NWL’s 62% ROE vs a 44% Share Price Fall: What the Gap Signals

15 mins ago

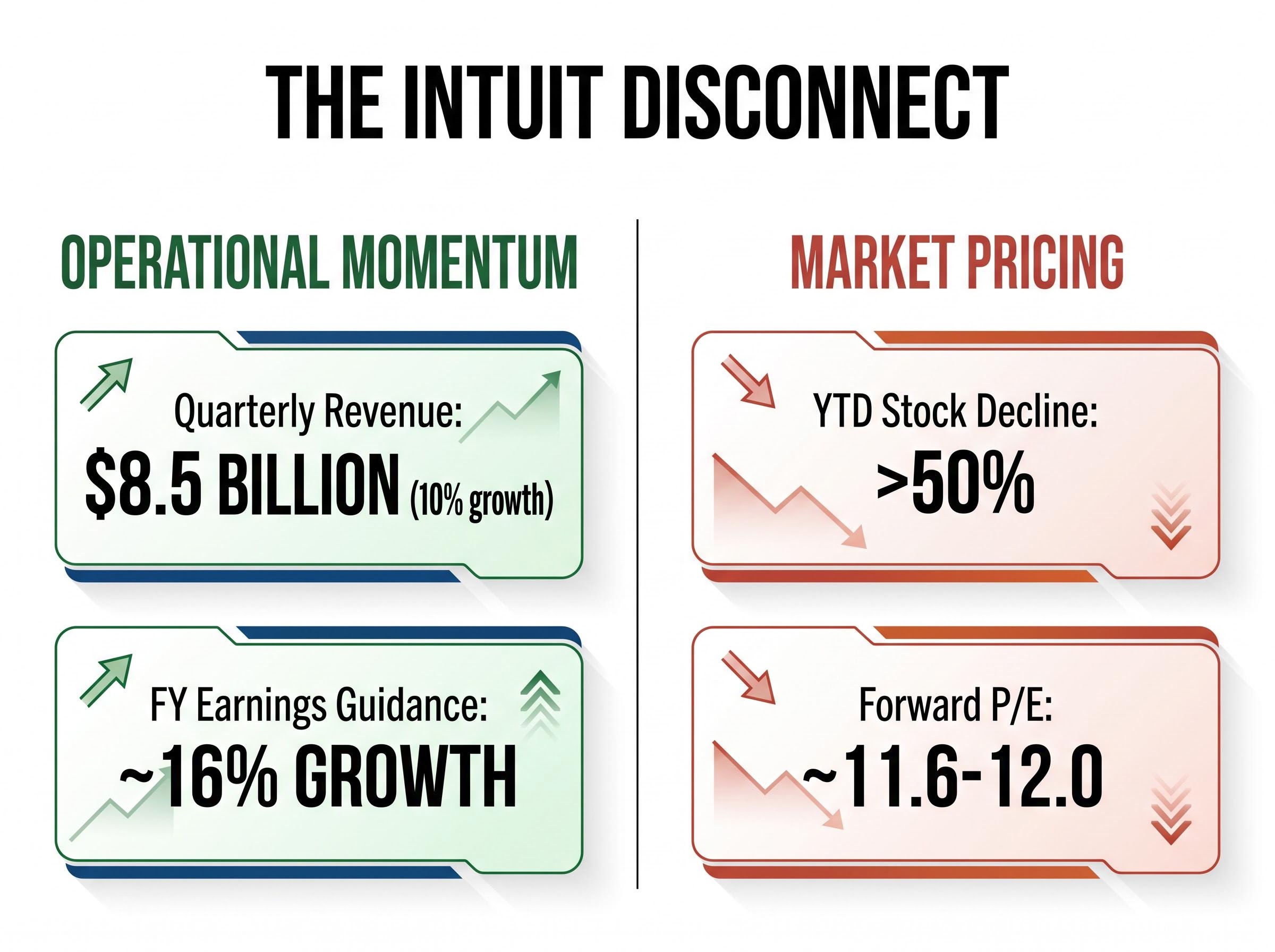

TurboTax Live just crossed 50% of total TurboTax revenue, growing 36% in a single year, yet the stock that owns it has fallen more than 50% in 2026. That gap between operational momentum and market pricing is the entire analytical question.

Intuit remains the dominant incumbent in U.S. consumer tax filing, but the shape of that dominance is changing fast. Budget filers are leaving. Policy risk has materialised and then partially reversed. AI is entering the conversation at the product level. A 17% workforce reduction has surfaced questions about whether management sees structural change arriving before the market does. The stock, trading at roughly $320–$400 range per share with a forward price-to-earnings ratio below 12, is priced as though the answer is already negative.

This analysis works through the structural shifts inside TurboTax specifically, assesses whether the selloff is pricing in real impairment or temporary noise, and gives investors a framework for weighing the competing forces before acting on either side.

