Why AI Is Pushing Memory Chip Prices Higher Through 2028

2 hrs ago

Starbucks shares surged approximately 5% in extended trading on 28 April 2026 after the company posted its strongest North American transaction growth in roughly three years, a result that suggests CEO Brian Niccol’s turnaround strategy is gaining measurable traction. The beat arrives at a moment when Starbucks stock had been under sustained pressure from declining U.S. market share, intensifying competition from Dutch Bros and McDonald’s, and investor scepticism about whether the “Back to Starbucks” programme could deliver results within a difficult consumer environment. What follows is a breakdown of what the Q2 numbers showed, what drove the recovery, why management raised guidance, and what Wall Street analysts now project for SBUX through fiscal 2028.

The after-hours move was not a sentiment trade. It was a direct response to a quarter that beat on nearly every metric Wall Street was watching.

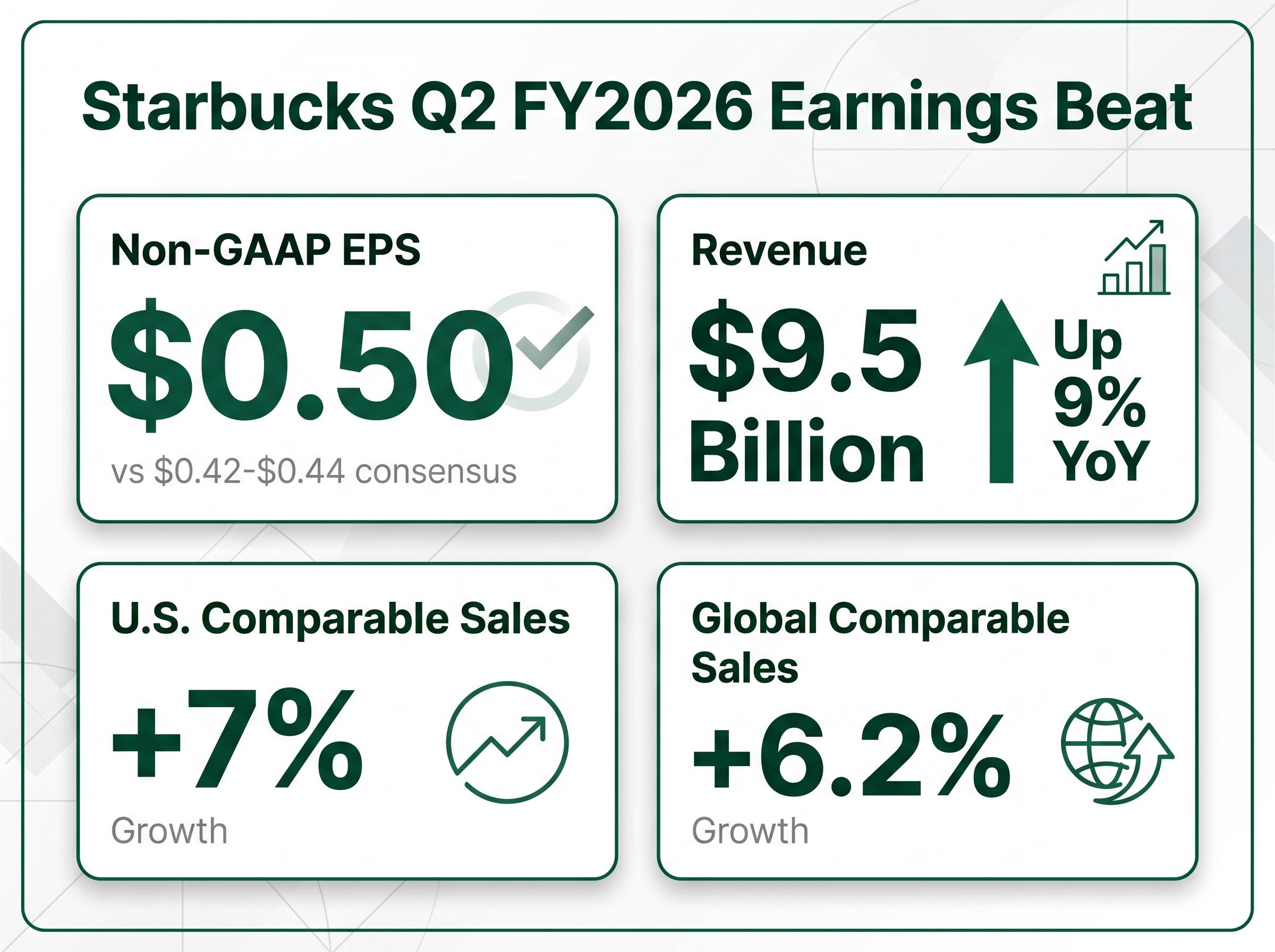

Non-GAAP EPS: $0.50 versus a Wall Street consensus range of $0.42-$0.44, the widest positive surprise in Starbucks’ recent quarterly history.

That closing price placed SBUX within striking distance of its 52-week high of $104.82, a level the stock has not sustained since the competitive pressures began eroding investor confidence. For context, the 52-week low sat at approximately $75.50, meaning the stock has recovered more than 35% from its trough.

The breadth of the beat is what gives it weight. Revenue, earnings, and comparable store sales all came in above expectations, and the traffic data confirmed that the improvement is demand-driven rather than price-driven.

| Metric | Q2 FY2026 Result | Prior Year / Consensus | Change or Beat |

|---|---|---|---|

| Consolidated Revenue | $9.5 billion | $8.7 billion (prior year) | Up 9% YoY |

| GAAP EPS | $0.45 | $0.34 (prior year) | Up 32% YoY |

| Non-GAAP EPS | $0.50 | $0.42-$0.44 (consensus) | Beat by $0.06-$0.08 |

| U.S. Comparable Store Sales | +7% | N/A | Strongest in ~3 years |

| Global Comparable Store Sales | +6.2% | N/A | Broad-based recovery |

The 7% U.S. comparable store sales figure is the headline number for operational investors. Positive traffic growth for a second consecutive quarter confirms that the recovery is being driven by more customers walking through the door, not simply higher average ticket sizes. Back-to-back quarters of positive traffic separate a genuine demand recovery from a one-period anomaly.

