Broadcom Miss Triggers Worst Semiconductor Crash Since 2020

10 hrs ago

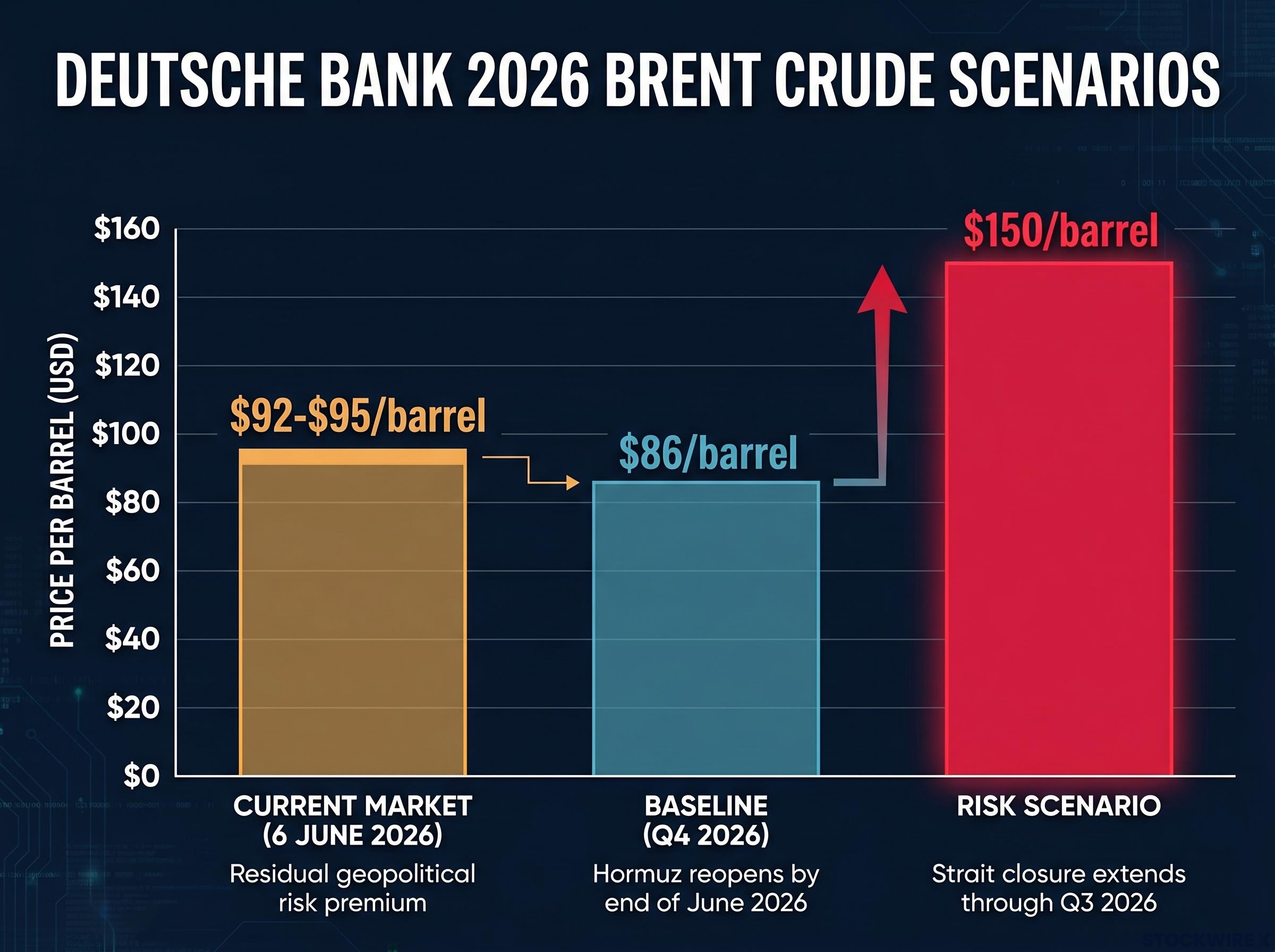

Deutsche Bank is warning that a single maritime chokepoint, the Strait of Hormuz, could push oil to $150 per barrel and tip Europe into recession. That scenario is not the base case, but the bank’s newly published World Outlook makes clear the margin between orderly recovery and severe disruption is measured in weeks, not months. Published 6 June 2026, the report by Jim Reid, Deutsche Bank’s Global Head of Macro and Thematic Research, identifies the US-Iran diplomatic track as the load-bearing assumption underneath every other 2026 macro forecast. With Brent crude already trading at $92-$95 per barrel, above the bank’s own Q4 baseline of $86, the gap between current prices and an oil price spike scenario is narrower than markets may appreciate. What follows is a breakdown of Deutsche Bank’s two oil price scenarios, the geopolitical timeline underpinning each, the specific consequences for European economies and European Central Bank (ECB) policy, and the historical framework Reid uses to contextualise 2026’s unusual collision of forces.

Deutsche Bank’s entire baseline scenario for 2026 rests on a single assumption: a US-Iran agreement concluded by the end of June 2026. Not a ceasefire in general terms, but a deal that specifically permits the resumption of commercial shipping through the Strait of Hormuz.

The most recent tangible milestone on that diplomatic track arrived in late May 2026, when US and Iranian negotiators reached a 60-day memorandum of understanding extending a ceasefire and launching further talks, according to Reuters, Axios, and the New York Times. President Trump and Iranian officials confirmed ongoing negotiations into early June 2026, with Iran reviewing a proposed agreement.

The key milestones on the diplomatic timeline:

The Strait of Hormuz is the narrow passage between the Persian Gulf and the Gulf of Oman through which a substantial share of the world’s seaborne oil exports transit. Deutsche Bank’s baseline is not merely tied to diplomatic progress; it is explicitly contingent on Hormuz shipping resumption. Without that physical reopening, the price moderation the bank projects cannot materialise.

