Futures Slide as June Jobs Report Puts Fed’s July Move in Focus

2 hrs ago

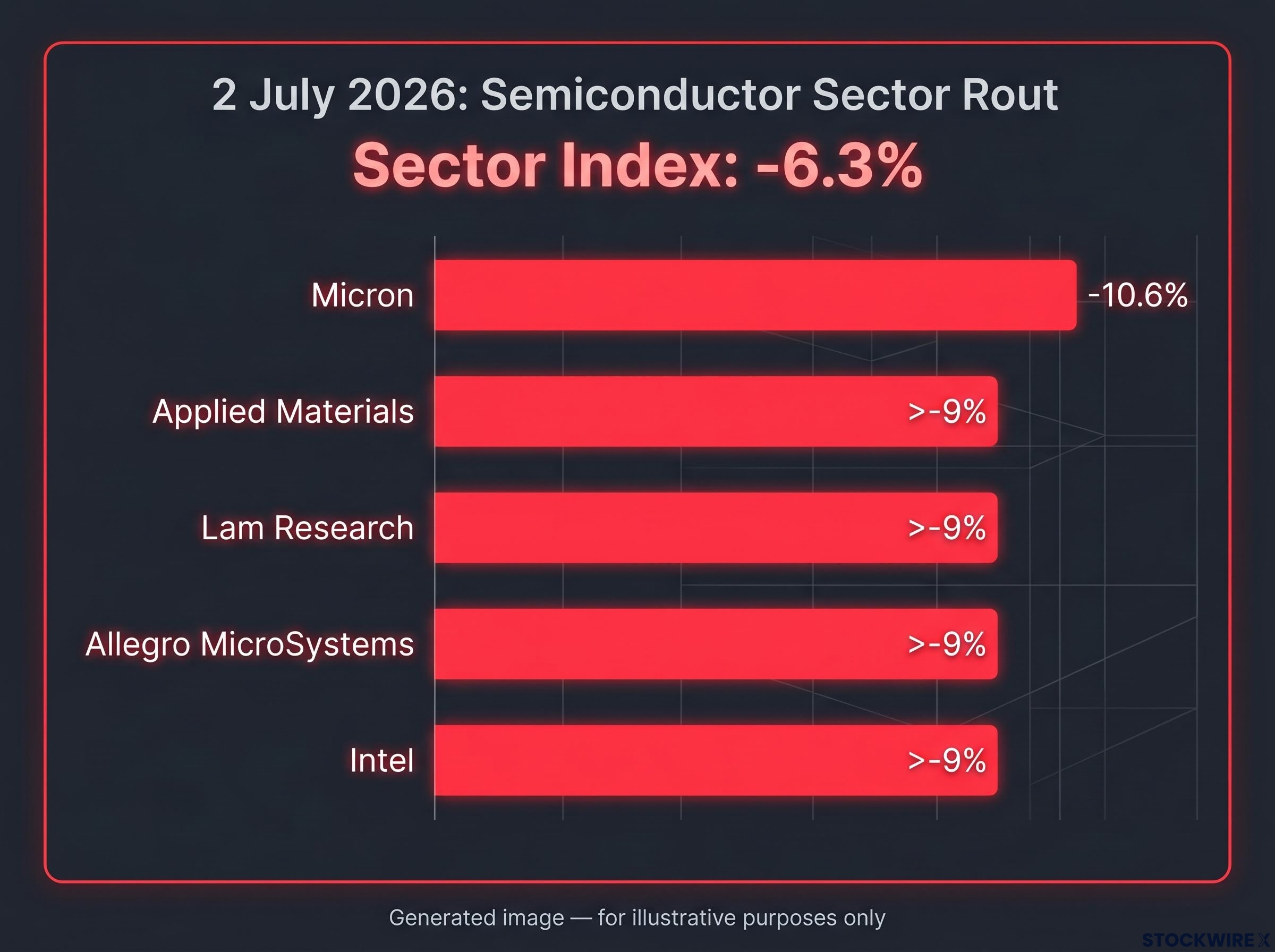

Semiconductor stocks suffered their worst single session of 2026 on Wednesday, with a sector index plunging 6.3% as losses swept across memory, equipment, logic, and legacy chipmakers in lockstep. Micron shed as much as 10.6% during the session. Applied Materials, Lam Research, Allegro MicroSystems, and Intel all posted intraday losses in excess of 9%. By Thursday morning, the selling had not stopped.

