Nvidia just cut its pool of Asia-based authorised AI chip buyers by more than half in a single regulatory sweep, and its shares dropped 3.52% to $203.53 on 14 July 2026, on trading volume of roughly 121 million shares. That combination of compliance action and market reaction tells you this is not a routine disclosure.

U.S. technology export controls have been tightening steadily, with the central aim of blocking advanced AI hardware from arriving at restricted end-users in China via third-country routing through transshipment and data-centre hubs such as Singapore, Malaysia, and Japan. Nvidia is not retreating from Asia. It is restructuring who it can legally sell to, and how fast it can approve new buyers will determine whether this is a one-quarter speed bump or something that reshapes its Asia-Pacific revenue mix for longer.

Here is the framework you need to read Nvidia’s next earnings call with fresh eyes: what the approved-buyer registry actually does, why these three specific markets attracted regulatory scrutiny, and what the friction-versus-structural-loss distinction means if you hold or are watching NVDA and broader AI chip stocks.

Nvidia’s buyer registry cut: what just happened and how big it is

Citing the Financial Times, reports indicate that Nvidia has slashed its eligible Asian AI chip buyer list by over half, with tightened compliance procedures now in force across Singapore, Malaysia, and Japan. The stock fell 3.52% on the news.

Market reaction: NVDA closed at $203.53 on 14 July 2026, down 3.52%, on trading volume of approximately 121.41 million shares.

The scale sounds severe, but the mechanism matters more than the headline figure. Buyers who have been removed from the approved list are able to seek reinstatement by fulfilling the revised compliance requirements. This is a registry tightening, not a blanket market exit or a product withdrawal.

The three affected markets and the nature of the compliance change in each:

- Singapore: Enhanced buyer pre-screening and documentation requirements for AI accelerator purchases routed through the city-state’s distribution channels.

- Malaysia: Updated end-use verification procedures targeting data-centre infrastructure buyers.

- Japan: Strengthened named-buyer approval processes for distributors handling higher-end AI chips.

The bottleneck driving this is the pace of approvals and documentation, not the absence of end demand. That distinction is worth sitting with: the “more than half” figure sounds like a demand collapse, but the reapplication pathway means the question investors should be asking is how long requalification takes before treating this as permanent lost revenue.

When big ASX news breaks, our subscribers know first

How an approved-buyer registry actually works

Nvidia must now pre-screen and log buyers before shipping higher-end AI accelerators, creating an auditable compliance layer. An approved-buyer registry is a system in which only named buyers and distributors can purchase specific chips, with oversight on volumes and use-case compliance. Think of it as a whitelist: if your name is not on it, the chips do not ship.

The registry fits within broader U.S. licensing arrangements that require buyers to demonstrate three things: sufficient security procedures, confirmed non-military end use, and full traceability of where the chips end up. Nvidia has publicly framed this as a proactive compliance posture, trading short-term sales convenience for long-term licence stability and reputational safety with U.S. regulators.

BIS end-use verification requirements establish the compliance baseline that exporters such as Nvidia must satisfy, including physical security assessments and Infrastructure as a Service restrictions designed to prevent unauthorised downstream access to restricted chips.

Understanding the registry as an auditable compliance architecture, rather than a quota or a ban, is the lens that determines whether you see this quarter’s revenue miss as a timing issue or a demand impairment. Most coverage treats export control actions as binary: blocked or not blocked. The registry model introduces a third state, pending requalification, which has a specific revenue recognition timeline that investors must factor into their models.

