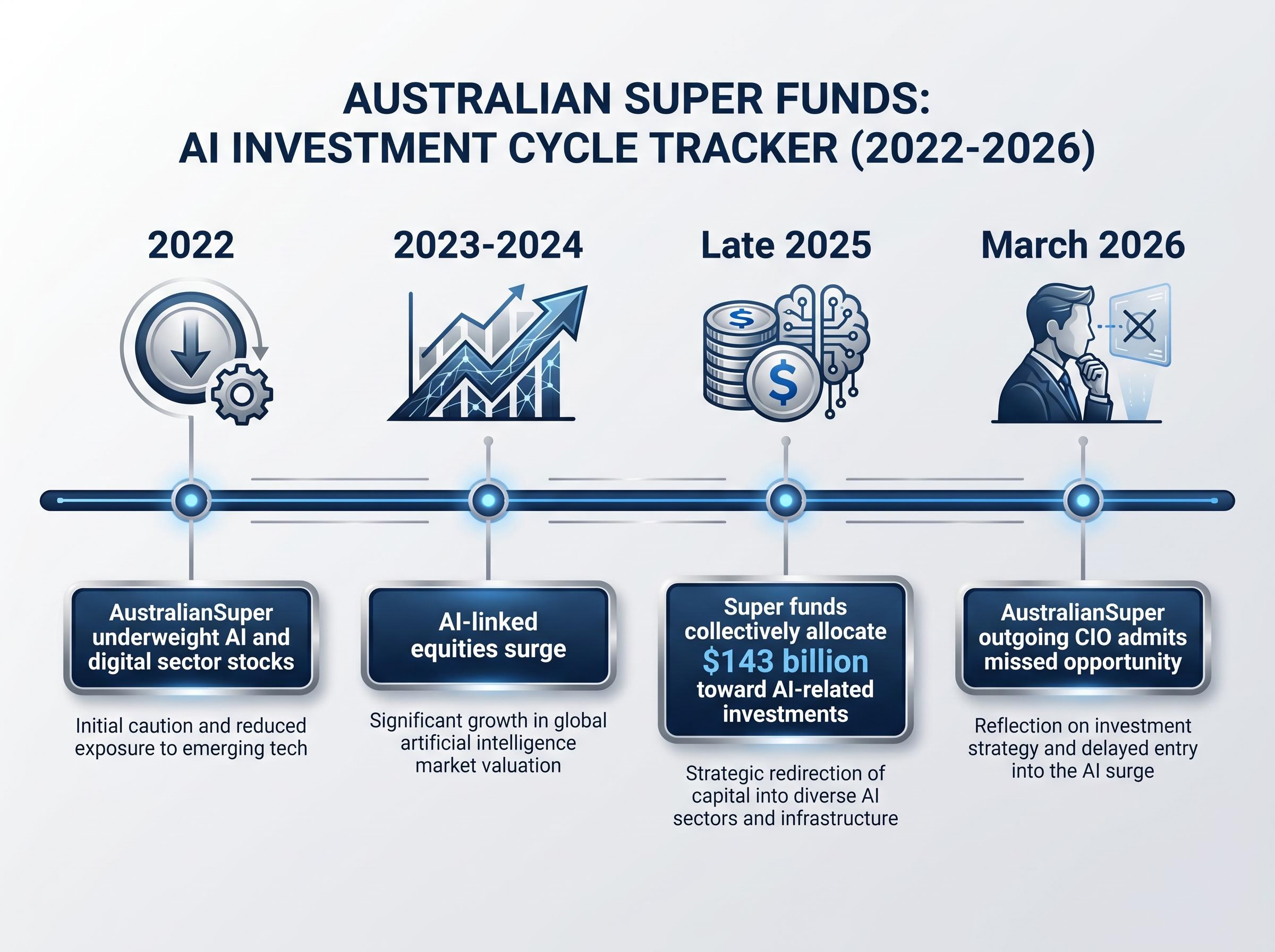

When AustralianSuper’s outgoing Chief Investment Officer admitted in March 2026 that the fund had missed significant gains by underweighting AI and digital sector stocks from around 2022 onwards, it was a rare moment of candour in an industry built on projecting confidence. The admission arrived during a period when Australian super funds were quietly repositioning portfolios as Middle East hostilities sent oil prices swinging 5-10% intraday and equity markets whipsawed through a 10% decline and recovery in early 2026. Publicly, funds described this activity as “harvesting volatility” or “raising liquidity to exploit opportunities.”

