NWL’s 62% ROE vs a 44% Share Price Fall: What the Gap Signals

15 mins ago

Intuit shares have lost more than half their value in 2026, recently trading near $302, yet every major Wall Street firm covering the stock has maintained a positive rating. That gap between price and analyst conviction frames the central question for investors evaluating INTU at current levels. The decline accelerated sharply in May 2026 following a Q2 FY2026 earnings release that, by management’s own characterisation, reflected a strong quarter. A simultaneous announcement of a 17% global workforce reduction unsettled markets even as executives framed it as a strategic reallocation toward AI. For U.S. investors weighing large-cap technology names at multiyear lows, Intuit presents a test case in separating sentiment from substance. What follows is a structured framework for evaluating the stock across five dimensions: current valuation context, segment-level business trajectory, the restructuring’s margin implications, competitive positioning and regulatory risk, and concrete return scenarios under conservative and optimistic assumptions.

A stock that has halved looks like damaged goods. The forward multiple tells a different story. At approximately $302, Intuit trades at roughly 17.6-17.8x forward earnings, a range that, as J.P. Morgan’s analysts observed, “implies little value for GenAI-driven upsell opportunities in Small Business and Self-Employed.”

“The current mid-teens forward P/E implies little value for GenAI-driven upsell opportunities in Small Business and Self-Employed.” — J.P. Morgan, 15 May 2026

That valuation compresses Intuit into a multiple typically reserved for low-growth, margin-stable businesses. It assigns near-zero credit for the AI optionality embedded across QuickBooks, TurboTax, and Credit Karma, products that management is actively re-engineering around generative AI capabilities.

The broader growth stock discount of approximately 21% below fair value, a level Morningstar data shows has occurred less than 5% of the time since 2011, provides the macro frame within which Intuit’s compression sits; the company is not an isolated case of sentiment-driven selling but part of a sector-wide repricing concentrated in software and AI-adjacent names.

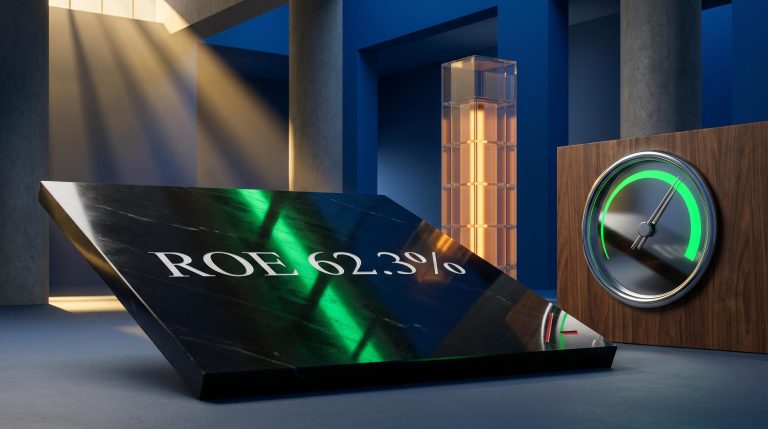

The Wall Street reaction to Q2 FY2026 earnings produced a cluster of target cuts between 15-19 May 2026. Every firm reduced its price target substantially, and every firm retained a positive rating.

| Firm | Previous Target | Revised Target | Rating |

|---|---|---|---|

| Morgan Stanley | $520 | $400 | Overweight |

| Goldman Sachs | $540 | $410 | Buy |

| J.P. Morgan | $450 | $390 | Overweight |

| Evercore ISI | $530 | $415 | Outperform |

Goldman Sachs argued that the post-earnings sell-off “over-discounts” regulatory risk. Evercore ISI called it “overdone” given durable small-business franchise strength. The reductions themselves ranged from approximately 20-27% off prior targets, yet even the lowest revised target (J.P. Morgan at $390) sits roughly 29% above the current share price.

