Nasdaq Falls 4% as Broadcom AI Miss Sparks Semiconductor Rout

5 hrs ago

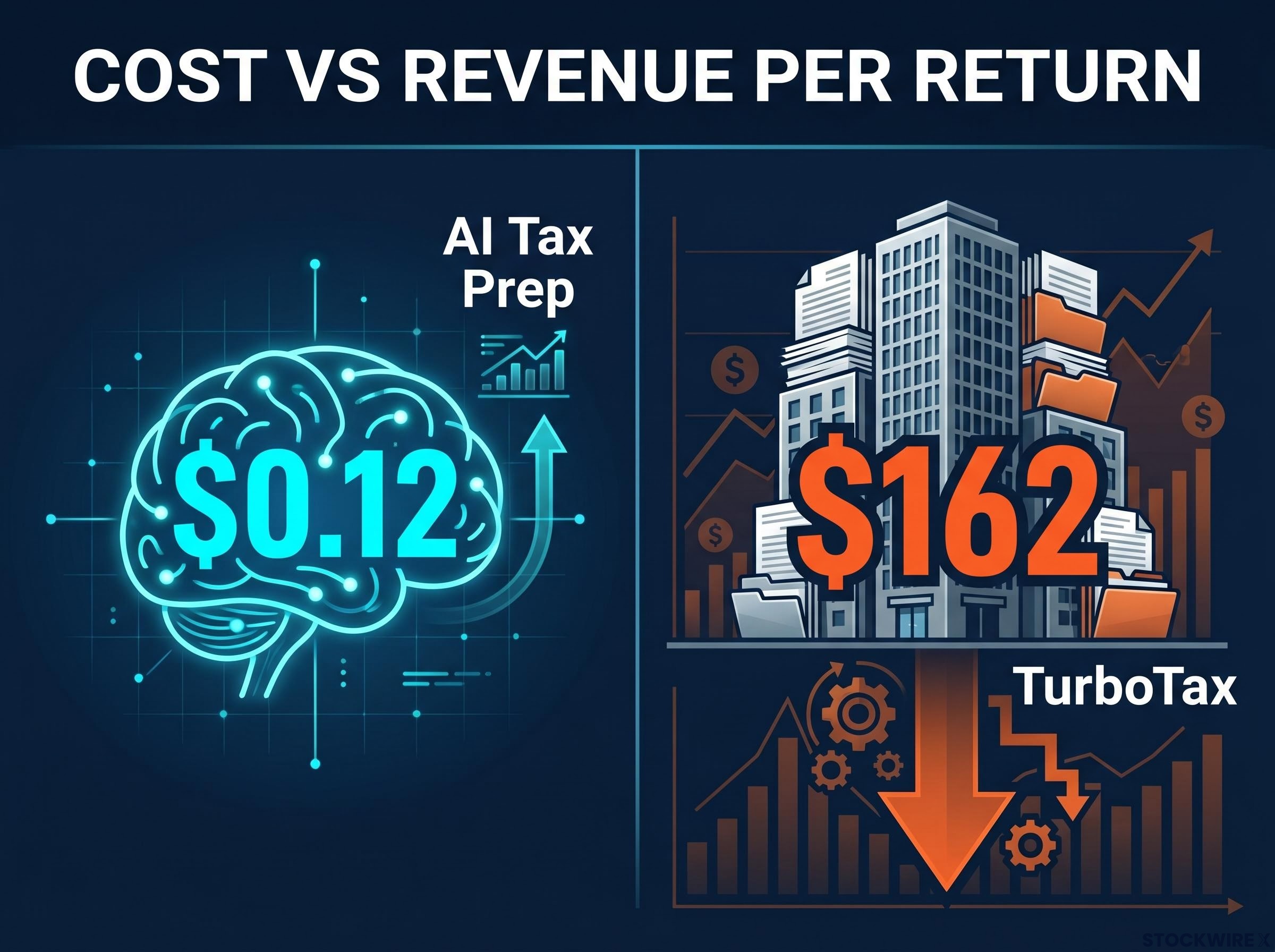

Goldman Sachs has cut its Intuit price target by nearly half, from $519 to $276, and downgraded the stock to a Sell rating. The call, led by analyst Gabriela Borges, rests on a single striking data point: AI-native tax preparation products can process a standard individual return for approximately $0.12, while TurboTax generates a blended average of roughly $162 per return. That cost gap, Goldman argues, is wide enough to fund a new class of competitors that do not need years of venture capital subsidy to undercut the incumbent. What follows is a breakdown of Goldman’s full thesis: the cost economics driving the call, the specific business units most exposed, what makes this competitive threat structurally different from prior fintech challenges, and the factors the analysts themselves say could soften the blow.

