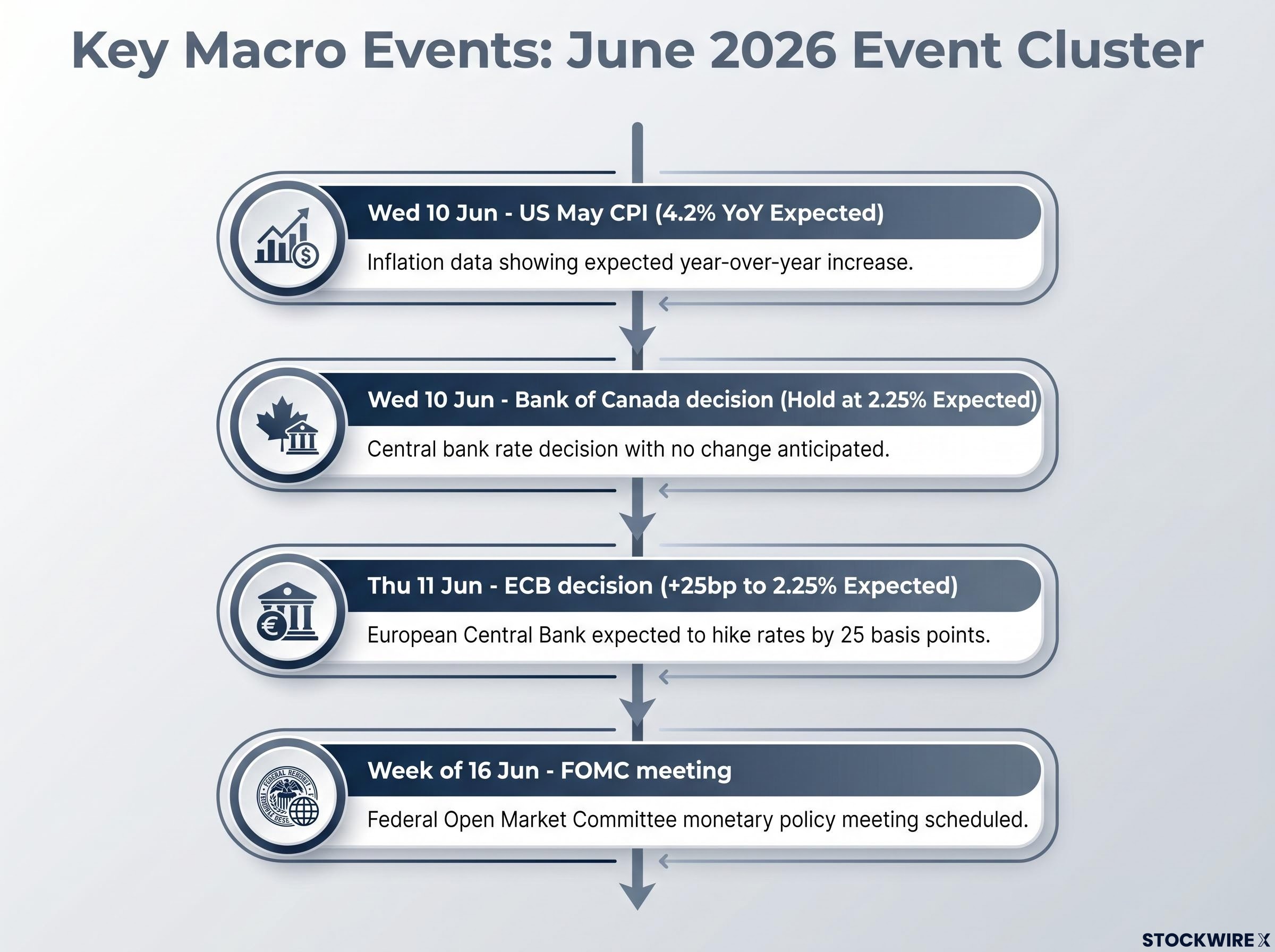

Three central bank decisions and a market-moving inflation print all land within 48 hours this week, making 10-11 June 2026 one of the most consequential two-day stretches for global macro investors in recent memory. The US May CPI release on Wednesday, followed by the Bank of Canada’s rate decision the same day and the European Central Bank meeting on Thursday, creates a tightly sequenced event cluster that will simultaneously test policy assumptions in three of the world’s largest economies. The FOMC meets the following week, meaning Wednesday’s inflation data will directly shape the stakes of that meeting.