Reuters reporting on the Q2 earnings beat confirmed that the revenue and comparable sales figures exceeded Wall Street expectations, with the publication noting the breadth of the outperformance as evidence that Niccol’s operational changes are translating into measurable financial results.

The Q2 beat did not arrive on the back of a favourable macro environment. It arrived because a specific operational programme, designed by Niccol and rolled out across the North American store base, is producing measurable results.

The core pillars of the “Back to Starbucks” plan include:

According to Evercore’s analysis, North America same-store sales have shown a 13-percentage-point improvement across the six most recent quarters, a trajectory that places the Q2 result within a sustained recovery arc rather than an isolated beat. The positive traffic growth for a second consecutive quarter is the direct outcome metric that ties the strategic inputs to financial results.

For investors assessing durability, the fact that many of these initiatives are still in early deployment stages carries a specific implication: margin expansion should follow as the reinvestment phase matures.

A company that beats and raises in the same quarter is making a specific statement: the outperformance was not a one-time event, and management has enough visibility into the second half to commit publicly to higher targets. Guidance raises are among the most direct signals management provides about near-term business trajectory.

| Metric | Prior Guidance | Updated Guidance |

|---|---|---|

| EPS Range | $2.15-$2.40 | $2.25-$2.45 |

| Global Comparable Sales Growth | Above 3% | At least 5% |

The comparable sales revision from above 3% to at least 5% is not a token adjustment. It represents a meaningful step-up in management’s confidence that the traffic recovery can sustain through the fiscal year’s second half. The revision follows two consecutive quarters of positive traffic growth, giving the raised targets a data foundation rather than aspirational framing.

The analyst reaction was broadly positive, but the forward projections reveal meaningful divergence on how quickly margin expansion will materialise, a split that reflects genuine uncertainty about the turnaround’s next phase.