The rating action is blunt by Wall Street standards. A near-50% price target reduction on a mega-cap software company signals a fundamental reassessment of the business model, not a routine trimming of estimates.

Borges and her team argue that consensus estimates for the next two years imply essentially no deceleration in Intuit’s revenue growth, a premise Goldman considers dangerously optimistic given the emerging AI competitive environment.

According to Goldman Sachs, Street estimates for the following two years imply essentially no deceleration in revenue growth, a premise the analysts view as optimistic given the competitive dynamics now forming around TurboTax.

Goldman expects shares to remain range-bound over coming quarters as estimate revisions weigh on sentiment. The note frames this not as a temporary overhang but as the beginning of a structural repricing cycle.

The numbers arrive first, and they carry their own argument. According to Goldman’s note, the AI inference cost to process a standard individual tax return sits at approximately $0.12. TurboTax’s blended average revenue per return is approximately $162.

| Metric | AI tax prep (Goldman estimate) | TurboTax |

|---|---|---|

| Cost / revenue per return | ~$0.12 | ~$162 |

| Implied margin available to AI entrants | Substantial; pricing can undercut TurboTax without sustained VC subsidy | |

That gap is what separates this competitive threat from earlier fintech disruption waves. Prior challengers to TurboTax typically required years of loss-making subsidies to offer free or discounted tax filing. The AI cost floor changes that calculus. A new entrant operating at inference cost does not need to burn capital to be price-competitive; the economics sustain aggressive pricing on their own.

The magnitude of this cost compression is documented in the Stanford HAI 2025 AI Index, which found that the inference cost for a system performing at GPT-3.5 level dropped more than 280-fold between November 2022 and October 2024, a trajectory that makes the $0.12 per-return figure Goldman cites structurally credible rather than speculative.

In Goldman’s base-case scenario, 20% of U.S. tax filers migrate to AI-only platforms by 2030, producing TurboTax revenue approximately 18% below fiscal 2025 levels.

Goldman’s base case projects TurboTax revenue approximately 18% below FY2025 levels by 2030, assuming 20% of U.S. filers migrate to AI-only platforms. Competitive pressures are expected to build materially over the next two years.