The conditions for this kind of broad repricing had been building for months. Chip stocks entered July priced for extraordinary AI-driven growth, with forward estimates embedding revenue and earnings trajectories that left almost no room for disappointment. When renewed doubts about the pace and durability of hyperscaler AI capital expenditure surfaced, the response was immediate and indiscriminate: every major subsector sold off together, from high-bandwidth memory to semiconductor equipment to optical networking.

Here is what the data tells you about which companies were hit hardest, what JPMorgan analyst Nikolaos Panigirtzoglou believes about the structural sustainability of chip stock outperformance versus cloud platforms, and what the pattern of repeated 2026 selloffs means for the road ahead.

The semiconductor sector index closed Wednesday’s session down 6.3%, making chipmakers the weakest-performing area within the S&P 500 and among the largest negative contributors to both the S&P 500 and Nasdaq.

6.3% single-session decline in the semiconductor sector index on 2 July 2026, the steepest drop for the sector this year.

The damage was not confined to one name or one subsector:

When memory, equipment, logic, and legacy names all sell off by the same magnitude on the same day, the cause is not company-specific. This was a sector-wide repricing event, and that distinction matters for how you think about exposure. A single-company miss can be isolated. A synchronised decline across every chip subsector tells you the market is reassessing the earnings base underneath all of these stocks simultaneously.

AI supply chain concentration matters for interpreting Wednesday’s synchronised selloff: foundries and memory producers such as TSMC and SK Hynix sit at structural chokepoints where every custom and third-party AI chip converges, which is why capex sentiment shifts propagate across memory, equipment, and logic names simultaneously rather than affecting only one subsector.

The pressure did not exhaust itself in Wednesday’s session. By approximately 04:42 ET on Thursday, premarket declines had spread across every major chip subsector, confirming that overnight trading brought no relief buying.

| Company | Subsector | Premarket Move |

|---|---|---|

| Micron | Memory / HBM | -2.1% |

| Western Digital | Memory / Storage | -2.1% |

| Coherent | Optical | -2.0% |

| Marvell Technology | Networking / AI silicon | -1.8% |

| AMD | Logic / AI GPU | -1.0% |

| Intel | Logic | -1.0% |

| Microchip Technology | Legacy / Embedded | -1.0% |

The premarket declines were smaller in magnitude than Wednesday’s losses. That is expected. The relevant signal is not the size of Thursday’s move but the fact that it happened at all. Memory, storage, optical, networking, logic, and legacy chipmakers all opened lower, which tells you that institutional sellers have not finished repositioning. The sector has not found a near-term floor.

Chip stocks entered this correction priced for perfection. Forward estimates for leading AI-exposed names had embedded very high revenue and earnings growth trajectories for 2026, with some bullish research on AI-related memory carrying projections of extraordinary expansion. As Barron’s warned, a “furious rally for chip stocks has raised fears of a new bubble.”

Semiconductor positioning data published in May 2026 complicates the reflexive bubble verdict: active long-only overweight in the sector stood at approximately 20%, half the 2017 cycle peak, and earnings estimates had been revised upward by more than 20%, giving the selloff a different character than a positioning unwind from speculative extremes.

That kind of valuation structure has a specific vulnerability. When forward multiples assume continuous, very high AI infrastructure spending, they leave no margin of error. Any signal that spending may slow, become more selective, or face longer payback timelines is enough to trigger a rapid repricing.

The mechanism is straightforward. Multiples that bake in extraordinary growth leave no buffer, so even a modest shift in tone on AI capital expenditure directly reduces the earnings base that underpins the current price. Prior 2026 selloffs were triggered not by outright demand collapses but by modest guidance disappointments. When your entry price assumes perfection, normal quarter-to-quarter noise becomes an outsized risk.

Writing on 2 July 2026 and cited via Investing.com, JPMorgan analyst Nikolaos Panigirtzoglou argued that chip and memory stocks have enjoyed a run of relative strength against hyperscaler cloud operators that is unlikely to hold over time. In his view, the gap in performance between AI chip and memory producers on one side and AI cloud providers on the other had been building in a “strong and almost steady” fashion since the previous September, reaching a point he described as “somewhat unsustainable in the long run.”

JPMorgan’s Panigirtzoglou characterised the prolonged outperformance of semiconductor stocks relative to hyperscaler cloud companies as “difficult to sustain” over the longer term.

