Two of the world’s most-watched central banks just did nothing. And that nothing is one of the most important signals long-term investors will receive this year.

At their June 2026 meetings, both the US Federal Reserve and the Reserve Bank of Australia held rates steady. The reasons behind each decision differ in detail but converge on the same uncomfortable message: inflation is not yet beaten, and cuts are not imminent. For investors watching equity markets climb while macro headlines remain gloomy, the instinct to either flee to cash or make a concentrated bet on a rate pivot is understandable. It is also, historically, costly.

By the end of this piece, you will have a clear framework for understanding what both decisions actually signal, how each major asset class responds to a prolonged higher-rate environment, and what specific portfolio adjustments are worth considering right now, regardless of which direction rates eventually move.

The June 2026 decisions: two holds, one shared message

The Fed held on 17 June. The RBA held on 16 June. The outcomes were identical. The domestic pressures behind them were not.

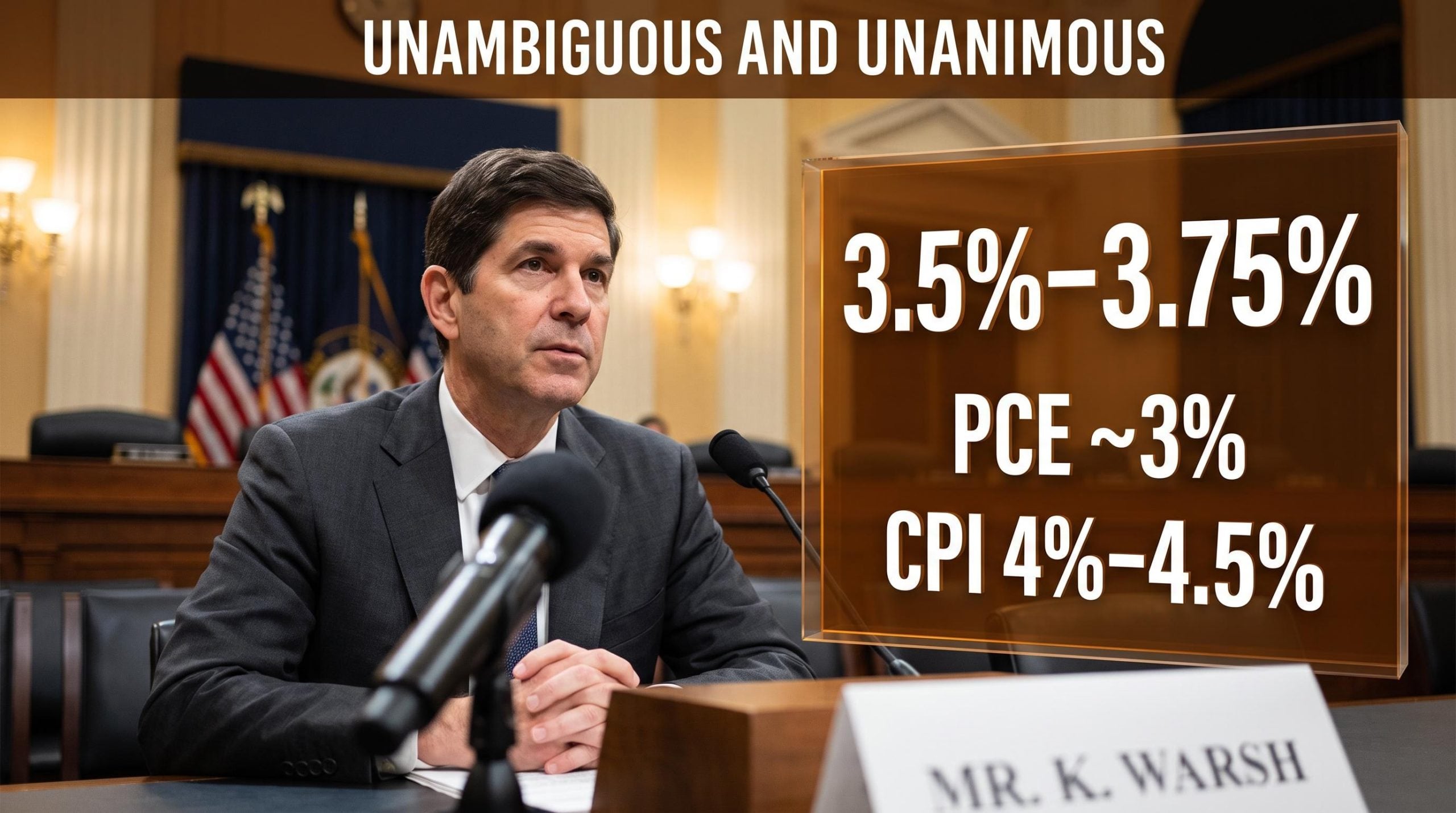

Despite coming into the role with a reputation for favouring looser monetary conditions, the Fed’s new chair opted to keep rates unchanged. Falling oil prices offered some relief on the inflation outlook, and political pressure from former President Donald Trump for cheaper borrowing had been vocal, yet neither was sufficient to prompt a move. The committee’s dot plot continued to point toward rates remaining elevated, reinforcing that no pivot is on the near-term agenda. Across the Pacific, the RBA confronted a parallel dilemma shaped by local conditions. Australia’s rates are among the steepest in the developed world, households are feeling the strain through weakening property auction results, and consumer confidence has turned markedly pessimistic. Even so, underlying inflation has not fallen far enough to justify easing.

The domestic pressures the RBA is navigating trace back to a sharp acceleration in Australian inflation data earlier in 2026, when headline CPI surged to 4.6% against a target band of 2-3%, triggering a series of consecutive rate hikes that left households and businesses absorbing the cumulative effect by the time June arrived.