Management called the most recent quarter strong. Consolidated quarterly revenue grew 10% to approximately $8.5 billion. Full-year GAAP earnings growth guidance came in at approximately 16%. The stock fell roughly 20% in a single session regardless, and more than 50% year-to-date.

The distinction that matters here is between valuation derating and earnings impairment. Earnings have not collapsed. What has collapsed is the multiple the market is willing to assign to those earnings. At roughly $300 per share and an approximate $85 billion market cap, INTU now trades at a trailing P/E of approximately 19.3-19.5 and a forward P/E of approximately 11.6-12.0, both well below the company’s historical range for a business of this earnings quality.

The key metrics tell the story of the disconnect:

Forward P/E of approximately 11.6-12.0 places Intuit at a valuation rarely seen for a company guiding to 16% earnings growth, a level that prices in material structural impairment whether or not the current financials reflect it.

The size and speed of this decline creates the question this analysis is built to answer: is the market seeing impairment the quarterly numbers have not yet surfaced, or has the repricing overshot?

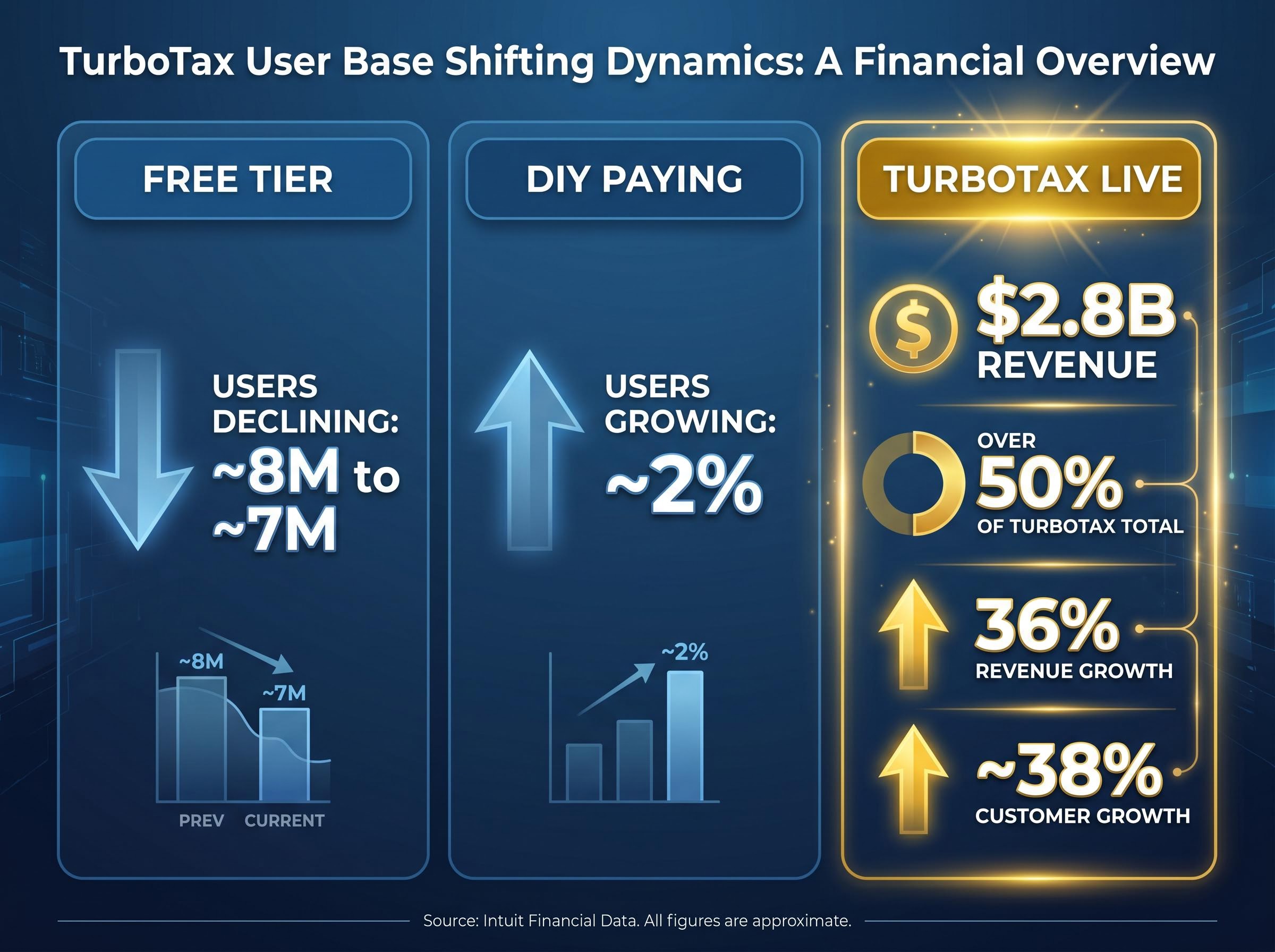

The volume story and the revenue story inside TurboTax are moving in opposite directions, and both are telling the truth. Online units sold are projected to decline roughly 2%. Free-tier filers are falling from approximately 8 million to approximately 7 million. The bottom of the funnel is shrinking.

