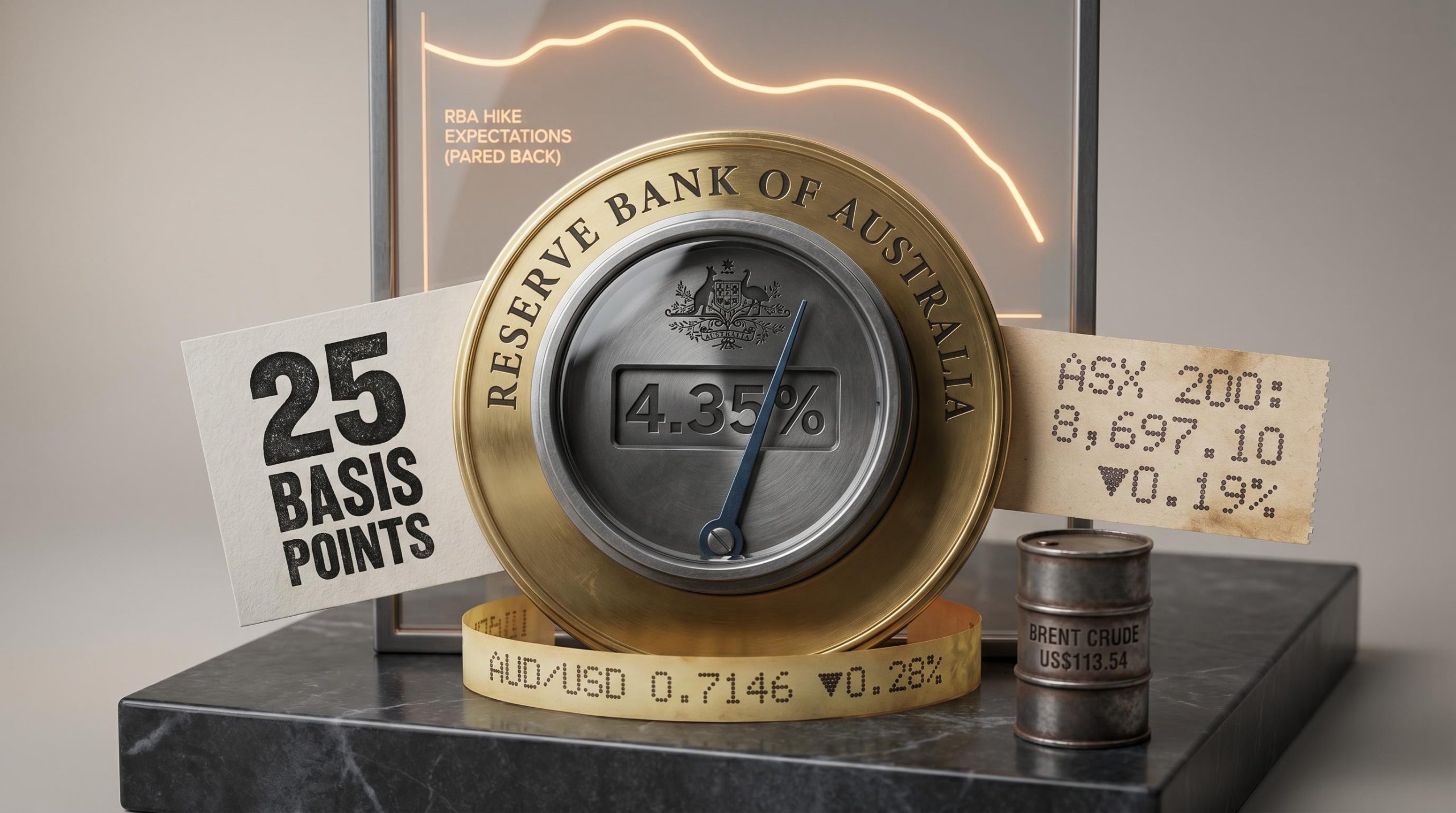

Governor Michelle Bullock raised the cash rate by 25 basis points to 4.35% on 5 May 2026, and then, in a press conference that moved markets more than the decision itself, suggested the Board now has room to wait. The hike was widely anticipated, with markets assigning roughly 75% odds ahead of the meeting. What was not priced in was the tone: Bullock walked back fears of an uninterrupted tightening sequence, acknowledging that policy settings are already restrictive and that household pain is real. Rate-sensitive sectors recovered in the afternoon session. The Australian dollar slipped. Bond markets pared back expectations for further hikes.

