AI Disruption in Tech: the $2T Legacy Software Repricing

3 mins ago

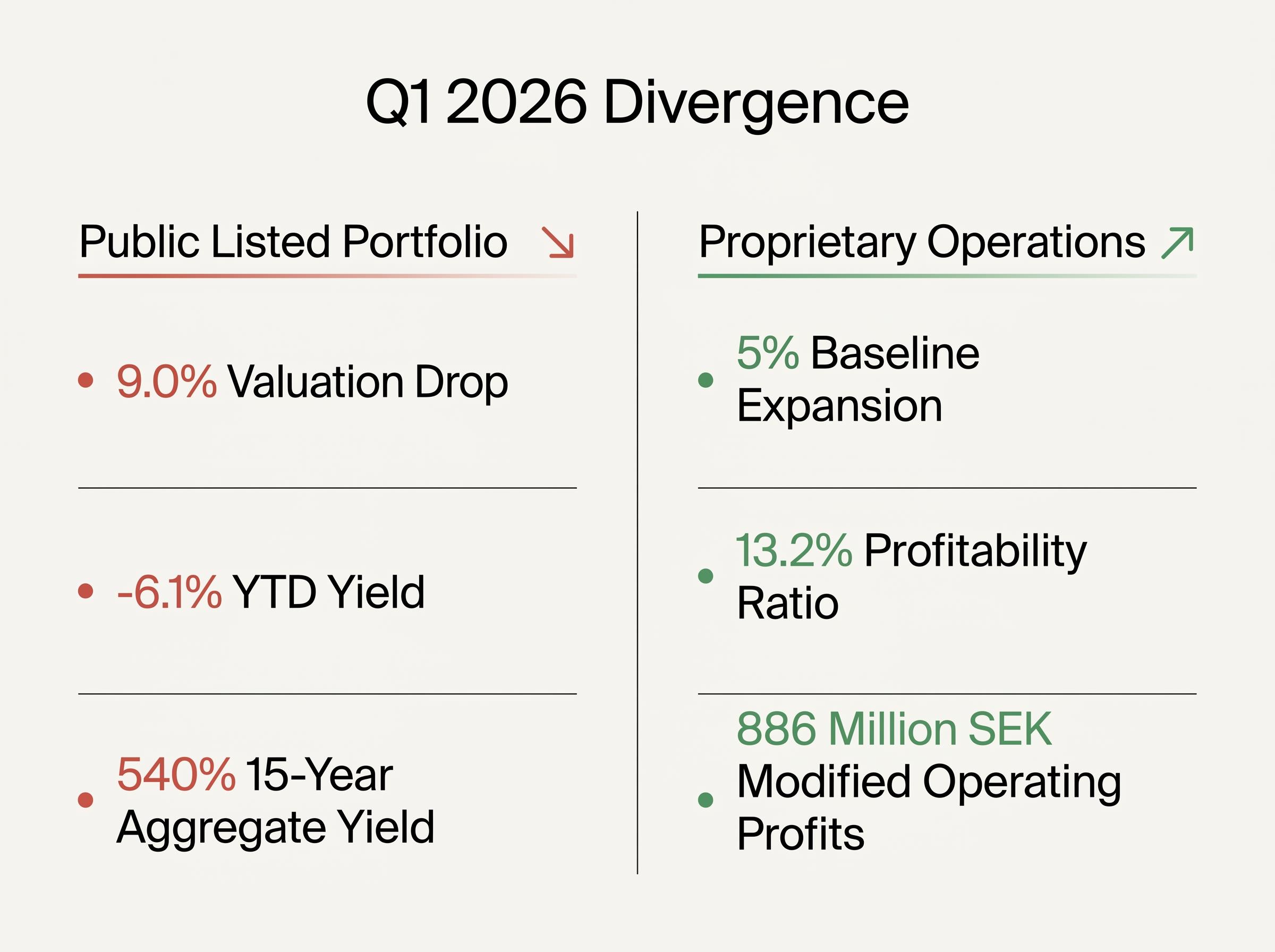

The recent Investment Latour earnings data reveals a striking divergence between public market perception and private operational mechanics. Following the late April 2026 financial disclosures, the conglomerate experienced a sharp 9.0% drop in corporate equity valuations. Beneath this surface-level contraction, proprietary subsidiary requests demonstrated a 5 percent baseline expansion on a constant currency basis.

