Nvidia has beaten Wall Street expectations on both revenue and earnings for two consecutive years, yet its stock has repeatedly sold off after results. Tonight, that paradox goes on trial again. With Q1 FY2027 earnings dropping after U.S. market close today (20 May 2026), the question is not simply whether Nvidia will beat consensus. It is whether a beat will matter. The 10-year U.S. Treasury yield is running near 4.64%, Nvidia’s stock has lagged both the Philadelphia Semiconductor Index and the S&P 500 semiconductors sector on a year-to-date basis, and macro sentiment is actively competing with AI optimism for investor attention. What follows lays out what Wall Street is watching, what the bar looks like in numerical terms, and why the post-earnings price reaction may tell investors more than the earnings figures themselves.

Strong results, weak returns: why Nvidia’s earnings streak has not lifted its stock

For two years, Nvidia has delivered double beats, clearing both revenue and earnings consensus quarter after quarter. Another beat tonight is the base case, not the surprise. That distinction matters.

Wolfe Research analyst Chris Senyek has framed the problem directly: post-earnings one-day price performance has been consistently weak despite the beat streak, raising the question of whether outperformance is already priced into the stock before the numbers arrive.

Wolfe Research has characterised tonight’s release as a test of whether another double-beat will again prompt investors to exit positions rather than build them, a pattern that has repeated across the prior two years of results.

The comparative data reinforces the concern. Nvidia has underperformed both the Philadelphia Semiconductor Index and the S&P 500 semiconductors sector year-to-date, even as the company’s operational results have continued to expand. Heading into tonight’s release, NVDA shares were trading at approximately $223-$224 in the pre-market session.

A stock that beats expectations and still loses ground is telling investors something. The question is whether tonight’s release changes the signal or confirms it.