This analysis examines what the evidence shows about how Australia’s largest super funds behave during periods of elevated volatility, why their communication with members is structurally unaccountable, and what the research says about whether any of it adds value for the 16 million Australians whose retirement savings sit within the system. The super fund investment strategy that members are told they have may not be the one their fund is actually running.

How super funds dress up market timing in sophisticated language

The language is worth examining closely. In recent months, major Australian super funds have used a specific vocabulary when describing portfolio activity triggered by geopolitical developments, from the escalation of the Iran conflict to shifting tariff policy under the Trump administration. The phrases share a common quality: they describe action without committing to a falsifiable position.

Consider the translations:

- “Harvesting volatility”: buying or selling assets in response to short-term price movements, which is market timing.

- “Raising liquidity to exploit opportunities”: selling existing positions to build cash reserves for future deployment at lower prices, which is a directional bet that prices will fall further.

- “Tactical repositioning around geopolitical risk”: adjusting portfolio weights based on a view about how a specific event will affect markets, which is market timing with a geopolitical label.

An April 2026 report in the Australian Financial Review, titled “Here’s how your super fund is trading Trump 2.0,” documented specific fund behaviours: certain funds raising equity allocations, others building cash reserves for rapid deployment. The activity was framed as sophisticated risk management, yet each decision implied a directional market view.

The contradiction sits at the centre of how large super funds communicate. They promote active management expertise as a competitive advantage to attract and retain members. At the same time, they describe their portfolio decisions in language vague enough to avoid scrutiny if those decisions prove costly. Making portfolio changes in response to near-term geopolitical developments, whether tariff announcements or conflict escalation, meets the definitional threshold for tactical market timing regardless of the label applied.

When big ASX news breaks, our subscribers know first

The structural reasons large funds cannot time markets reliably

Investment Magazine reported in March 2026 that AustralianSuper’s outgoing CIO acknowledged the fund regretted underweighting AI and digital sector stocks, tracing the missed opportunity back to approximately 2022.

That admission deserves more than a headline. Holding a below-benchmark weight in a sector is itself a directional bet: an implicit call that the market’s valuation of that sector is excessive. When AI-linked equities surged through 2023 and 2024, that underweight position cost members returns they would have captured simply by maintaining benchmark-level exposure. No sophisticated analysis was required. The market’s own weighting would have done the work.

The scale of the subsequent correction is telling. By late 2025, Australian super funds had collectively allocated an estimated $143 billion toward AI-related investments, according to the Australian Financial Review. The repositioning that followed the earlier miss was enormous, yet it came after the bulk of the gains had already been priced in.

The market efficiency problem

The structural challenge is not unique to AustralianSuper. When a geopolitical event becomes visible to a fund’s investment team, it is simultaneously visible to millions of other market participants processing the same information. Responses that previously unfolded over months now occur within hours. The ceasefire announcements, blockade developments, and diplomatic talks during the Iran conflict period shifted almost continuously, meaning any tactical repositioning required multiple sequential calls, each of which had to be correct.

Consistently making correct timing calls requires not just being right, but being right before the market is. For any single institution, regardless of its research budget or global network, that is an exceptionally high bar. The CIO admission illustrates this is the structural reality of active management, not an exception to it.

The market efficiency problem facing large super funds has been sharpened by the arrival of zero execution lag among retail participants: geopolitical signals that once took weeks to propagate through investor behaviour now move prices within hours, compressing the window in which any institution can act on information the market has not already absorbed.

CFA Institute research on active management outcomes identifies market efficiency as the structural barrier that prevents most active managers from consistently outperforming, reinforcing why the information advantage required to time geopolitical events correctly is effectively unavailable to any single institution, regardless of its resources.

