The Case for Copper and Battery Metals as Infrastructure Bets

6 hrs ago

Starbucks shares jumped nearly 6% after the close on 28 April as the company posted its strongest North America transaction growth in roughly three years, a milestone that signals the “Back to Starbucks” turnaround is moving from promise to measurable result. The beat matters because Starbucks has spent six quarters executing a costly reset under CEO Brian Niccol, absorbing labour reinvestment, menu simplification, and a loyalty programme overhaul while comparable sales lagged. Investors have been waiting for the moment when that spending starts converting into transaction volume. Q2 FY2026 appears to be that moment.

What follows breaks down exactly what drove the beat, what management revised upward in guidance, and what analysts are now projecting for margin recovery through FY2028, giving retail investors a complete picture of where the company stands today and what remains to be proven.

The post-market rally of approximately 5.84% on 28 April was not a reaction to a marginal beat. It was the market repricing a turnaround thesis that had spent six quarters accumulating doubt.

Non-GAAP earnings per share came in at $0.50, roughly 19% above the Wall Street consensus range of $0.42-$0.44. That gap between expectation and delivery is what moved the stock.

EPS beat: Non-GAAP EPS of $0.50 exceeded consensus estimates by approximately 19%, the widest positive earnings surprise Starbucks has delivered since the turnaround began.

The headline numbers confirm the scale of the outperformance:

For retail investors tracking consumer discretionary names, a near-6% post-earnings move on above-consensus EPS signals a meaningful sentiment reset, not just an in-line print.

North America comparable store sales rose 7.1% in the quarter. The breakdown is where the real signal sits.

| Region | Comparable Sales Growth | Transaction Growth | Average Ticket Growth |

|---|---|---|---|

| North America | +7.1% | +4.4% | +2.6% |

| Global | +6.2% | — | — |

Transaction volume growth, not just ticket inflation, is the indicator that separates genuine demand recovery from price-led revenue. A +4.4% transaction print after years of traffic erosion is the data point analysts pointed to as the quarter’s most telling signal.

This result did not appear in isolation. According to Evercore, North America same-store sales growth improved by 13 percentage points across the prior six quarters, a trajectory that reframes Q2 as the acceleration of a documented trend rather than an isolated event.

The Q2 print represents the point where accumulated operational changes started converting into foot traffic at measurable scale. That distinction, between a one-quarter anomaly and a trend inflection, is what gives the number its weight.

The turnaround strategy that CEO Brian Niccol has led since taking the role carries the internal label “Back to Starbucks.” For investors unfamiliar with the specifics, the plan involves three initiative categories, each targeting a different part of the customer experience and operating model:

The sequencing matters. These are not three initiatives launched simultaneously; they are layered investments activated over consecutive quarters, each building on the operational foundation laid by the previous one.

CEO Brian Niccol characterised the Q2 result as a “milestone” and a “turn in the turnaround,” framing the quarter as the point where accumulated investment began producing visible returns.

For investors evaluating whether the recovery is durable, the layered initiative timeline suggests multiple levers remain in early activation, with the loyalty programme and Energy Refresher still ramping.