Severe foreign exchange headwinds have temporarily masked this core operational momentum, translating strong local-currency growth into reported top-line declines. Market evaluators are currently penalising the revenue contraction without accounting for the underlying margin defence deployed by the operating groups.

This analysis deconstructs the first-quarter metrics to reveal how specific internally managed industrial divisions are maintaining their pricing power. By examining the structural advantages of these subsidiaries, commercial stakeholders can see how the organisation continues to capitalise on global megatrends despite immediate macroeconomic stress. The gap between the shock’s severity and the market’s response reveals how long-term capital is pricing this temporary volatility.

The internally managed industrial model provides a distinct defensive moat against external economic pressures. While the publicly traded asset portfolio is subject to immediate market volatility, the fully owned proprietary groups operate with insulated pricing power. This structural separation allows the conglomerate to defend margins even when foreign exchange translations wipe out approximately 6 percent of quarterly corporate revenue.

This structural separation is particularly critical when contextualising the recent severe price collapse, which was largely driven by a negative 9.0 percent return in the listed investment portfolio rather than any failure in core manufacturing operations.

The operational differences between these two arms define the company’s survival mechanics. These internal divisions maintain efficiency through three primary structural advantages:

Publicly traded portfolios offer liquid market exposure but suffer from immediate sentiment-driven valuation swings during reporting seasons. Proprietary industrial groups operate under direct management control, enabling rapid pricing adjustments and targeted cost mitigation across the supply chain. * Internally managed divisions facilitate targeted capital allocation into high-growth sectors without requiring public shareholder consensus or facing activist pressure.

These operational realities explain why the headline revenue miss does not reflect a failing business model. The integration strategy continuously feeds this industrial growth engine with fresh capital and strategic acquisitions. Recent expansions into forestry equipment and regional ventilation markets demonstrate this capital deployment strategy in action. According to company data, newly integrated enterprises are projected to add roughly 500 million SEK toward annualised turnover.

Margin Resilience Proprietary divisions retained a highly stable 13.2% profitability ratio during the first quarter, proving the structural advantage of internally managed operations during periods of macroeconomic stress.

Modified operating profits reached 886 million SEK across these proprietary divisions. This operational resilience serves as a vital educational foundation for understanding the broader corporate strategy. It shows commercial evaluators exactly why the internal industrial engine survives severe currency fluctuations that otherwise compress top-line reporting.

Specific volume and revenue metrics from standout subsidiaries provide the clearest evidence of ongoing operational momentum. Divisional data proves that industrial demand remains highly active in targeted sectors, countering the broader stagnant market backdrop. The exceptional first-quarter trajectory of the Nord-Lock and Caljan divisions illustrates this localised strength.

These units are capitalising on specialised contracts and sustained infrastructure activity across their target geographies. According to market rumors, Nord-Lock secured 166 million SEK in operating profit at a 29.4 percent ratio. This performance was driven by intense demand for highly engineered fastening solutions.

This robust underlying industrial growth is actively offsetting foreign exchange headwinds, allowing core subsidiaries to maintain strong profitability despite the broader 20 percent share price contraction.

Similarly, according to market rumors, Caljan recorded a 34 percent surge in baseline orders and a 44 percent jump in core revenues. This exceptional volume yielded a 16.5 percent profit margin as warehouse automation and logistics upgrades accelerated globally.

These high-performing logistics and fastening units contrast sharply with the softer environments navigated by construction-exposed divisions. Hultafors, for example, maintained a 14.9 percent operating ratio despite sluggish volumes in the residential and commercial building sectors. The conglomerate’s diversification absorbs these cyclical shocks effectively.

| Subsidiary | Order Surge Percentage | Operating Profit | Profit Margin |

|---|---|---|---|

| Nord-Lock | 30% | 166 million SEK | 29.4% |

| Caljan | 34% | Data Not Disclosed | 16.5% |

| Hultafors | Sluggish Volume | Maintained Stability | 14.9% |

| Swegon | Data Not Disclosed | Data Not Disclosed | Data Not Disclosed |

The inclusion of climate control and ventilation subsidiary Swegon highlights the broader industrial strategy, though specific first-quarter order surge metrics remain undisclosed. The raw numbers from the disclosing divisions prove the operational momentum thesis without relying on managerial optimism. Readers gain actionable intelligence from these granular metrics, identifying which verticals are currently funding the conglomerate’s broader expansion efforts.