What follows is a breakdown of the decision, Bullock’s post-meeting commentary, how ASX sectors split on the day, which individual stocks moved sharply and why, and the specific data releases between now and the June meeting that will determine whether the pause signal holds.

Bullock blinks: why the press conference mattered more than the rate move

The 25 basis point hike to 4.35% was fully anticipated. It had been priced by futures markets and forecast by every major bank. The operative market event of the day was not the number but what Bullock said after it.

The 4.35% decision was the third consecutive tightening move from a starting point of 3.85% in January 2026, and eight of nine Board members voted for the hike, a margin that understates how narrow the threshold between hiking and holding has become as the cumulative effect of 50 basis points in five months works through the economy.

The RBA May 2026 monetary policy statement confirmed the Board’s assessment that inflation was still not sustainably within the target band, providing the formal justification for a move that markets had already priced but whose accompanying language they had not.

In the post-meeting press conference, the Governor struck a noticeably softer tone than markets had expected from a Board that just raised rates. Three acknowledgements stood out:

- The Board may have overweighted inflation risk relative to consumer spending risk in recent months

- The rate rise would cause genuine household hardship, with limited ability to offset elevated global energy costs

- There is now room to observe incoming data before committing to further moves

Bullock described current monetary policy settings as “a bit restrictive,” a characterisation that marked a measurable shift from the language used in the March statement.

The RBA’s own growth forecast reinforced the concession. Australian economic growth is projected to decline to approximately 1.1%, a level Bullock described as “very weak.” Bond markets responded immediately: expectations for additional hikes were pared back in the hours following the press conference, suggesting traders read the tone as a genuine signal rather than rhetorical softening.

Per capita output contraction running at roughly 0.7% across 2025 helps explain why Bullock framed 1.1% headline GDP growth as ‘very weak’: the aggregate figure is inflated by population growth, while the average Australian household has been experiencing declining real living standards for several consecutive quarters.