When big ASX news breaks, our subscribers know first

What the numbers actually need to look like tonight

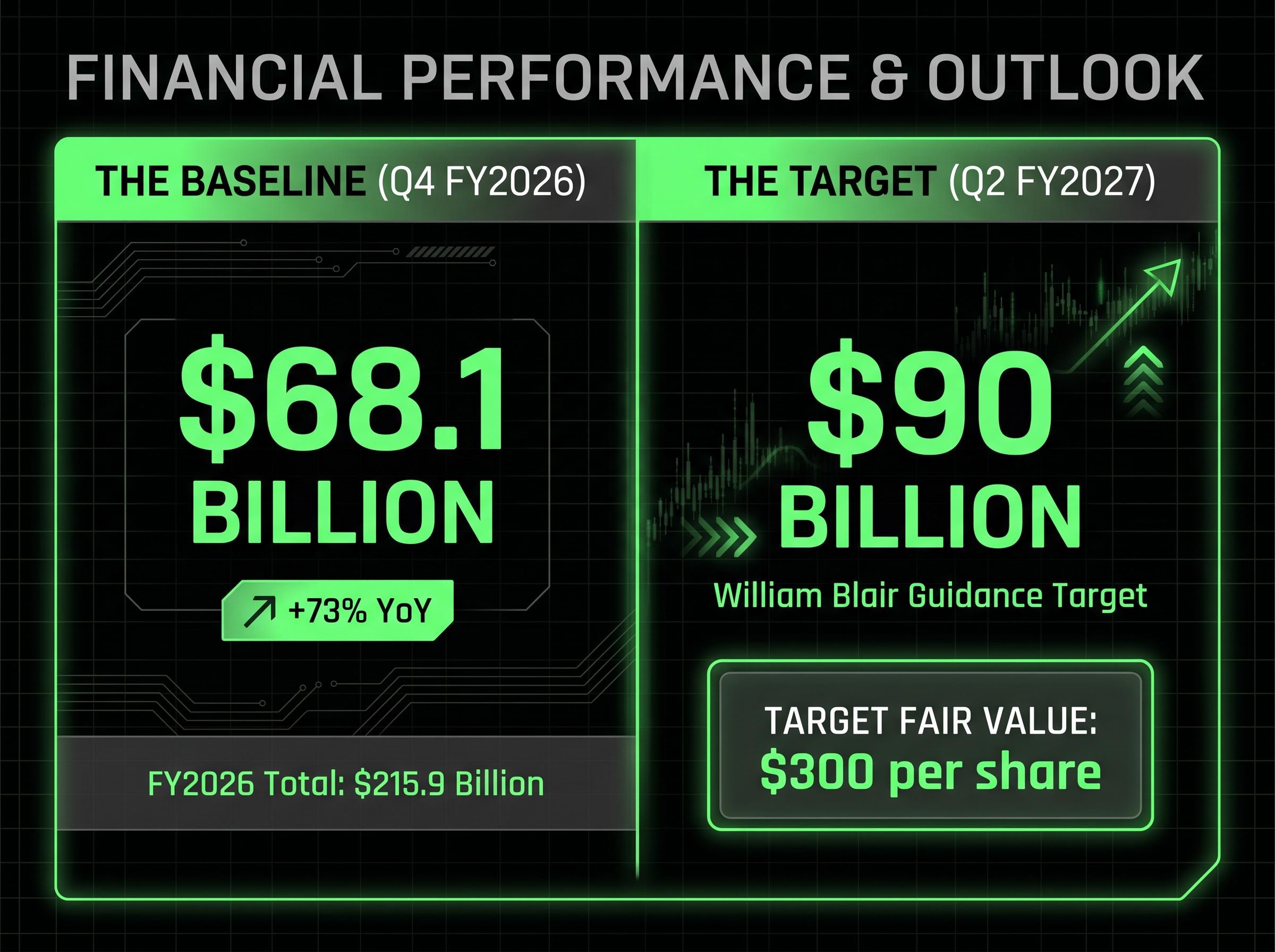

The most recent confirmed baseline is Q4 FY2026, released on 25 February 2026. Nvidia reported quarterly revenue of $68.1 billion, up 20% quarter-over-quarter and 73% year-over-year. Full-year FY2026 revenue came in at $215.9 billion, a 65% annual increase.

Those are the numbers the market has already absorbed. Tonight’s Q1 FY2027 release needs to clear a higher bar.

| Metric | Most Recent Actual (Q4 FY2026) | Full-Year FY2026 | Analyst Watch Level Tonight |

|---|---|---|---|

| Quarterly Revenue | $68.1 billion | — | Above Q4 baseline |

| Full-Year Revenue | — | $215.9 billion | — |

| Q2 FY2027 Guidance | — | — | Above $90 billion |

The guidance number Wall Street is actually watching

For a company growing at Nvidia’s pace, forward guidance typically moves the stock more than the current-quarter result. The market is pricing what comes next, not what just happened.

William Blair analyst Sebastien Naji identified approximately $90 billion in Q2 FY2027 revenue guidance as the threshold that would constitute a genuine beat-and-raise outcome. Naji maintains an Outperform rating on Nvidia with a fair value estimate of approximately $300 per share, implying meaningful upside from current pre-market levels, but that estimate is contingent on guidance holding above this benchmark. The $90 billion figure is the single most important number to evaluate when the release lands tonight.

Why bond yields and macro sentiment are complicating the AI trade

Even a clean earnings beat lands in a market environment that is not automatically receptive to growth-stock positioning.

The 10-year U.S. Treasury yield was approximately 4.61% as of 18 May 2026 (per Federal Reserve Economic Data) and has been hovering near 4.64-4.65% intraday today. When the yield on a risk-free government bond rises, it increases the rate used to discount future earnings back to present value. For a company like Nvidia, where a significant portion of the stock’s valuation rests on expected earnings years into the future, a higher discount rate compresses what investors are willing to pay today for those future profits.

Discount rate compression becomes most acute when yield moves are both large and rapid; the 30-year Treasury briefly exceeded 5.19% intraday on 19 May 2026, its highest level since 2007, a move driven by the Moody’s sovereign downgrade, sticky inflation expectations, and heavy Treasury supply that collectively reset the rate environment for high-multiple growth stocks in a matter of days.

The Federal Reserve Economic Data for the 10-year Treasury yield shows the DGS10 series tracking constant maturity rates in real time, confirming the 4.61% reading cited for 18 May 2026 and providing the historical baseline against which today’s elevated yield environment can be assessed.

The 10-year U.S. Treasury yield near 4.64-4.65% represents one of the most persistent headwinds for high-multiple growth stocks heading into this earnings season.

