3 ASX Sector ETFs That Returned Up to 136% in One Year

13 mins ago

Australia’s share market has a concentration problem. Financials and materials dominate the S&P/ASX 200, which means a standard index allocation gives you heavy exposure to banks and iron ore but very little to the technology companies reshaping global commerce, security, and infrastructure.

Three BetaShares ETFs listed on the ASX offer a direct, rules-based answer to that gap. HACK targets global cybersecurity, ASIA captures Asian technology spanning hardware production and consumer platforms, and ATEC tracks domestically listed Australian technology businesses. All three are passive index products designed as satellite allocations, meaning they sit alongside a core portfolio rather than replacing it.

Here is what each fund actually holds, what it costs, how it has performed to 30 June 2026, and whether the combination makes sense as a complement to a standard ASX portfolio. The numbers tell a more nuanced story than any of the three headlines suggest.

The S&P/ASX 200 is built on banks and resources. That composition served Australian investors well during commodity supercycles and a housing boom, but it leaves a structural gap: technology exposure in a standard ASX index fund is a fraction of what a global benchmark delivers.

ASX 200 concentration risk is more pronounced than the index’s 200-stock label implies, with financials and materials together accounting for more than 50% of the index by market-cap weight, a structural feature that no amount of stock selection within the index can resolve.

Thematic technology ETFs solve this without requiring you to pick individual stocks across unfamiliar exchanges. They provide a pre-built, transparent basket of companies organised around a specific growth thesis, rebalanced according to published rules, and accessible through a single ASX brokerage account.

The three ETFs covered here each address a different dimension of that gap:

The shared structural thesis across all three is straightforward: economic value is migrating into digital environments, and that migration is a durable, multi-decade driver rather than a single-cycle phenomenon. The question is not whether technology exposure belongs in a portfolio. It is which segments, and with what risk profile.

Cybersecurity is no longer a peripheral IT line item. It has become a board-level governance obligation for corporations and governments alike. Every expansion of cloud infrastructure, every AI application deployed, every networked device added to a corporate environment widens the attack surface that needs protecting. That spending is structurally non-discretionary: companies cannot defer it the way they might defer a marketing budget or a facilities upgrade.

The IDC global cybersecurity spending forecast projects total security spend to exceed $308 billion in 2026, growing at 11.8% annually, with AI-driven security platforms and rising cyberattack frequency identified as the primary structural demand drivers underpinning that trajectory.

