Lenovo shares hit an all-time high on 26 May 2026 after the company reported a quarterly net profit figure that redrew the investment case overnight: a 479% year-on-year surge to US$521 million. The result, delivered on quarterly revenue of US$21.6 billion, caps two consecutive sessions of record-breaking price action and repositions a company best known as the world’s largest PC maker as a direct beneficiary of enterprise AI infrastructure spending. The earnings print arrives as global investors scan the AI hardware supply chain for equity exposure beyond the concentrated Nvidia trade. What follows breaks down what drove the numbers, what the Infrastructure Solutions Group (ISG) result signals for the broader AI server market, and what the dual tailwinds of AI demand and a recovering PC market mean for investors tracking this stock.

Lenovo shares reach all-time high across two consecutive sessions

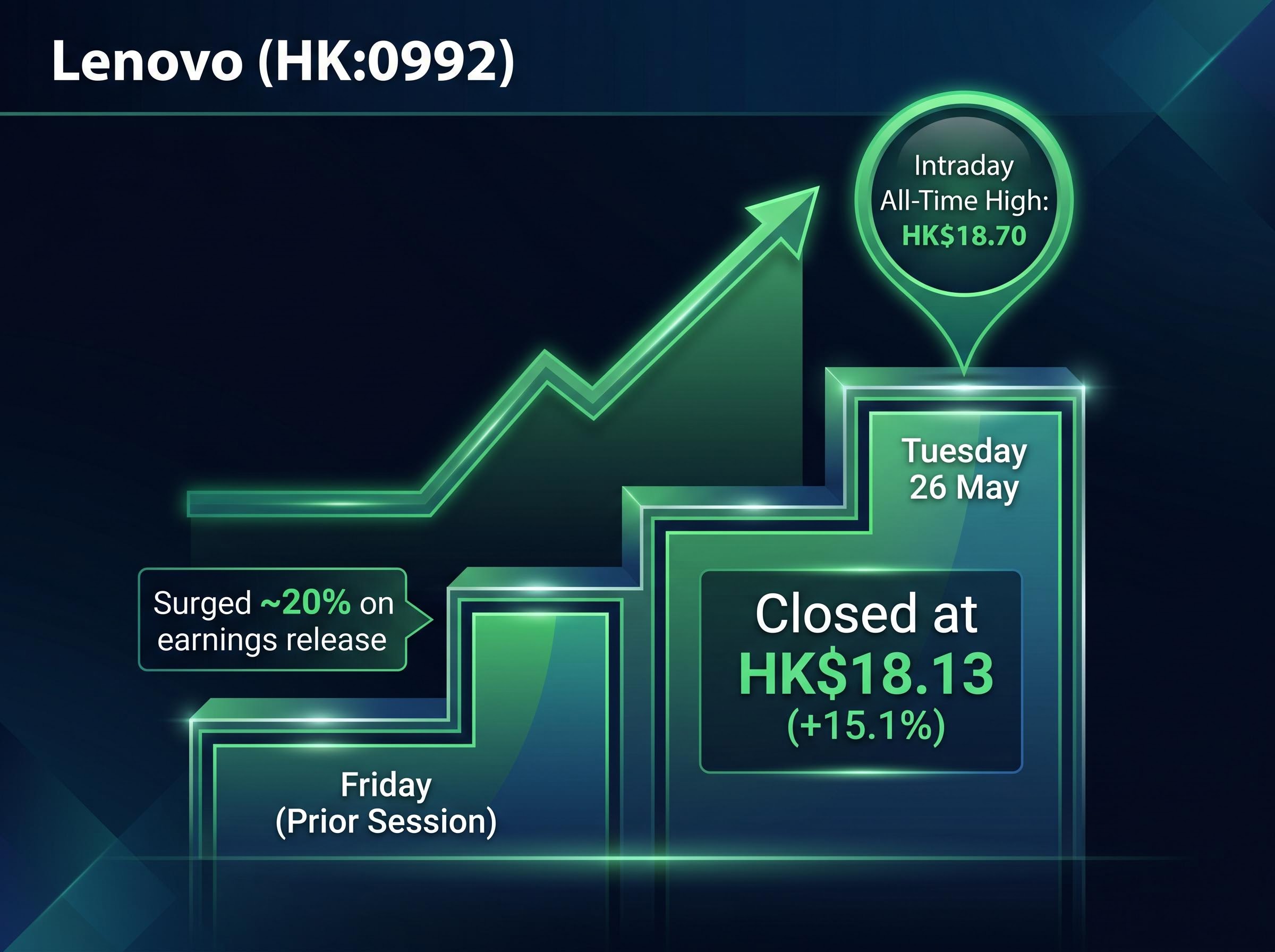

The two-session sequence that carried Lenovo (HK:0992) to a verified all-time high was not a single spike. It was a staggered repricing that suggests the market needed time to absorb the scale of the earnings beat.

