How to Position for the Most Event-Dense Week of July 2026

3 hrs ago

In early 2025, unprofitable AI-adjacent stocks were outrunning some of the most financially disciplined businesses on global exchanges by a wide margin. Then the market turned. Volatility surged, speculative names compressed, and companies with stable earnings, low debt, and high returns on equity began reclaiming lost ground. The question Australian investors searching for answers on quality investing are actually asking is straightforward: does owning boring, profitable, low-debt companies beat chasing the next momentum trade over a full cycle?

The question is not new, but the 2025-2026 environment has made it unusually live. Persistent inflation, volatile interest rate expectations, and a rotation away from speculative growth names have pushed the quality factor back to the centre of Australian investor conversations. Two ASX-listed ETFs, QUAL and AQLT, have brought the strategy within easy reach of everyday portfolios. What follows is a clear explanation of what quality investing means, how its screening criteria work in practice, why it diverges structurally from a plain ASX 200 index fund, and how to assess whether it belongs in a portfolio.

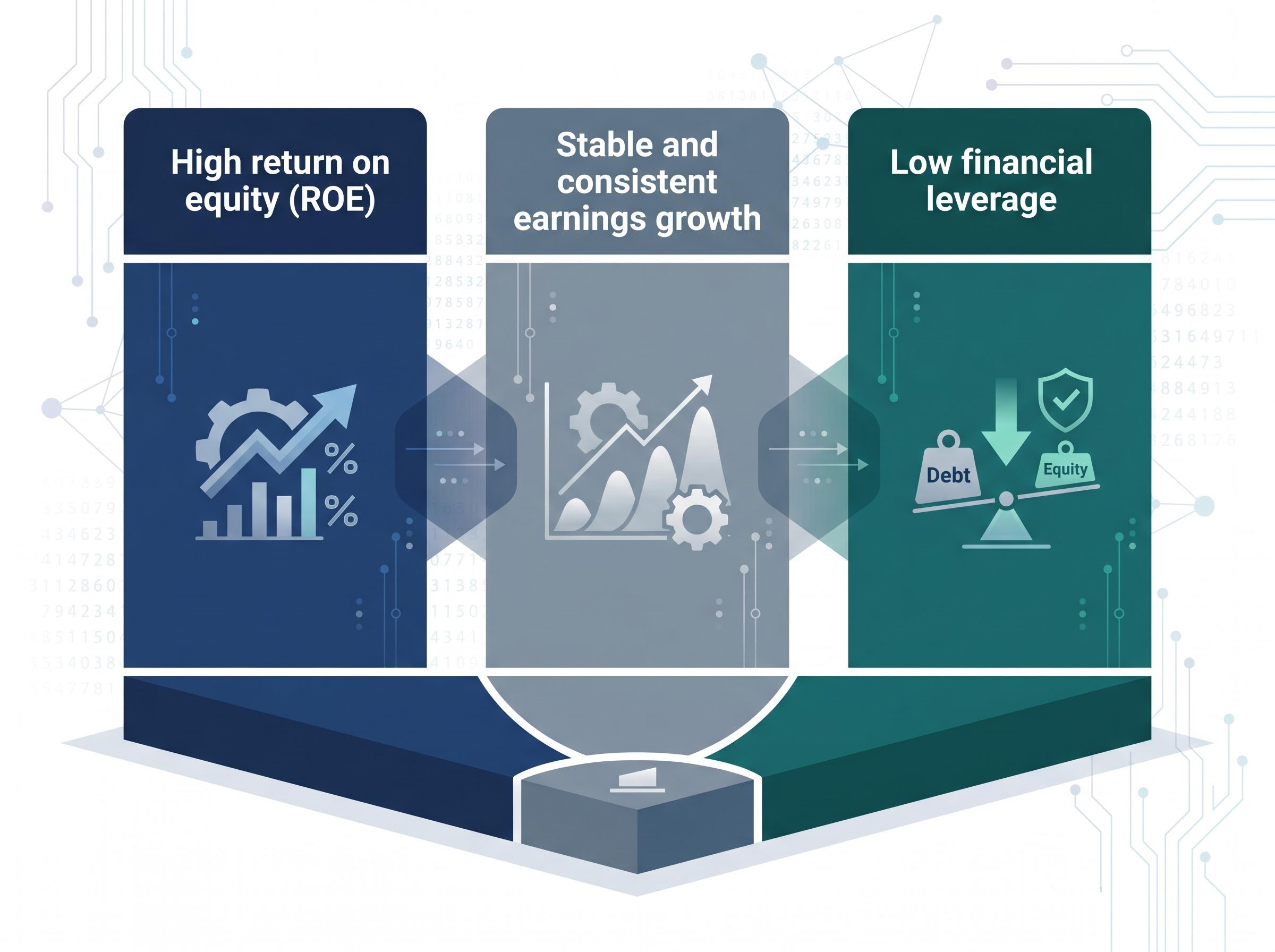

The instinctive assumption is that “quality” simply means large, well-known companies. BHP, Commonwealth Bank, household names. That assumption is wrong, or at least dangerously incomplete. Quality investing is not about brand recognition or market capitalisation. It is a quantitative discipline built on three measurable criteria.

The core screening metrics, formalised by MSCI and underpinning products like QUAL, are:

These criteria trace an intellectual lineage back to Benjamin Graham and Warren Buffett, both of whom emphasised financial resilience and compounding capacity as the foundation of long-term wealth creation.

How does quality differ from its closest cousins? Value investing seeks stocks trading below intrinsic value; it hunts for bargains. Growth investing targets rapid revenue expansion, often in early-stage or unprofitable companies; it hunts for potential. Quality can overlap with both, but its filter is distinct.

Quality investing prioritises proven, sustainable earnings power and financial discipline over bargains or hype. A company can be expensive by value metrics and slow-growing by growth metrics and still rank highly on quality screens.

