The closure of the Strait of Hormuz in March 2026 transformed a regional geopolitical conflict into an immediate domestic economic constraint. By late April 2026, global energy markets reflect a sustained volatility that forces institutional and retail investors to reconsider baseline assumptions about consumer spending. Evaluating this geopolitical impact on stock market sectors reveals a clear macroeconomic conflict. Soaring energy input costs are colliding directly with squeezed consumer purchasing power.

The resulting pressure has fractured the United States equity landscape into distinct groups of winners and losers. This analysis unpacks the resulting sector divergence across US equities. It contrasts the structural margin destruction occurring within the travel industry with the operational resilience demonstrated by discount retailers.

Understanding how a barrel of oil dictates domestic consumer retail behaviour provides a crucial framework for portfolio positioning. The gap between the severity of the supply shock and the varied corporate responses reveals how capital markets price physical world disruptions.

The Energy Shock at the Strait of Hormuz

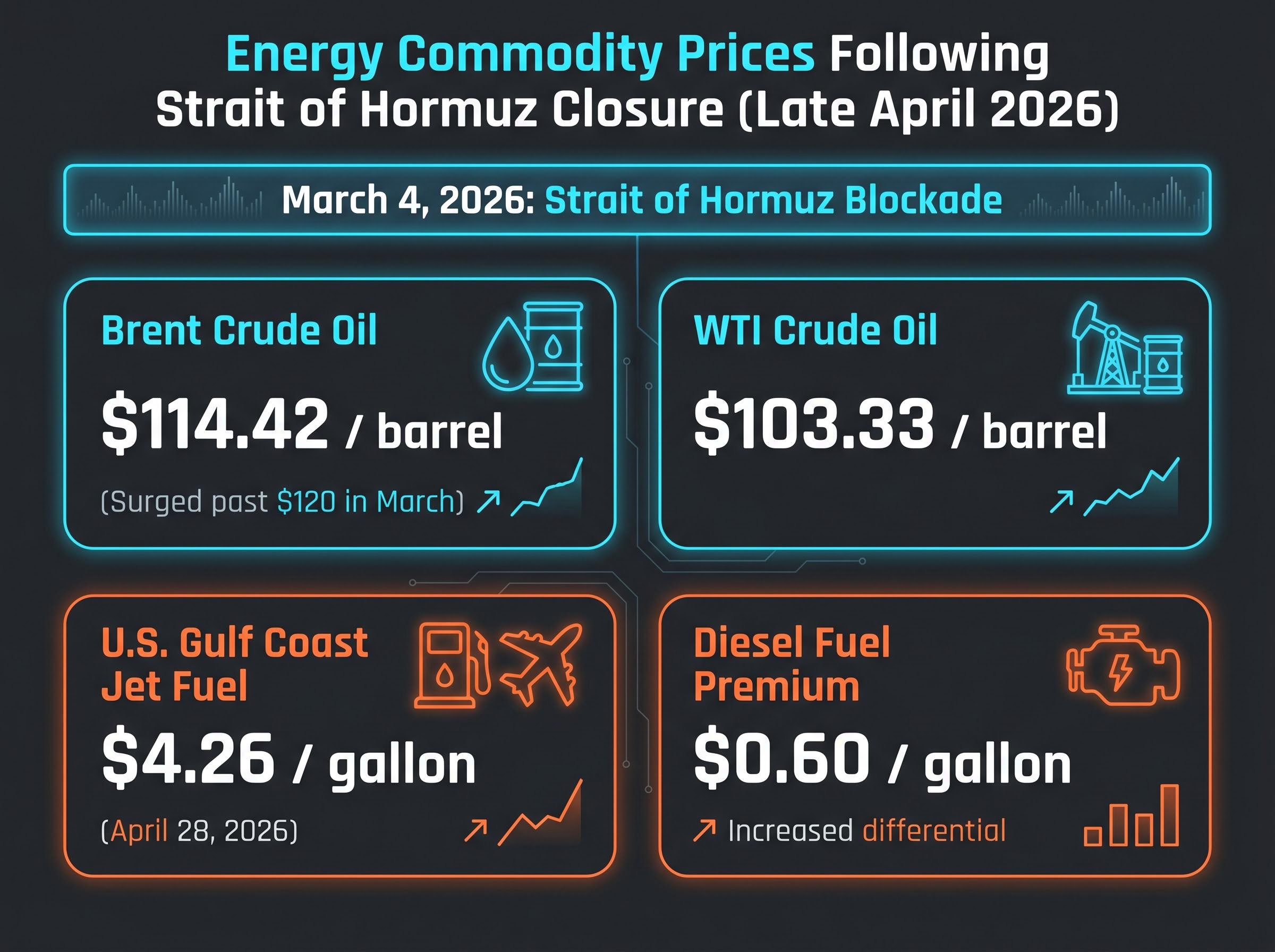

United States embargoes on Iran culminated in the complete closure of the Strait of Hormuz on March 4, 2026. This military blockade severed crucial global supply channels and triggered a structural shift in crude availability. Rather than a temporary panic, the resulting oil price surge has established a persistent supply constraint that industries must now absorb into their baseline projections.

By April 29, 2026, West Texas Intermediate (WTI) crude oil trades at approximately $103.33 per barrel. Brent crude sits at approximately $114.42 per barrel, having previously surged past $120 per barrel during the initial days of the March disruption. The blockade places a disproportionate burden on kerosene-based products due to specific crude refinery shortages.

According to Sterling Neblett of Centurion Wealth Management, the rapid surge in spot oil prices to over $100 per barrel creates persistent, unavoidable inflationary pressure across the industrial economy. Threats of Iranian mines previously added a $0.60 per gallon premium to diesel prices as regional crude remained stranded. Consequently, U.S. Gulf Coast jet fuel prices reached up to $4.26 per gallon by April 28, 2026.

| Energy Commodity | Price Benchmark (Late April 2026) |

|---|---|

| Brent Crude Oil | $114.42 per barrel |

| WTI Crude Oil | $103.33 per barrel |

| U.S. Gulf Coast Jet Fuel | $4.26 per gallon |

| Diesel Fuel Premium | $0.60 per gallon |

Understanding the permanence of these price floors is essential for evaluating companies tied to physical commodities and complex supply chains. The data indicates that fuel inputs will remain elevated, permanently altering the cost structures of energy-intensive industries.

