Vance Pulls Out of Iran Talks, Sending Brent Below $80

13 mins ago

On 29 April 2026, Investment AB Latour shares contracted by nearly 20% following the release of its first-quarter earnings. An objective investment analysis of Latour requires looking past this immediate market reaction to understand the underlying industrial fundamentals. The morning sell-off was driven heavily by foreign exchange headwinds and net asset value adjustments rather than core business failures.

Inside the company’s proprietary factories, commercial demand remains strong. A stark divergence has emerged between the macroeconomic panic reflected in the equity pricing and the cash-generating reality of the manufacturing subsidiaries.

This assessment provides a framework for dissecting the first-quarter earnings report. Investors must determine whether the morning sell-off represents a structural decay in the portfolio or a transient macroeconomic pricing anomaly. By separating paper losses from organic commercial growth, financial professionals can better evaluate the true strength of the industrial operations.

Reported revenue figures often obscure the operational health of international manufacturing businesses. When a company operates globally but reports in a local currency, fluctuating exchange rates create reporting headwinds that mask organic commercial growth.

Longitudinal NBER research on exchange rate variability demonstrates that localized currency fluctuations frequently distort the perceived risk and cost of capital for multinational firms, even when their underlying commercial operations remain highly productive.

According to company data, during the first quarter, foreign exchange translations negatively impacted corporate revenue by approximately 6%. This paper loss stands in direct contrast to a 5% baseline expansion in incoming requests across the proprietary subsidiaries.

The weakness of the Swedish Krona alters the consolidated reporting figures, but it does not indicate a structural loss of market share or a decline in product competitiveness. The physical volume of goods ordered and shipped continues to expand.

“For long-term holding companies, transient currency fluctuations rarely alter the intrinsic cash-generating capacity or structural advantages of proprietary manufacturing subsidiaries.”

Understanding this mechanism allows investors to separate macroeconomic noise from fundamental signals. Evaluating commercial strength independently of monetary policy shifts provides a clearer picture of an enterprise’s true trajectory.

The market reaction on Wednesday morning was immediate and severe. Institutional algorithms and retail investors systematically sold off positions as headline figures triggered automated risk limits.

Corporate equity valuations sank 19.73% during initial trading sessions, dropping from 262.75 SEK down to 210.90 SEK. The primary catalysts for this negative sentiment were a 5.9% drop in net asset valuation alongside rising debt obligations. According to company data, total consolidated debt obligations expanded to 15.3 billion SEK, pressuring the perceived safety of the balance sheet.

This rapid equity contraction created a rare NAV discount for the holding company, presenting an unusual valuation dynamic for investors accustomed to its historical pricing premiums.

However, these lagging benchmark comparisons ignore the resilient expansion in non-acquired invoiced goods. The manufacturing divisions continued to execute on their forward order books. Modified operating profits for the industrial operations reached 886 million SEK, retaining a strong 13.2% profitability ratio despite the top-line contraction.

| Headline Metric | Q1 2026 Reported Figure | Underlying Commercial Reality |

|---|---|---|

| Equity Valuation | Drop to 210.90 SEK (-19.73%) | Market reaction driven by FX and NAV adjustments |

| Net Asset Value | Contraction of 5.9% | Asset pricing reflects current interest rate pressures |

| Operating Profit | 886 million SEK | Sustained 30.2% profitability ratio in core operations |

This contrast reveals the gap between the macroeconomic pricing of the holding company and the industrial reality of its holdings. The punishment applied to the equity pricing reflects broader monetary fears rather than a failure of the proprietary business model.

A forensic examination of the manufacturing divisions reveals divergent outcomes that challenge the broader narrative of contraction. While construction-exposed units faced sluggish environments, other sectors experienced surging demand. The internal industrial engine remains fundamentally sound, with exceptional growth in specific niches offsetting cyclical weakness elsewhere.

The fastening and logistics subsidiaries are currently benefiting from substantial infrastructure, defence, and energy contracts. These divisions demonstrate how targeted industrial positioning can capture high-margin growth even during periods of consolidated macroeconomic weakness.

