US Jobs Report Misses by Half as June Adds Just 57,000

5 hrs ago

In financial markets, good news and bad news have a way of looking identical. A strong jobs report means the economy is healthy, which is good, until it means the Federal Reserve keeps rates higher, which is bad. A weak jobs report means rate cuts might be coming, which is good, until it means the economy is slowing, which is bad. The June payrolls data, released today, has delivered the most uncomfortable possible outcome: a report that is both soft enough to keep the Fed on hold and sticky enough in the places that matter to keep the hiking debate alive.

The miss lands at a moment when the Fed’s next move is genuinely contested. Most of Wall Street expects a prolonged pause, rates staying where they are while the economy absorbs existing restriction. But at least one major forecaster, KPMG, is projecting two additional hikes before year-end. That is not a fringe view. It is a conditional one, built on a specific reading of wage inflation that today’s data did not dismiss.

Here is what the June report actually settles, what it leaves open, and what that means for how you should be thinking about your portfolio through the fall.

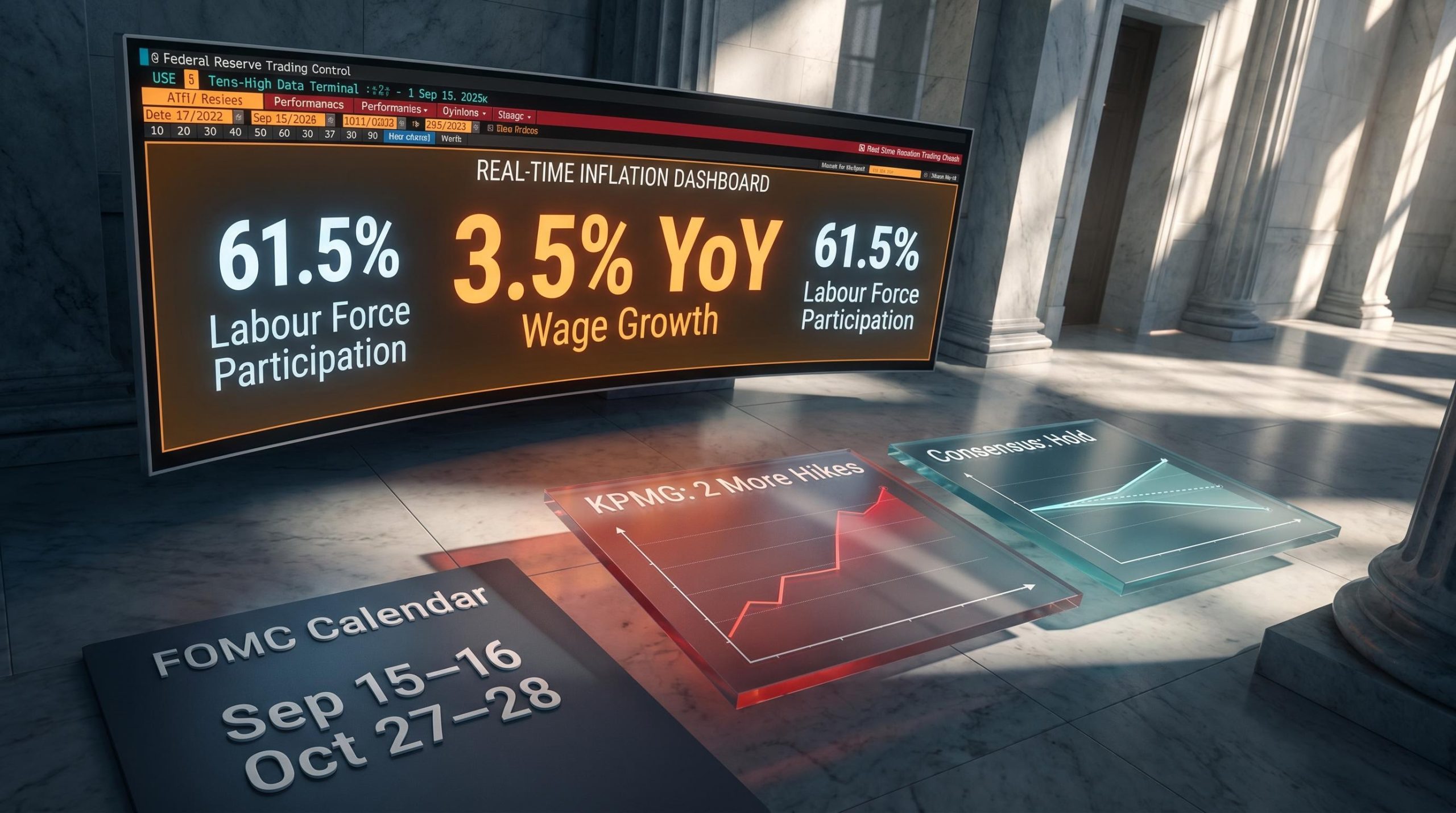

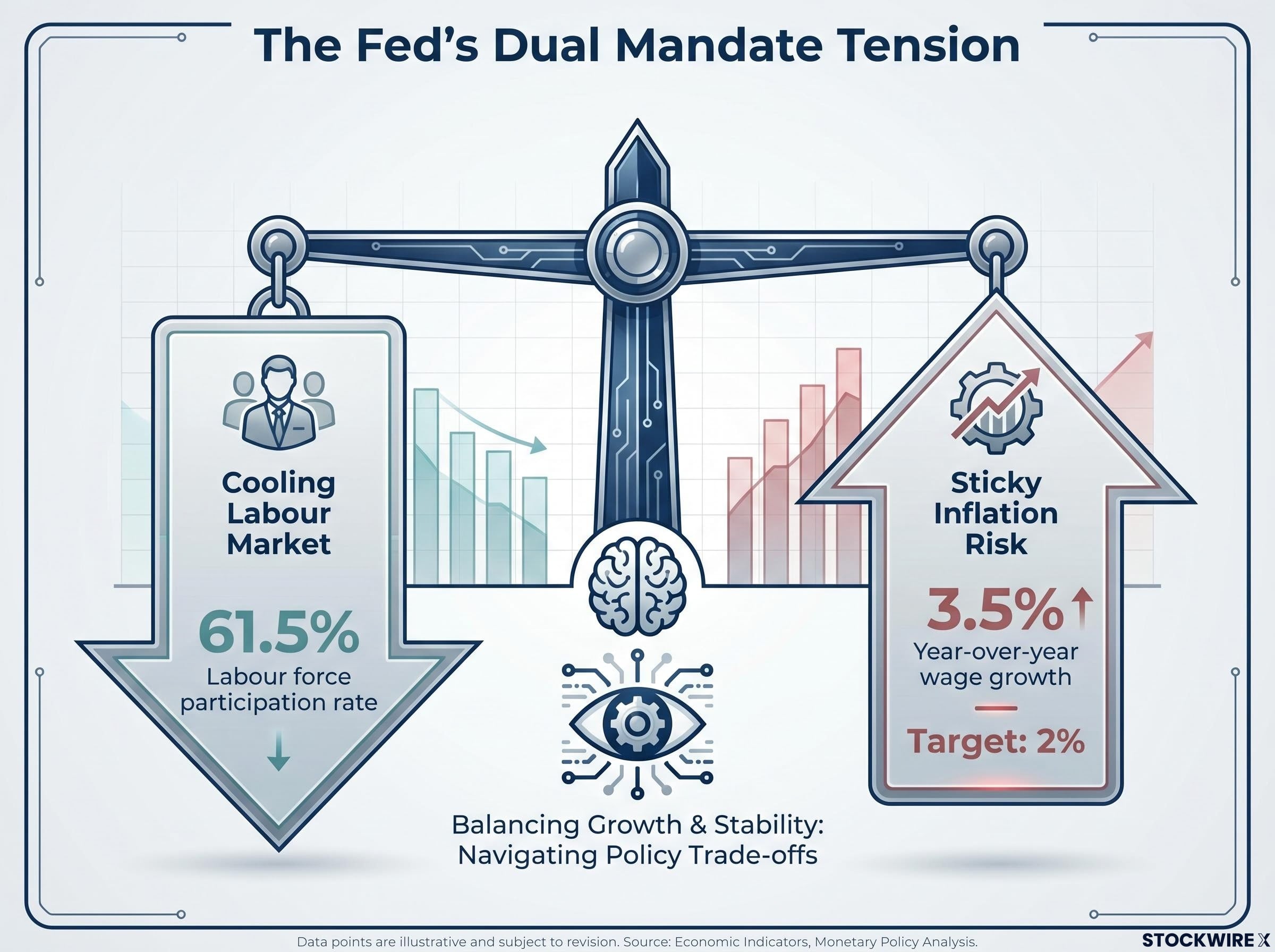

The headline number missed consensus expectations. Payrolls came in below what economists had forecast, and the labour force participation rate dipped to 61.5%, confirming that the labour market is cooling rather than re-accelerating. On its own, that is a straightforward dovish signal: fewer people working, fewer people looking for work, less pressure on the Fed to tighten further.