The top of the funnel is expanding. Paying units are projected to grow 2%. Total TurboTax revenue grew approximately 7%. And the segment driving that growth is not incremental; it is structural.

| Tier | Unit Trajectory | Revenue Contribution | Growth Rate |

|---|---|---|---|

| Free | Declining (~8M to ~7M) | Minimal (no direct revenue) | Negative |

| DIY Paying | Growing ~2% | Below 50% of TurboTax revenue | Low single digits |

| TurboTax Live | Growing ~38% (customers) | $2.8B, over 50% of TurboTax | 36% revenue growth |

TurboTax Live reaching $2.8 billion in revenue, now over 50% of total TurboTax revenue, is not a feature of the product pivot. It is evidence the customer base has already repositioned. The filers who remain are choosing higher-touch, higher-value service. The filers who are leaving were contributing little to revenue in the first place.

Filers entering TurboTax via Credit Karma represent a lower-cost acquisition channel built on existing financial data. These users arrive with income, credit, and tax-relevant information already in the system, creating a stickier onboarding path than cold search traffic.

This channel is projected to grow 54%, partially offsetting the free-tier attrition by replacing departed lower-value users with warmer, higher-intent prospects. The unit economics of the replacement are favourable: lower acquisition cost, higher conversion probability, and a natural upsell path into TurboTax Live.

The policy threat to Intuit’s lower-tier business was not hypothetical. The IRS launched its Direct File pilot for the 2024 filing season across 12 states, producing 140,803 accepted returns from 423,450 log-ins. Users claimed more than $90 million in refunds and saved an estimated $5.6 million in preparation fees.

The programme then accelerated:

The U.S. Treasury’s Direct File pilot data confirmed 140,803 accepted returns, over $90 million in refunds claimed, and an estimated $5.6 million in preparation fees saved during the 2024 season, figures that quantify the programme’s demonstrated appeal to exactly the lower-complexity filers TurboTax has been strategically moving away from.

Up to 32 million taxpayers became potentially eligible for Direct File during its 2025 expansion, a cohort that overlaps directly with TurboTax’s free and entry-level paid tiers.

The November 2025 suspension represents a meaningful near-term reprieve. Intuit’s record $3.9 million in federal lobbying spending in 2025 provides context for the scale of industry response to the programme.

The suspension does not, however, eliminate the policy risk permanently. IRS Free File continues at the $89,000 adjusted gross income (AGI) threshold for the 2026 season. The political logic for a free government filing option has not disappeared with one administrative reversal. Investors who treated the suspension as a permanent resolution may be underpricing the policy tail risk that remains.

The distinction between tax policy noise versus genuine legislative signal is directly relevant here: the IRS Direct File suspension emerged from an administrative decision with no legislative anchor, a structural feature that historically correlates with partial or full reversals as political conditions shift.

The U.S. consumer tax filing market operates across three distinct tiers, each with different competitive dynamics, price points, and vulnerability profiles.

| Tier | Representative Products | Price Point | Vulnerability |

|---|---|---|---|

| Free Government | IRS Direct File (suspended), IRS Free File | $0 | Limited scope; policy-dependent availability |

| Commercial DIY | TurboTax DIY, H&R Block Digital, FreeTaxUSA, Cash App Taxes, TaxAct | $0-$150+ | Price competition from free alternatives |

| Human-Assisted | TurboTax Live, H&R Block in-office | $100-$400+ | AI displacement of guided services |

H&R Block, the nearest scaled competitor, reported U.S. tax preparation and related services revenue of approximately $3.76 billion in fiscal 2025. Cash App Taxes, FreeTaxUSA, and TaxAct occupy the low-cost commercial tier, though current public market share figures for these providers are not available.

TurboTax’s historical dominance in the DIY tier rests on switching costs that accumulate with each filing year:

The lower-income free tier is structurally the most vulnerable to disruption. These filers have simpler returns, lower switching costs, and are the most responsive to free government alternatives. This explains why Intuit’s strategic move upmarket into TurboTax Live is rational: the assisted tier carries higher switching costs, higher revenue per user, and less exposure to government competition than the free tier it is vacating.

Intuit reduced its workforce by approximately 17% of total headcount. Management framed the decision around organisational speed and efficiency, explicitly stating the reduction was unrelated to AI.

Management’s stated position is that the 17% workforce reduction is “unrelated to AI,” a framing that sits uncomfortably alongside a simultaneous acceleration of AI investment across every major product line.