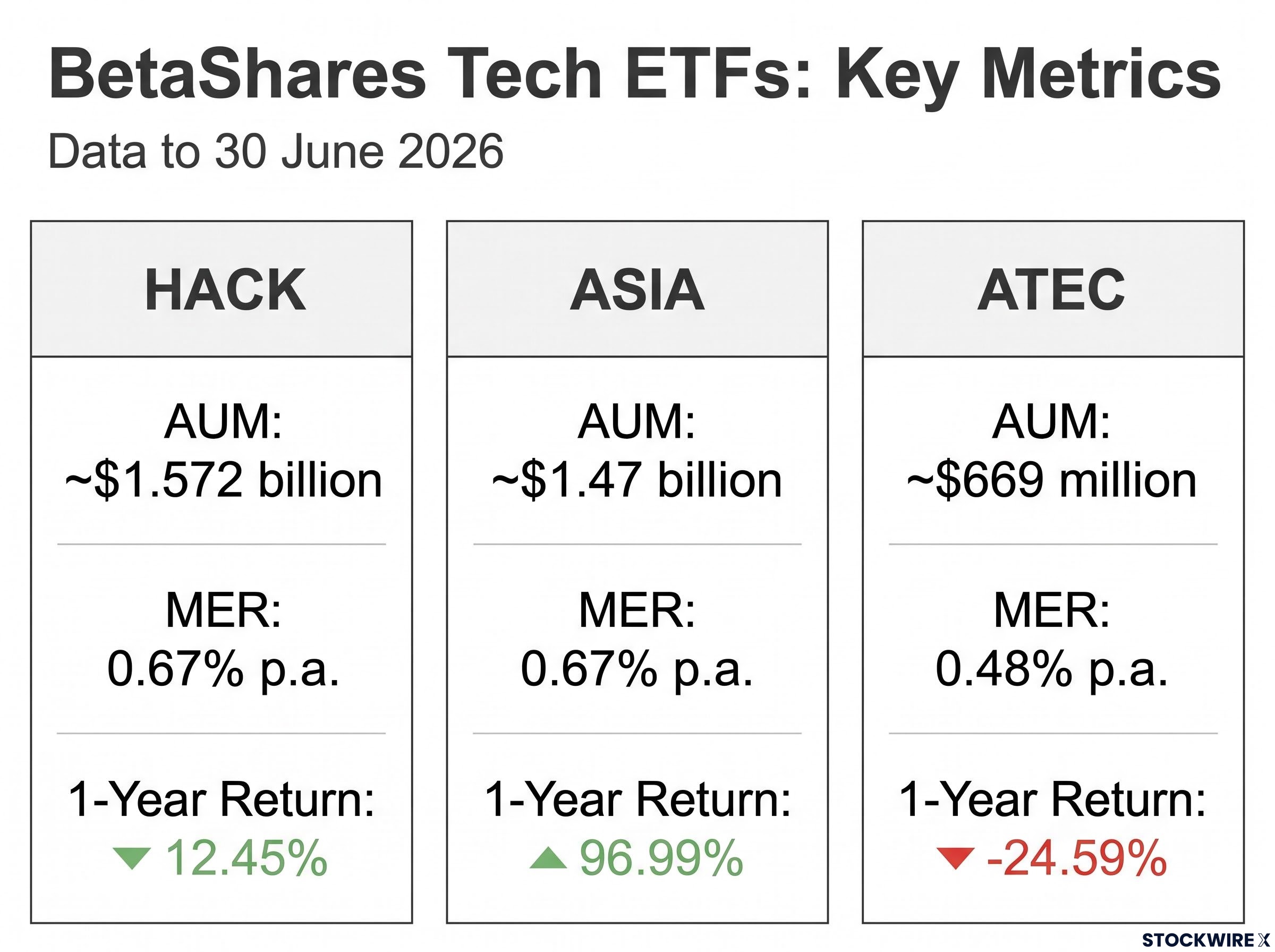

HACK tracks the Nasdaq Consumer Technology Association Cybersecurity Index (AUD), a basket of global companies involved in cybersecurity hardware, software, and services. The portfolio tilts heavily toward systems software and electronic technology, with technology services representing more than 76% of holdings and electronic technology at approximately 21%. Geographic exposure is predominantly US and North American. Representative holdings include Palo Alto Networks (NASDAQ: PANW) and Fortinet (NASDAQ: FTNT).

Key stats:

Since inception, HACK has returned 18.41% p.a. after fees, assuming reinvestment of distributions. Past performance is not indicative of future performance.

The 23.92% three-year annualised return is compelling on its face, but it comes from a fund concentrated in a single niche of the technology economy. If cybersecurity spending growth slows or valuations compress across high-multiple software names, HACK has limited diversification to absorb the impact. Unhedged USD exposure adds another layer: when the Australian dollar strengthens against the US dollar, your AUD-denominated returns take a hit regardless of what the underlying stocks do.