The May payrolls surge of 172,000, nearly double the 85,000 consensus, had reinforced a resilient labour market thesis through most of June, which is part of what makes the June miss so analytically significant: it breaks a streak of above-consensus prints rather than extending an already-soft trend.

Then there is the wage line. Year-over-year wage growth registered at 3.5% in June, and that single number is what makes this report genuinely ambiguous. A weaker headline print would normally hand the Fed a clean reason to stay put. But 3.5% wage growth keeps the inflation risk alive, because wages at that level are broadly inconsistent with a sustained 2% inflation regime once you account for productivity.

The tension between those two signals, soft employment but sticky wages, is what separates this report from a clean policy signal. It is a setup for debate, not a resolution.

| Metric | Value | Period | Fed signal |

|---|---|---|---|

| Labour force participation rate | 61.5% | June 2026 | Cooling labour market; supports patience |

| Year-over-year wage growth | 3.5% | June 2026 | Sticky inflation risk; keeps hiking debate open |

| Payrolls vs. expectations | Below consensus | June 2026 | Reduces near-term hike urgency |

The consensus view is not groupthink. It is a reasoned analytical position that lands on a specific reading of the dual mandate: when payrolls soften, the Fed’s employment objective re-enters the calculus as a counterweight to its inflation objective. The risk of overtightening into a slowing labour market becomes more salient, and the argument for patience sharpens.

Five credible, independent voices have converged on precisely this conclusion:

When that many analysts with that breadth of institutional perspective land on the same call, the preponderance of evidence favours patience, and you should weight your base case accordingly.

Michael Feroli of JPMorgan read the June data as broadly reassuring for the Fed’s pause position, arguing that a pullback in labour market momentum removes the upside inflation risk that a re-accelerating jobs market would have posed, and that policymakers at the centre of the FOMC now have firmer ground on which to hold rates steady.

The July 28-29 FOMC meeting is effectively settled. The question has already shifted past it, toward whether the fall meetings remain holds or become live. That distinction matters, because it determines whether the current policy rate is a ceiling or a waypoint.

The Fed operates under a dual mandate: price stability and maximum employment. Those two objectives can and do conflict. Right now, they are pulling in opposite directions. Inflation remains above the 2% target the Fed is working toward, which argues for keeping rates high or raising them further. But the labour market is softening, which argues for caution before adding more restriction.

At a “data-dependent pause,” the mechanism is not a formula. It is a judgment. The Fed is assessing whether existing rate levels are restrictive enough to continue pulling inflation down without pushing the labour market into outright contraction. Each monthly data release is an input into that judgment, not a trigger for automatic action.

That lag point matters directly to you. Rate changes take 12-18 months to fully transmit through the economy. Decisions made at the September or October meetings will not fully hit until mid-to-late 2027. The Fed is making a judgment about economic conditions more than a year out, under genuine uncertainty.

Policy transmission lags are longer and less predictable than most investors assume: Milton Friedman’s original framing of ‘long and variable lags’ has been repeatedly validated by empirical episodes, and the 12-18 month timeline is a central estimate around a wide distribution, not a precise forecast.

Wage growth at 3.5% is not simply one more line in the report. Sticky wages feed into services inflation through labour costs, which is the component of inflation the Fed watches most closely because it is the hardest to reverse. If businesses are paying 3.5% more for labour, those costs flow into the prices consumers pay for services, from healthcare to hospitality.

Productivity improvements can partially offset this dynamic: if workers produce more per hour, businesses can absorb higher wages without raising prices. But the current productivity environment does not fully neutralise a 3.5% wage print. That is why the Fed treats the wage line as a leading indicator of future inflation, not just a coincident measure.

Federal Reserve Bank of Boston research on wage growth and inflation finds that elevated wage gains are not automatically inflationary when productivity improvements and normalising markups absorb the additional labour costs, but the current productivity environment limits how much of that offset applies to the 3.5% figure in June’s report.

Investors who understand the dual mandate tension can read each incoming data point as the Fed reads it, turning routine monthly releases into forward-looking signals rather than historical footnotes.

Diane Swonk of KPMG U.S. is not making a contrarian bet. She is making a conditional forecast: two additional rate hikes by the end of 2026, contingent on wages and inflation remaining sticky through the July and August data. The mechanism is specific. KPMG believes financial markets are underpricing the Fed’s sensitivity to wage inflation in the mid-3% range, and that the June report did not provide enough evidence to dismiss that risk.