What follows is a preview of what each decision is expected to deliver, what would constitute a genuine surprise, and how the outcomes interact across currencies, equities, and rate markets globally.

Why Wednesday’s US inflation print is the week’s most watched data release

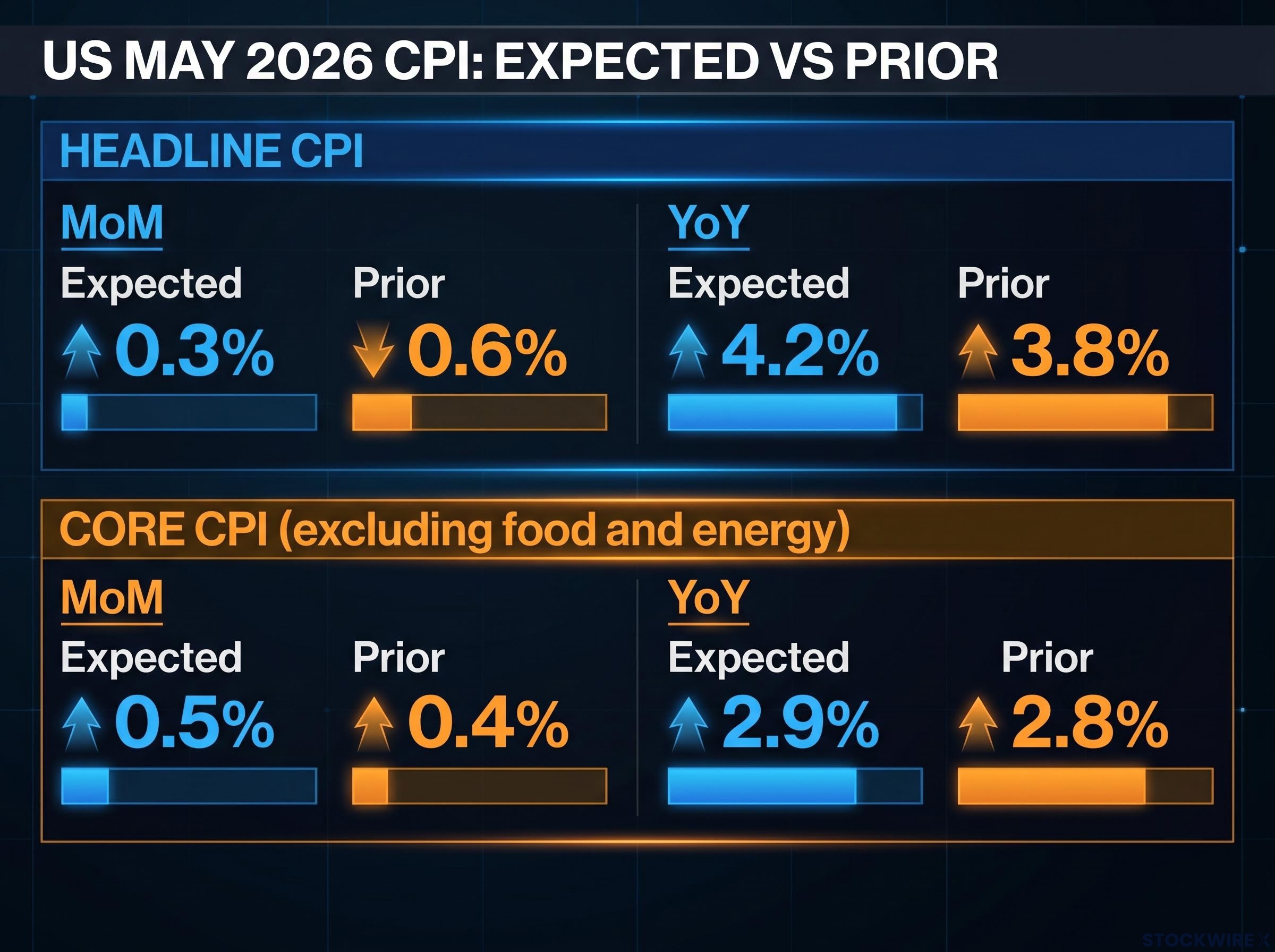

Consensus forecasts for the May 2026 CPI report point to a deceleration in the headline number but a stubborn uptick in core prices. Higher gasoline costs are expected to push the headline figure upward, while shelter and core goods may partially offset the increase.