The structural logic underpinning the view is worth understanding. If ultimate pricing power and long-term margins accrue more to the cloud platform operators, Microsoft, Amazon, and Alphabet, than to their chip and memory vendors, then the earnings multiple gap between the two groups becomes hard to justify. Reuters has separately cited investor concern over debt-funded AI spending by hyperscalers, questioning both execution and returns on investment.

For investors holding both semiconductor and cloud platform exposure, this is a prompt to reassess which side of the AI infrastructure trade actually captures the durable margin, not just the current narrative momentum.

Wednesday’s 6.3% sector index decline was not an isolated event. It fits a pattern that has defined semiconductor trading throughout 2026.

According to research compiled by Perplexity (not independently verified), the Philadelphia Semiconductor Index fell more than 6% on 5 June 2026 following a modest Broadcom AI revenue guidance miss, and dropped 7.9% on 23 June 2026 as investors scrutinised debt-funded AI spending alongside a more hawkish Federal Reserve. Micron, also per unverified Perplexity data, has fallen approximately 30% from its 18 March peak. Equipment makers like Applied Materials and Lam Research, alongside memory names like Micron and Western Digital, have appeared repeatedly at the centre of each episode.

The June 2026 semiconductor crash, triggered by a Broadcom AI outlook that fell short of investor expectations despite 143% year-over-year AI chip revenue growth, established the template for Wednesday’s episode: modest guidance disappointment, outsized sector response, trillion-dollar market cap destruction in a single session.

The pattern characteristics are consistent:

After multiple large corrections in a short window, bulls need to demonstrate earnings follow-through from AI spending commitments, not just continued spending announcements from hyperscalers. There is a distinction between hyperscalers reaffirming capex plans (necessary but not sufficient) and chip supplier earnings actually expanding at the pace valuations assumed. The latter is the harder, more important test. This pattern should recalibrate your volatility expectations and position-sizing assumptions regardless of your view on AI’s long-term trajectory.