The Federal Reserve’s June 2026 FOMC statement confirmed that the committee views inflation as still elevated and reaffirmed that rates would remain at current levels, with no forward guidance pointing toward near-term easing.

| Central Bank | Decision Date | Key Domestic Pressure | Policy Signal |

|---|---|---|---|

| US Federal Reserve | 17 June 2026 | Persistent inflation; political pressure for cuts | Dot plot signals rates elevated through 2026 |

| Reserve Bank of Australia | 16 June 2026 | Housing stress; weak consumer sentiment | Inflation not yet contained; no easing signal |

Both institutions are pausing, not declaring victory.

The fact that two central banks with different domestic pressures landed on identical postures tells you “higher for longer” is not a US-specific story. Your portfolio needs to be built for a world where that holds for longer than markets currently price.

When big ASX news breaks, our subscribers know first

Why “higher for longer” is harder to sit with than it sounds

Here is the discomfort: equity markets are rising. At the same time, consumer sentiment in Australia is notably negative, property auction clearance rates are falling, and inflation in both economies remains sticky. Those two realities feel contradictory. They are not, but the tension between them is where costly investor mistakes get made.

The temptation splits into two familiar responses. The first is to flee to cash, treating the macro uncertainty as a reason to step aside until the picture clears. The second is to make a concentrated bet that a rapid rate pivot is coming, loading up on the assets most sensitive to cuts. Both are historically expensive.

The discomfort is compounded by a genuine policy uncertainty that even the central banks themselves are navigating. Both institutions face two distinct failure modes:

- Cut too early and risk reigniting inflation, forcing a more painful second round of tightening

- Hold too long into a fragile economy, particularly in Australia where housing and consumer stress are already visible, and risk tipping the economy into an unnecessary contraction

That asymmetry is not something that resolves before you need to make portfolio decisions. It is the environment itself.

The psychological trap: mistaking caution for strategy

There is a difference between deliberate cash allocation aligned to your time horizon and reactive caution driven by uncomfortable headlines. The first is strategy. The second is a timing bet dressed as prudence.

