 target to Bank of America’s $130, illustrating the width of conviction.

The current price sits near consensus fair value. Three conditions would validate the bull case and shift the stock toward the upper end of that range:

Q3 FY2026 earnings represent the first major data checkpoint. The specific metrics to monitor are loyalty membership figures, Energy Refresher revenue contribution, and North America incremental margin trajectory relative to the full-year guidance raise.

No post-28 April analyst updates from additional firms have emerged as of 29 April 2026, a near-term data gap that may resolve in the coming days as research teams publish responses to the Q2 results.

The investment thesis, as both Evercore and Wolfe have framed it, is not a trade on near-term margin recovery. It is a multi-year position on whether Niccol’s operational reset produces the EPS compounding that would justify a premium multiple through FY2028. The Q2 results moved the probability. They did not remove the uncertainty.

The multi-year earnings compounding thesis that Evercore is building for Starbucks has a structural parallel in how JPMorgan and Oppenheimer are currently framing T-Mobile: a near-term target cut paired with unchanged long-term conviction, where the investment case rests on whether a $2.7 billion cost reduction programme delivers on schedule rather than on any single quarter’s results.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Starbucks reported 6.2% global comparable sales growth and 4.4% North America transaction volume growth, exceeding consensus expectations and signaling a clear inflection point in its performance.

Incremental operating margin measures the proportion of each additional revenue dollar that flows through to operating profit after variable costs. For Starbucks, it signals the rate of change in profitability during its recovery, even if overall operating margins remain compressed.

Significant risks include the permanence of labor costs, ongoing wage inflation, potential commodity price volatility, and execution challenges in achieving the $2 billion productivity savings target by FY2028.

Evercore projects a more aggressive margin inflection in FY2027, leading to a higher FY2028 EPS estimate of $4.00, while Wolfe Research's more conservative outlook places FY2028 EPS at $3.65, focusing on loyalty and new product catalysts.

Investors should monitor loyalty program engagement data, revenue contribution from the Energy Refresher launch, and the trajectory of North America incremental margins during Q3 FY2026 earnings.