Understanding the definition is one step. Understanding how the screen translates into an actual portfolio is the step that demystifies why quality ETFs hold what they hold.

QUAL (VanEck MSCI World ex Australia Quality ETF) applies MSCI’s quality index methodology to a global universe. The process starts with the three criteria above, scoring every eligible stock on its ROE, earnings stability, and leverage. Each stock receives a composite quality score. The portfolio then weights its approximately 300 holdings by market capitalisation multiplied by that quality score, meaning the most financially disciplined companies carry the heaviest portfolio weight.

The MSCI Quality Index methodology formalises these three criteria into a composite quality score by measuring each eligible stock’s return on equity, earnings variability, and debt-to-equity ratio, then weighting holdings by market capitalisation multiplied by that score.

This is applied universe-wide rather than sector-by-sector. The screen does not guarantee equal sector representation. It surfaces whatever passes the filter, which is why quality portfolios often look structurally different from their parent benchmarks. Notable QUAL holdings that illustrate the output include Microsoft (MSFT), Apple (AAPL), and Visa (V), companies with high ROE, consistent earnings, and conservative balance sheets.

AQLT (BetaShares Australian Quality ETF) applies comparable screening criteria to ASX-listed equities, using the same fundamental trio: profitability, earnings consistency, and balance sheet resilience. Representative holdings include BHP Group (BHP), Commonwealth Bank (CBA), and Wesfarmers (WES).

Its management fee (0.35% p.a.) is marginally lower than QUAL’s (0.40% p.a.), and both sit in the low-cost range for factor-based ETF access.

| Feature | QUAL | AQLT |

|---|---|---|

| Investment universe | Global ex-Australia | Australian equities |

| Approximate holdings | 300 | Varies (quality-screened ASX) |

| Weighting methodology | Market cap x quality score | Quality-factor weighted |

| Management fee | 0.40% p.a. | 0.35% p.a. |

| Example holdings | Microsoft, Apple, Visa | BHP, CBA, Wesfarmers |

Many Australian investors treat an ASX 200 index fund as a default “safe” allocation. The assumption is that owning 200 of the country’s largest companies provides broad diversification. The reality is more concentrated than it appears.