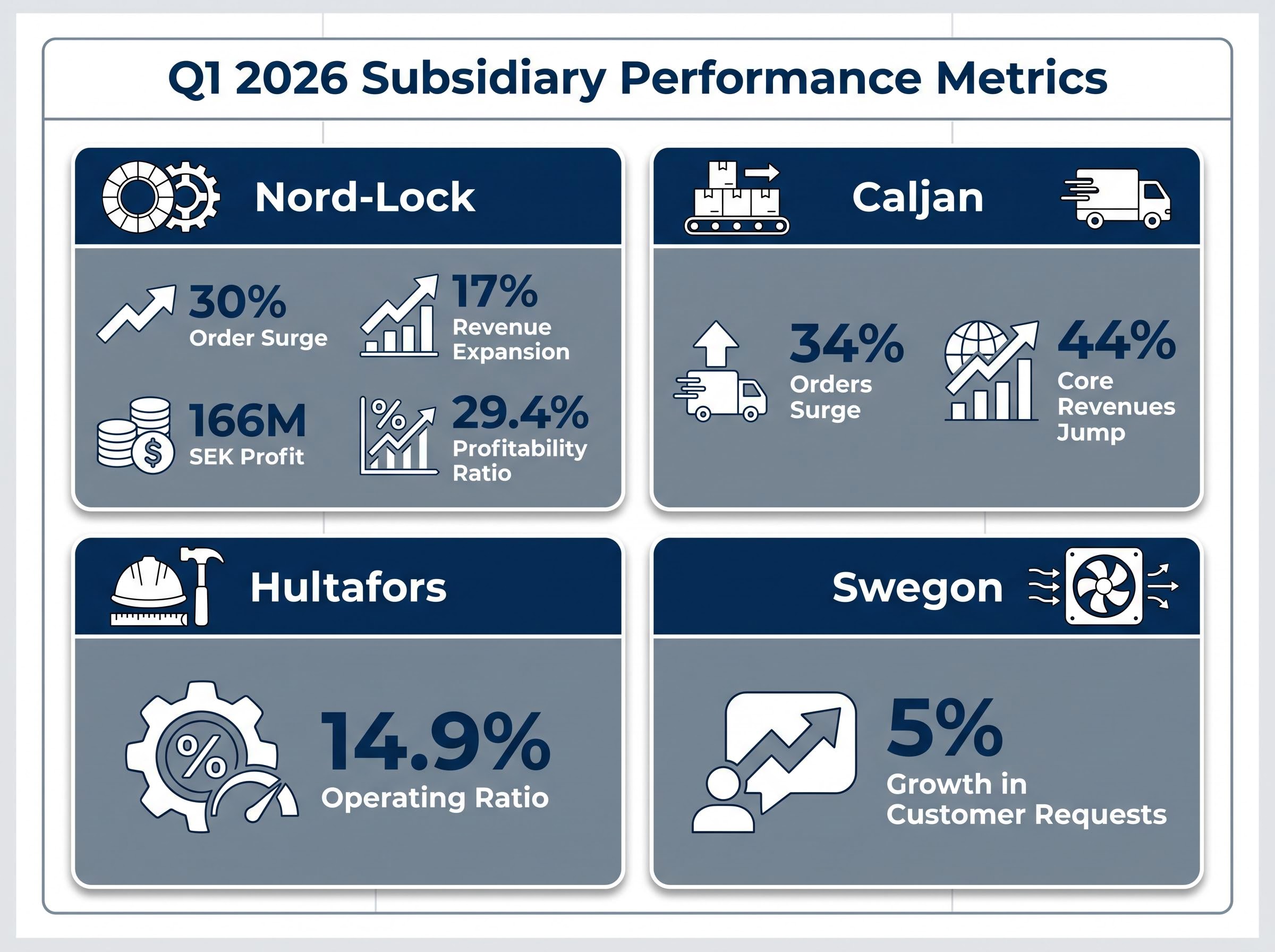

The performance metrics for these two standout divisions highlight their cash-generating capacity:

According to company data, Nord-Lock achieved a 30% baseline order surge and a 17% intrinsic revenue expansion. The fastening division generated 166 million SEK in operating profit, achieving a 29.4% profitability ratio. Caljan saw baseline orders surge by 34%, driven by logistics automation requirements. Core revenues for the Caljan division jumped by 44% during the quarter.

These double-digit expansions prove the core business is actually accelerating in markets insulated from consumer spending slowdowns.

The divisions exposed to the residential and commercial building sectors are navigating a softer environment by prioritising margin protection over volume expansion. Management has actively calibrated operations to defend profitability ratios despite sluggish volume.