For readers wanting to quantify the broader macroeconomic damage, our full explainer on oil price recession risks details the four simultaneous transmission channels that historically turn supply shocks into negative growth environments.

When big ASX news breaks, our subscribers know first

How Commodity Spikes Trigger Sector Rotation

The transmission mechanism of energy inflation explains why identical macroeconomic headwinds cause some equities to fall while others attract capital. Elevated fuel costs operate as a regressive tax on consumer discretionary spending. When household budgets are constrained by basic living expenses, consumers engage in “trading down” to stretch their diminished purchasing power.

This behavioural shift causes margin compression for businesses that cannot easily pass elevated costs onto their customers. Margin compression occurs when a company’s costs to produce or deliver goods rise faster than the prices it can charge, shrinking the percentage of revenue that becomes profit. Companies reliant on essential domestic consumption behave differently during crises compared to those exposed to global supply chains.

Energy inflation transmits through the broader economy across three primary channels:

Input costs: Direct manufacturing and operational expenses rise when raw materials and facility energy requirements become more expensive. Logistics and distribution: Freight providers impose mandatory fuel surcharges that increase the cost of moving inventory from factories to retail shelves. * Consumer wallet share: Higher prices at the petrol pump leave middle-income households with less discretionary capital for non-essential purchases.

This dynamic is accelerating the rapid depletion of household financial buffers, creating a massive divergence between headline retail sales and actual middle-class purchasing power.

Understanding these channels provides a framework for tracking sector rotation as capital flees vulnerable consumer discretionary stocks for resilient consumer staples.

Margin Destruction in the Aviation and Travel Industries

Abstract fuel costs quickly become harsh operational realities for airlines heavily dependent on kerosene-based inputs. JetBlue Airways serves as a direct proxy for this aviation sector vulnerability. On April 28, 2026, the airline reported a widened Q1 net loss of $319 million directly attributed to high fuel costs.

To preserve cash flow, JetBlue announced capacity cuts and fare hikes designed to recoup only 30% to 40% of the increased fuel expenses in Q2. The inability to fully offset these expenses highlights the fundamental weakness of the current aviation business model when confronted with external geopolitical shocks.