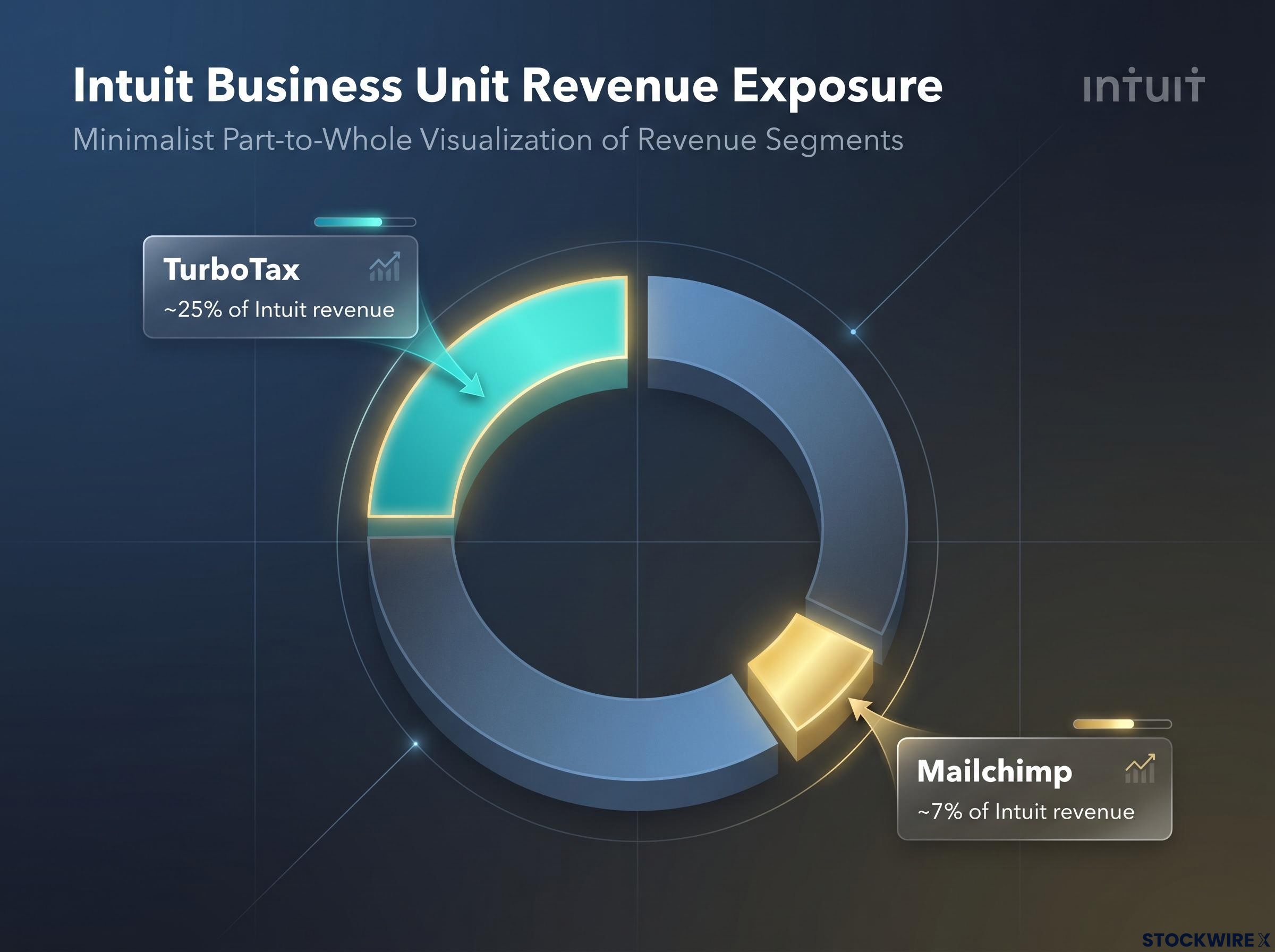

TurboTax accounts for approximately 25% of Intuit’s total revenue and operating income, making it the largest single source of competitive risk in Goldman’s framework. The entire base-case scenario, with its 18% revenue decline projection, sits on this business unit.

| Business unit | Approximate share of Intuit revenue | Goldman’s directional risk assessment |

|---|---|---|

| TurboTax | ~25% | Primary exposure; base-case revenue decline of ~18% vs FY2025 by 2030 |

| Mailchimp | ~7% | Secondary pressure; slight YoY revenue decline in most recent quarter |

Investors often treat Intuit as a diversified business where QuickBooks insulates against TurboTax volatility. Goldman’s note complicates that view. Mailchimp, representing roughly 7% of revenue, posted a slight year-over-year revenue decline in the most recent reported quarter, despite management targeting double-digit exit-rate growth in fiscal 2026.

Goldman expects further deceleration as Intuit adjusts its cost structure for a lower-growth profile. The combination of TurboTax competitive risk and Mailchimp softness is the basis for Goldman’s view that two-year consensus estimates are too optimistic; both revenue lines are under simultaneous pressure rather than offsetting each other.

AI-native tax preparation refers to processing a standard individual tax return using AI inference, where the computational cost sits at the model’s inference price point, rather than through a traditional software licence or assisted-service model. The distinction matters because it creates a cost floor dramatically lower than any prior competitive model in the tax filing market.

Intuit has survived more than 20 years of technological disruption, a track record Goldman’s own note acknowledges. The company adapted through the emergence of free online filing and the shift to mobile. That history is not trivial. It is the strongest counterargument to any disruption thesis.

What Goldman argues is structurally different this time is the cost mechanism. Prior fintech challengers needed sustained venture capital to subsidise free filing. AI-native processing does not. The inference cost floor is low enough that new entrants can be price-competitive from day one without external funding.

The pricing pressure Goldman identifies in tax preparation is part of a broader legacy software repricing cycle: across the US software market, AI inference economics are forcing a reassessment of per-unit and per-seat models that were built on human-labour cost assumptions, with the wealth destruction in early 2026 concentrated precisely in the platforms most exposed to this cost-floor compression.