When big ASX news breaks, our subscribers know first

What the RBA’s 4.35% rate actually means for Australian investors

How the cash rate flows through to your mortgage and portfolio

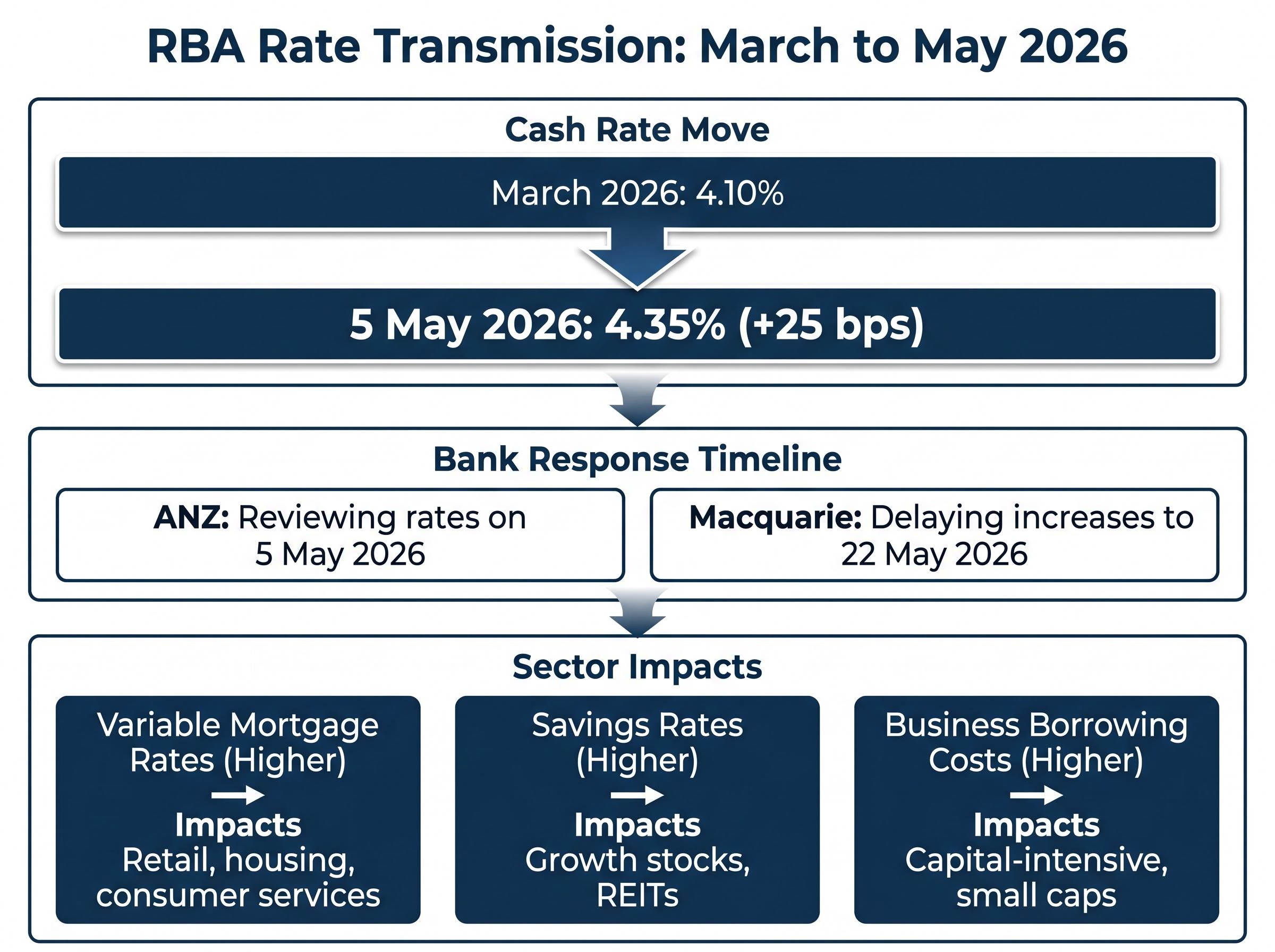

The RBA sets the overnight cash rate, the interest rate at which banks lend to each other on a daily basis. Commercial banks then pass changes through to variable mortgage rates and savings accounts, typically within days to weeks. Borrowers on variable rates feel the impact fastest. Fixed-rate borrowers are insulated until their terms expire, at which point they refinance into the prevailing rate environment.

On 5 May 2026, ANZ announced it was reviewing home loan rates following the decision. Macquarie confirmed it would delay any rate increases to 22 May 2026. Both moves illustrate how the transmission chain works in practice: the RBA moves, and the banking system follows on its own timeline.

Why 4.35% is a different beast from earlier hikes in this cycle

The cash rate has moved from 4.10% in March 2026 to 4.35% in May. At an elevated base, each incremental 25 basis point increase compresses consumer spending capacity more than the same-sized hike at a lower level. Bullock’s 1.1% growth forecast is evidence that the compressive effect is already materialising.

| Rate transmission channel | Direction at 4.35% | Equity valuation impact | Sector implication |

|---|---|---|---|

| Variable mortgage rates | Higher | Compresses consumer discretionary earnings | Retail, housing, consumer services |

| Savings rates | Higher | Raises the risk-free rate alternative to equities | Growth stocks, REITs |

| Business borrowing costs | Higher | Raises discount rates, lowers present value of future earnings | Capital-intensive sectors, small caps |

Retail investors who understand this transmission mechanism are better positioned to anticipate which asset classes tighten under sustained high rates and which sectors benefit from a policy pause.