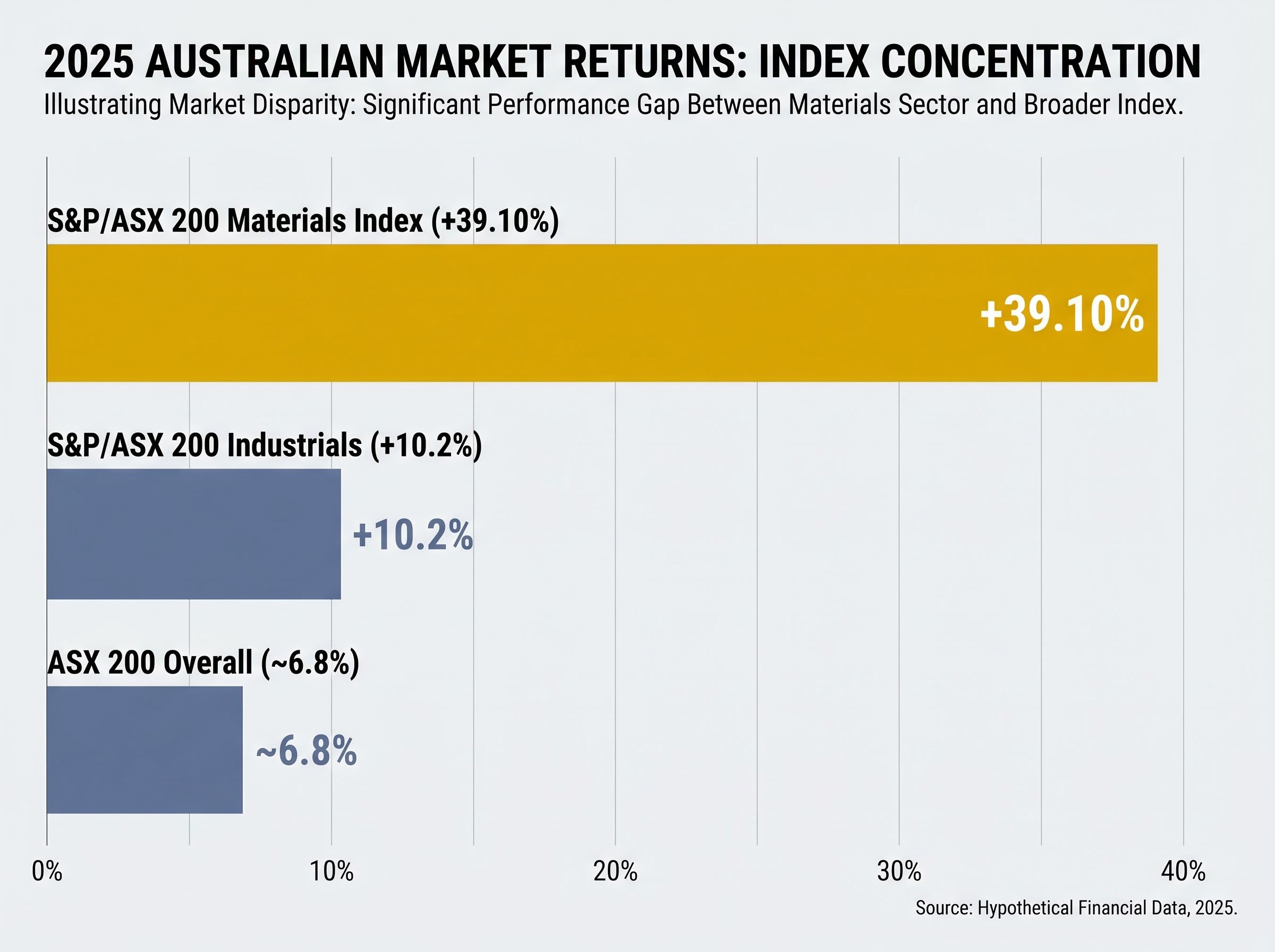

The ASX 200 is heavily weighted toward two sectors: banks and mining. This is a structural feature of the Australian market, not a flaw, but it introduces meaningful cyclical sector risk that most passive investors do not consciously choose. In 2025, that concentration became starkly visible.