The cost of timing errors is compounded by a second problem: even if you step aside at the right moment, you still need to decide when to step back in. Research consistently shows this cost is real and measurable over time. Markets rising despite gloomy headlines is not a paradox to resolve before investing. It is the normal condition of investing through volatile cycles. Waiting for the contradiction to disappear means waiting indefinitely.

Morningstar research on market timing costs demonstrates that investors who shift between equities and cash in response to macro uncertainty consistently underperform fully invested portfolios over comparable periods, with the gap compounding materially across multiple rate cycles.

What “higher for longer” actually means for each asset class

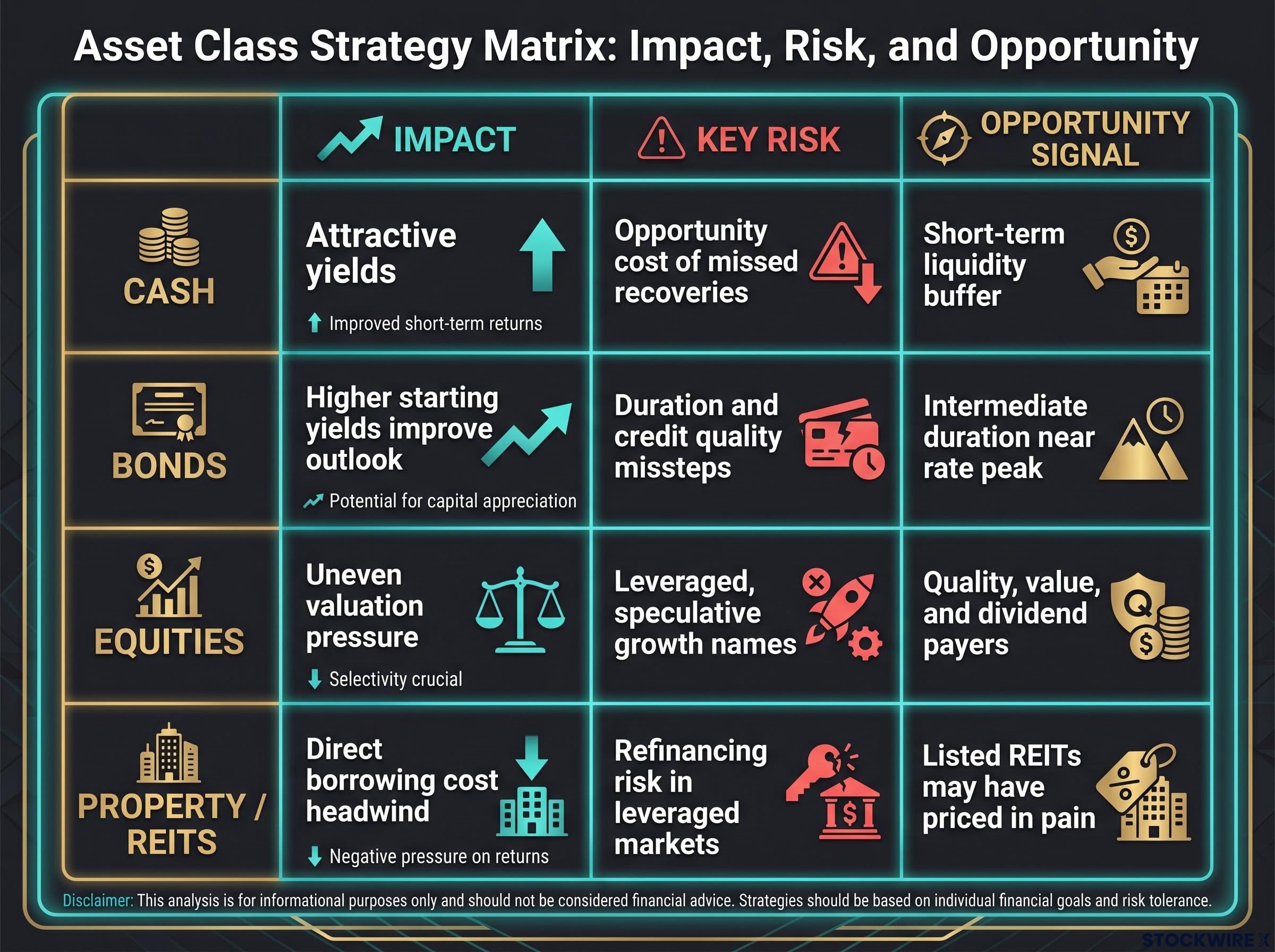

Not every asset class absorbs higher rates the same way. The differences are where portfolio decisions live.

Cash and short-term instruments offer yields that look attractive relative to the past decade. That is real. But the opportunity cost of staying there too long, missing the early stages of equity or bond recoveries, is where the damage accumulates. Cash is a position, not a default.

Bonds: starting yields change the maths

Starting yields today are meaningfully higher than during the ultra-low-rate era. That single fact improves prospective long-term bond returns even before any rate cuts materialise. The term “starting yield” refers to the yield available when you buy a bond; higher starting yields mean more income from day one, which cushions against price fluctuations.

Within fixed income, the decisions that matter are duration (how sensitive your bonds are to rate changes) and credit quality. Shorter-duration, high-quality bonds provide ballast and liquidity. Intermediate duration becomes more attractive if rates are near their peak. And the distinction between investment-grade and speculative credit, bonds issued by financially strong companies versus those with weaker balance sheets, matters more when borrowing costs stay elevated and weaker borrowers face refinancing pressure.

For investors wanting to translate the duration and credit quality principles outlined above into specific allocation decisions, our dedicated guide to bond portfolio management examines the 1-5 year curve segment favoured by BlackRock, PIMCO, Vanguard, and J.P. Morgan Asset Management, with worked analysis on how to calibrate duration given your spending timeline and risk tolerance.