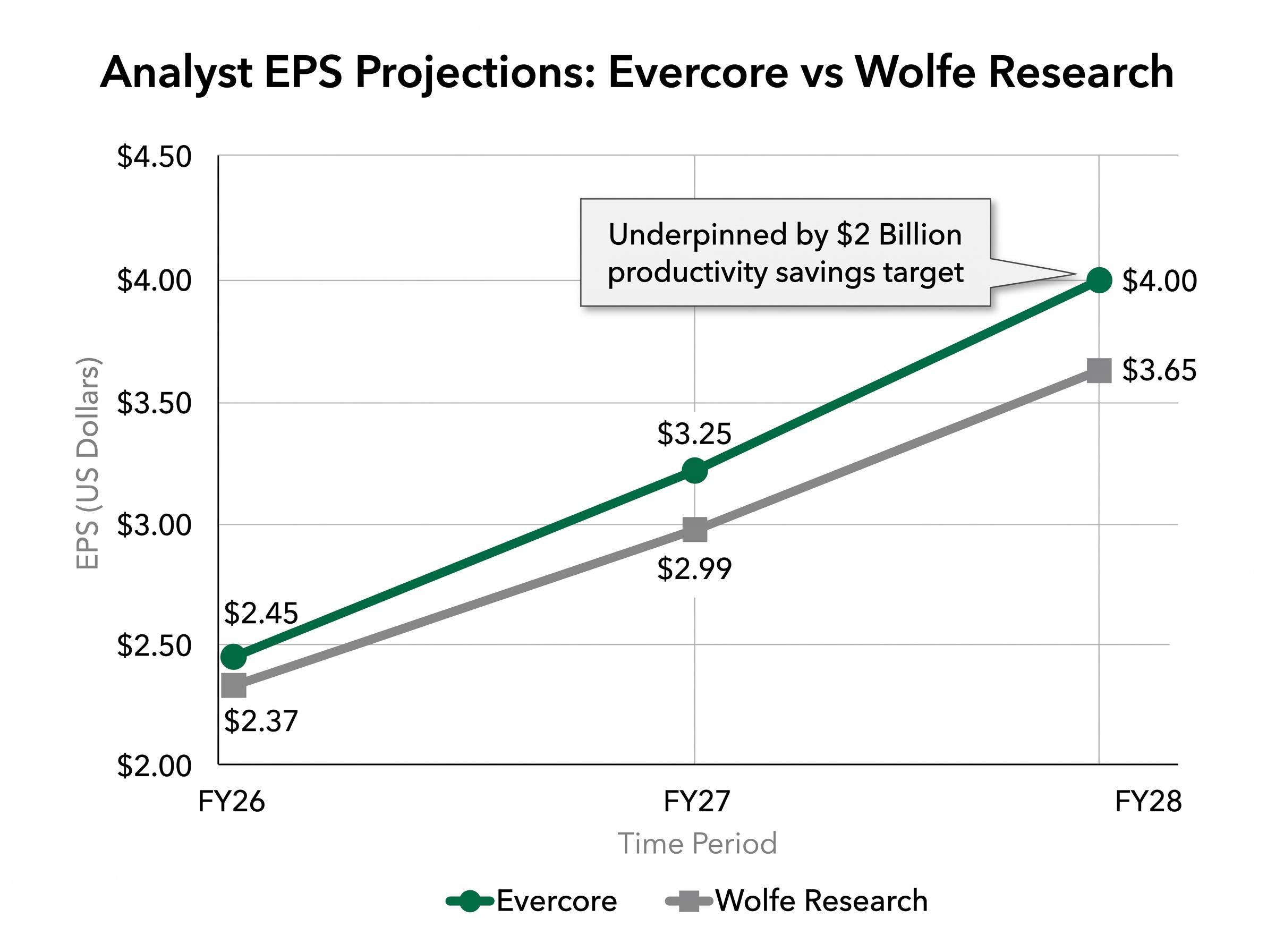

Goldman Sachs led the bullish response, raising its price target to $180 following the earnings release. Evercore maintained its Outperform rating and lifted its price target to $115 from $110, while raising its FY26 EPS estimate to $2.45 from $2.30. Evercore’s multi-year trajectory projects FY27 EPS of $3.25 and FY28 EPS of $4.00, underpinned by a $2 billion productivity savings target by FY28.