Where the requalification delay hits revenue timing

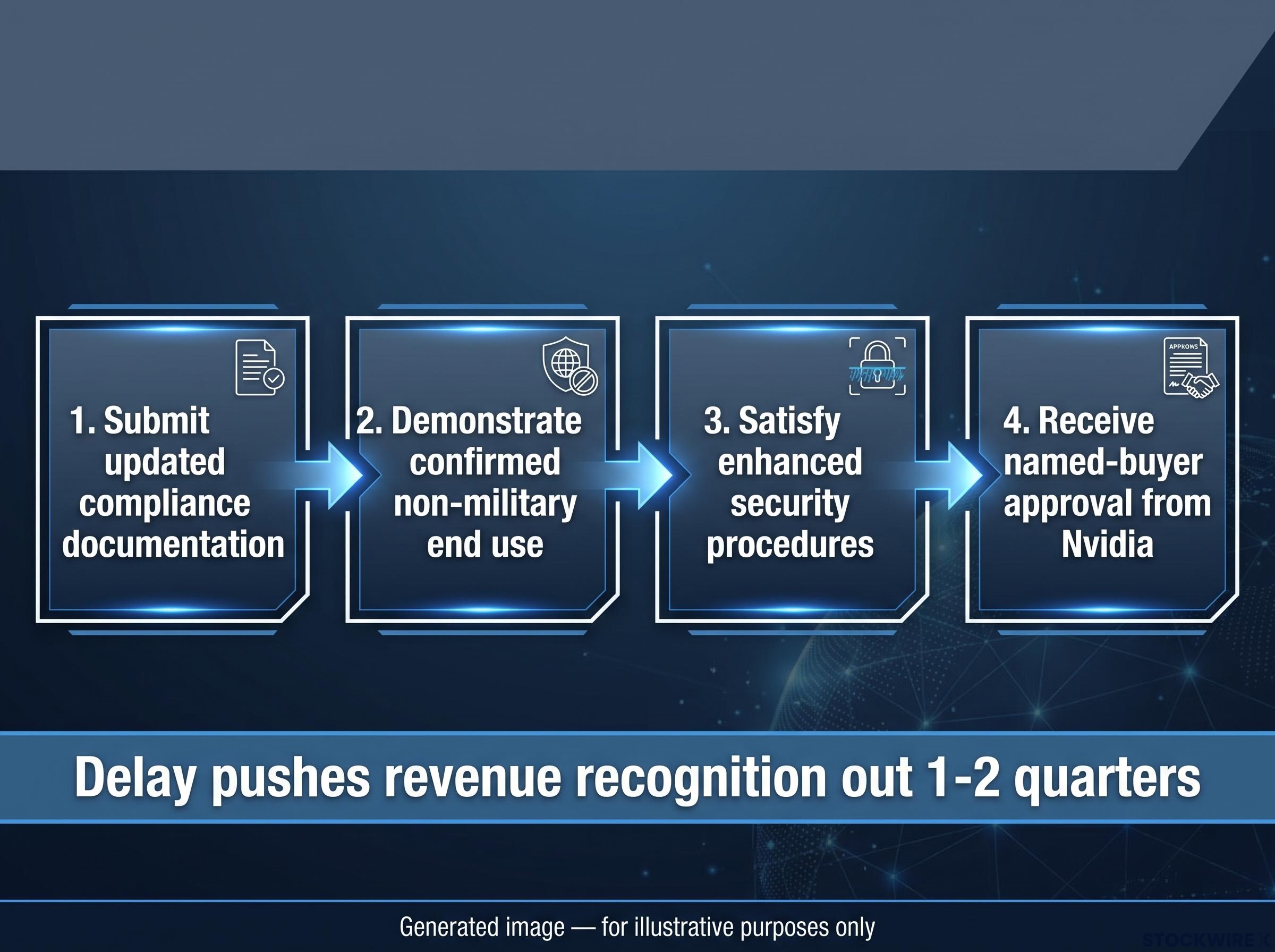

A removed buyer must complete four sequential steps to regain access:

- Submit updated compliance documentation

- Demonstrate confirmed non-military end use

- Satisfy enhanced security procedures

- Receive named-buyer approval from Nvidia under the new registry framework

The delay occurs between removal and reinstatement. This gap can push revenue recognition out by one to two quarters without eliminating the underlying order. The pace of Bureau of Industry and Security (BIS) approvals, not customer willingness to reapply, is the primary variable controlling how long this gap lasts. The H20 chip’s regulatory history illustrates how quickly the rules themselves can shift: what was a compliant product in one period became effectively restricted within 12-18 months.

Why Singapore, Malaysia, and Japan became the focus of regulatory scrutiny

The instinctive read is that these are markets of concern in themselves. They are not. Singapore, Malaysia, and Japan are important transshipment and data-centre hubs whose routing roles, not their domestic end-markets, placed them under regulatory scrutiny as potential back-door channels for restricted chips to reach China.

| Market | Primary role | Regulatory exposure |

|---|---|---|

| Singapore | Transshipment hub and distribution centre | Routing risk for restricted chips via regional distribution channels |

| Malaysia | Data-centre hub | End-use verification gaps in fast-growing AI infrastructure buildout |

| Japan | Both transshipment and data-centre hub | Distributor-level circumvention concerns for higher-end accelerators |

U.S. policy has progressed from country-level bans to performance-threshold controls to detailed licensing regimes targeting third-country circumvention routes. That progression is not slowing down.

The registry tightening sits within a broader regulatory progression: the U.S. Commerce Department closed the third-country subsidiary loophole in May 2026, requiring export licences for any Chinese-headquartered entity purchasing advanced AI chips regardless of where that entity physically operates, directly targeting the Malaysia and Singapore routing channels that made the current registry action necessary.