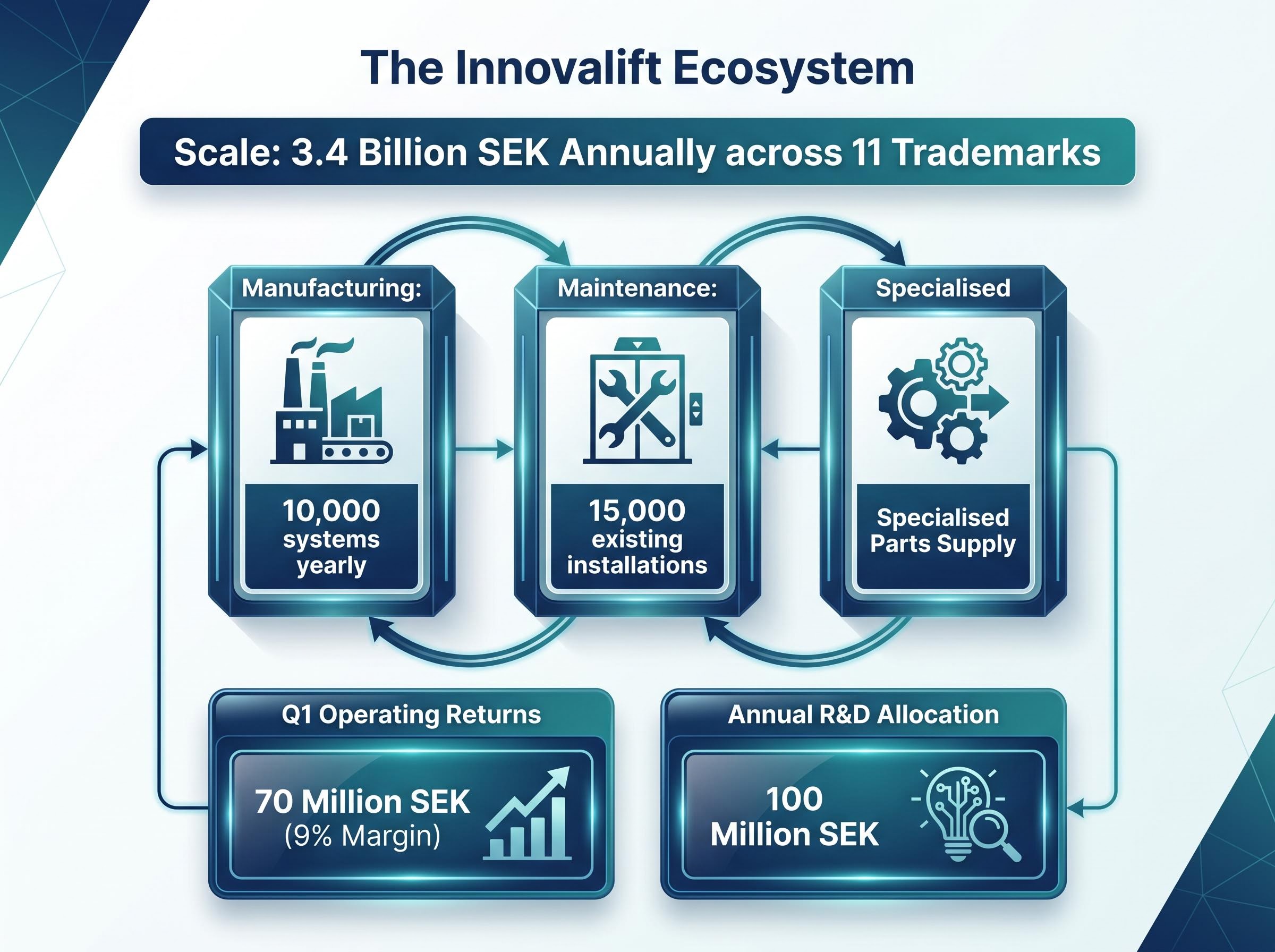

The accessibility division structurally insulates the broader portfolio by aligning with undeniable demographic shifts. Moving beyond the 90-day earnings cycle reveals how the Innovalift segment connects to massive, long-term global changes like ageing populations. The global home elevator market is projected to grow from $3.8 billion in 2026 to $6.5 billion by 2036. This macro-level expansion provides a predictable tailwind for accessibility and vertical mobility operations.

