Semiconductor Stocks Suffer Worst Session of 2026 in 6.3% Rout

11 mins ago

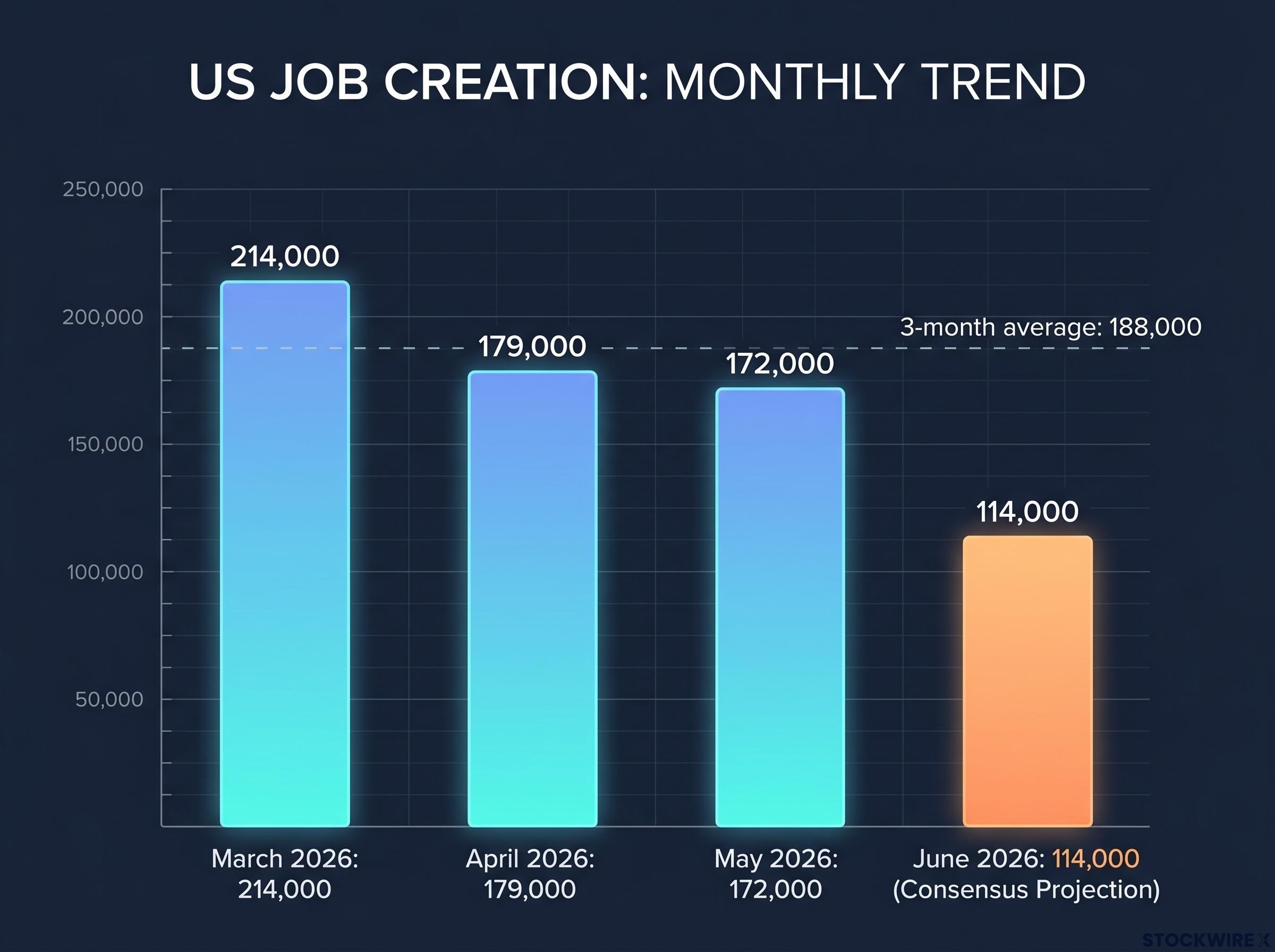

Forecasters put June U.S. job creation at just 114,000, a figure roughly 60,000 below what the economy delivered in May, pointing to a meaningful deceleration in the labour market.