Oil spills into the rate story: the Middle East wildcard

5 May 2026 was not a clean macro event. Overnight, an Iranian military strike on a UAE energy facility sent ICE Brent crude surging 5.8% to above US$114 per barrel. Prices eased 0.8% to approximately US$113.54 during Asian trade, but the damage to the inflation outlook was already done.

Reuters reporting on the Brent crude surge confirmed prices reached $114.96 per barrel following the Iranian strike, with Gulf shipping also disrupted, a supply shock that embedded fresh inflationary pressure into the same trading session the RBA was delivering its May decision.

Brent crude surged 5.8% overnight to above US$114 per barrel following the Iranian strike on a UAE energy facility, the largest single-session move in the contract since early 2026.

Higher energy prices are themselves inflationary. That reality complicates any RBA pause signal: if energy-driven inflation persists, the Board may be forced to hike again regardless of domestic demand signals. The RBA flagged Middle East energy risks in both its March and May statements. Bullock went further in the press conference, stating that even a quick resolution to the conflict would leave economic effects persisting through the remainder of 2026.

The three inflation pressure channels the RBA is monitoring:

- Energy prices, now elevated by the Brent spike and Middle East supply uncertainty

- Wages, with the labour market still tight relative to the Board’s comfort level

- Aggregate demand, which the 1.1% growth forecast suggests is already weakening

The first hard inflation read the RBA will have before the June meeting is the 28 May retail trade figure. The next quarterly Consumer Price Index (CPI) release is not due until July 2026, meaning the Board will make its June decision with limited updated inflation data and a volatile energy backdrop.

Winners and losers across ASX sectors on rate day

The ASX 200 (XJO) finished at 8,697.10, down just 0.19% on the day. That headline number masked a sharp intra-day split. Morning selling gave way to afternoon recoveries in rate-sensitive sectors after Bullock’s press conference shifted the narrative.

| Sector | Index code | Closing level | Change (%) |

|---|---|---|---|

| Energy | XEJ | 10,932.4 | +0.89% |

| Information Technology | XIJ | 1,807.9 | +0.76% |

| Communication Services | XTJ | 1,751.7 | +0.71% |

| Utilities | XUJ | 10,391.8 | +0.67% |

| Real Estate | XPJ | 3,573.6 | +0.38% |

| Consumer Staples | XSJ | 11,894.8 | +0.35% |

| Consumer Discretionary | XDJ | 3,387.7 | -0.43% |

| Financials | XFJ | 9,470.8 | -0.50% |

| Materials | XMJ | 22,974.3 | -0.55% |

Sectors that gained ground on 5 May 2026

Energy led the board, up 0.89%, driven entirely by the Brent crude spike rather than domestic factors. Utilities tracked energy higher on earnings overlap with energy generation. Information Technology and Communication Services gained as the dovish press conference eased pressure on growth-stock valuations. Real Estate’s +0.38% move was the clearest direct read-through of the pause signal, recovering in the afternoon as bond yields pulled back.

Sectors that fell despite the dovish pivot

Consumer Discretionary dropped 0.43% as the household pain narrative weighed on sentiment. Financials fell 0.50%, with net interest margin compression concerns dominating; Westpac (WBC) fell 2.3% on the day after reporting half-year cash earnings of $3.5 billion, up just 0.1% on the prior period. Commonwealth Bank (CBA) was the only major bank to finish higher, gaining 0.4%. Materials declined 0.55%, partly because Chinese markets were closed for the Labour Day holiday, removing a key pricing signal for base metals and lithium stocks.

Three stocks that moved sharply and why they matter

On high-volatility rate days, stock-level moves can be misread as macro signals. Three names from the session illustrate the difference between rate-driven sector pressure and company-specific catalysts.