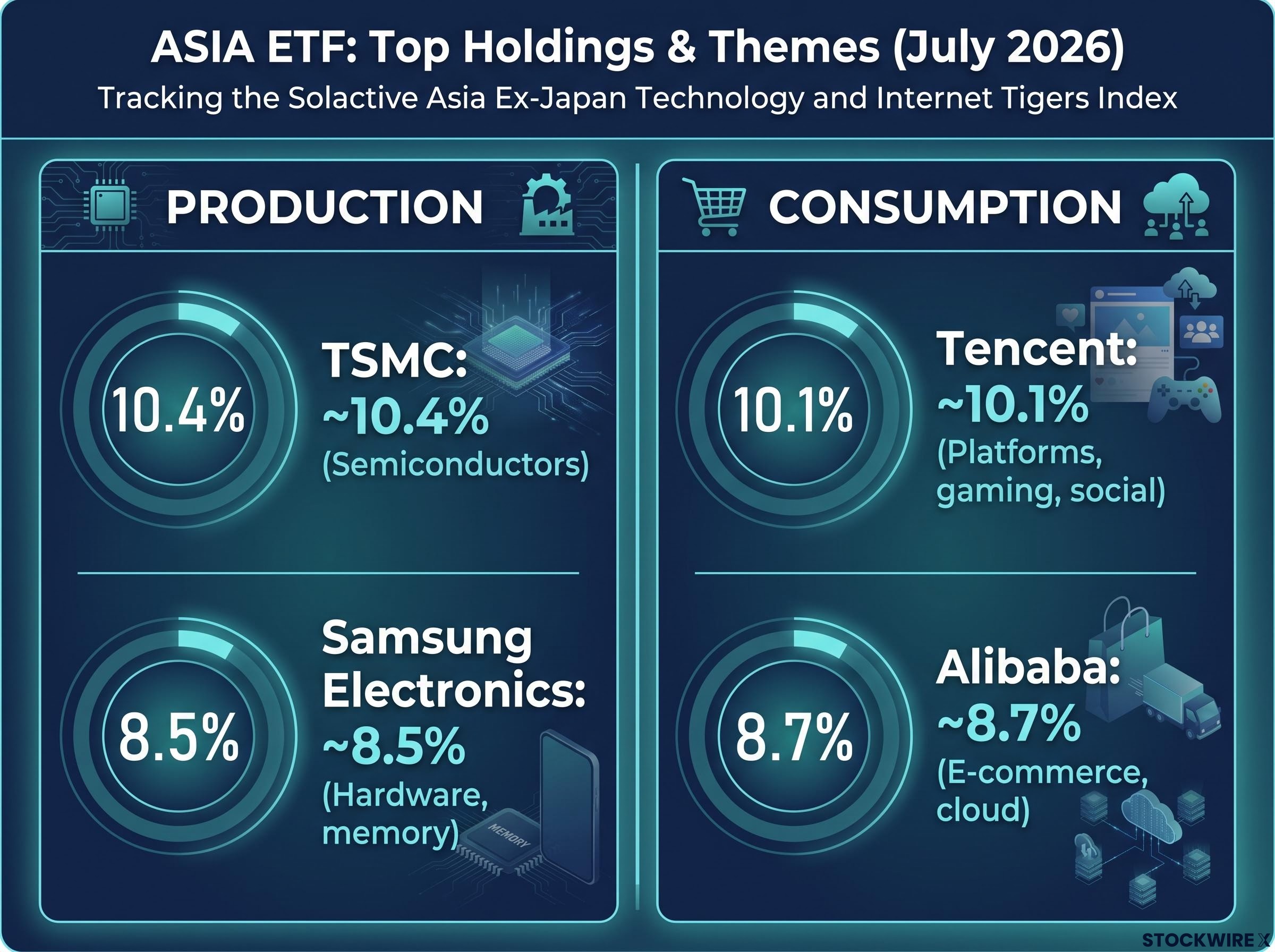

The Asian region sits at the centre of the global technology economy from two distinct angles. It is the manufacturing base for the semiconductors, memory chips, and hardware that the world’s digital infrastructure depends on, while simultaneously hosting enormous populations that are embracing e-commerce, social platforms, gaming, and cloud services in growing numbers. ASIA captures both dimensions in a single fund.

Key stats:

The fund tracks the Solactive Asia Ex-Japan Technology and Internet Tigers Index, and its top holdings illustrate meaningful concentration in a handful of mega-cap names:

| Holding | Approximate Weight | Segment |

|---|---|---|

| TSMC | ~10.4% | Semiconductors (production) |

| Tencent | ~10.1% | Platforms, gaming, social (consumption) |

| Alibaba | ~8.7% | E-commerce, cloud (consumption) |

| Samsung Electronics | ~8.5% | Hardware, memory (production) |

Individual holding weights are approximate and sourced from fund data as at July 2026.

Representative holdings include Tencent Holdings (operator of WeChat) and Baidu (NASDAQ: BIDU).

A 96.99% one-year return and a 47.82% three-year annualised return are exceptional numbers. They also reflect a recovery in Asian technology valuations rather than a baseline expectation you should project forward. The geopolitical environment that drove earlier underperformance has not fundamentally resolved.

China’s regulatory crackdowns on technology platforms, which affected Tencent and Alibaba during 2021-2022, are a live risk category rather than a resolved one. Beijing’s willingness to intervene in the operations and valuations of its largest technology companies remains a structural feature of the market, not an anomaly.

Taiwan-related geopolitical tension creates a specific risk pathway for TSMC, which is the fund’s largest single holding. Any escalation in cross-strait tensions could reprice the entire semiconductor supply chain overnight.

Asian semiconductor valuations have already demonstrated this repricing speed in practice: Kioxia fell more than 14% and SK Hynix lost 6.6% in a single session on 1 July 2026, wiping weeks of AI-rally gains on catalysts that did not confirm any actual cut in AI infrastructure spending.

The practical implication: investors should be prepared for periods of double-digit drawdowns, including potentially negative annual returns. This fund is not suitable for short-term trading.

If the core argument for technology ETFs is diversifying away from the ASX’s bank and resources concentration, ATEC makes that argument at the domestic level. The fund tracks the S&P/ASX All Technology Index, giving exposure to Australian-listed technology and technology-enabled businesses spanning SaaS, digital marketplaces, logistics software, payment services, and data centres.

Key stats:

At 0.48%, ATEC carries the lowest management fee of the three funds, which makes it comparatively attractive as a domestic technology satellite. But the performance numbers demand honest assessment.

| Holding | ASX Code | Approximate Weight | Subsector |

|---|---|---|---|

| Xero | XRO | ~12.3% | SaaS / accounting software |

| WiseTech Global | WTC | ~11.4% | Logistics software |

| REA Group | REA | ~7.2% | Digital marketplace |

| NEXTDC | NXT | ~4-6% | Data centres |

| Technology One | TNE | ~4-6% | Enterprise SaaS |

Individual holding weights are approximate and sourced from fund data as at July 2026.