Hultafors successfully maintained a 14.9% operating ratio during the quarter. This stability indicates disciplined cost control rather than structural decline. Meanwhile, Swegon recorded a 5% inherent growth in customer requests, suggesting that building ventilation upgrades continue to attract capital allocation.

By drilling down into these specific subsidiaries, the cash-generating reality beneath the parent company’s consolidated earnings becomes visible. The portfolio contains areas of high-margin momentum that the consolidated currency translation obscured.

Evaluating the first-quarter volatility requires expanding the timeline from a single reporting period to a multi-year horizon. Short-term valuation dips are a recurring feature of holding companies, rather than evidence of systemic failure.

Recognising underpriced stock market risk during periods of high geopolitical tension allows institutional capital to distinguish between standard cyclical compressions and fundamental corporate breakdowns.

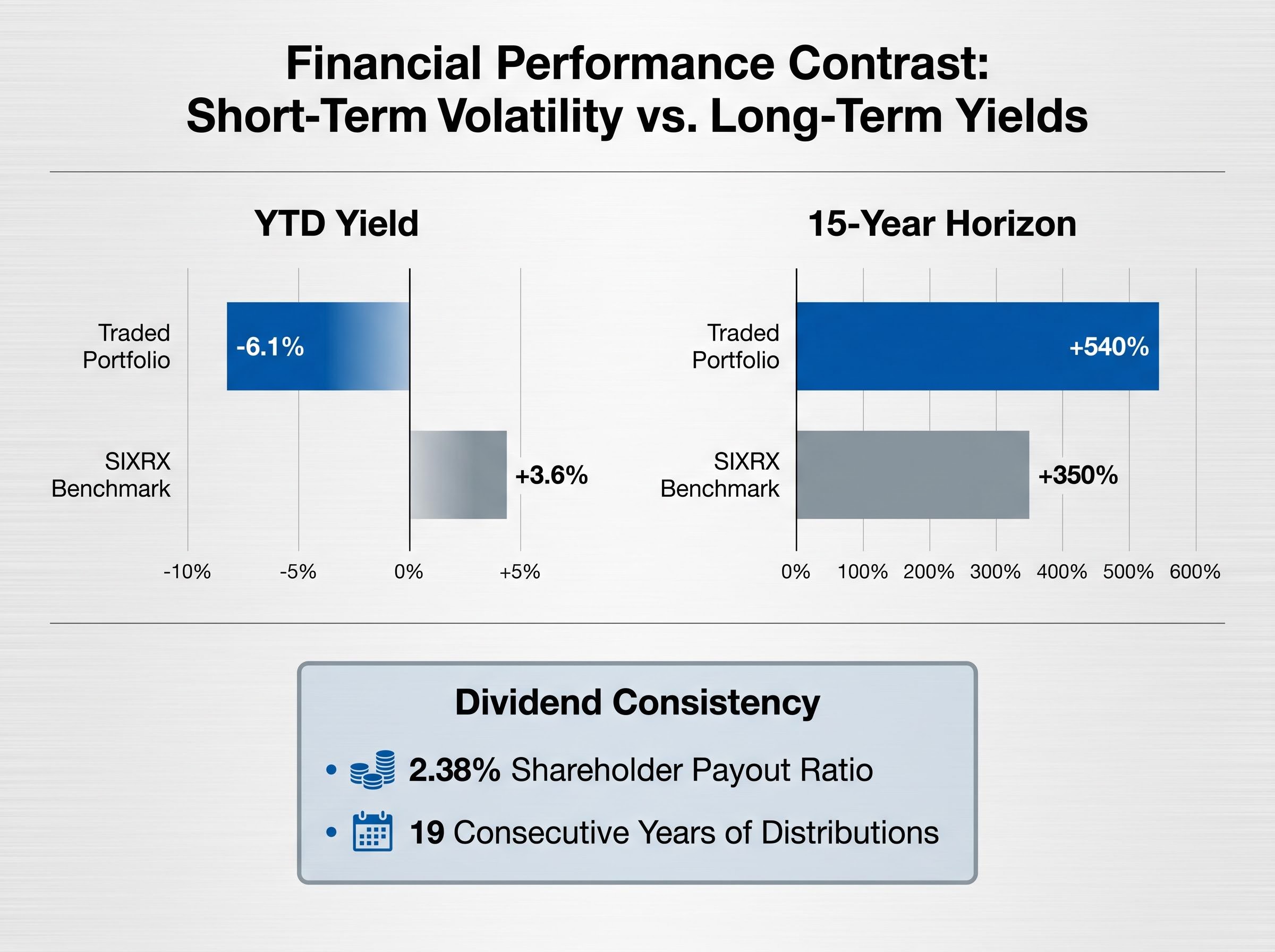

According to company data, the year-to-date aggregate yield for the publicly traded asset portfolio stood at a negative 6.1%. This compares poorly to the broader SIXRX benchmark, which recorded a 3.6% advance over the same period. However, contrasting this short-term underperformance against prolonged timeframes reveals a different trajectory.

Over a 15-year horizon, the traded portfolio generated a 540% aggregate yield, heavily outperforming the benchmark index’s 350% gain. The enterprise also provides a 2.38% shareholder payout ratio, supported by 19 consecutive years of distributions. This historical consistency offers commercial investors the confidence required to weather transient drawdowns.

“Leadership maintains a philosophy of extended holding periods, focusing on leveraging structural advantages through varying economic cycles rather than optimising for quarterly reporting expectations.”

The current turbulence represents a standard cyclical compression. The strategy relies on maintaining disciplined capital allocation and allowing compounding returns to accumulate over decades, absorbing periodic foreign exchange shocks along the way.

Leadership is actively shaping the portfolio for future cycles rather than passively waiting for foreign exchange headwinds to subside. Recent corporate manoeuvres represent calculated optimisations designed to compound future capital. Management is utilising the current economic turbulence to upgrade portfolio quality and set the stage for margin expansion.

This structural upgrade is executing across three primary strategic growth vectors:

According to company data, as part of this optimisation, Caljan is shuttering a specialised German division that generated 60 million SEK annually but operated with minimal profitability. Simultaneously, newly integrated enterprises across the broader portfolio are projected to add roughly 500 million SEK toward annualised turnover.