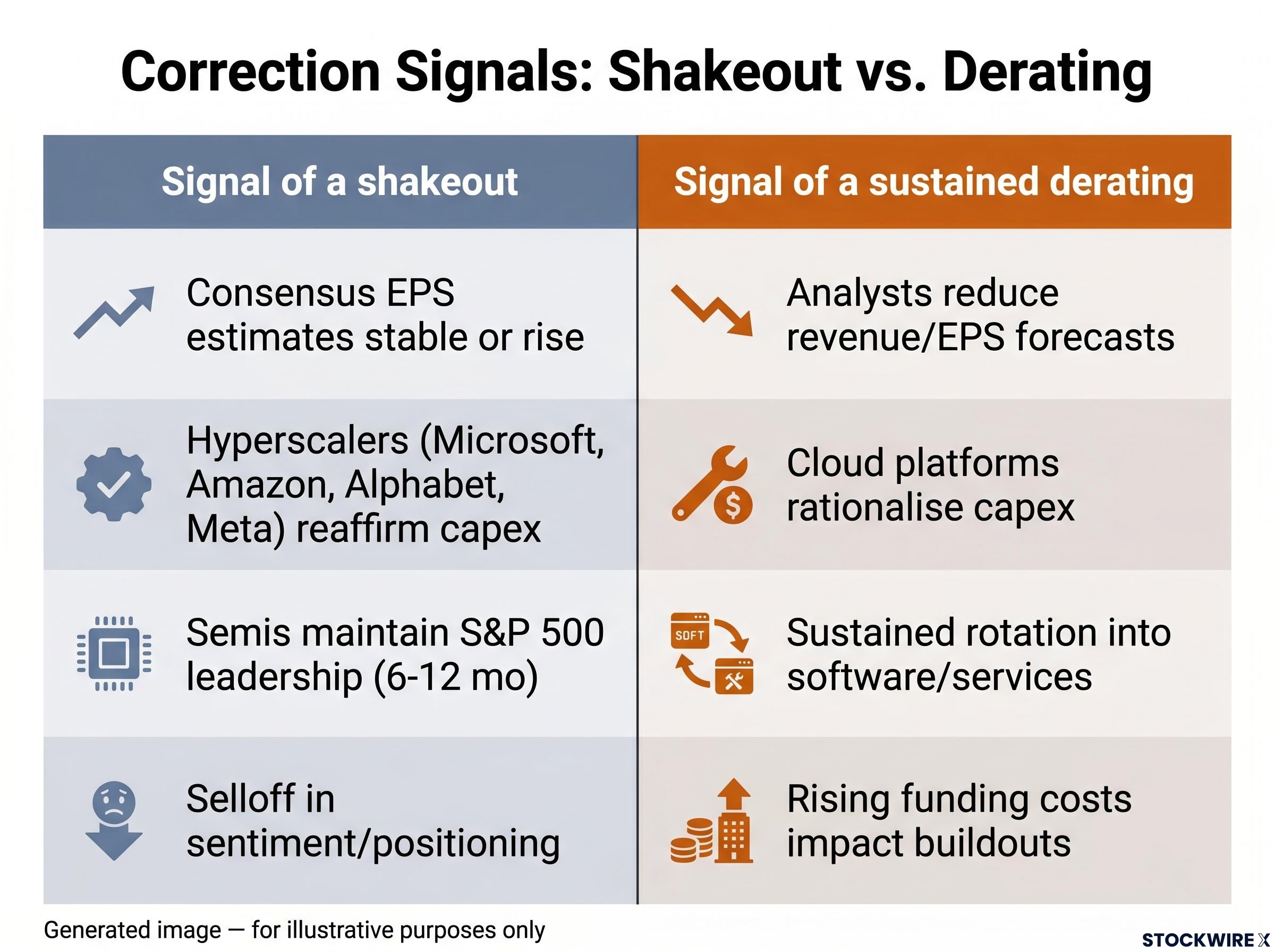

The question now is whether this is a temporary shakeout or the beginning of a sustained derating. Observable signals can help distinguish between the two.

| Signal of a shakeout | Signal of a sustained derating |

|---|---|

| Consensus EPS estimates for AI-exposed chip names remain stable or rise | Analysts systematically reduce revenue and EPS forecasts across memory, GPU, equipment, and networking names |

| Hyperscalers (Microsoft, Amazon, Alphabet, Meta) reaffirm AI capex plans | Cloud platforms begin discussing capex “rationalisation,” stretching timelines, or prioritising only highest-ROI projects |

| Semiconductors maintain relative leadership over the S&P 500 on a 6-12 month basis | Sustained rotation out of semiconductors into software or services for multiple consecutive quarters |

| Selloff concentrated in positioning and sentiment rather than fundamentals | Rising funding costs make multi-year AI buildouts harder for hyperscalers to justify |

The single most important variable to monitor is the gap between hyperscaler AI capital expenditure commitments and the actual earnings those commitments generate for chip suppliers. If that gap closes via rising earnings, current price levels can be justified. If it closes via lower valuations, the sector is in a derating phase. Watch for that signal across the next two to three earnings cycles; it will tell you more than any single session’s price action.

For investors trying to determine whether this correction marks the early stage of a sustained derating, our comprehensive walkthrough of semiconductor cycle indicators covers the five-signal framework for distinguishing a peak-cycle shakeout from the beginning of a structural downturn, including how memory, equipment, and logic names sequence through the cycle differently.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced are subject to market conditions and various risk factors.

The 6.3% sector index decline was driven by renewed doubts about the pace and durability of hyperscaler AI capital expenditure, which triggered a broad repricing across every major chip subsector simultaneously, from memory and equipment to logic and legacy chipmakers.

A sector-wide repricing occurs when memory, equipment, logic, and legacy chipmakers all sell off by a similar magnitude on the same day, signalling that the market is reassessing the earnings base underpinning the entire sector rather than reacting to a single company's results.

Micron posted the steepest intraday loss at up to 10.6%, while Applied Materials, Lam Research, Allegro MicroSystems, and Intel each shed more than 9% during the session.

JPMorgan analyst Nikolaos Panigirtzoglou argued that if long-term pricing power and margins accrue more to cloud platform operators like Microsoft, Amazon, and Alphabet than to their chip suppliers, then the earnings multiple gap between the two groups becomes hard to justify, prompting investors to reassess which side of the AI infrastructure trade captures durable margins.

The key signal is whether consensus earnings estimates for AI-exposed chip names remain stable and hyperscalers reaffirm capital expenditure plans (shakeout indicators) versus analysts systematically cutting revenue forecasts and cloud platforms signalling capex rationalisation (derating indicators), with the next two to three earnings cycles providing the most definitive read.