Under the baseline, Brent crude eases to $86 per barrel by Q4 2026. The condition is straightforward: the Strait of Hormuz reopens, supply normalises, and the geopolitical risk premium drains from the market.

Under the risk scenario, that does not happen. A sustained Strait closure extending through Q3 2026 pushes crude toward $150 per barrel, according to Reid’s World Outlook.

| Scenario | Brent Crude Price (Q4 2026) | Key Condition |

|---|---|---|

| Baseline | $86/barrel | Hormuz reopens by end of June 2026 |

| Risk Scenario | $150/barrel | Strait closure extends through Q3 2026 |

| Current Market (6 June 2026) | $92-$95/barrel | Residual geopolitical risk premium |

The fact that Brent is currently trading above the bank’s own Q4 baseline signals that markets are already pricing in residual risk. The gap between $95 and $150 is the premium traders would need to absorb if the diplomatic track collapses.

The Hormuz risk premium is unlikely to decompress rapidly even if a diplomatic deal is reached, because the IEA projects a two-year supply chain recovery timeline under a best-case resolution and the near-total withdrawal of commercial war-risk insurance has structurally altered the economics of tanker operations through the strait.

Deutsche Bank’s Jim Reid identifies crude oil surging toward $150 per barrel as the explicit named downside scenario if a sustained Strait of Hormuz closure extends through Q3 2026.

The Strait of Hormuz is the world’s most consequential oil chokepoint, a narrow maritime corridor carrying a substantial proportion of global seaborne crude exports. A closure does not destroy supply. It reroutes it at significant cost and delay, creating acute short-term shortage dynamics where buyers bid up prices for immediate delivery.

This mechanism produces non-linear price responses rather than gradual adjustments:

EIA data on Hormuz oil transit confirms that the strait accounted for approximately 20% of global petroleum liquids consumption and one quarter of total global maritime traded oil in the first half of 2025, figures that explain why even a partial closure produces price effects far exceeding the volume of supply physically removed from the market.

Reid’s invocation of the 1990 parallel is not decorative. It serves as a documented historical case where a geographically concentrated supply disruption produced price effects far exceeding the volume of oil physically removed from the market.