The Innovalift division exemplifies this forward-looking strategy. According to company data, the subsidiary generates 3.4 billion SEK annually while targeting absolute zero carbon outputs before 2050. By aligning technological integration with demographic mega-trends, leadership is positioning the core industrial engine to capture structural demand when macroeconomic conditions normalise.

This aggressive decarbonisation timeline positions the subsidiary to benefit directly from the EU Net-Zero Industry Act, ensuring its manufacturing processes remain fully compliant with incoming regional climate mandates.

The nearly 20% market reaction on 29 April 2026 disproportionately punished foreign exchange headwinds while entirely ignoring exceptional subsidiary order growth. The fundamental value of the proprietary industrial operations remains intact. The underlying manufacturing divisions continue to generate strong margins and capture infrastructure market share.

Anticipated earnings per share and top-line projections for 2026 and 2027 are holding steady despite the current equity pricing. The reiteration of a sustained 30.2% profitability ratio in the industrial core confirms that operational efficiency has not decayed. Assuming currency markets stabilise by the second quarter, the portfolio is well-positioned for immediate margin expansion.

For investors weighing these operational strengths against the current macroeconomic climate, our comprehensive walkthrough of stock market warning signals provides essential context on how broader geopolitical pressures might delay that expected stabilisation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Investment AB Latour's nearly 20% share decline on 29 April 2026 was primarily driven by foreign exchange headwinds and net asset value adjustments reported in its first-quarter earnings. These factors masked strong underlying commercial demand in its manufacturing subsidiaries.

Foreign exchange translations negatively impacted Investment AB Latour's corporate revenue by approximately 6% in Q1 2026. This was a paper loss, contrasting with a 5% baseline expansion in incoming requests across its proprietary subsidiaries.

Nord-Lock saw a 30% order surge and 17% revenue expansion, while Caljan experienced a 34% order surge and 44% core revenue jump. These fastening and logistics divisions demonstrated strong performance, benefiting from infrastructure, defense, and energy contracts.

Over a 15-year horizon, Investment AB Latour's traded portfolio generated a 540% aggregate yield, significantly outperforming the SIXRX benchmark's 350% gain. The company also boasts 19 consecutive years of shareholder distributions.

Leadership is focusing on divesting low-margin assets, making targeted bolt-on acquisitions in high-margin niches, and expanding into demographic-aligned mega-trends. This includes initiatives like Innovalift's zero carbon output target by 2050.