A -24.59% one-year return is a real number that investors must reckon with. It reflects genuine sensitivity in Australian technology valuations under rate pressure, not a temporary anomaly to explain away. The 1.02% five-year annualised return reinforces the point: this segment of the market has faced sustained headwinds. The since inception return of 9.25% p.a. provides longer-term context, but near-term performance has been genuinely challenged.

Smaller Australian technology companies in ATEC’s portfolio may exhibit meaningful sensitivity to interest rate movements. Their valuations are typically based on discounted future earnings, which reprice when the discount rate rises. When rates stay elevated, the repricing can be sustained rather than temporary.

Earnings quality and rate sensitivity are the two variables that best explained the divergence in ATEC’s underlying holdings during the 48% drawdown the S&P/ASX 200 Information Technology Index recorded between August 2025 and March 2026, with cash-flow-positive companies recovering materially faster than high-growth but unprofitable peers.

The ASX is a relatively small market. Domestically listed technology valuations can swing more sharply than US or global tech when investor sentiment shifts, because there are fewer participants and less liquidity to absorb the selling pressure.

The practical implication is the same as for ASIA: investors should be prepared for periods of double-digit drawdowns, including negative annual returns. This fund is not suitable for short-term trading.

None of these three funds replaces a core broad-market equity index. They are satellite allocations designed to tilt your portfolio toward technology and structural growth themes that the ASX’s bank-and-resources composition leaves underweight.

What makes the combination coherent is that the three exposures are complementary rather than overlapping:

| ETF | Focus | Geographic Exposure | MER | Currency Profile |

|---|---|---|---|---|

| HACK | Cybersecurity | US / North America | 0.67% p.a. | Unhedged USD |

| ASIA | Asian technology | Asia ex-Japan | 0.67% p.a. | Multi-currency Asian |

| ATEC | Australian technology | ASX-listed | 0.48% p.a. | Domestically denominated |

All performance figures cited are after fees, assume reinvestment of distributions, and are not indicative of future performance.

The right question is not which of these funds posted the best recent return. It is which of their underlying risk profiles fits your time horizon, your existing portfolio composition, and your capacity to tolerate drawdowns without selling at the worst moment.

Before investing in any of these ETFs, ask yourself three questions:

ATEC’s -24.59% one-year return is a concrete reminder that these funds can and do deliver negative outcomes over meaningful periods. The drawdown is the price of access to structural growth; the question is whether your circumstances allow you to sit through it.

The behaviour gap in thematic ETFs, where reported time-weighted returns diverge sharply from the money-weighted returns investors actually experience, is a concrete illustration of why entry timing and position sizing matter as much as the underlying fund’s structural thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A financial adviser can help determine appropriate satellite allocation sizes relative to your core portfolio. These three ETFs are not mutually exclusive choices.

HACK, ASIA, and ATEC each address a structurally distinct technology theme that the ASX’s financials-and-resources composition leaves underweight. Cybersecurity spending is non-discretionary and growing. Asia’s digital economy spans both the production infrastructure and the consumer platforms that the rest of the world depends on. Australia’s own technology sector, while smaller and more volatile, contains globally competitive businesses that generate revenue well beyond domestic borders.

These are durable long-term trends, not one-cycle phenomena. But durability does not mean linearity. Each fund carries specific risks that can deliver periods of genuinely painful underperformance, and investors who understand those risks before they invest are the ones most likely to stay positioned through them.

If you want to explore further, examine the BetaShares fund pages directly for current holdings, fees, and performance data. Match what you find against your own portfolio context, risk tolerance, and time horizon. That is the work that turns information into a decision.

—

HACK tracks global cybersecurity companies, ASIA captures Asian technology spanning semiconductors and consumer platforms across Asia ex-Japan, and ATEC tracks Australian-listed technology businesses through the S&P/ASX All Technology Index. All three are passive index ETFs listed on the ASX and designed as satellite allocations alongside a core portfolio.

ASIA delivered a standout 96.99% one-year return after fees, HACK returned 12.45%, and ATEC posted a negative 24.59% return, reflecting sustained pressure on Australian technology valuations from elevated interest rates and a significant drawdown in the S&P/ASX 200 Information Technology Index.

HACK and ASIA both charge a management expense ratio of 0.67% per annum, while ATEC is the cheapest of the three at 0.48% per annum, a gap of 0.19 percentage points that compounds meaningfully over a long holding period.

ASIA investors are exposed to China's regulatory risk (Beijing has previously intervened in the operations of major holdings like Tencent and Alibaba) and Taiwan geopolitical tension, which creates a specific repricing risk for TSMC, the fund's largest single holding at approximately 10.4%.

Financials and materials together account for more than 50% of the ASX 200 by market-cap weight, leaving technology severely underweight relative to global benchmarks. ETFs like HACK, ASIA, and ATEC provide rules-based, single-trade access to technology segments that a standard ASX index allocation structurally misses.