The key forecasts, alongside their prior readings:

- Headline CPI: 0.3% month-on-month (prior: 0.6%) and 4.2% year-on-year (prior: 3.8%)

- Core CPI (excluding food and energy): 0.5% month-on-month (prior: 0.4%) and 2.9% year-on-year (prior: 2.8%)

The forecasts for May represent a continuation of a trajectory that began with the April CPI shock, when headline inflation printed at +0.6% monthly, double the consensus forecast, pushing the annual rate to 3.8% and eliminating near-term rate cut expectations in a single release.

Each core reading sits one-tenth of a percentage point above the prior figure. That single tenth matters enormously this week, because the FOMC meets the following week with a new chair making his inaugural call. A print that lands at or above forecast would feed directly into a rate-pricing environment that is already shifting.

The BLS Consumer Price Index release schedule confirms the May 2026 CPI data is published on Wednesday 10 June, placing it squarely before either the Bank of Canada or ECB speaks and giving it the first-mover advantage in resetting risk appetite for the entire event cluster.

Hotter-than-expected US inflation data could intensify equity selling pressure as money markets begin pricing in the possibility of more than one Federal Reserve rate increase by year-end 2026.

When big ASX news breaks, our subscribers know first

What the Federal Reserve’s new chair inherits at his first FOMC meeting

The policy bind facing the Fed exists independently of who occupies the chair. Over recent months, the six-month average of private sector payrolls has improved, leading some officials to question whether current interest rates are less restrictive than previously assumed. If the economy is absorbing rates more comfortably than models suggest, the case for further tightening strengthens regardless of the chair’s personal leanings.

The Fed’s internal inflation debate has been documented publicly through the April 28-29 FOMC minutes, which confirmed a unanimous hold framed explicitly as a data-collection pause rather than an end to the tightening cycle, with most committee members concluding that conditions remain far from the threshold required for rate cuts.

The added weight of an inaugural call

The new chair enters this environment with a dovish reputation. That reputation now collides with an internal debate that has shifted in a hawkish direction. Wednesday’s CPI print will determine just how wide the gap is between the chair’s perceived inclination and the data he has to work with.

A significant equity correction would complicate the calculus further, though it would not simplify it. Job losses at scale are what typically convert a slowdown into a contraction; a falling market alone does not change the inflation arithmetic. The new chair’s first meeting will test whether his dovish instincts can coexist with an institution that is already questioning its own restrictiveness.

The ECB’s June decision and why Lagarde’s words will matter more than the rate itself

The 25 basis point increase to the ECB deposit rate, bringing it to 2.25% at the Thursday, 11 June 2026 meeting, is widely expected and largely priced in. The rate number itself is unlikely to move markets.

The forward guidance is the variable that will.

| ECB Metric | Current / Expected | Market Implication |

|---|---|---|

| Deposit rate post-June meeting | 2.25% | Fully priced; limited reaction expected |

| Total tightening priced through September | 50bp+ | Any upward revision pressures euro rates |

| EUR/USD current level | Below 1.16 | Hawkish guidance could stabilise the pair |

| EUR/USD bearish target | Just above 1.14 (mid-March 2026 low) | Dovish surprise accelerates move lower |

Core inflation has exceeded ECB baseline projections, and several Governing Council members have adopted hawkish public stances ahead of the meeting. The ECB is framing this hike as an insurance measure against stagflation risk and Middle East-driven energy uncertainty. Updated staff economic projections and energy price shock scenarios, released alongside the decision, could shift market pricing independently of the rate move.

The guidance issued after the decision is where markets are likely to react most sharply, not the rate move itself. Any signal from President Lagarde about September tightening will determine whether EUR/USD holds above 1.14 or breaks lower.

Bank of Canada holds at 2.25%: what energy-driven inflation means for the pause

The Bank of Canada is expected to hold its benchmark rate at 2.25% on Wednesday, 10 June 2026. The decision itself carries the least surprise potential of the week’s three events, but the framing matters.

The Bank of Canada’s April 2026 policy hold statement explicitly cited the Middle East conflict, its effect on energy prices, and ongoing US trade policy uncertainty as the primary factors justifying an unchanged overnight rate at 2.25%, establishing the same framework the June decision is expected to follow.