The compounding costs of elevated portfolio turnover

The cost of getting timing calls wrong, or even getting them right but executing them expensively, is not abstract. Elevated portfolio turnover generates specific cost categories that compound over time.

| Cost Category | How It Arises | Visibility to Member | Potential Long-Term Impact |

|---|---|---|---|

| Transaction costs | Brokerage, settlement, and execution fees on each trade | Often embedded within investment management fees; not separately itemised | Persistent drag that compounds across decades of accumulation |

| Price impact | Large-volume trades move prices against the fund, particularly in less liquid markets | Not disclosed; absorbed into portfolio returns | Larger funds face proportionally greater impact costs |

| Mistimed entries and exits | Buying after a rally has occurred or selling after a decline, locking in losses | Visible only in aggregate return figures over time | Single mistimed calls (such as the AI underweight) can cost years of outperformance |

| Cash drag | Holding elevated cash reserves earns lower returns than invested capital during rising markets | Not typically separated from investment return reporting | Opportunity cost during sustained equity rallies reduces terminal balance |

These costs are governed by the following disclosure and accountability frameworks:

The reactive trading costs that compound most severely are not always the most visible: transaction fees and settlement charges are measurable, but the CGT discount forfeited on positions sold within 12 months and the opportunity cost of missing recovery sessions together account for the majority of long-run return drag identified in behavioural finance research on Australian retail investors.

The ASIC Regulatory Guide 97 fee disclosure requirements determine precisely which cost components funds must itemise in Product Disclosure Statements and which can be buried within aggregate investment management fees, a distinction that directly shapes how much of the true cost of active management is visible to members.

- ASIC Regulatory Guide 97 (RG 97) sets the requirements for fee and cost disclosure in Product Disclosure Statements, determining what funds must and must not show members.

- APRA’s annual superannuation performance test assessed 52 MySuper products in 2025, providing the primary mechanism for benchmarking whether active management decisions are producing value over time.

For a member in a balanced super option, even small persistent return drags from unnecessary trading activity compound over a 30-40 year accumulation phase into materially lower retirement balances. Some funds cited in reporting have themselves acknowledged that refraining from action is frequently the optimal strategy during elevated volatility, while simultaneously repositioning.

Understanding how super funds are actually structured to invest

The communication from large super funds often implies a degree of tactical agility that their portfolio structures do not support. Understanding what sits inside these portfolios recalibrates expectations about what responsiveness is actually possible at scale.

Large industry funds allocate significant portions of their portfolios to illiquid private markets assets: infrastructure, property, and private equity. These holdings cannot be sold within days or weeks in response to a geopolitical development. They are long-duration commitments, often locked for years, that generate returns through operational performance rather than market pricing.

