Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

42 mins ago

SK Hynix debuted on the Nasdaq on Friday, 11 July 2026 at an offer price of $149 per ADR, raising approximately $26.5 billion in the largest first-time U.S. listing by a foreign company. The stock closed its first session at $168.01, up roughly 13%. Forty-eight hours later, domestic shares in Seoul plunged as much as 15.4% intraday, the worst single-day decline in the company’s history, dragging the Kospi down approximately 9% and triggering a 20-minute market-wide trading halt.

The whipsaw is not a random event. It is the sharpest expression yet of a question that has been building across every AI chip equity for months: whether valuations that have priced in years of future growth can survive contact with present-day market mechanics. That question now collides with the start of Q2 2026 earnings season, which will deliver its own verdict on whether AI capital spending is still accelerating or beginning to plateau.

Here is what the two-session swing actually tells you, what structural forces amplified it, and the specific data points over the next fortnight that will determine whether this week marked a healthy reset or the start of something larger.

The debut numbers spoke for themselves. SK Hynix priced its ADR offering at $149, opened roughly 14% above that level on the Nasdaq (ticker: SKHY, initially SKHYV), and closed at $168.01, a first-day gain of approximately 12.76-13%. By any measure, it was the most successful foreign ADR debut in U.S. market history.

Then Seoul opened on Monday.

Domestic shares fell as much as 15.4% intraday, a decline that rippled across the broader Korean market. The Kospi dropped approximately 9%, forcing a 20-minute market-wide trading halt. Premarket Nasdaq 100 futures shed approximately 0.9%, a clear indication that the selloff would extend beyond Asian markets.

Market circuit breakers operate on a tiered threshold system across major exchanges: the U.S. framework triggers halts at 7%, 13%, and 20% S&P 500 declines, while Korea’s market-wide pause on Monday illustrates how individual country mechanisms differ in both threshold levels and halt duration.

SK Hynix shares fell as much as 15.4% in Seoul on 13 July 2026, the largest single-day percentage decline in the stock’s history.

Key metrics from the two-session sequence:

The 48-hour arc is not a contradiction. What U.S. investors priced in on Friday, Korean investors were forced to reconcile on Monday, and the scale of that reconciliation tells you just how far sentiment had stretched.

The gap between the two sessions was not a mystery. It was structural, and understanding the mechanics turns Monday’s rout from a shock into something closer to a predictable outcome.

Here is how the three-step arbitrage dynamic works:

After Monday’s decline, U.S. ADRs were still trading at a premium of several tens of percent to the Seoul-listed stock. That premium is itself a live data point. It tells you U.S. investors have not fully capitulated to the Korean market’s reassessment. Whether the premium narrows because U.S. ADR prices fall or because Korean prices recover will be the market’s revealed verdict on fair value over the coming sessions.

Before the listing, SK Hynix had already done something remarkable. Its market capitalisation peaked near $1.35 trillion. Shares were up more than 200% year-to-date and more than 600% over certain 12-month windows, driven almost entirely by one catalyst: surging demand for high-bandwidth memory (HBM) used in AI servers.

The company holds approximately 60% of global HBM market share by revenue, making it the single most concentrated bet on AI infrastructure spending anywhere in public equity markets.

Key valuation metrics before the rout:

Even the company’s own leadership saw the risk clearly.

SK Group’s chairman previously acknowledged that while the underlying AI industry is not itself a bubble, AI-related stocks have “increased too quickly and excessively” and should be expected to see corrections.

A stock up 600% in 12 months requires every subsequent piece of news to justify not just current operations but years of future growth already priced in. When even a record-breaking debut fails to extend the momentum, the path of least resistance becomes the exit. The surprise is not that it fell. The surprise is that it took this long.