Goldman’s note names three AI-powered competitors the analysts are tracking:

Intuit has its own AI counter-narrative. The company has built Intuit GenOS, described as a proprietary generative AI operating system powering TurboTax, Credit Karma, QuickBooks, and Mailchimp, according to the company’s Investor Day FY26 presentation.

Intuit has described its competitive positioning as resting on “proprietary data, domain-specific AI platform capabilities, and AI-powered human expertise.” (Intuit Q3 FY24 press release, 23 May 2024)

Whether that proprietary platform can defend a $162 revenue-per-return model against a $0.12 cost floor is the question Goldman’s note forces into the open.

Goldman’s Sell rating is not an argument that Intuit is headed to zero. The note identifies three specific factors that could partially cushion earnings, each worth weighing against the scale of the projected revenue decline:

The bear case rests on DIY self-file volume erosion, but TurboTax Live growth tells a different story: the assisted-filing segment has crossed $2.8 billion in revenue and now represents over 50% of total TurboTax revenue, growing 36% in a single year, which is precisely the upmarket migration Goldman identifies as the most strategically interesting offset to AI displacement of self-filers.

Goldman’s framing is precise: these factors could partially cushion earnings, not reverse the competitive trajectory. The distinction matters for sizing the downside.

Goldman’s 2030 projection, TurboTax revenue approximately 18% below FY2025 assuming 20% filer migration, provides the clearest forward framework. The critical variable is migration velocity. The 20% figure is a base-case threshold, not a certainty. How quickly AI-native products gain consumer adoption will determine whether the bear case, base case, or a softer scenario plays out.

Three variables will shape which path materialises:

Goldman’s call carries implications beyond Intuit. It reflects a shift in how analysts model AI disruption risk for software incumbents, treating AI cost economics as a structural pricing-floor threat rather than a long-run hypothetical. The note applies a specific quantitative framework, cost-per-unit versus revenue-per-unit, that could be replicated across other software categories where AI inference can replicate the core product function.

For investors trying to size the downside from Goldman’s framework against current market pricing, Intuit’s forward valuation has already compressed sharply, with the stock trading near $302 and every major Wall Street firm, including Morgan Stanley, J.P. Morgan, and Evercore ISI, still maintaining positive ratings after cutting price targets by 20-27%, a divergence that raises questions about whether the market has already discounted the competitive scenario Goldman is modelling.

Goldman expects Intuit’s shares to remain range-bound as estimate revisions weigh on sentiment over coming quarters.

Goldman’s quantitative case rests on a specific cost asymmetry and a migration assumption. Both are contestable. Neither is easily dismissed. A $0.12 processing cost against $162 in revenue per return is a gap large enough to fund aggressive competition without external subsidy, and that structural reality does not depend on any single competitor succeeding.

Intuit’s adaptive track record over more than two decades is the strongest counter-argument, though Goldman’s own analysts acknowledge it while still arriving at a Sell rating. The two metrics that will function as early signals of which scenario is unfolding are Mailchimp’s growth trajectory in upcoming quarters and any TurboTax market share data disclosed in future earnings reports.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors. Forward-looking statements attributed to Goldman Sachs reflect that firm’s analytical assumptions and are subject to change based on market developments and company performance.

Goldman Sachs downgraded Intuit to a Sell rating and cut its price target from $519 to $276, representing a near 50% reduction, based on the view that AI-native tax preparation products pose a structural threat to TurboTax's revenue model.

AI inference can process a standard individual tax return for approximately $0.12, compared to TurboTax's blended average revenue of roughly $162 per return, giving new entrants enough margin to price competitively without requiring years of venture capital subsidies.

TurboTax, which accounts for approximately 25% of Intuit's total revenue, is the primary exposure, while Mailchimp, representing roughly 7% of revenue, is also under pressure after posting a slight year-over-year revenue decline in its most recent quarter.

Goldman's base case projects TurboTax revenue approximately 18% below fiscal 2025 levels by 2030, assuming that 20% of U.S. tax filers migrate to AI-only platforms over that period.

Goldman identifies three potential cushions: Intuit's partnership with Anthropic as an AI capability enhancer, the possibility that displaced DIY filers migrate to higher-revenue assisted filing services, and a 17% workforce reduction announced in May 2026 that provides a cost-structure lever.