- Westpac (WBC), down 2.3%: Half-year cash earnings of $3.5 billion came in broadly at consensus, with expenses down approximately 2% excluding notable items. The sell-off reflected soft net interest income, signalling that the rate environment at 4.35% is not cleanly positive for bank margins. Westpac became the day’s proxy for net interest margin compression across the sector.

- Flight Centre (FLT), up 4.2%: The travel group reaffirmed full-year underlying profit guidance of $315-$350 million, and the market rewarded the earnings visibility. Not all consumer-facing businesses are equally exposed to household pressure, and Flight Centre’s result demonstrated that distinction.

Flight Centre reaffirmed full-year underlying profit guidance of $315-$350 million, providing a concrete example of earnings visibility in a stressed consumer environment.

- Gentrack Group (GTK), down 38.5% to $2.99: The largest single-day faller in the ASX 300 reached a new 52-week low. A decline of this magnitude on rate day can masquerade as a macro move, but this was company-specific. Investors positioned in individual equities need to distinguish between sector-wide rate pressure and idiosyncratic collapses.

What to watch before the June RBA meeting

The next six weeks are a data-watching period. Three releases will determine whether the pause signal holds or evaporates:

- Retail trade (28 May 2026): The first hard read on consumer spending since the hike. A weak print reinforces the case for a pause; a resilient print complicates it.

- Employment data (18 June 2026): A loosening labour market would give the Board room to hold. Persistent tightness keeps wage-driven inflation risk on the table.

- Quarterly CPI (July 2026): Technically post-June meeting, but it shapes the August outlook. The Board will make its June decision without an updated CPI print, relying on softer indicators and the retail trade figure.

Westpac’s pre-meeting base case anticipated potential further hikes in both June and August. If upcoming data surprises to the upside, the market’s post-press-conference repricing may prove premature.

The federal budget conflict with RBA tightening adds another layer of complexity to the June outlook: the 12 May budget includes personal income tax cuts and energy rebates that directly stimulate the demand the RBA is trying to cool, creating a fiscal and monetary policy tug-of-war that Bullock will need to account for in the Board’s June deliberations.

The ASX 200’s technical picture remains cautious. Two reference levels for investors managing exposure:

- Overhead supply sits at 9,022, with the all-time high at 9,201; both define the ceiling for any relief rally

- Support on a pullback clusters around 8,262-8,379

Price sits below both the short-term trend ribbon (approximately 8,762-8,769) and the long-term trend ribbon (approximately 8,686-8,858), with a pattern of declining peaks and troughs maintaining a supply-dominated bias.

The pause is priced in, but it is not guaranteed

Bullock’s press conference was the operative event of 5 May 2026. The sector rotation was the market’s immediate interpretation. The next six weeks of data will confirm or refute it.

The pause narrative rests on three conditions:

- Inflation remains contained, with no further upside surprises in the May retail trade or June employment figures

- Energy prices stabilise, with no escalation of Middle East hostilities beyond the current disruption

- Consumer spending remains soft, confirming that the rate rises are transmitting as intended

None of these is guaranteed. Brent crude remains above US$113, and Bullock herself acknowledged that even a quick resolution to the conflict would leave economic effects persisting through 2026.

Investors wanting to stress-test the pause thesis against the downside scenario should consult our deep-dive into Australia’s stagflation risk, which examines consumer confidence at a 50-year low, record corporate insolvencies in 2025, and the labour market indicators that would signal whether unemployment is about to breach the RBA’s comfort zone.

The Australian dollar closed at AUD/USD 0.7146, down 0.28% on the session, a reminder that the currency market is also pricing the rate path and adding another layer of cross-asset sensitivity for internationally exposed portfolios.

Investors positioned in rate-sensitive sectors on the pause thesis should define in advance what data outcome would cause them to reconsider. The June meeting is six weeks away. The data arrives sooner.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.