The S&P/ASX 200 Materials Index (XMJ) returned +39.10% in 2025. The ASX 200 overall returned approximately 6.8%. Materials did not just outperform; they masked weakness across the rest of the index.

The S&P/ASX 200 Industrials sector returned +10.2% (total return 13.98%) over the same period. The gap between the top-performing sector and the index headline figure illustrates how a small number of heavily weighted cyclical sectors can dominate overall returns.

Quality screening addresses this concentration by elevating companies based on fundamental financial health rather than market-cap weighting alone. Quality-screened Australian portfolios differ from the ASX 200 in several structural ways:

The result is a portfolio that may still hold some of the same names as the ASX 200, but weights them differently and, over time, produces different sector exposure.

Quality investing has a recognisable cycle. Understanding that cycle is the difference between holding with conviction and rotating out at exactly the wrong moment.

The pattern is consistent across decades. During speculative or momentum-driven rallies, when low-quality, unprofitable companies lead the market higher, quality tends to lag. Investors chasing the hottest names see quality portfolios as dull. Then conditions tighten: growth slows, costs rise, risk appetite contracts. Quality reasserts itself.

The 2025 experience followed this pattern precisely. In early 2025, AI-driven momentum and speculative enthusiasm carried unprofitable companies higher while quality lagged. By late 2025, the rotation arrived. Slowing US employment data, rising costs, and weakening consumer data triggered a defensive shift.

In November 2025, VanEck’s QUAL outperformed the MSCI World ex Australia Index by 105 basis points (1.05%), as of 30 November 2025 per Morningstar Direct data (net of fees, pre-brokerage, distribution reinvestment assumed).

Historical analogues reinforce the pattern:

NBER q-factor research on return on equity provides empirical grounding for the quality premium, demonstrating that profitability factors, including ROE, explain cross-sections of stock returns in ways that subsume earlier factor models, lending academic weight to the long-run case for quality screens.

Magellan’s Alan Pullen has predicted a “quality comeback” in 2026 amid rising volatility, a view consistent with the factor’s historical behaviour during periods of stress and tightening.

The historical case for quality is well established. The question for Australian investors right now is whether the 2026 environment offers something more than a standard cyclical repeat.

The combination of persistent inflation, interest rate uncertainty, and slowing growth, stagflationary signals, specifically favours companies that pass quality screens. The logic runs through three channels. Pricing power protects margins when input costs rise, meaning quality companies can pass through inflation rather than absorb it. Low debt reduces interest rate sensitivity, insulating these businesses from the refinancing pressure that weighs on leveraged names. Stable earnings reduce the volatility of analyst forecasts, which matters because high-leverage or unprofitable growth companies see their valuations compress sharply when forward earnings estimates become unreliable.

Contrast this with the position of high-growth or thematic names. AI-adjacent companies and early-stage ventures that depend on cheap capital and multiple expansion are structurally disadvantaged when rates stay elevated. The gap between quality and speculative growth widens in this environment.

Inflation-aware portfolio construction extends beyond quality equities alone; short-duration bond funds and high-yield cash ETFs serve complementary roles for investors who want to manage purchasing power risk across fixed income, cash, and equity allocations simultaneously.

March 2026 ASX records confirmed that the anticipated volatility has materialised, with heightened market activity and record futures month volumes. Macquarie characterised 2026 as having a “supportive backdrop” for quality, with inflation as the primary focus. The Financial Times, cited by VanEck in 2025, urged investors to buy quality to escape exposure to unprofitable speculative names.

Investors exploring how to structure a full defensive allocation beyond quality equities will find our full explainer on defensive ASX positioning in 2026 covers the three-tier framework of cash ETFs, short-duration bond funds, and quality equity products, including why conventional safe haven assets such as long bonds and gold have failed to protect portfolios during the current stagflationary oil shock.

VanEck’s data showed quality valuations narrowing toward their 10-year average as of 31 October 2025. This does not mean quality is cheap in absolute terms. It means the premium investors pay for superior fundamentals is less stretched than during the growth-stock dominance of the low-rate era.