The pre-market tone on 2 July 2026 tells the story: all three major index futures are in the red, with the Dow futures contract sliding 95 points, S&P 500 futures retreating 22 points, and Nasdaq 100 futures dropping 250 points as traders brace for a shortened holiday trading week. This is not panic. It is precision caution ahead of a number that will determine whether the Federal Reserve holds rates in July or keeps a hike on the table. Layered into that calculus: oil prices are falling as U.S.-Iran diplomatic talks in Doha produce cautious optimism, easing one of the Fed’s key inflation concerns.

Three forces are shaping the market right now: what the payrolls deceleration actually signals, what the Fed has already communicated, and how lower oil prices are doing disinflation work the central bank no longer has to do alone. Here is what each payroll threshold means for equities, bonds, and the July rate decision, and how to position around the number rather than react to it.

This is not just a labour market read. It is the single data point most likely to determine whether the Fed raises rates again in July or stays on hold. That makes it a policy signal first and a growth statistic second.

The recent payroll sequence tells you why the projected step-down matters:

The three-month rolling average reached roughly 188,000 jobs per month, a two-year high, with each of those prior reports coming in ahead of what analysts had pencilled in. A drop to 114,000 in June is not statistical noise. It is a structurally significant cooling, and it gives the Fed permission to stay patient. Understanding that permission is the key to reading Friday’s number correctly.

The May 2026 payroll beat of 172,000 jobs, nearly double the 85,000 analyst consensus, extended a three-month run of above-expectation readings that had kept a July rate hike firmly on the table and made the projected June deceleration a structurally significant shift rather than routine noise.

Private-sector employment data, released ahead of the official Labour Department figure, came in below expectations and immediately shifted rate-hike probability pricing. According to Deutsche Bank analysts, the combination of weaker private payrolls and softer factory activity data added further weight to the dovish repricing already under way. By the time the official number lands, markets have already absorbed the direction of travel.

Fed Chair Kevin Warsh acknowledged that inflation risks have come down, while simultaneously stressing his commitment to price stability and making clear he would not be providing forward guidance on the path for interest rates.

Warsh’s framing that inflation risks have diminished, delivered without forward guidance, effectively closed the door on a July hike for most market participants, even before the June jobs number arrives.

Warsh’s June press conference was the moment that crystallised the market’s dovish repricing, with his framing of diminished inflation risks delivered alongside an explicit refusal to offer forward guidance creating the conditional hold signal that now makes June payrolls the primary swing factor for the July meeting.

That sequence matters. With May inflation running at approximately 3.8%, still well above the Fed’s 2% target, hike risk was genuinely live until recently. The string of strong payrolls from March through May had kept that possibility on the table. Warsh’s remarks, combined with the softer private payroll data, shifted the market’s probability pricing toward a July hold.

But this repricing is conditional, not permanent. Warsh declining to offer forward guidance while acknowledging diminished inflation risk is the Fed’s way of keeping options open. A June print above 150,000 with strong wage data could reopen the hike debate. A Morningstar note from economists flagged that some still see room for multiple hikes in 2026 if jobs and inflation re-accelerate. The dovish shift is data-dependent, and the reader who over-rotates into rate-sensitive assets on the assumption that hikes are permanently off the table is taking a position the Fed itself has not endorsed.

Lower oil prices are the quiet third variable in this macro setup, and they explain why the Fed’s patience is not purely a labour market story.

U.S.-Iran diplomatic talks in Doha produced constructive signals this week, easing fears about Middle Eastern supply disruptions and pulling crude prices lower. The key developments:

Deutsche Bank analysts observed that the encouraging diplomatic signals pushed crude prices lower and helped reduce market anxiety around inflation.

The transmission mechanism is straightforward: lower crude flows through to petrol, transportation costs, and industrial input prices, reducing headline inflation without requiring Fed action. Combined with softer jobs data, the Fed now has two independent reasons to hold in July. For you as an investor, lower oil prices reduce the probability of an inflation flare that forces the Fed’s hand, and that makes the soft-landing scenario more durable than the labour data alone would suggest.

The inflation trajectory into the July meeting is shaped by a dynamic the headline CPI figure alone does not capture: gasoline prices fell roughly 11.5% from their mid-May peak through 30 June 2026, meaning the energy spike that drove headline CPI to 4.2% has already partially reversed and the next print is likely to come in cooler before the FOMC meets.