- Friday (prior session): Shares surged approximately 20% on the initial release of quarterly results

- Tuesday 26 May: Shares reached an intraday peak of HK$18.70, before closing at HK$18.13, a further 15.1% single-session gain

All-time intraday high: HK$18.70, recorded on 26 May 2026

The pattern is worth noting. A single-day earnings pop followed by a second leg higher on the next trading session often reflects institutional accumulation rather than a purely retail-driven reaction. The first session prices the headline; the second session prices the positioning change.

Lenovo’s two-session re-rating is consistent with a broader AI hardware performance divergence that has opened a record 133-percentage-point spread between the top and bottom deciles of technology stock returns in 2026, with storage and server assembly companies leading a surge fuelled by the same hyperscaler capex commitments driving ISG’s order book.

For investors unfamiliar with the stock, Lenovo is Hong Kong-listed and trades under ticker HK:0992. The combined two-session return represents the defining price event for the stock in 2026 to date.

When big ASX news breaks, our subscribers know first

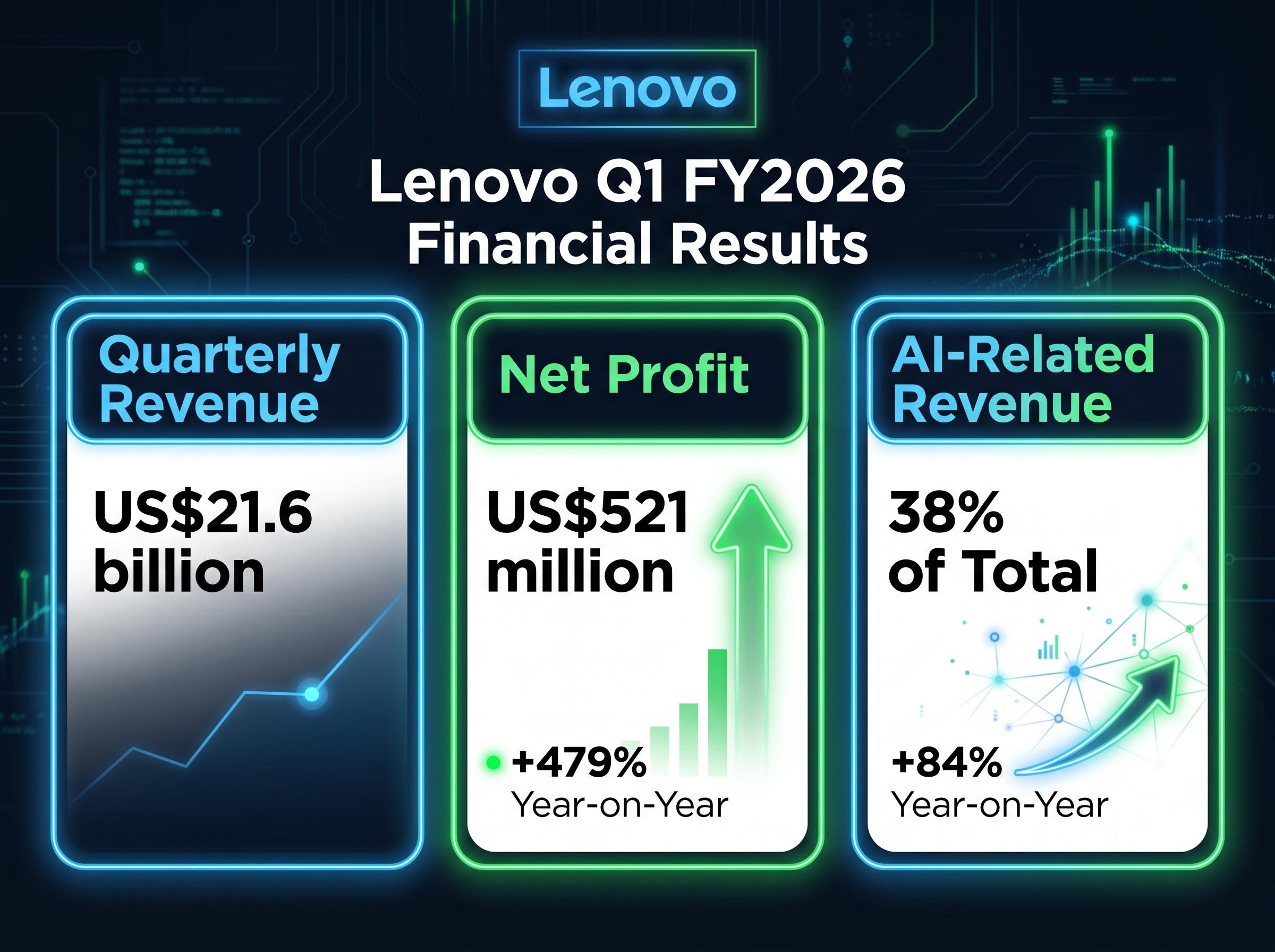

The headline numbers: quarterly revenue, net profit, and what 479% actually means