Equities: not a uniform warning

Higher rates raise the discount rate used to value future earnings, which pressures valuations. But the impact varies sharply across the equity universe. Companies with strong balance sheets, consistent free cash flow, and pricing power absorb higher rates. Leveraged, cash-burning businesses suffer them.

The discount rate pressure the article describes has a specific mechanism: a rising real yield hurdle rate means every equity, credit, and alternative asset must now generate higher real returns just to justify its current price, which is why leveraged and cash-burning businesses face disproportionate pressure even when headline index levels hold up.

Financials can benefit from higher net interest margins (the spread between what banks earn on loans and pay on deposits), depending on the shape of the yield curve. Value and dividend-paying stocks often outperform when capital is no longer free. US equity markets have demonstrated they can rise in a higher-rate world when earnings are resilient, supported by productivity gains and AI-related tailwinds, but the margin for error narrows when valuations are rich.

Property and real assets face the most direct headwind. Higher borrowing costs weigh on housing and commercial property, particularly in leveraged markets like Australia, where declining auction clearance rates reflect the pressure in real time. Listed Real Estate Investment Trusts (REITs), companies that own and operate income-producing property, may have already priced in some of this pain. But fundamentals like vacancies, rent growth, and refinancing risk matter more than ever.

| Asset Class | Rate Environment Impact | Key Risk | Opportunity Signal |

|---|---|---|---|

| Cash | Attractive yields | Opportunity cost of missed recoveries | Short-term liquidity buffer |

| Bonds | Higher starting yields improve outlook | Duration and credit quality missteps | Intermediate duration near rate peak |

| Equities | Uneven valuation pressure | Leveraged, speculative growth names | Quality, value, and dividend payers |

| Property / REITs | Direct borrowing cost headwind | Refinancing risk in leveraged markets | Listed REITs may have priced in pain |

The asset class map tells you where this rate environment creates friction and where it creates opportunity. Your current allocation should reflect a deliberate view on both, not a passive inheritance of last cycle’s positioning.