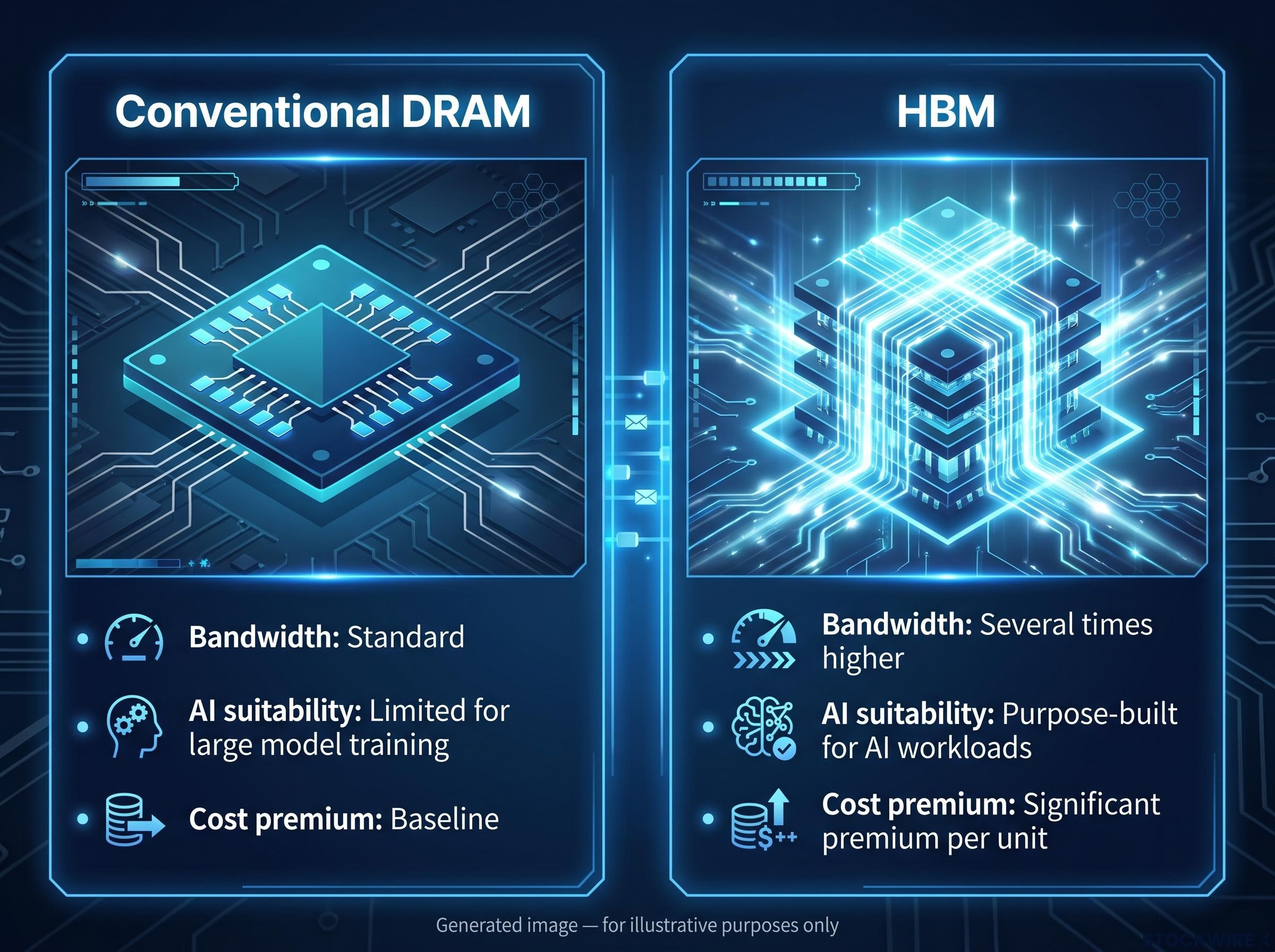

The AI models driving investment in companies like Nvidia have a bottleneck, and it is not processing power. It is memory bandwidth. As model sizes and training runs expanded over the past two years, conventional DRAM (the standard memory chip in most electronics) could not feed data to processors fast enough. The result was a compute traffic jam: processors sitting idle, waiting for data.

High-bandwidth memory, or HBM, solves that problem. It stacks multiple layers of memory chips vertically and connects them with high-speed pathways, delivering far more data per second than conventional DRAM. It is more expensive to produce, but for AI workloads, it is not optional.

| Attribute | Conventional DRAM | HBM |

|---|---|---|

| Bandwidth | Standard | Several times higher |

| AI suitability | Limited for large model training | Purpose-built for AI workloads |

| Cost premium | Baseline | Significant premium per unit |

Manufacturing HBM requires stacking and bonding memory dies with extreme precision, a process with high defect rates and steep learning curves. Only a handful of companies globally can produce it at scale, and SK Hynix holds roughly 60% of global HBM revenue as the primary supplier to Nvidia and other AI chip leaders.

DRAM supply constraints sit at the centre of SK Hynix’s bull thesis: SK Hynix projects a global shortage lasting through 2030, HBM inventory stands at just 3-4 weeks industry-wide, and all three major producers are fully sold out through 2026, a structural tightness that even $180 billion in planned annual capital expenditure cannot resolve quickly.