The headline figure commands attention. US$521 million in net profit for the March 2026 quarter (Q1 FY2026), up 479% year-on-year, is the kind of growth rate that stops portfolio managers mid-scroll.

| Metric | Q1 FY2026 Figure | Year-on-Year Change |

|---|---|---|

| Revenue | US$21.6 billion | Strong growth (multi-segment) |

| Net Profit | US$521 million | +479% |

The revenue figure is structurally credible for a company of Lenovo’s scale. As the world’s largest PC manufacturer, the group already operated at a revenue run-rate measured in tens of billions. The profit growth, however, demands context.

A 479% year-on-year increase reflects both genuine operational improvement and a compressed prior-year base. Investors interpreting the figure should weigh what the year-ago quarter’s profit looked like before extrapolating the growth rate forward. Both over-extrapolating (assuming this rate persists) and dismissing it (treating it as a statistical anomaly) carry portfolio risk. The figure sits somewhere between: real margin expansion driven by ISG’s profitability inflection and the mathematical leverage that a depressed base period provides.

What is Lenovo’s Infrastructure Solutions Group and why is it the company’s fastest-growing division?

Lenovo is three businesses under one roof. Most investors know the PC and smartphone operation. Fewer have tracked the Infrastructure Solutions Group, the division building AI servers and data centre equipment, and it is ISG that explains the earnings inflection.

ISG designs, manufactures, and distributes server hardware for cloud service providers and enterprise customers. It is distinct from the legacy consumer hardware business in both its customer base and its margin profile. The division’s stated differentiators include:

- Neptune liquid cooling technology, which addresses the thermal management challenge that high-density AI server racks present to data centre operators

- Hybrid AI Advantage framework, combining hybrid infrastructure, a model factory, and an agent platform to position Lenovo as an end-to-end AI infrastructure provider

- A dual demand base spanning cloud service providers on one side and enterprise and small-to-medium business (SMB) customers on the other

ISG revenue grew 37% year-on-year for the March 2026 quarter. But the growth rate alone understates the significance of the result.

From breakeven to profit engine: ISG’s financial inflection point

According to Lenovo’s 2024/25 Annual Report, ISG achieved breakeven in the second half of FY2024/25 and has since been described by management as turning into a sustainably profitable business. Chairman and CEO Yang Yuanqing cited strong growth in both the cloud service provider segment and the enterprise/SMB segment as the dual demand pillars driving the transition.

This shift from a loss-making growth bet to a profitable division is the structural story beneath the headline profit surge. It changes how the market should model Lenovo’s earnings quality. A division that was diluting group margins a year ago is now contributing to them. That is a qualitative inflection, not just a quantitative one.

Lenovo’s PC and consumer hardware segment: AI tailwinds meet memory chip supply pressure

The ISG story captured the headlines, but the consumer hardware segment provided its own contribution to the quarterly beat. Sustained demand for PCs, tablets, and smartphones reinforced the revenue result alongside infrastructure sales.

Two distinct forces are driving this segment, and they carry different implications:

- Structural market share gains: Lenovo holds leadership as the world’s largest PC maker, and its position in the consumer hardware market has strengthened through the period, contributing revenue growth that reflects competitive positioning rather than cyclical recovery alone

- Cyclical pull-forward purchasing: Consumers and enterprises appear to be accelerating hardware purchases ahead of anticipated memory chip price increases tied to supply shortages, providing a demand tailwind with a potential expiry date

The memory chip dynamic is a double-edged signal: it validates current demand strength but also raises the question of whether some revenue has been borrowed from future quarters.

The memory shortage expected to persist through late 2027 is not isolated to Lenovo’s supply chain: Apple’s Q2 2026 result flagged the same dynamic as a risk to its own device cycle, with consumers and enterprises front-loading hardware purchases ahead of anticipated component cost increases, a pattern that implies the pull-forward demand Lenovo is currently benefiting from is a sector-wide phenomenon rather than a company-specific tailwind.