Evercore projects North America incremental margins exceeding 50% in FY27, compared with an estimated negative 7% in FY26, a margin inflection that represents the core of the multi-year bull case.

Wolfe Research offered a more conservative trajectory, estimating FY26 EPS of $2.37, FY27 of $2.99, and FY28 of $3.65. Wolfe noted encouraging early signals from the March loyalty programme overhaul and the April Energy Refresher product launch as additional forward catalysts.

| Analyst Firm | FY26 EPS Estimate | FY27 EPS Estimate | FY28 EPS Estimate |

|---|---|---|---|

| Evercore | $2.45 | $3.25 | $4.00 |

| Wolfe Research | $2.37 | $2.99 | $3.65 |

| Starbucks Guidance | $2.25-$2.45 | N/A | N/A |

The gap between Evercore’s $4.00 and Wolfe’s $3.65 FY28 EPS estimates illustrates the range of outcomes still in play. That divergence centres on how quickly margin flow-through materialises, something Evercore explicitly flagged as still building.

One strong quarter confirms the turnaround is producing results. It does not reverse a structural market share decline that has been building for three years.

These pressures form the environment within which Niccol’s turnaround must prove durable. The Q2 beat demonstrates that the “Back to Starbucks” strategy can drive traffic recovery. Whether it can simultaneously reclaim lost market share against competitors who are still expanding is a different, longer-term question.

The National Coffee Association’s Spring 2026 consumer trends data shows away-from-home coffee consumption and specialty coffee demand both expanding, a backdrop that provides Starbucks with a structural tailwind even as it competes for share within a growing overall market.

The Q2 results established three things clearly: the earnings beat was broad-based, the traffic recovery is real, and management has enough confidence in the trajectory to raise guidance. For SBUX investors, those are genuine positives.

What remains unresolved is whether the reinvestment phase can transition into sustained margin expansion. Evercore’s projection of North America incremental margins exceeding 50% in FY27 represents the key forward catalyst. The $2 billion productivity savings target by FY28 is the multi-year proof point that would confirm the turnaround’s full thesis.

Evercore’s FY28 EPS estimate of $4.00 implies that the margin inflection, if it materialises, could nearly double earnings power from current levels within two years.

SBUX now trades within 2.5% of its 52-week high of $104.82. A sustained break above that level would likely require evidence that comparable sales growth above 5% is holding and that margin flow-through is beginning to appear in reported numbers. The Q2 beat was the proof of concept. The next several quarters will determine whether it was the beginning of a structural recovery or a high-water mark for the reinvestment phase.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst estimates and company guidance, are subject to change based on market developments and company performance.

Starbucks stock rose approximately 5% in extended trading on 28 April 2026 because the company beat Wall Street expectations on revenue ($9.5 billion, up 9% year-over-year), non-GAAP EPS ($0.50 versus a consensus of $0.42-$0.44), and U.S. comparable store sales (+7%), while also raising full-year guidance.

The Back to Starbucks plan is CEO Brian Niccol's turnaround strategy focused on improving in-cafe experiences, increasing barista pay, enhancing the menu, and driving customer visit frequency. Q2 FY2026 results suggest it is working, with North America same-store sales improving by 13 percentage points across the six most recent quarters and positive traffic growth recorded for a second consecutive quarter.

Goldman Sachs raised its price target to $180, while Evercore lifted its target to $115 from $110 and projects FY28 EPS of $4.00. Wolfe Research takes a more conservative view, projecting FY28 EPS of $3.65, with the divergence centering on how quickly margin expansion materialises.

Starbucks still faces meaningful competitive pressure from Dutch Bros and McDonald's McCafe, and its U.S. market share has fallen to approximately 48% from 52% in 2023. The key forward risk is whether the current reinvestment phase can transition into sustained margin expansion, with analysts divided on the speed of that inflection.

Starbucks raised its FY2026 EPS guidance range to $2.25-$2.45 from a prior range of $2.15-$2.40, and lifted its global comparable sales growth target to at least 5% from the previous target of above 3%, reflecting management confidence in the durability of the traffic recovery.