The counter-reading is straightforward. A reduction at this scale, at this moment in AI’s capability trajectory, is more plausibly interpreted as Intuit recalibrating headcount to a future where AI handles more of the work currently performed by knowledge workers inside the product. The timing is difficult to separate from the intent.

Intuit’s stated AI initiatives span the full product portfolio:

The connection to TurboTax Live’s investment case is direct. If AI-native tax tools can replicate the guided-interview experience and provide accuracy guarantees at lower cost, TurboTax Live’s $2.8 billion in revenue and 36% growth rate could become a ceiling rather than a trajectory. The workforce reduction is the most legible signal that management is positioning for structural change. The open question for investors is whether the AI investment strengthens Intuit’s competitive position or represents an acknowledgment that external pressure is already building.

AI pricing models in financial software are already being restructured by peers: Xero’s XeroForce launch introduced a three-tier model with a usage-based tier that links costs directly to automation volume, a design that converts AI capability from a feature into a recurring revenue mechanism and illustrates one path Intuit’s own AI investments could follow.

Starting from a forward P/E of approximately 11.6-12.0 and current GAAP earnings growth guidance of approximately 16%, the valuation mathematics shift depending on three variables: earnings growth rate, terminal multiple, and margin trajectory.

The low case deliberately strips out optimism. Assuming 6% earnings growth (well below current guidance), a 14x forward earnings multiple (modest re-rating from current levels), and no margin benefit from the headcount reduction, Intuit would generate over $6.7 billion in projected GAAP after-tax earnings within five years. Cash flow contribution to total return adds an estimated 5-6% annually. The resulting annual return estimate sits in the high single digits.

What makes the low case analytically interesting is that most companies under a comparable framework do not produce acceptable returns even in their conservative scenario. Intuit does.

| Scenario | Earnings Growth Assumption | Multiple Assumed | Estimated Annual Return |

|---|---|---|---|

| Low Case | 6% | 14x forward | High single digits |

| Base Case | 10-12% | 18-20x forward | Mid-teens |

| High Case | 14-16% | 22-25x forward | Potentially high 20% range |

The upside variables not captured in the low case are where margin expansion enters the picture:

The dividend, raised 15% to approximately $4.80 annually (approximately 1.5% yield), adds a modest but growing cash return component. Under realistic assumptions, the current entry point offers a return floor that clears reasonable hurdle rates even before accounting for the structural tailwinds management is investing in.

Investors who want to stress-test their own return assumptions across the low, base, and high cases outlined above will find our comprehensive walkthrough of scenario analysis for stocks mid-transition useful — it covers probability weighting, entry price discipline, and how to define monitoring triggers that enable evidence-based updates each quarter.

Intuit is a dominant incumbent navigating a genuine structural transition, and the current valuation prices in more impairment than the available evidence currently supports.

Three conditions would validate the bull case:

Two conditions would invalidate the thesis:

At a forward P/E of approximately 11.6-12.0, the stock is priced for a worse outcome than either the current financials or the structural trajectory currently indicate. The question is not whether Intuit faces real risks; it does. The question is whether those risks justify a valuation multiple that implies earnings contraction in a business guiding to 16% growth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

TurboTax Live is Intuit's human-assisted tax filing service that pairs filers with tax professionals through a digital interface. It has grown to $2.8 billion in revenue, now accounting for over 50% of total TurboTax revenue, making it the primary growth engine for Intuit's consumer tax segment.

The decline reflects a valuation derating rather than an earnings collapse, with the market assigning a much lower multiple to Intuit's earnings amid concerns about policy risk from IRS Direct File, AI disruption to its core business, and a 17% workforce reduction that raised structural questions. Intuit's forward P/E has fallen to approximately 11.6-12.0 despite the company guiding for roughly 16% full-year GAAP earnings growth.

The IRS suspended Direct File in November 2025, meaning it will not be available for the 2026 filing season, which provides Intuit a near-term reprieve from direct government competition. However, IRS Free File continues at the $89,000 AGI threshold, and the policy risk has not been permanently eliminated since the suspension was an administrative decision without a legislative anchor.

If AI-native tax tools can replicate TurboTax Live's guided-interview experience and accuracy guarantees at lower cost, the segment's $2.8 billion revenue base and 36% growth rate could face a ceiling rather than continuing its upward trajectory. Intuit's simultaneous 17% workforce reduction and accelerated AI investment across all product lines signals that management is positioning for structural change in how the product is delivered.

Investors should track TurboTax Live revenue growth relative to its current 36% rate, QuickBooks segment growth within the 13-16% range, and whether the QuickBooks profit share expands toward the expected 70% of total operating profit. The Credit Karma acquisition channel growth rate, currently projected at 54%, is also a leading indicator of whether Intuit is successfully replacing lower-value free-tier filers with higher-intent prospects.