This distinction matters for investors modelling the next two to three periods. If a meaningful share of PC-segment demand reflects purchases pulled forward to beat rising component costs, the revenue tailwind may fade once supply normalises or buyers complete their accelerated refresh cycles. The structural share gains, by contrast, are more durable. Separating the two is the analytical task the headline numbers do not perform on their own.

What Lenovo’s results signal for the AI hardware supply chain

Lenovo’s ISG performance is more than a single-stock story. It is a data point about the state of enterprise AI infrastructure spending globally.

According to Lenovo corporate disclosures, AI-related revenue grew 84% year-on-year to account for 38% of total group revenue in a recent quarter. That concentration tells a clear story: AI infrastructure is no longer a niche vertical for this company. It is approaching parity with the legacy business as a revenue driver.

Investors who have tracked the AI infrastructure buildout through Nvidia, Dell Technologies, Hewlett Packard Enterprise (HPE), and Super Micro Computer now have a corroborating data point from a different layer of the supply chain. Lenovo sits downstream of chip designers and upstream of enterprise end-customers, making its order book a signal of capex commitments flowing through the system.

Where Lenovo sits in the AI hardware supply chain

| Supply Chain Layer | Key Players | Lenovo’s Role |

|---|---|---|

| Chip Design & Supply | Nvidia, AMD | Customer (procures GPUs and accelerators) |

| Server Assembly & Distribution | Lenovo, Dell, HPE, Super Micro | Global-scale assembler with direct enterprise relationships |

| End Customers | Cloud providers, enterprise, SMB | Sells directly to both cloud and enterprise/SMB segments |

For investors who cannot or prefer not to access Nvidia directly, Lenovo’s results offer an alternative exposure point to the same AI capex cycle at a different valuation and risk profile. The 38% AI revenue concentration also suggests that any slowdown in enterprise AI spending would register in Lenovo’s results faster than it would have two years ago, when the division was smaller and loss-making.

Asian hardware assemblers and memory manufacturers occupy a structurally distinct position in the AI hardware supply chain from the US chip designers they source from: Samsung and SK Hynix, for instance, trade at roughly half the forward P/E of Nasdaq 100 peers despite earnings growth forecasts running nearly three times faster, a valuation asymmetry that frames why Lenovo’s own rerating may not yet be complete.

The next major ASX story will hit our subscribers first

The outlook from here: what investors should watch in the quarters ahead

Earnings beats create short-term price reactions. Sustaining a position through the quarters ahead requires understanding what variables will determine whether this result marks the beginning of a trend or a peak.

Yang Yuanqing’s qualitative forward commentary, drawn from Lenovo’s most recent annual report and corporate disclosures, frames continued AI infrastructure investment and multi-year AI PC and AI server demand as strategic priorities. Management has not provided specific numeric next-quarter targets. The guidance is directional, not granular.

Yang Yuanqing has described ISG as a “sustainably profitable” business, signalling management’s confidence that the division’s breakeven-to-profit transition is structural rather than temporary.

Three variables deserve investor attention in the coming quarters:

- ISG margin trajectory: Breakeven has been achieved. The question now is whether profitability deepens as AI server volumes scale, or whether competitive pricing pressure caps margins at current levels.

- Memory chip supply normalisation: When the supply shortage eases, the pull-forward demand tailwind in the PC segment may reverse. Timing this shift is the key risk to near-term consumer hardware revenue.

- AI server order cadence: The pace at which cloud service providers and enterprise customers convert pipeline interest into committed orders will determine whether ISG’s 37% growth rate is sustainable or decelerating.

A Lenovo corporate release also noted record group revenue of US$22.2 billion, up 18% year-on-year, in a recent fiscal quarter, reinforcing the multi-segment growth trajectory, though the precise quarter designation for that figure warrants confirmation against formal filings.

For readers wanting to model the market Lenovo’s ISG is growing into, our dedicated guide to the server CPU market forecast details Citi’s projection of a $29.3 billion to $131.5 billion expansion by 2030, including a newly defined agentic CPU segment growing at a 185% CAGR that would make server assembly at Lenovo’s scale a direct beneficiary of the fastest-growing data centre procurement category.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Lenovo’s record quarter reframes the company’s identity for investors

The story beneath the 479% profit surge and the all-time share price record is a company executing a genuine pivot. Lenovo entered this cycle as a PC hardware leader with an early-stage infrastructure ambition. It exits the March 2026 quarter with a sustainably profitable AI server division generating 37% revenue growth and AI-related sales approaching 38% of group total.

This is not a one-quarter anomaly. It is the visible outcome of a multi-year infrastructure investment cycle reaching the profitability threshold. Investors who have tracked Lenovo primarily through a consumer hardware lens now have financial evidence to reassess the stock through an AI infrastructure framework, with all the valuation and risk implications that reframing carries.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.