Swonk’s position at KPMG is that investor hopes for a Fed standstill are misplaced. In her assessment, year-over-year wage growth at 3.5% sits at a level that remains difficult to square with the Fed’s 2% inflation objective, and current market pricing underestimates the likelihood that policymakers respond with further tightening before the year is out.

The dot plot revision at the June 17 meeting had already shifted the Fed’s own year-end rate projection upward to 3.8%, putting at least one 25 basis point hike into the FOMC’s internal baseline before the June payrolls data even arrived.

The July meeting is not considered live in KPMG’s model. The scenario looks toward the fall: the September 15-16 and October 27-28 FOMC meetings, where the divergence between the consensus and KPMG views will become visible.

This is not the base case, but it is the risk case that matters most for positioning. If you hold duration-heavy fixed income or rate-sensitive equity positions, a fall hike surprise would be disproportionately painful.

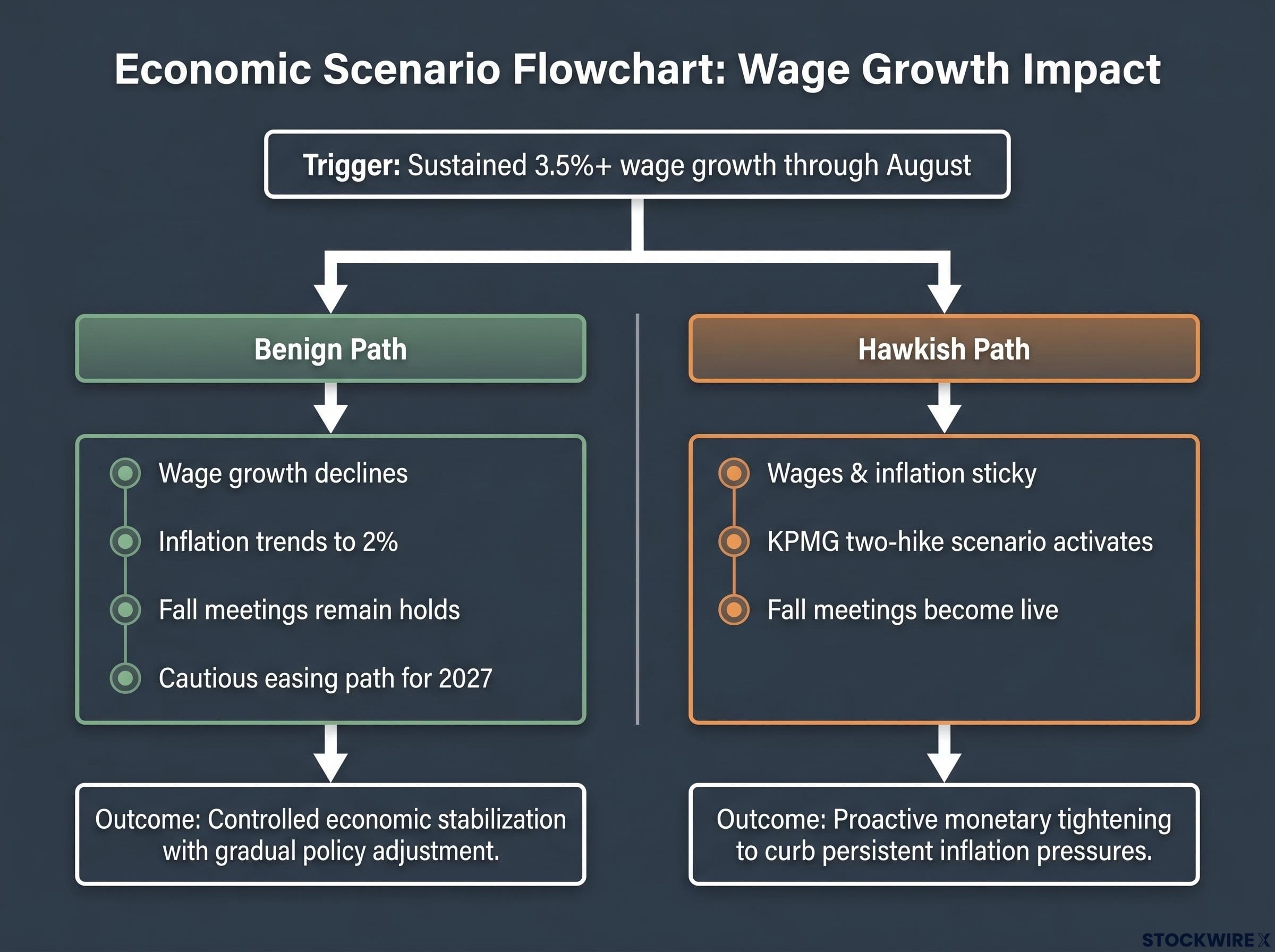

Benign path: Wage growth resumes its decline in July and August data. Inflation continues trending toward 2%. The fall meetings remain holds. The Fed signals a cautious easing path for 2027. Rate-sensitive assets hold their recent gains.