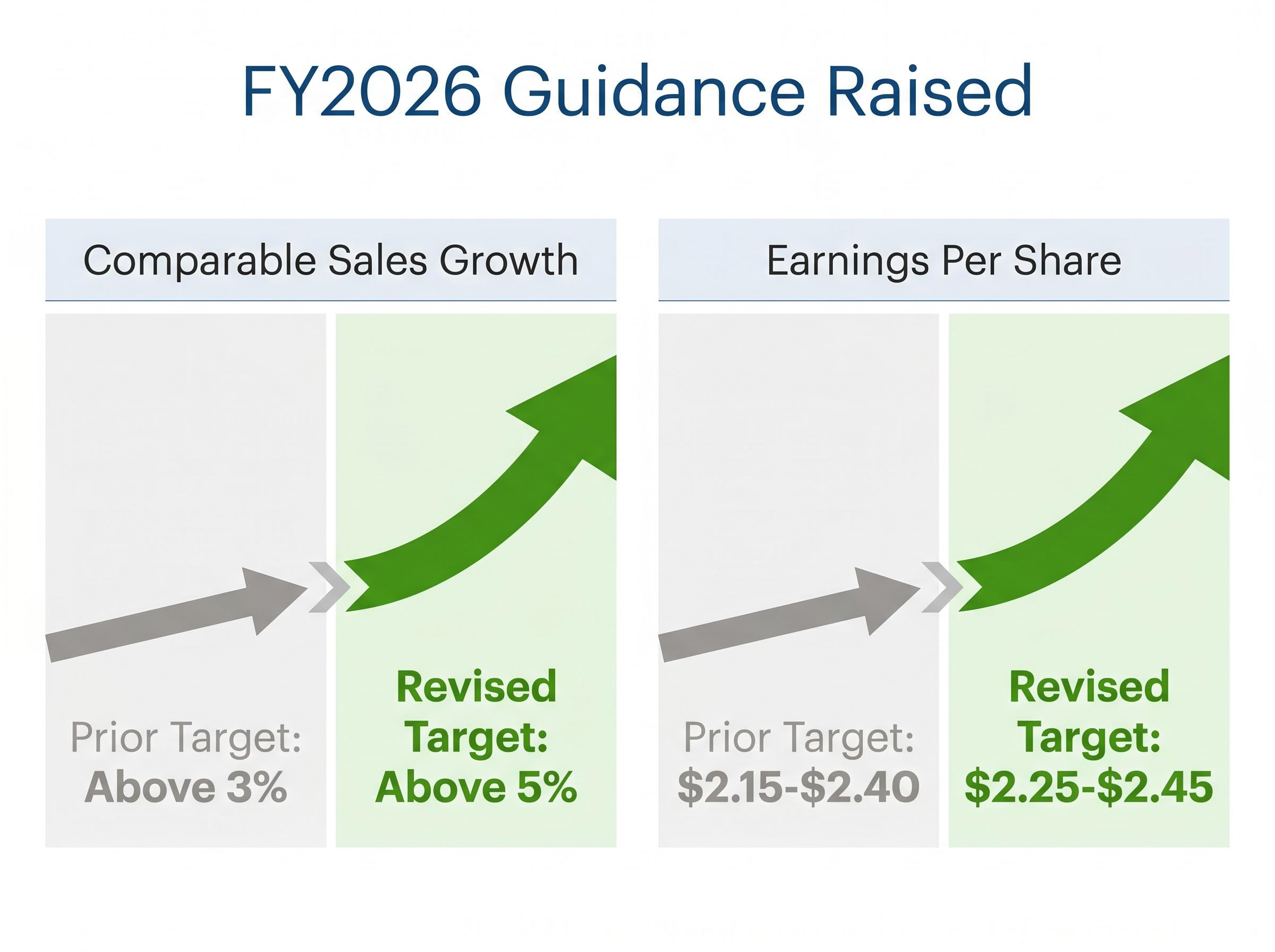

A mid-year guidance raise is not a routine update. It is a deliberate management statement that the original targets understate what the business is now delivering.

Starbucks revised both revenue and earnings guidance upward following the Q2 print:

| Metric | Prior Target | Revised Target |

|---|---|---|

| Comparable sales growth | Above 3% | Above 5% |

| EPS | $2.15-$2.40 | $2.25-$2.45 |

The comparable sales revision, from above 3% to above 5%, is a two-percentage-point raise on the metric investors have been watching most closely. The company attributed the increase to progress across its operational, marketing, and product programmes.

Both the revenue and EPS lines moved upward, indicating broad-based confidence across the income statement rather than a single-line improvement.

Evercore responded by raising its price target to $115 from $110, maintaining an Outperform rating. The firm lifted its EPS estimates across three fiscal years, and Wolfe Research followed with its own upward revisions.

| Firm | FY2026 EPS | FY2027 EPS | FY2028 EPS |

|---|---|---|---|

| Evercore | $2.45 (from $2.30) | $3.25 (from $3.09) | $4.00 (from $3.92) |

| Wolfe Research | $2.37 | $2.99 | $3.65 |

The bullish tone on revenue is broadly shared. The divergence sits in margin recovery timing.

Evercore projects North America incremental margins at negative 7% in FY2026, then exceeding 50% in FY2027, a swing that depends on cycling past labour reinvestment costs and realising $2 billion in projected productivity savings by FY2028.

That margin projection is the high-stakes claim in the current analyst debate. Wolfe Research’s more conservative FY2027 EPS estimate of $2.99 versus Evercore’s $3.25 reflects genuine uncertainty about the pace at which top-line recovery converts into bottom-line expansion. Analysts on both sides noted that margin flow-through remains in an early building phase.

The gap between those two estimates is where the investment thesis splits. One scenario requires labour costs to normalise on schedule and productivity savings to ramp by FY2028. The other assumes a slower trajectory.

Brian Niccol noted continuing positive momentum into April, with accelerating sales and margin improvements. That forward commentary is encouraging, but the next two quarters carry the burden of proof.

Three conditions would confirm Q2 as a genuine inflection rather than a one-quarter outperformance:

The cost-side pressures are specific. Labour reinvestment spending has compressed margins through the turnaround’s early phases, and coffee input price inflation remains a headwind. For Evercore’s FY2027 margin thesis to materialise, both pressures need to ease while productivity initiatives ramp.

The macroeconomic backdrop and intensifying competitive pressures add further complexity to the outlook. Revenue recovery is confirmed. Margin recovery is projected but not yet delivered.

Q2 FY2026 represents the strongest evidence to date that the “Back to Starbucks” strategy is converting operational investment into transaction volume. Three things were confirmed: a revenue beat of meaningful scale, transaction growth at a level unseen in roughly three years, and a mid-year guidance raise on both comparable sales and earnings.

One thing remains unproven: margin flow-through at scale. The story has moved from “will the turnaround work?” to “how fast will the margins follow?”

Q3 FY2026 results will be the next test. Post-earnings reactions from Goldman Sachs, JPMorgan, and Morgan Stanley were not yet available at time of publication; those updates could shift the broader institutional consensus on the margin timeline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Starbucks stock jumped nearly 6% after reporting non-GAAP EPS of $0.50, approximately 19% above Wall Street consensus, alongside North America comparable store sales growth of 7.1% and the strongest transaction volume growth in roughly three years.

The 'Back to Starbucks' plan is CEO Brian Niccol's multi-quarter turnaround strategy built around three pillars: labour reinvestment to improve in-store speed, a loyalty programme overhaul launched in March 2026, and new product launches such as the Energy Refresher in April 2026.

Starbucks raised its FY2026 comparable sales growth target from above 3% to above 5%, and lifted its EPS guidance range from $2.15-$2.40 to $2.25-$2.45, reflecting broad-based confidence across both the revenue and earnings lines.

Evercore projects Starbucks EPS of $2.45 in FY2026, $3.25 in FY2027, and $4.00 in FY2028, while Wolfe Research holds more conservative estimates of $2.37, $2.99, and $3.65 respectively, with the divergence driven by differing views on how quickly margin recovery will materialise.

The key unresolved risk is margin recovery: labour reinvestment costs continue to compress margins, and Evercore's bullish FY2027 thesis depends on cycling past those costs and realising $2 billion in productivity savings by FY2028, a target that has not yet been delivered.