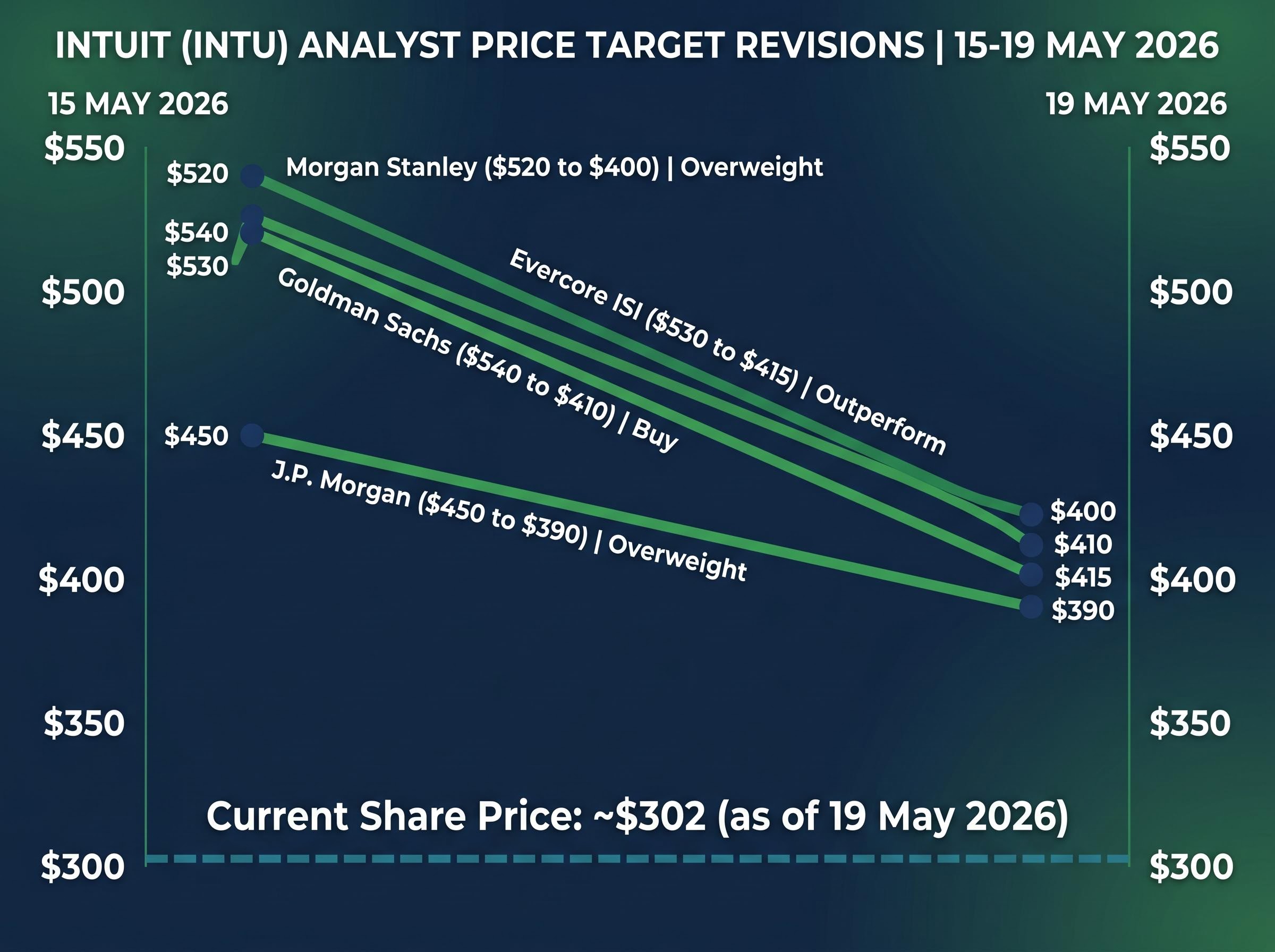

Consolidated quarterly revenue grew 10% to approximately $8.5 billion in the most recent period. The composition of that growth matters more than the headline.

Global Business Solutions, the QuickBooks ecosystem, grew 15% in the quarter. Management projects approximately 16% growth for the full fiscal year. Within that segment, online accounting revenue climbed 22%, online payment volume expanded 30%, and the enterprise tier grew 38%. This division accounted for over 60% of total operating profit in FY2025, and management expects that share to reach approximately 70% within a few years.

The consumer segment (TurboTax) grew approximately 8%. The more instructive figure sits underneath: TurboTax Live revenue reached $2.8 billion, representing over 50% of total TurboTax revenue and growing 36%.

TurboTax Live crossed the 50% threshold of total TurboTax revenue, growing 36%, a mix shift that moves the consumer segment toward higher-margin assisted filing.