Currencies, global diversification, and the AUD/USD dynamic

Currency is the dimension most investors underestimate when central banks diverge. Two scenarios matter here:

- The Fed cuts first: If US rates fall before Australian rates, downward pressure on the USD follows, supporting non-US assets and the AUD

- Global stress resurfaces: The USD reverts to safe-haven behaviour regardless of relative rate levels, which can weigh on AUD-denominated returns from global holdings

Both outcomes are plausible, and the genuine uncertainty between them argues for diversification rather than a directional currency bet.

Currency diversification is a structural hedge, not a speculative bet.

For any investor with significant domestic concentration, whether in Australian property, AUD cash, or domestic equities, some unhedged global exposure is not speculation. It is structural diversification against the specific risks already concentrated in your balance sheet: housing, employment, and currency, all of which correlate with the Australian domestic cycle.

The next major ASX story will hit our subscribers first

A practical portfolio framework for sitting with uncertainty

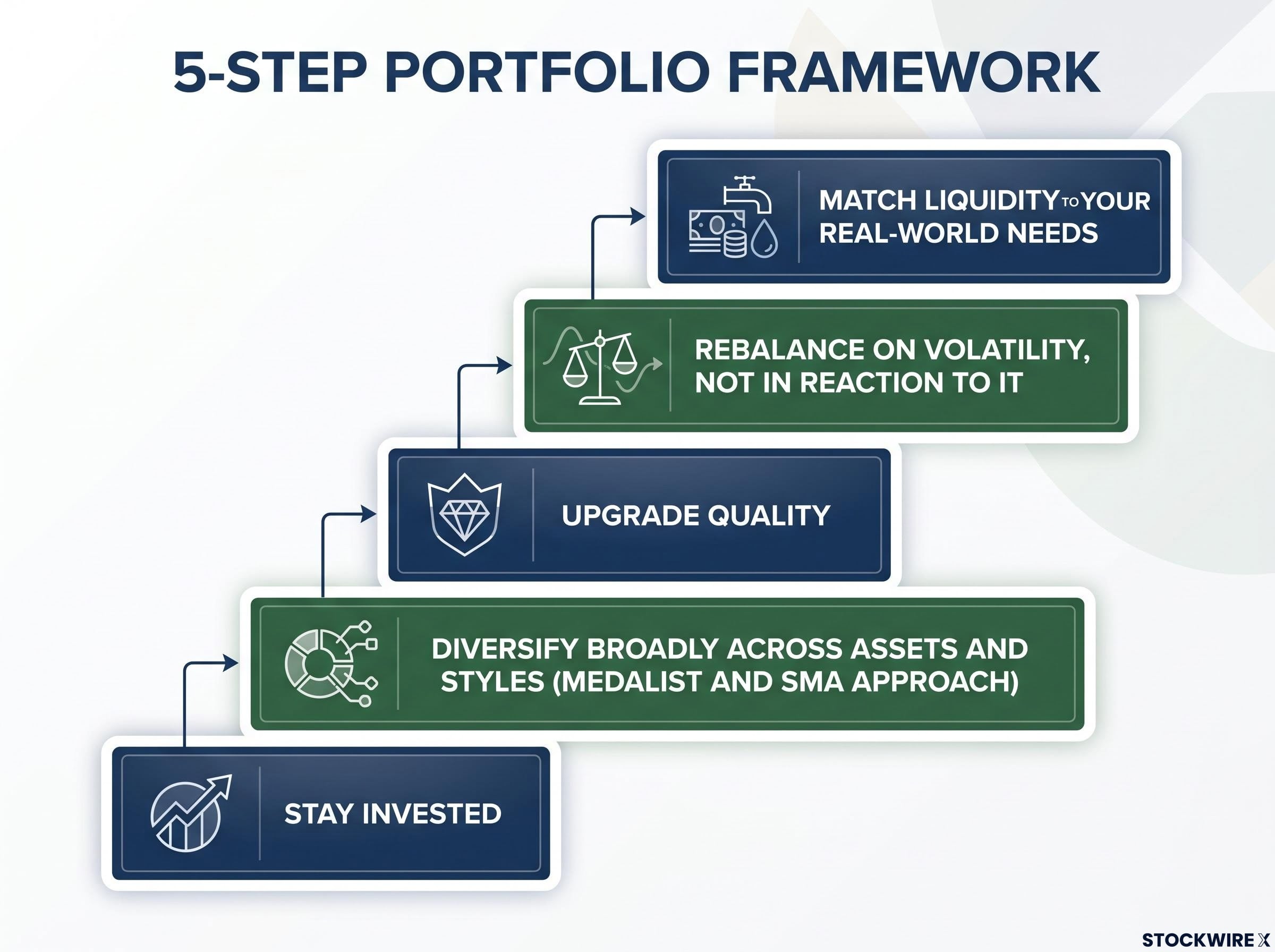

Central bank paths are notoriously hard to forecast, even for professionals. Building a portfolio that performs across multiple scenarios is more reliable than trying to front-run each meeting outcome. Here are five steps grounded in the conditions described above:

- Stay invested. The cost of stepping out and mistiming the re-entry compounds over time. A stay-the-course approach, anchored to your time horizon, outperforms reactive repositioning in the vast majority of historical periods.

- Diversify broadly across assets and styles. Rather than concentrating on a single macro view, spread exposure across equities, bonds, and cash. Within equities, vary by region, style (growth, value, quality), and sector. Within bonds, blend durations. The Medalist and SMA approach puts this into practice by identifying strong managers within individual asset classes and then combining those managers across a broad range of asset classes, building diversification into the portfolio’s structure from the ground up.

- Upgrade quality. In equities, prefer businesses with strong balance sheets, consistent free cash flow, and pricing power. In fixed income, favour investment-grade over speculative credit unless you are explicitly compensated for the additional risk.