The H20 case documents a 12-18 month policy change cycle in which a compliant chip became effectively restricted. That pace quantifies how quickly compliance risk can materialise for investors in any semiconductor name with Asia-Pacific distribution through these hubs.

If you hold any semiconductor stock with significant Asia-Pacific distribution through these three markets, the third-country circumvention logic means your exposure to future tightening rounds is higher than a simple China-revenue percentage would suggest. These are not one-off targets. They are structurally recurring ones.

Friction or structural loss: the revenue question that matters most for investors

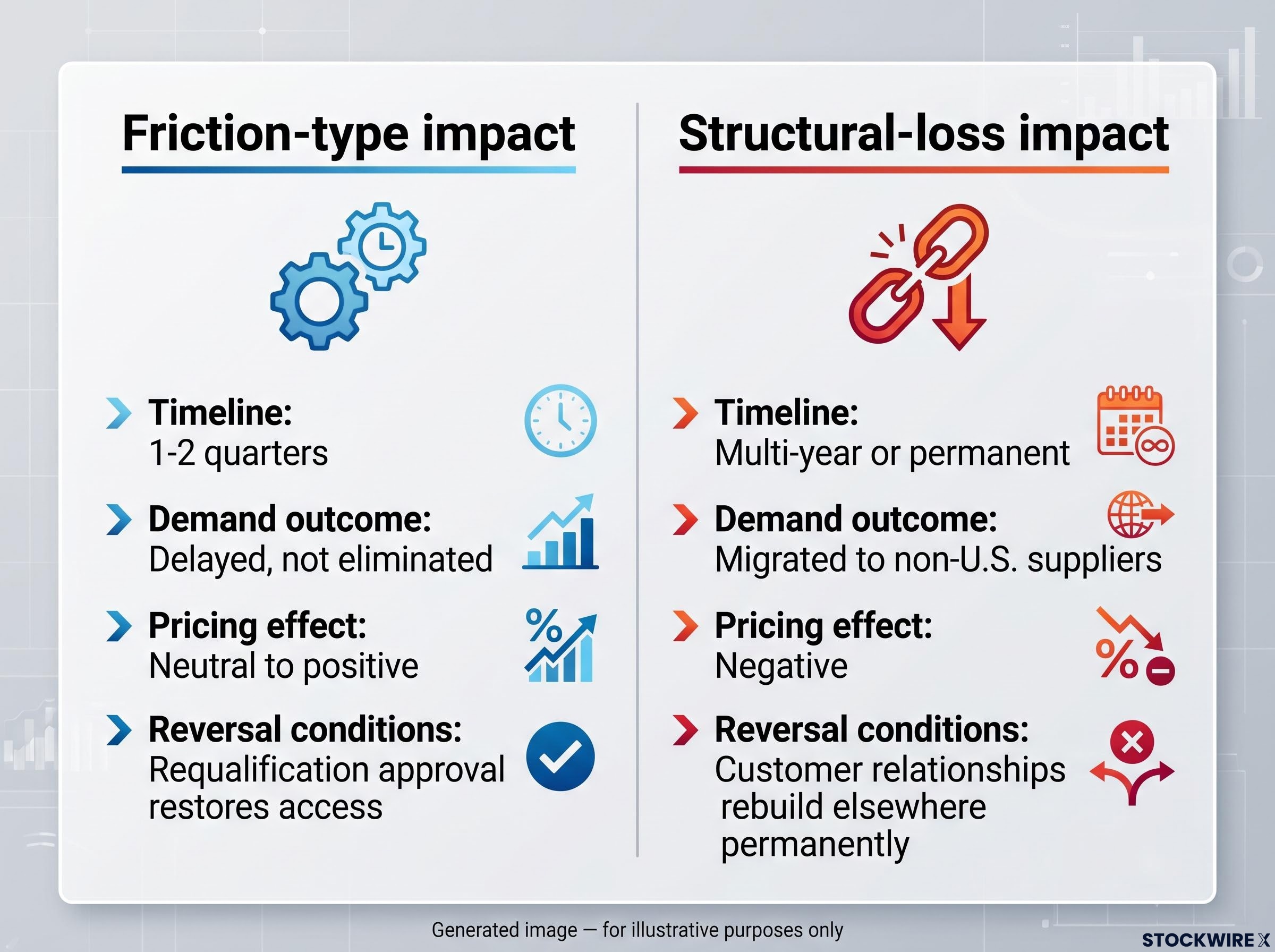

Two types of impact are in play, and conflating them produces the wrong positioning. The distinction is clean:

| Dimension | Friction-type impact | Structural-loss impact |

|---|---|---|

| Timeline | 1-2 quarters | Multi-year or permanent |

| Demand outcome | Delayed, not eliminated | Migrated to non-U.S. suppliers |

| Pricing effect | Neutral to positive (scarcity supports pricing) | Negative (lost volume weakens leverage) |

| Reversal conditions | Requalification approval restores access | Customer relationships rebuild elsewhere permanently |

The current registry action skews toward temporary friction for most affected customers, because reapplication remains open. But the condition that tips it toward structural loss is specific: slow approvals that give non-U.S. or domestic alternatives, particularly state-backed chip development programmes in China, enough time to establish customer relationships that do not revert.