That creates a structural competition between AI spending optimism and yield pressure. Wolfe Research framed tonight’s release not merely as a company-specific event but as a test of broader market conditions: whether AI investment conviction can reassert itself as the dominant narrative or whether persistent yield pressure continues to cap the upside for even the strongest fundamental performers.

Investors who understand why yields matter to Nvidia’s multiple will be better positioned to interpret the post-earnings price movement, regardless of what the revenue figure says.

How Nvidia is building revenue beyond its core chip business

The beat-or-miss binary on GPU sales is only one dimension of tonight’s release. Sophisticated investors are watching whether Nvidia is becoming something larger than a semiconductor manufacturer dependent on a single product cycle.

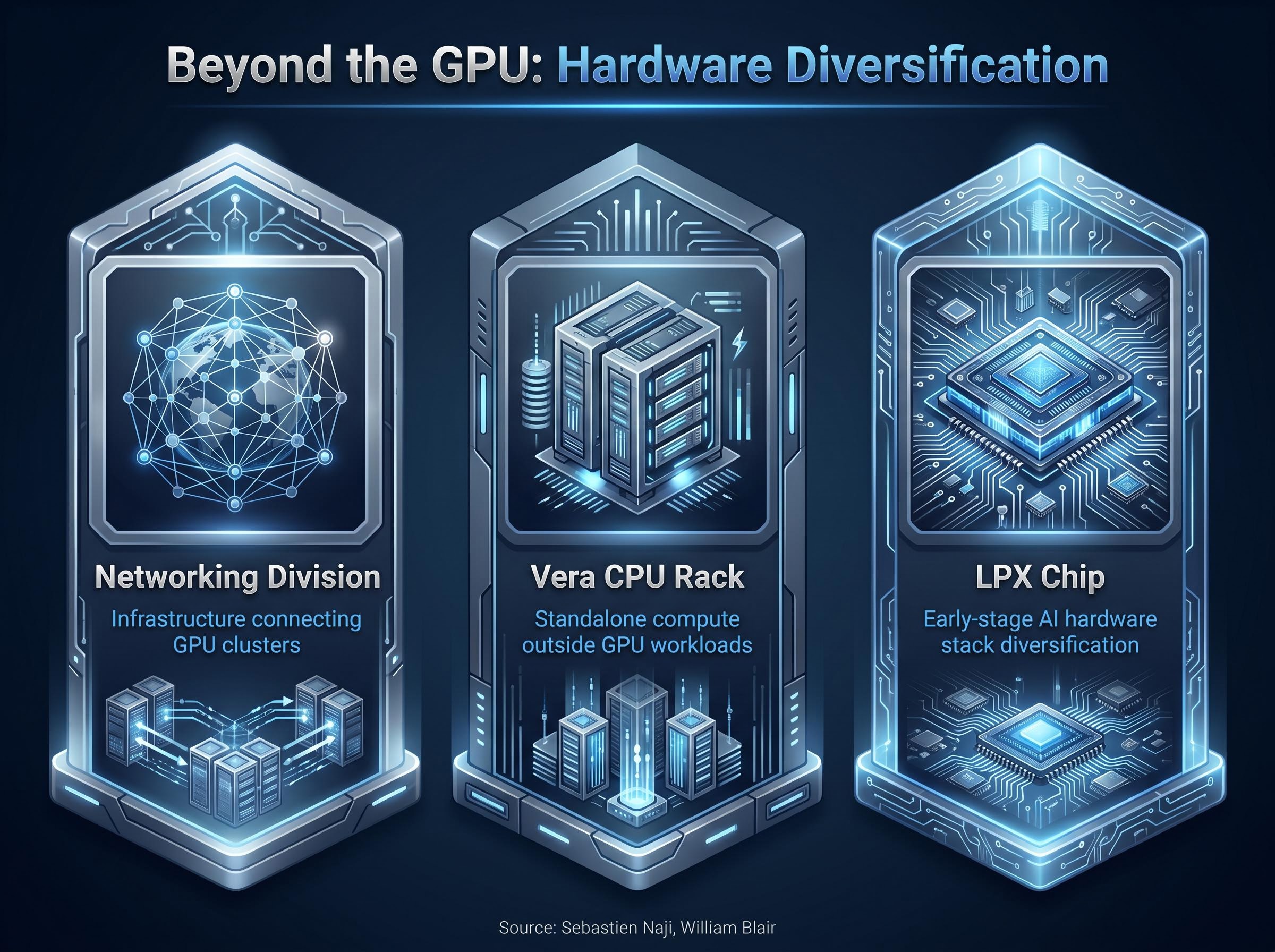

William Blair’s Sebastien Naji identified three specific areas beyond GPU hardware as central to the investment thesis:

- Networking division: The infrastructure connecting GPU clusters at scale, where Nvidia is competing for a growing share of data centre budgets beyond the chips themselves.

- Vera CPU rack: A standalone product that positions Nvidia to capture compute spending outside GPU-specific workloads, broadening the company’s addressable market within AI infrastructure.

- LPX chip: An early-stage commercial product where initial traction would signal that Nvidia’s product portfolio is diversifying into new segments of the AI hardware stack.

These three areas represent the evidence base for Nvidia’s claim to be a system-level infrastructure provider. Technology capital expenditure is beginning to migrate across more parts of the stack, and Nvidia’s ability to capture that migration underpins William Blair’s $300 fair value estimate.

GPU dominance is already priced in. Tonight’s commentary on these product lines may matter as much as the headline revenue number.

What the post-earnings price reaction will actually tell investors

Given Nvidia’s history of fundamental beats paired with muted or negative stock reactions, how the shares trade after tonight’s release is itself a data point about investor conviction in the AI trade at this valuation and yield level.

When a result is widely anticipated, price often moves on the difference between expectations and forward guidance rather than on the absolute numbers. This is the mechanism behind the so-called “sell the news” dynamic. Chris Senyek at Wolfe Research flagged the specific risk that a strong result might again prompt position exits, the same pattern observed over the prior two years of double beats.

The expectations gap mechanics behind post-earnings price moves are well-documented but routinely misread: with 84% of S&P 500 companies beating estimates in Q1 2026, well above the 10-year average of 76%, markets have recalibrated to expect beats, which means a double beat no longer generates the incremental buying it once did and instead shifts the entire pricing burden onto the guidance line.

How to read tonight’s after-hours move

Two scenarios offer interpretive clarity:

- Strong guidance plus a rally above pre-market levels: This would signal that the Q2 FY2027 guidance cleared the macro hurdle and that AI conviction is reasserting itself over yield pressure.

- Strong guidance plus a flat or negative reaction: This would reinforce the pattern Wolfe Research identified and suggest that rising yields are still winning the narrative battle, even against operational outperformance.

Post-release NVDA price movement will be observable via Nasdaq and real-time quote services after approximately 4:00-4:30 PM ET today.

The bar has never been higher, and that is the problem

Nvidia’s consistent outperformance has reset the market’s base case. A beat is assumed. Only a genuine upside surprise on guidance or demonstrable non-GPU growth can generate incremental buying at this stage.

William Blair maintains a constructive view, with an Outperform rating and a $300 fair value estimate. Yet even that bullish case requires the non-GPU product lines to show commercial traction and the Q2 FY2027 guidance to clear the $90 billion threshold that Sebastien Naji identified as the beat-and-raise marker.

William Blair estimates Nvidia’s fair value at approximately $300 per share, but that figure is contingent on forward guidance and diversification progress meeting expectations tonight.

Tonight’s release is as much a referendum on whether AI investment conviction can overcome macro headwinds as it is an assessment of Nvidia’s operational performance. Wolfe Research and William Blair frame the event from different but complementary angles: one watching for the exit pattern to repeat, the other looking for the structural thesis to hold. The earnings figures will arrive shortly after the close. The price reaction will arrive minutes later. For investors, the second may carry more information than the first.

Investors exploring the longer-horizon question of how much runway the AI trade actually has will find our full explainer on the AI bull market timeline, which examines Paul Tudor Jones’s 1-2 year runway estimate alongside hyperscaler capex verification data, Arm Holdings valuation comparisons to peak dot-com pricing, and the single capex growth threshold that strategists identify as the most important signal to monitor.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.