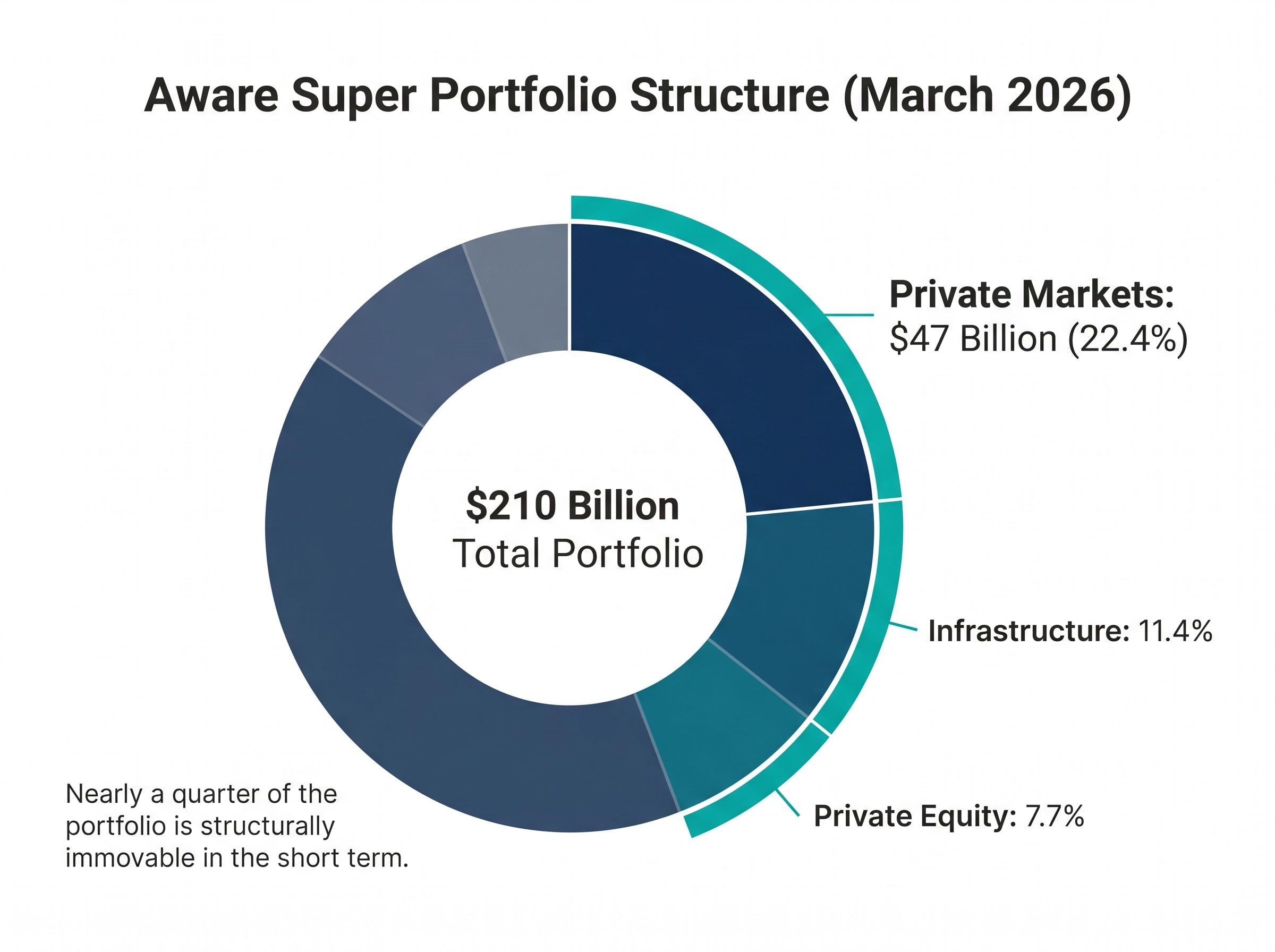

Aware Super’s portfolio as of March 2026 illustrates the point. The fund manages $210 billion in total, with approximately $47 billion (roughly 22.4%) allocated to private markets. Within that allocation, 11.4% sits in infrastructure and 7.7% in private equity. Nearly a quarter of the portfolio is structurally immovable in the short term.

| Fund | Portfolio Size | Private Markets Allocation | Stated Investment Philosophy |

|---|---|---|---|

| Aware Super | $210 billion | ~22.4% ($47 billion) | Whole-of-fund model with significant private markets focus |

| AustralianSuper | Australia’s largest fund | Significant (undisclosed breakdown) | Long-horizon diversified allocation with dedicated liquidity management |

| Vanguard Super | Smaller scale | Minimal | Simplicity, transparency, and low cost |

Why scale makes tactical agility harder, not easier

AustralianSuper’s appointment of a Chief Liquidity Officer reflects the scale challenge directly. The infrastructure being built is designed to manage the complexities of large illiquid portfolios, ensuring the fund can meet member withdrawals and operational requirements. It is not infrastructure for rapid tactical trading.

Large funds moving significant capital in and out of listed positions create their own price impact, particularly in smaller or less liquid Australian markets. A fund managing hundreds of billions of dollars cannot reposition meaningfully around a ceasefire announcement without moving the market against itself. The Iran conflict period, where diplomatic signals shifted almost continuously, would have required multiple sequential timing calls, each correct, each executed without excessive market impact. At this scale, the physics of capital deployment work against tactical agility.

The accountability gap between fund claims and member scrutiny

Phrases like “harvesting volatility” and “raising liquidity” share a useful quality for the institutions that deploy them: they provide no testable prediction. A member reading these phrases in a fund update cannot determine, after the fact, whether the decisions they described produced positive or negative outcomes.

The only consistent public market view super funds appear willing to express is an expectation of continued volatility. This is not a meaningful forecast. Some degree of market movement is always present, making an expectation of volatility essentially unfalsifiable.