Holding is not the same as easing. Three factors are keeping the BoC in place:

- Energy inflation persistence: Energy-driven price pressures are seen as potentially durable, keeping the central bank biased toward caution rather than rate cuts

- Soft economic data: Recent readings have weakened, arguing against tightening

- Trade and geopolitical uncertainty: Ongoing trade tensions and Middle East-linked risks collectively favour patience over action

The result is a neutral-to-hawkish bias that leaves the door open in both directions. The BoC is not signalling that its work is done; it is signalling that the balance of risks does not yet justify movement. For CAD positioning and for the broader question of whether North American central banks are moving in sync or diverging on inflation, the accompanying statement deserves close attention.

How the three decisions interact across currencies, equities, and rate markets

The three events are not independent. They are sequenced, and the order matters. Wednesday morning’s CPI print lands before either central bank speaks and immediately resets the week’s risk appetite.

The three events covered this week sit inside a larger central bank decision cluster that also includes the Bank of Japan and the Bank of England, both moving on 18 June, meaning the sequential risk-digestion window markets normally rely on between major policy announcements is compressed to an extent with no close modern precedent.

| Event | Date | Expected Outcome | Key Market Sensitivity |

|---|---|---|---|

| US May CPI | Wed 10 Jun | 4.2% YoY | Equities and Fed rate pricing |

| Bank of Canada decision | Wed 10 Jun | Hold at 2.25% | CAD and rate curve |

| ECB decision | Thu 11 Jun | +25bp to 2.25% | EUR/USD and euro rates |

| FOMC meeting | Week of 16 Jun | TBD | All risk assets |

If the CPI print overshoots, US dollar bulls already targeting the late March 2026 year-to-date high will have fresh momentum. That dollar strength compounds the pressure on EUR/USD, which is already below 1.16, and partially offsets any hawkish lift the ECB decision might provide to the euro.

Equities are the most sensitive cross-asset variable. The threshold to watch is whether money markets begin pricing more than one Fed rate hike by year-end 2026. If they do, the repricing could intensify equity selling pressure ahead of the FOMC meeting the following week, when the new chair has to convert this week’s data into an actual decision.

How to read a central bank week: what each institution is actually signalling

Three distinct communication layers are at work this week, and confusing them is the most common mistake retail investors make during a central bank cluster:

- The rate decision: The instrument itself. This is the headline number, and this week it is the least informative layer. The ECB’s 25bp hike is priced. The BoC’s hold is expected. The Fed has not yet met.

- The forward guidance and press conference tone: This is where markets react most sharply. Lagarde’s comments on September tightening, and the BoC’s characterisation of its pause as temporary or open-ended, will move currencies and rates more than the rate numbers.

- Updated projections and scenario analysis: The ECB’s staff economic projections and energy price shock scenarios function as a third communication layer that can shift market pricing independently. These projections reveal what the institution’s own models are telling policymakers, distinct from what the press conference chooses to emphasise.

The guidance issued after the decision is where markets are likely to react most sharply, not the rate move itself.

The BoC’s neutral-to-hawkish bias illustrates how a hold communicates a directional lean. The new Fed chair’s inaugural FOMC meeting illustrates how institutional credibility and personal reputation interact with formal policy tools. Neither of these dynamics is captured by the rate number alone.

When the dust settles, the FOMC meeting next week is where this week’s data will be tested

This week does not resolve the global policy picture. It calibrates it. The CPI print, the ECB’s forward guidance, and the BoC’s framing are three inputs that the new Fed chair will have to reconcile at the FOMC meeting scheduled for the week of 16 June 2026.

The range of plausible outcomes at that meeting is unusually wide. A dovish chair, a questioning internal debate on restrictiveness, and a potential equity correction create a decision environment where a hold, a hike, and a hawkish hold are all within reach depending on what this week delivers.

Three variables deserve close tracking in the days ahead:

- Magnitude of CPI deviation from forecast: A tenth of a percentage point above consensus on core CPI is where Fed rate pricing begins to shift materially

- Lagarde’s September guidance tone: Whether the ECB signals further tightening beyond 50bp or softens the path forward

- BoC language on energy inflation persistence: Any shift from “potentially persistent” to a firmer characterisation signals a change in the North American inflation consensus

Investors who track all three outcomes will be better positioned to anticipate the FOMC’s tone than those who focus on any single release in isolation.

Investors tracking the FOMC meeting the week of 16 June as the culmination of this week’s data will find our deep-dive into the Fed rate outlook reversal useful context, covering how markets shifted from pricing 50-75 basis points of cuts to a 65-70% probability of a hike in just ten weeks, alongside the institutional investor rotations now underway into value, financials, and floating-rate instruments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections and forward-looking statements referenced in this article are subject to market conditions and various risk factors.