- Rebalance on volatility, not in reaction to it. If equities have run ahead of macro concerns, trim back to your target allocation. Use volatility around Fed and RBA communications as a rebalancing trigger, not a reason for wholesale strategy changes.

- Match liquidity to your real-world needs. Keep enough safe, liquid assets to cover near-term spending and contingencies so you are never a forced seller into a downturn. Align your equity allocation with your time horizon and tolerance for drawdowns, not with the latest rate headline.

“Individual risk tolerance should govern portfolio construction, not short-term macro noise.”

None of these five steps require you to predict where rates go next. They are designed to build a portfolio that performs across multiple outcomes, which is precisely the right response to an environment where even central banks do not know what they will do next quarter.

Investors ready to move from the framework above to specific allocation decisions will find our full explainer on building a resilient inflation portfolio, which details a 40% equities, 30% bonds, 20% alternatives, and 10% cash structure, with ASX ETF recommendations for each sleeve and guidance on integrating physical gold and commodity exposure as an inflation hedge.

The rate plateau is an environment, not an emergency

Two central banks holding rates steady is not a reason to wait for a cleaner macro moment. It is a signal to build for duration and resilience. The inflation fight is not over, policy will remain relatively tight, and the timeline for cuts remains genuinely uncertain.

The practical response is specific, not abstract. Review your allocation against the quality and diversification criteria laid out above. Make one adjustment this week rather than waiting for certainty that may not arrive in the form you expect.

When cuts do eventually come, investors who stayed diversified and quality-tilted will be positioned to benefit from the recovery without having missed the runway leading into it. The rate plateau rewards patience, discipline, and a portfolio built to handle more than one outcome. That is the only honest strategy when even policymakers are navigating quarter by quarter.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—