When quality valuations approach their long-run average, entry points become more attractive because the investor is paying a lower relative premium for companies with proven compounding characteristics. For Australian investors assessing timing, this narrowing represents a more favourable starting point than the frothier periods of recent years.

Quality stock valuations narrowing toward their 10-year average coincides with a broader macro backdrop in which US consumer sentiment has reached historic lows even as equity indices have pushed to record highs, a disconnect that historically precedes volatility episodes where financially disciplined companies tend to hold their ground.

Four ASX-listed ETFs provide direct access to the quality factor, each serving a distinct portfolio function.

| Ticker | Provider | Investment universe | Management fee | Key differentiator |

|---|---|---|---|---|

| QUAL | VanEck | Global ex-Australia (300 stocks) | 0.40% p.a. | Longest track record (inception 29 October 2014) |

| QHAL | VanEck | Global ex-Australia (hedged) | Not confirmed | Currency-hedged version of QUAL |

| AQLT | BetaShares | Australian quality equities | 0.35% p.a. | Domestic quality screen addressing ASX concentration |

| QLTY | BetaShares | Global quality leaders | 0.35% p.a. | Global quality with BetaShares methodology |

The genuine choice is not which ETF is “best” but which combination suits a portfolio’s existing exposures. AQLT addresses the ASX concentration problem directly, applying quality screens to Australian equities and tilting domestic allocation away from the banks-and-mining default. QUAL and QLTY add internationally diversified quality exposure, reducing overall cyclical sector concentration.

QUAL, QHAL, and QLTY each provide quality factor exposure to international equities rather than Australian shares, which means adding any of them to a portfolio increases global equity weight rather than substituting for an existing domestic holding.

An investor using a broad ASX 200 fund alongside AQLT gets quality-tilted domestic exposure. Adding QUAL layers on global diversification. The hedged variant QHAL suits investors who want to remove currency risk from the international allocation.

A compact selection of carefully chosen ETFs, each serving a distinct purpose, can form a solid portfolio foundation without redundancy. The goal is complementary function, not product accumulation.

Quality investing is not a market-timing strategy or a thematic bet. It is a structural commitment to businesses with the financial characteristics to compound value across economic cycles: high returns on equity, stable earnings, and conservative balance sheets.

The honest trade-off is real. Quality will lag during speculative rallies when momentum carries unprofitable names higher. Investors who understand this are less likely to abandon the strategy at precisely the moment it looks least exciting.

In an era of persistent inflation, rate uncertainty, and heightened volatility, the case for owning businesses with pricing power, stable earnings, and low debt is as strong as it has been in a decade. Australian investors may benefit from examining the sector composition of their current portfolio, particularly any ASX 200 exposure, and considering whether quality-screened alternatives address concentration risks they may not have consciously taken on.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Consulting a licensed financial adviser is recommended before making portfolio changes, particularly regarding tax implications of ETF holdings for Australian investors.

Quality investing is a quantitative strategy that selects companies based on three measurable criteria: high return on equity, stable and consistent earnings growth, and low financial leverage. It prioritises proven, sustainable earnings power over bargain hunting or chasing high-growth names.

QUAL (VanEck MSCI World ex Australia Quality ETF) screens approximately 300 global stocks using MSCI's quality methodology at a management fee of 0.40% per annum, while AQLT (BetaShares Australian Quality ETF) applies comparable quality screens to ASX-listed equities at 0.35% per annum, addressing the ASX 200's concentration in banks and mining.

The ASX 200 is heavily weighted toward banks and mining, meaning a small number of cyclical sectors can dominate overall returns. Quality-screened portfolios instead weight companies by fundamental financial health, reducing exposure to cyclical sector swings.

Quality tends to lag during speculative or momentum-driven rallies when unprofitable companies lead the market higher, but historically reasserts itself when conditions tighten, growth slows, and risk appetite contracts. Investors who understand this cycle are less likely to exit the strategy at the wrong time.

Four ASX-listed ETFs provide quality factor access: QUAL and its currency-hedged variant QHAL (both VanEck, global ex-Australia), and AQLT and QLTY (both BetaShares, covering domestic and global quality respectively), with management fees ranging from 0.35% to 0.40% per annum.