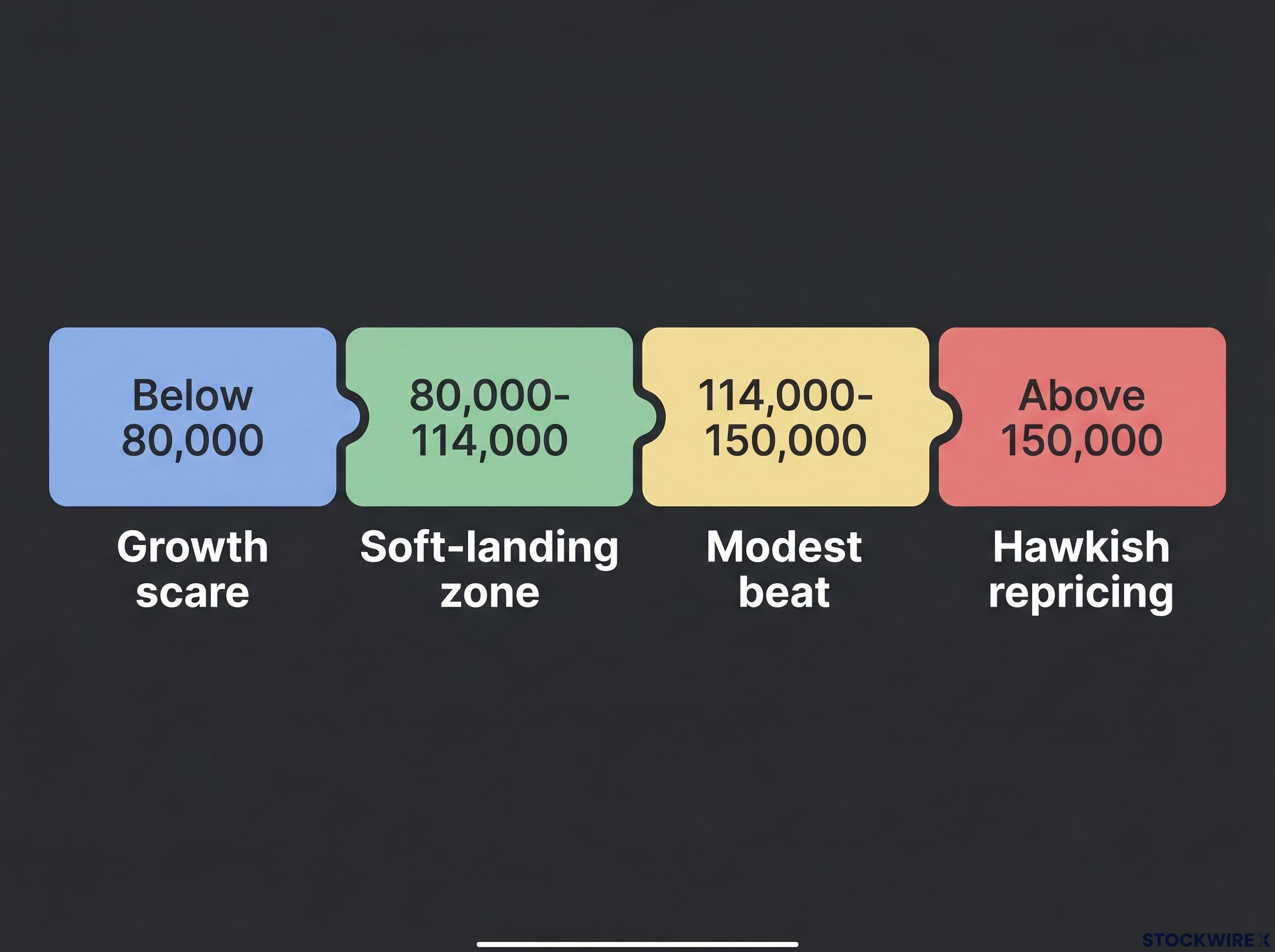

The most useful way to frame Friday’s number is not as a point forecast but as a threshold exercise. Each band carries a distinct market narrative, and knowing which band requires action is more valuable than predicting the exact print.

| Jobs outcome | Market narrative | Likely asset reaction | Key sectors to watch |

|---|---|---|---|

| Below 80,000 | Growth scare: “bad news for earnings” overwhelms “good news for rates” | Treasuries rally, dollar softens, gold strengthens | Defensives and quality dividend names outperform; cyclicals and small caps under pressure |

| 80,000-114,000 | Soft-landing zone: cooling but not collapsing | Rate-sensitive sectors supported; yields drift lower | Utilities, REITs, staples; tech and quality growth can perform well |

| 114,000-150,000 | Modest beat: still strong, Fed can stay patient for now | Limited change to July hike odds; volatility muted unless wages surprise higher | Broad market holds; watch wage details closely |

| Above 150,000 | Hawkish repricing: labour too strong for dovish comfort | Dollar strengthens, yields rise, growth and high-duration assets face selling pressure | Value and financials may hold up better; rate-sensitive growth under pressure |

Wage and unemployment data within the report matter alongside the headline number, particularly if the print lands in the middle bands. Consensus expects unemployment to hold steady at 4.3% and wage growth at approximately 0.3% month-on-month and 3.4% year-on-year. A headline print of 120,000 with a wage surprise to the upside tells a very different story from the same headline with flat wages.