That manufacturing moat is the core of the bull thesis. Cloud providers and data-centre operators continue to commit capital to multi-year AI infrastructure builds, which means end-demand for HBM is structural and durable. The question for investors is not whether the business is sound. It is whether the stock price had already priced in years of that soundness in advance, which is a meaningfully different risk to manage.

The honest answer is that the evidence does not resolve cleanly into either camp.

| Bubble signals | Structural support |

|---|---|

| More than 600% gain over 12 months | Approximately 60% global HBM market share |

| Single-catalyst narrative (HBM as AI bottleneck) | Confirmed hyperscaler capex commitments |

| SK Group chairman’s own warning on AI stock excess | Multi-year foundry and equipment orders |

| Record single-day decline; Kospi contagion and halt | No negative earnings pre-announcement or guidance cut |

The bubble-consistent signals are real. Near-vertical appreciation driven by a narrow narrative, followed by a record selloff that dragged an entire national index lower, fits the pattern of sentiment-driven excess meeting gravity. The broader AI chip sector had already shown signs of fatigue in the weeks before the listing.

AI stock valuations across the semiconductor sector had already shown signs of strain before the SK Hynix listing: Broadcom fell approximately 15% in early July 2026 after reiterating, not cutting, its guidance, a pattern that illustrates how far sentiment had stretched ahead of any negative fundamental signal.

The counterevidence is equally real. There was no fundamental trigger for Monday’s decline: no earnings miss, no guidance cut, no customer cancellation. Demand for HBM remains structurally intact. The selloff was driven by positioning, arbitrage mechanics, and profit-taking after an extraordinary run.

The analytical consensus frames this as a high-beta correction in an overextended market leader rather than evidence that end-demand for AI memory or compute is collapsing.

Monday’s decline was driven by sentiment and positioning rather than a deterioration in orders or guidance. That means you should not conflate price behaviour with business health. But you also should not dismiss the valuation signal that a 15% drop sends.

Three specific signals will determine how this story is read by the end of the month:

These are not abstract indicators. They are the specific data points that will tell you whether Monday was a one-session event or the opening chapter of a broader AI chip repricing.

The two-session swing confirmed what the SK Group chairman had already said publicly: sentiment and positioning in AI chip stocks had outrun fundamentals, and a correction was overdue. That correction arrived with force.

What it did not confirm is any deterioration in the business itself. There has been no negative earnings signal, no guidance cut, no evidence of demand destruction for HBM. SK Hynix remains the dominant supplier in a market with structural, multi-year demand.

The appropriate posture through earnings season is specific rather than reactive. Watch TSMC and ASML guidance for the fundamental check. Track the ADR premium for the market’s revealed view on fair value. Read the broader Q2 numbers for the macro context. The next several weeks of earnings data will determine whether Monday’s rout was the correction the chairman anticipated or the opening move of something larger.

For investors wanting to weigh the structural support case in more depth, our dedicated guide to the semiconductor bubble debate covers Bank of America’s analysis of free cash flow yields, earnings revision momentum, and positioning data that collectively challenge the bubble framing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An ADR (American Depositary Receipt) is a U.S.-listed security that represents shares in a foreign company. Each SK Hynix ADR represents one-tenth of a Korean-listed common share, meaning 10 ADRs equal one domestic share, and pricing between the two markets is linked but not instantly synchronised.

Debut-day euphoria on the Nasdaq pushed SK Hynix ADR pricing well above domestic Korean valuations, and when Seoul reopened on Monday, local investors and arbitrageurs sold heavily to close that gap, triggering a 15.4% intraday decline and a 20-minute market-wide trading halt.

High-bandwidth memory (HBM) stacks multiple memory chips vertically to deliver far greater data throughput than conventional DRAM, making it essential for AI workloads. SK Hynix holds approximately 60% of global HBM revenue as the primary supplier to Nvidia and other AI chip leaders, making it the most concentrated public equity bet on AI infrastructure spending.

Three signals matter most: TSMC and ASML earnings guidance in the week of 13 July 2026 (the most direct check on AI capex health), the pace at which the SK Hynix ADR premium over Seoul-listed shares narrows, and the tone of broader Q2 2026 corporate guidance across banking, industrials, and technology.

SK Hynix raised approximately $26.5 billion at an offer price of $149 per ADR, making it the largest first-time U.S. listing by a foreign company in market history.