H20 and H200 approval dynamics illustrate the dual-approval problem that compounds the registry friction: even where U.S. clearances exist, Beijing has withheld its own required approvals for H200 shipments to roughly 10 cleared Chinese firms, meaning the requalification timeline investors must model is subject to regulatory delays on both sides of the trade.

Why buyer tier matters: hyperscalers versus regional distributors

Well-resourced hyperscalers with established compliance teams and existing licensing relationships can navigate requalification faster than smaller regional distributors, which face proportionally higher friction and longer timelines.

This bifurcation concentrates the revenue risk in mid-tier and smaller channel partners, not in Nvidia’s highest-value accounts. Whether you treat this quarter’s expected revenue miss as a buying opportunity or a warning signal depends on which side of the friction-versus-structural-loss line the registry action ultimately lands. The approval timeline over the next 60-90 days is the key observable.

The next major ASX story will hit our subscribers first

What this signals for the broader semiconductor and AI chip sector

Nvidia’s registry approach is not an isolated compliance exercise. It is a practical template that AMD and other advanced accelerator vendors will be required to replicate, since performance-based controls and regional restrictions apply across the industry. Any firm selling near-frontier AI chips into sensitive regions now needs comparable end-user verification and auditable buyer lists.

The indirect exposure runs further. If compliance bottlenecks slow AI chip deployment in Asia, that feeds back into data-centre capex plans and, with a lag, into leading-edge fabrication demand. Companies such as ASML and major semiconductor equipment makers face this second-order pressure.

Custom silicon competitive pressure from Alphabet, Amazon, and Microsoft is most acute in inference workloads, the same segment that Asia-Pacific data-centre buyers are primarily deploying, meaning the registry friction arrives at a moment when Nvidia’s hold on incremental AI accelerator demand in the region is already being contested from two directions simultaneously.

Categories of companies with direct versus indirect export control exposure:

- AI chip designers (Nvidia, AMD): Direct exposure through buyer registries and licensing requirements.

- Foundries and semiconductor equipment makers (ASML, leading foundries): Indirect, lagged exposure through capex feedback loops.

- Cloud providers and hyperscalers: Mixed exposure depending on regional allocation and compliance standing.

Export controls are reshaping which suppliers and which channels capture global AI chip demand. They are not suppressing aggregate demand. The total addressable market is not shrinking; supply chain routes and buyer relationships are being restructured around compliance architecture.

Any semiconductor position with meaningful Asia-Pacific AI chip revenue exposure now carries an embedded compliance execution risk. That risk should be explicitly modelled in your valuation work, not treated as a generic geopolitical macro factor. Companies that build approved-buyer infrastructure earlier will have lower friction costs in future tightening rounds.

Three variables to watch before Nvidia’s next earnings call

The “more than half” buyer cut is a backward-looking data point. The forward-looking earnings signal lives in three specific observables, ranked by immediacy:

- Requalification approval rate and timeline. The pace of reinstatement under the new registry determines whether this is a one-quarter event or a multi-quarter drag. This is the single most important variable, and early data points could emerge within 60-90 days.

- Nvidia’s Asia-Pacific channel commentary on the next earnings call. Listen specifically for language on book-to-bill ratios or order pipeline health in Singapore, Malaysia, and Japan. Silence on these markets would itself be a signal.

- BIS guidance updates on third-country routing rules. A further tightening of circumvention rules could expand the registry cut beyond the current three markets. The 12-18 month policy change cycle means investors should not assume current registry parameters are stable.

Investors who anchor on the current buyer-cut figure as a fixed data point are looking backward. These three variables are where the friction-versus-structural-loss question gets answered in real time, and tracking them gives you a material informational edge heading into Nvidia’s next earnings release.

For investors wanting to contextualise the registry-driven revenue risk against Nvidia’s current financial position, our full explainer on Nvidia’s Q1 FY2027 earnings baseline covers the $81.6 billion revenue record, $91 billion Q2 guide, and $80 billion buyback that define the scale from which any Asia-Pacific friction would be measured.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding requalification timelines, regulatory developments, and revenue impacts are speculative and subject to change based on market developments and company performance.