Credit Karma is projected to generate approximately $2.7 billion in revenue for the current fiscal year, growing at approximately 19%. Its contribution to operating profit, however, remains modest at roughly 6% of the total (FY2025 data), and its performance is tied to consumer credit conditions, a genuine cyclical consideration rather than one to dismiss.

| Segment | Recent Growth Rate | FY2026 Guidance | Share of Operating Profit |

|---|---|---|---|

| Global Business Solutions | 15% | ~16% | ~60%+ (trending toward 70%) |

| Consumer (TurboTax) | ~8% | Not separately guided | ~34% |

| Credit Karma | ~19% | ~$2.7B revenue | ~6% |

GAAP earnings are projected to grow approximately 16% for the full fiscal year. The dividend was raised 15% to approximately $4.80 annually, representing roughly a 1.5% yield. This is not the financial profile of a business in structural decline.

Intuit announced on 14 May 2026 that approximately 17% of its global workforce would be eliminated. Bloomberg News reported the figure at roughly 7,000 employees, though this has not been independently confirmed. The largest reductions were concentrated in corporate support functions and overlapping roles created by prior acquisitions, particularly within Mailchimp and Credit Karma.

CEO Sasan Goodarzi framed the cuts explicitly:

“This is a reallocation toward AI, product, and customer-facing roles rather than a pure cost-takeout.” — Sasan Goodarzi, CEO, Intuit (Wall Street Journal, 16 May 2026)

The sceptical reading is straightforward: Intuit over-hired after its Mailchimp and Credit Karma acquisitions, and this is a correction dressed in AI language. Both readings can be partially true. The margin arithmetic, however, stands on its own.

The gap between the one-time charge and the recurring savings is the margin lever investors should focus on. A $600-$700 million hit produces $800 million to $1 billion in annual savings, a payback period well under one year.

Goodarzi stated plans to “hire several thousand people in AI engineering, data science, and design” even as overall headcount declines. The destination for that redeployed investment is GenOS, Intuit’s internal generative AI platform, and Intuit Assist, the customer-facing AI assistant built on top of it.

Intuit Assist is now integrated across TurboTax, QuickBooks, Credit Karma, and Mailchimp, handling automated categorisation, cash-flow forecasting, and conversational financial queries. In QuickBooks, Intuit Assist moved from beta to broader rollout in early 2026, according to Motley Fool and Wall Street Journal reporting. Bloomberg Technology confirmed in March 2026 that R&D allocation is actively shifting toward GenOS, the underlying reason that headcount reductions in support functions are framed as compatible with continued product development velocity.

Whether the narrative is partially corporate-speak matters less than whether the margin math and AI investment pipeline are real. The evidence suggests they are.

Investors often reduce Intuit to “the TurboTax company.” The business is more accurately understood as a multi-product financial platform where data continuity, accountant network effects, and embedded payments create structural stickiness.

QuickBooks holds more than 70% of the U.S. cloud-based small-business accounting market, according to IDC research cited by CNBC (25 March 2026). Morningstar characterises the share at roughly 80% by revenue among cloud-based solutions for very small businesses, a figure that reflects a different market segmentation methodology. Morningstar retains a “wide moat” rating for Intuit as of 20 February 2026.

The competitive dynamics that matter break down as follows:

Xero’s AI monetisation strategy, which involves a three-tier pricing model combining bundled features, standalone add-ons, and usage-based automation pricing, illustrates the commercial template that accounting software incumbents are racing to deploy; Intuit’s GenOS and Intuit Assist platform represent its own version of this shift, with the key difference being QuickBooks’ 70%+ U.S. market share providing a far larger installed base over which to amortise AI development costs.

A Jefferies analyst concluded that Intuit’s installed base and data moat make large-scale displacement “unlikely in the next 3-5 years.”

The IRS Direct File programme, after a multistate pilot in the 2024 filing season, is slated to expand nationally for the 2026 filing season for simple returns. Participation in 2025 remained at a low single-digit percentage of eligible filers, according to Treasury and IRS statistics cited by Barron’s.

TIGTA’s 2026 review of IRS Direct File found that actual registrations reached approximately 751,000 taxpayers against an eligible pool estimated at 32 million across 25 states, a participation rate that supports the characterisation of Direct File as a contained threat rather than a mass-market alternative to TurboTax.