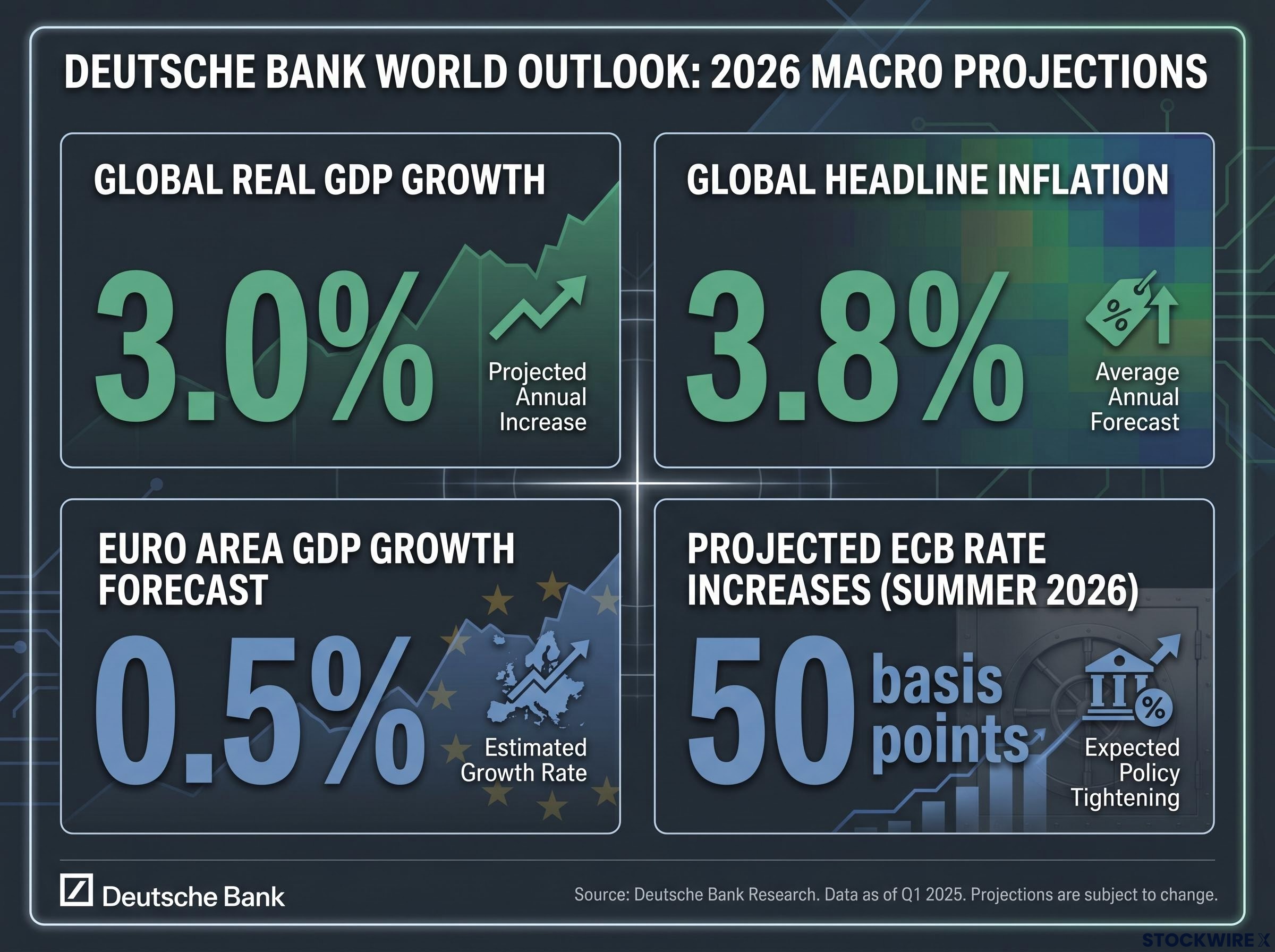

Europe was already fragile before the Strait became a variable. Deutsche Bank’s World Outlook cut its euro area GDP growth forecast for 2026 to 0.5%, with the energy price shock identified as the primary driver of that deterioration.

Eurozone services contraction was confirmed in May 2026 PMI data, with the composite reading falling to a 31-month low of 47.5 and a 4.5-point gap opening between US and eurozone services PMI, a divergence that illustrates how the same oil shock is landing asymmetrically across the Atlantic and complicating any coordinated global policy response.

At 0.5%, the euro area is operating with almost no buffer against contraction. A single quarter of negative output would constitute a technical recession.

Under the adverse Hormuz closure scenario, Deutsche Bank projects European economies would tip from this near-recessionary baseline into outright recession.