Hawkish path: Wages and inflation prove sticky at or above current levels. The KPMG two-hike scenario activates. Fall meetings become live. Duration-heavy and rate-sensitive positions come under pressure, and the market’s current “Fed is done” pricing reverses sharply.

The empirical trigger that separates these two paths is specific: sustained 3.5%-plus wage growth through August. That is the variable to watch, and knowing it gives you a data-watching framework rather than a vague sense of unease.

The initial session reaction embedded a distinctly optimistic interpretation of the softer employment figures:

Each of these moves follows the same internal logic: softer employment equals lower rates, lower rates equal higher valuations and weaker dollar. The logic is clean.

It is also conditional.

Day-one reactions to payroll data typically price the most straightforward scenario. Fewer hikes, lower yields, risk-on. What the current market move does not price is the possibility that labour softness eventually transmits into weaker consumer spending and earnings. Lower rates help equity valuations, but only if the softness that produced those lower rates does not become an earnings problem.

There is also a “held too long” scenario that is not yet reflected in asset prices: one where the Fed stays restrictive while the labour market deteriorates meaningfully. That would produce a different set of asset price outcomes entirely, and it is worth holding in your mental model even as the immediate reaction moves the other way.

The next 60 days of data will determine whether the consensus hold view or the KPMG hike view prevails. Three specific inputs matter:

Investors who watch only the headline payroll number and ignore the wage component are monitoring the wrong variable. It is the wage trajectory, not the jobs count, that will determine whether the Fed makes a move before year-end.

For investors who want to understand the institutional backdrop behind the fall meetings, our dedicated guide to Warsh’s early policy signals covers the inflation environment Warsh inherited, his preference for trimmed mean PCE over headline CPI, and what his accelerated balance sheet runoff signals about his tolerance for persistent price pressures.

| Meeting | Date | Key prior data | Decision trigger |

|---|---|---|---|

| September FOMC | 15-16 September 2026 | July and August payrolls, July core PCE/CPI | Wages sticky above 3.5% = meeting becomes live for a hike |

| October FOMC | 27-28 October 2026 | September payrolls, August core PCE/CPI | Last realistic window for a 2026 hike if hawkish path activates |

The June jobs report meaningfully reduces near-term hike risk. It shifts the July 28-29 meeting to a clear hold and hands the decision to fall data rather than resolving it. Both the consensus path, extended pause and eventual easing, and the KPMG path, two additional hikes by year-end, remain live. The next 60 days of wage and inflation data will determine which one becomes operational.

The appropriate posture is “on hold but not done,” not “the hiking cycle is over.” One soft report has bought time, not certainty. The portfolio decisions that matter most over the next three months hinge on data that has not been released yet, and the single variable with the most discriminating power is wage growth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Fed's dual mandate requires it to pursue both price stability and maximum employment simultaneously. In 2026, those two objectives are pulling in opposite directions: inflation remains above the 2% target, arguing for higher rates, while a softening labour market argues for caution before adding further restriction.

Wage growth at 3.5% is broadly inconsistent with a sustained 2% inflation regime because higher labour costs feed directly into services prices, which is the component of inflation the Fed watches most closely and finds hardest to reverse. The current productivity environment does not fully offset a 3.5% wage print, so the Fed treats it as a leading indicator of future inflation risk.

KPMG chief economist Diane Swonk is projecting two additional 25 basis point rate hikes before the end of 2026, contingent on wages and inflation remaining sticky through July and August data. Her view is that markets are underpricing the Fed's sensitivity to mid-3% wage growth.

The September 15-16 and October 27-28 FOMC meetings are the two windows where a hike could activate if wage growth stays at or above 3.5% through the summer data. The July 28-29 meeting is effectively settled as a hold by the June payrolls miss.

The three most critical inputs are the wage growth line in the July and August payrolls reports, core PCE and CPI prints for July and August, and whether payroll softness deepens into a trend or stabilises as a one-month result. Wage trajectory carries more discriminating power than the headline jobs count.