“Airlines face a mathematical impossibility when attempting to pass one hundred percent of doubled fuel costs onto consumers without destroying the underlying baseline travel demand.”

The broader aviation sector reflects this turbulence, with the Dow Jones U.S. Airlines Index falling 8.8% year to date by early April 2026. Resilient baseline travel demand means little if the underlying fuel inputs destroy the operational profit margin.

Anomalies within traditional transportation benchmarks further complicate the sector outlook, as short squeezes in specific equities have occasionally masked the underlying weakness of heavy freight and passenger operators.

The Booking Platform Ripple Effect

The margin destruction extends beyond asset-heavy airlines to asset-light technology companies facilitating global transit. Booking Holdings demonstrated this vulnerability when it cut its annual revenue growth forecast to high single digits on April 28, 2026. While the platform saw its EBITDA rise 19% to $2.2 billion, margins remain under intense pressure from macroeconomic realities and reduced consumer confidence.

Management reported a negative impact on room night expansion directly linked to international hostilities. This ripple effect illustrates that travel booking platforms cannot out-innovate the physical constraints of expensive global transit. Even software platforms ultimately rely on consumers possessing the discretionary income to book physical flights and hotel rooms. The sector remains fundamentally impaired until global crude supply normalises.

The Structural Advantage of Discount Retailers

Capital leaving the travel sector is actively rotating toward businesses demonstrating a structural advantage in an inflationary environment. Discount retailers are navigating the Hormuz blockade impacts with relative resilience. Diminished purchasing power drives middle-income shoppers to seek value at warehouse clubs and off-price apparel stores.

A domestic demand focus insulates these companies from the worst of the global shipping bottlenecks and international fuel surcharges. Costco reported Q1 CY2026 revenue of $69.6 billion, confirming the steady traffic flowing toward bulk purchasing models. Shoppers are consolidating their trips to maximise fuel efficiency, benefiting retailers capable of fulfilling multiple household needs simultaneously. The upcoming Q3 FY2026 earnings report, scheduled for May 28, 2026, is expected to further validate this consumer pivot.

TJX Companies showcases similar fundamental strength within the off-price apparel category. The retailer reported comparable sales up 5% and a strong pretax profit margin of 13.5%. The ability to maintain a 13.5% pretax margin indicates that off-price models possess superior pricing power compared to traditional department stores. On April 9, 2026, TJX issued confident FY2027 forward guidance of $4.93-$5.02 earnings per share.

This defensive investment strategy highlights where capital flows when traditional growth sectors become fundamentally impaired by geopolitical events. Discount retailers maintain their strength through three specific defensive characteristics:

- Membership revenue models: Upfront subscription fees provide highly predictable cash flow that helps offset temporary gross margin pressure.

- Inventory opportunism: Buyers can negotiate favourable terms with manufacturers desperate to offload excess stock during broader economic slowdowns.

- Domestic supply chain reliance: Sourcing and selling within the same geographic footprint limits exposure to international freight disruptions and maritime insurance spikes.

These structural advantages position discount retail as a reliable harbour for investors seeking shelter from global supply chain volatility.

Navigating a Market Anchored by Inflation

The inflation generated by soaring oil prices has effectively anchored Federal Reserve monetary policy for the foreseeable future. By late April 2026, the Federal Reserve benchmark rate target range stands stubbornly at 3.50% to 3.75%. The energy shock has forced a “higher for longer” interest rate environment that prevents central bankers from loosening policy to support struggling sectors.

According to CME FedWatch Tool data from April 2026, there is a 66% probability of the Federal Reserve holding rates steady for the remainder of the year. Market analysts project that the next interest rate reduction will not occur until later in the year or into 2027. This persistent tightening connects directly to the sectoral divergence between domestic discount retail and global travel providers.

Institutional recession probability modeling now heavily weights this delayed timeline, with major financial groups warning that a prolonged pause in rate cuts could trigger zero economic growth across the following quarters.

Investors must recalibrate their expectations for equity performance through the rest of 2026. Capital allocation strategies require a strict focus on companies that can maintain margins despite elevated operational costs and restrictive monetary conditions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.