Three factors make Europe disproportionately exposed:

Here is the counterintuitive consequence of the energy shock: the ECB is projected to raise rates even as Europe flirts with recession. Deutsche Bank forecasts 50 basis points of ECB interest rate increases during summer 2026.

The rate path is not driven by economic strength. It is a forced response to imported inflation.

Cost-push inflation mechanics operate differently from the demand-driven variety that central banks are designed to cool: rising energy input costs flow through to consumer prices regardless of whether households are spending more, which is precisely why the ECB faces the uncomfortable task of tightening into a weakening economy.

The distinction matters for investors holding eurozone rate-sensitive assets:

The mechanism is cost-push inflation, not demand-pull. Rising energy input costs flow through to consumer prices regardless of whether households are spending more. Deutsche Bank revised global headline inflation for 2026 to 3.8%, and Reid observed that elevated nominal GDP figures are being driven paradoxically by the inflationary pressures themselves, creating a distorted growth picture that complicates central bank signalling.

Deutsche Bank’s World Outlook highlights two distinct forces operating simultaneously in 2026: a sustained AI-driven investment cycle producing technology sector optimism and equity market momentum, alongside a geographically concentrated Middle East supply disruption generating energy-driven inflation and recessionary pressure on import-dependent economies.

The distinctive feature of 2026 is not that either force is present. It is that both are operating at significant scale simultaneously:

Jim Reid frames 2026 as a simultaneous collision of late-1990s technology optimism and 1990-era Gulf War supply shock dynamics, a combination without a clean historical precedent.

Against this backdrop, Deutsche Bank projects global real GDP growth of 3.0% alongside global headline inflation of 3.8% for 2026. The numbers themselves tell the dual-force story: growth sustained by AI-driven momentum, inflation elevated by the energy shock. Neither force cancels the other; both persist.

Structural buffers supporting global GDP, including IT investment at a record 4.9% of GDP in Q1 2026, have prevented current output data from fully reflecting the Hormuz disruption, partly because the transmission lag from an oil shock to reported GDP figures runs approximately four quarters, meaning June’s diplomatic outcome will shape data that does not appear in official releases until well into 2027.

Deutsche Bank’s entire 2026 baseline, from $86 oil to a 0.5% euro area growth floor to the ECB’s projected rate path, rests on a US-Iran agreement by the end of June 2026. If June passes without a deal, the $150 oil and European recession scenario moves from risk case to baseline for the second half of the year.

Three things to monitor as the deadline approaches:

The Strait of Hormuz is not only an energy story. It is the structural fault line underneath Deutsche Bank’s entire 2026 global outlook, the single variable from which oil prices, European growth, ECB policy, and global inflation projections all cascade.

What remains unresolved is whether the June diplomatic window delivers a deal, whether the late May memorandum of understanding holds, and whether energy-driven inflation has already embedded itself deeply enough to persist regardless of the outcome. The answers will arrive within weeks, not quarters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking scenarios are subject to change based on diplomatic developments and market conditions.

The Strait of Hormuz is a narrow maritime corridor connecting the Persian Gulf to open ocean, through which a substantial share of global seaborne crude exports transit. A closure does not destroy supply but reroutes it at significant cost and delay, creating acute short-term shortage dynamics that drive non-linear oil price spikes.

Deutsche Bank's risk scenario projects Brent crude rising to $150 per barrel if the Strait of Hormuz remains closed through Q3 2026, compared to a baseline forecast of $86 per barrel by Q4 2026 if a US-Iran deal allows Hormuz shipping to resume by end of June 2026.

Europe is disproportionately exposed because the euro area relies heavily on imported energy, its baseline GDP growth is already a fragile 0.5%, and a Hormuz-related price shock transmits directly into consumer prices, leaving almost no buffer before a single quarter of negative output triggers a technical recession.

Deutsche Bank forecasts 50 basis points of ECB rate increases during summer 2026 driven not by strong economic growth but by imported cost-push inflation, meaning the central bank is forced to tighten into a weakening economy, creating an uncomfortable and uncertain policy environment.

Deutsche Bank's entire 2026 baseline assumes a US-Iran agreement permitting Hormuz shipping resumption by the end of June 2026, with the late May 2026 memorandum of understanding providing the most recent tangible progress on that track. If June passes without a deal, the $150 oil and European recession scenario moves from risk case to base case for the second half of the year.