The scenario grid tells you that the safest positioning right now is not a bet on any single outcome but an understanding of which threshold would require you to act, and why.

A soft landing means inflation falls without unemployment rising sharply or growth contracting. The Fed is trying to cool the economy enough to bring prices down, but not so much that it triggers a recession. That is the specific balancing act markets are pricing right now.

The current data describes a path toward that outcome, not away from it. But the path is narrow.

Three conditions need to hold simultaneously for the soft-landing narrative to remain intact:

That last point deserves more of your attention than the headline payrolls number. Unemployment rising alongside weaker payrolls signals a harder landing than unemployment staying flat with fewer new hires. Steady unemployment at 4.3% is the data point keeping the soft-landing thesis alive.

The Federal Reserve soft-landing probability framework, published by the Fed’s own research division, identifies stable unemployment as the single most important variable separating a genuine soft landing from a growth scare scenario, reinforcing why the 4.3% unemployment rate carries more diagnostic weight than the headline payrolls number.

The fragility is real: two or three consecutive prints below 80,000 would shift the conversation from soft landing to growth scare. But right now, the data supports the thesis. Understanding that framework protects you from the reactive trades that lock in losses when the market interprets nuanced data in a way the headline alone does not convey.

Holiday-week liquidity is thinner than normal, which means price moves after the number will be faster and potentially more exaggerated than a typical Friday release. Spreads widen. Stops trigger more easily. The first 30 minutes of trading after the headline drops are the most dangerous window for impulsive decisions.

Practical steps for managing the event:

The investor who treats this print as one input in a multi-month thesis is better positioned than the one treating it as a verdict. That distinction is where discipline separates returns.

Investors who want a framework for acting on this macro setup without reactive trading will find our comprehensive walkthrough of geopolitical risk investing covers the behavioural research on why headline-driven repositioning consistently underperforms, with specific guidance on dollar-cost averaging and diversification during high-uncertainty periods.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Three forces are reinforcing each other right now: a cooling labour market, a patient Fed, and oil-driven disinflation from diplomatic progress in Doha. Together, they describe the most constructive macro setup for risk assets in months.

But each force is conditional. The Fed’s patience depends on continued cooling. The oil tailwind depends on diplomacy holding. The soft-landing narrative depends on unemployment staying flat. If June payrolls land in the 80,000-150,000 band, the July meeting is almost certainly a hold, but the August jobs number will set the tone for September.

The jobs report is a policy signal now, not just a labour market read. Understanding that shift is the informational advantage that keeps you positioned ahead of the reaction, not scrambling behind it.

—

The US jobs report, released monthly by the Bureau of Labor Statistics, measures nonfarm payroll additions, unemployment, and wage growth. The Federal Reserve uses it as a primary indicator when deciding whether to raise, hold, or cut interest rates, making it one of the most market-moving data releases on the economic calendar.

Consensus forecasters expect approximately 114,000 jobs added in June 2026, down roughly 60,000 from May's 172,000 print and well below the three-month rolling average of 188,000, representing a structurally significant deceleration rather than statistical noise.

A print in the 80,000-150,000 range makes a July hold the most likely outcome; a print above 150,000 with strong wage growth could reopen the hike debate, while a print below 80,000 would shift the narrative from soft landing to growth scare, pressuring cyclicals and lifting Treasuries.

U.S.-Iran diplomatic talks in Doha produced constructive signals during the week of 2 July 2026, easing fears about Middle Eastern supply disruptions and pulling crude prices lower, which reduces headline inflation pressure and gives the Fed an additional independent reason to hold rates in July.

Use limit orders rather than market orders around the release window, size positions conservatively, and frame decisions on a 3-12 month horizon rather than reacting to a single print, since holiday-week liquidity thins spreads and can exaggerate short-term price moves.