According to company data, the subsidiary currently generates 3.4 billion SEK annually across eleven distinct trademarks. This scale is supported by a calculated shift toward recurring revenue models rather than a pure reliance on cyclical new installations. The division relies on three distinct pillars to secure its revenue base:

According to company data, first-quarter subsidiary metrics showed 70 million SEK in operating returns at a 9 percent margin. Commercial readers evaluating these numbers can see the true long-term security of this recurring revenue base. The strategic weighting toward maintenance contracts smooths out the earnings volatility traditionally associated with industrial manufacturing.

The European accessibility sector remains highly fragmented, creating a prime target for future consolidation without the need to enter new business categories. Operating eleven distinct trademarks across ten integrated organisations gives the division a significant strategic advantage. It allows the conglomerate to acquire regional competitors, integrate their service contracts, and scale operations rapidly through existing distribution networks.

The organisation commits 100 million SEK annually to research and engineering. This capital allocation directly supports the 2050 carbon neutrality goal while simultaneously capturing market share from smaller competitors who cannot fund environmental compliance. The interplay between sustainable engineering and strategic acquisitions positions the division to absorb smaller operators as regulatory pressures mount.

This systematic acquisition strategy relies on absorbing local operators and migrating their client books onto the proprietary maintenance platform. By executing this consolidation playbook, the conglomerate continuously expands its defensive revenue moat while advancing its broader carbon reduction objectives.

For readers wanting to see how this consolidation playbook impacts corporate valuation, our dedicated guide to Latour’s strategic acquisitions details how adding 500 million SEK in annualised net sales is helping to counteract listed portfolio underperformance.

A clear synthesis of the current data highlights the contrast between listed portfolio values and the internally managed subsidiaries. The listed asset portfolio experienced a 9 percent drop in value, driving a negative 6.1 percent year-to-date yield. However, this short-term metric stands against a 540 percent aggregate yield over a fifteen-year horizon.

Executive commentary suggests that foreign exchange pressures are expected to soften moving into the second quarter of 2026. Anticipated top-line projections for the 2026 and 2027 fiscal periods are holding steady. This operational stability confirms that the core industrial engine remains structurally sound.

The latest Riksbank monetary policy report provides institutional context for this outlook, detailing the macroeconomic drivers behind the Swedish krona’s recent appreciation and its specific impact on export valuations.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. These statements are speculative and subject to change based on market developments and company performance.

Monetary valuation shifts and mature sector stagnation remain primary hazards in the near term. The rotational capital flow currently penalising the stock price ignores the structural advantages encoded into the proprietary divisions. By maintaining pricing power and executing strategic consolidations, the conglomerate has built a framework designed to outlast immediate cyclical downturns.

The commercial verdict points to sustainable margins driving future value. Evaluators who look past the immediate market penalty will recognise the underlying strength of the proprietary industrial model.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The paradox lies in a 9.0 percent drop in corporate equity valuations driven by foreign exchange headwinds, which masked a 5 percent baseline expansion in proprietary subsidiary requests on a constant currency basis.

The internally managed industrial model provides insulated pricing power, direct management control, and targeted capital allocation, allowing proprietary divisions to defend margins even during significant revenue translation declines.

Nord-Lock achieved 166 million SEK in operating profit with a 29.4 percent ratio, while Caljan saw a 34 percent surge in orders and a 44 percent jump in revenues, reporting a 16.5 percent profit margin.

The Innovalift strategy focuses on the growing global home elevator market by manufacturing systems, securing high-margin maintenance contracts, and supplying specialised parts across eleven trademarks, generating a stable recurring revenue base.