Event-driven trading patterns among Australian retail investors in 2026 mirror the behaviour documented in large fund communications: volumes on the Selfwealth platform doubled during the April 2025 tariff announcement, then fell more than 20% after the March 2026 RBA rate hike, confirming that headline-reactive repositioning is not unique to institutional portfolios.

The structural imbalance runs deeper. Funds have access to granular portfolio data, trading records, and performance attribution analysis. Members receive periodic statements and communications that aggregate all of this into a single return figure. The gap between what the institution knows and what the member can evaluate is substantial.

APRA’s performance test (assessing 52 MySuper products in 2025) provides the primary available tool for evaluating active management outcomes, though it is a backward-looking 10-year aggregate measure. It captures whether a fund’s total active management programme delivered value over a long horizon. It does not capture whether individual tactical decisions during specific periods of volatility helped or hurt.

The October 2025 superannuation tax concession changes (effective July 2026), affecting balances over $3 million, add a further layer of complexity. Funds managing different member cohorts may adjust strategies in response, with limited transparency for affected members about how those adjustments are being made.

Median balanced option returns of approximately 9.3% in calendar year 2025 and approximately 10.5% in FY2025 are strong aggregate figures. They do not reveal whether active management contributed to or detracted from those outcomes.

Members seeking to probe their fund’s accountability can ask specific questions:

- What was the fund’s active management contribution (positive or negative) to total returns over the past 12 months?

- What percentage of the portfolio was tactically repositioned in response to geopolitical events during the 2025-2026 period?

- How do the fund’s total costs (including transaction costs and price impact) compare to a passive benchmark strategy?

- What is the fund’s portfolio turnover rate, and how does it compare to prior years?

Building a super strategy that performs without requiring correct predictions

The analytical thread running through each of the preceding sections converges on a single point. Super funds that need to be right about geopolitical events, sector rotations, and market timing calls to justify their fees are asking members to absorb risks that a simpler, cheaper strategy eliminates by design.

Chris Brycki, Founder and CEO of Stockspot, framed this directly in an investment update during the Iran conflict period in 2026: the greatest threat to retirement outcomes during volatile periods is not the volatility itself but the impulse to react to it.

That framing aligns with the structural evidence. Median balanced option returns of approximately 9.3% (calendar year 2025) and 10.5% (FY2025) were delivered by diversified portfolios without requiring correct calls on the Iran conflict, tariff policy, or AI sector timing. The returns came from broad market exposure, maintained through volatility.

The attributes of a long-term super strategy that does not depend on correct predictions are identifiable:

Broad diversification across asset classes and geographies, the first attribute of a strategy that does not depend on correct predictions, requires confronting ASX home bias directly: Australian investors historically overweight domestic equities relative to global markets, a concentration that increases exposure to exactly the sector and event risks a geopolitically-driven fund strategy attempts to navigate.

- Broad diversification across asset classes and geographies, reducing dependence on any single sector or event outcome.

- Cost minimisation, including low management fees and minimal portfolio turnover, to preserve the compounding advantage over decades.

- Systematic rebalancing back to target allocations, removing the temptation to make directional bets in response to headlines.

- Explicit acknowledgement of uncertainty, rather than communications that imply the fund can forecast geopolitical outcomes.

APRA’s performance test framework, while imperfect as a backward-looking aggregate measure, remains the available tool for evaluating whether active management is earning its keep. Members can use it as a starting point for comparing their fund’s outcomes against the benchmark a passive approach would have delivered.

Demanding better from funds managing your retirement

The evidence points in a consistent direction. Major Australian super funds are making tactical positioning decisions in response to geopolitical events, describing that activity in language designed to resist scrutiny, while the evidence base for such activity generating net value for members remains weak. The AustralianSuper CIO admission, the structural constraints of large illiquid portfolios, and the cost mechanics of elevated trading all point to the same conclusion.

Members have specific tools available. APRA’s MySuper performance test results compare funds against tailored benchmarks. RG 97 fee disclosures in Product Disclosure Statements reveal cost structures. Direct engagement with fund investor relations teams can surface the answers to the accountability questions outlined above.

The superannuation system was designed for long-term investing. Members are best served by funds that communicate with the same honesty and specificity they expect from the system’s regulators, not by funds that dress up short-term positioning as sophisticated strategy.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.