Raymond James characterised Direct File as “a reputational overhang more than an immediate earnings threat.” Morningstar estimated that even under an aggressive adoption scenario, TurboTax could lose 5-10 percentage points of U.S. DIY share over a decade. No major simplification bill has passed that would materially restructure the U.S. individual income tax system in a way that displaces TurboTax’s core use cases.

Bank of America analysts reinforced the containment argument: “TurboTax’s most profitable cohort is more complex filers,” the segment least threatened by a free-filing tool designed for simple returns.

The bear case is deliberately pessimistic. It assumes:

Under those assumptions, Intuit would generate over $6.7 billion in GAAP after-tax earnings within five years. Combined with the current 1.5% dividend yield and 5-6% estimated annual cash-flow contribution, the bear-case scenario produces an estimated annual total return in the high single digits.

That floor is itself notable. Most large-cap names reviewed under equivalent valuation frameworks do not clear a high-single-digit return threshold in the bear case.

| Scenario | Assumed EPS Growth | Assumed Terminal Multiple | Estimated 5-Year Annual Return |

|---|---|---|---|

| Bear Case | 6% | 14x | High single digits |

| Expected Case | ~13-16% | ~18-20x | Mid-teens |

| Optimistic Case | ~16-20% | ~22-25x | Potentially high 20% range |

The expected and optimistic cases rely on management executing at or above current guidance, with AI-driven upsell and margin expansion contributing to multiple re-rating. Annual returns in these scenarios are estimated in the teens to potentially high 20% range. As J.P. Morgan observed, the current forward P/E already implies little credit for GenAI-driven upsell; any evidence of execution on that front would likely shift the multiple.

US Tech valuation spreads relative to international developed markets have reached multi-decade extremes in 2026, a structural tension that complicates the simple rerating thesis: if capital continues rotating out of the sector, even fundamentally improving businesses like Intuit may face multiple compression headwinds that outpace earnings growth in the near term.

These scenarios are not predictions. They are a structured way to stress-test what would have to be true for the current price to represent fair value.

The binary framing is tempting. The evidence resists it.

Valuation sits at a multiyear low. The fastest-growing segment is accelerating. The restructuring creates a quantifiable margin lever. The competitive position remains structurally intact. Regulatory risks are real but currently bounded.

The investment case holds if:

The thesis would weaken materially if:

Management projects approximately 16% GAAP earnings growth for the full fiscal year. All four covering firms maintain positive ratings despite target cuts. The 15% dividend increase and net cash position signal financial health alongside the restructuring. Even the bear-case return scenario (high single digits annually) clears a threshold that most large-cap names at similar valuations do not.

The question is not whether Intuit is cheap. The multiple confirms that it is. The question is whether the conditions that make it cheap are temporary or structural, and that is a judgement call each investor makes against their own time horizon and conviction.

Investors exploring whether a concentrated single-stock position in Intuit fits their overall portfolio will find our comprehensive walkthrough of stocks vs ETFs portfolio construction useful; it covers the volatility trade-offs, tax treatment, and core-and-satellite frameworks that apply directly to decisions about holding individual large-cap names versus broad technology index exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

At approximately $302 per share, Intuit trades at roughly 17.6-17.8x forward earnings, a multiple typically associated with low-growth businesses that assigns near-zero credit for AI optionality across QuickBooks, TurboTax, and Credit Karma. Analysts at J.P. Morgan note this implies little value for GenAI-driven upsell opportunities.

Intuit announced the elimination of approximately 17% of its global workforce on 14 May 2026, with reductions concentrated in corporate support functions and roles created by the Mailchimp and Credit Karma acquisitions. CEO Sasan Goodarzi framed it as a reallocation toward AI engineering, data science, and customer-facing roles rather than a pure cost reduction.

Intuit expects annualised cost savings of $800 million to $1 billion once the restructuring is complete, against one-time pre-tax charges of approximately $600-$700 million, implying a payback period of well under one year.

Current evidence suggests Direct File is a contained threat rather than a mass-market alternative; actual registrations reached approximately 751,000 taxpayers against an eligible pool of 32 million, and analysts note TurboTax's most profitable cohort consists of complex filers who are least likely to use a free tool designed for simple returns.

QuickBooks holds more than 70% of the U.S. cloud-based small-business accounting market according to IDC research, with Morningstar placing the figure closer to 80% by revenue among cloud solutions for very small businesses. Competitor Xero has made limited inroads in the U.S., and accounting-firm surveys show no statistically significant QuickBooks share loss between 2023 and 2025.