Barclays Lifts S&P 500 Target to 7,800 on AI Earnings Bet

2 hrs ago

The Federal Reserve’s preferred inflation gauge came in exactly where analysts expected for May 2026, and on a day when oil prices have been doing some of the heavy lifting, that matters more than the headline number alone suggests.

Released today by the Bureau of Economic Analysis (BEA), the May 2026 Personal Consumption Expenditures (PCE) report shows headline and core readings that matched or slightly undershot consensus forecasts. The result removes one tail risk from the near-term policy landscape: the Fed does not face a hot-print surprise that would force a hawkish reassessment. But the numbers also confirm that inflation remains well above the 2% target, leaving the central bank in the same cautious holding pattern it has maintained for months.

Here is what the numbers actually say, why falling oil prices have complicated the read, what the Fed is likely to do next, and which indicators over the remainder of 2026 will determine whether today’s relative calm holds.

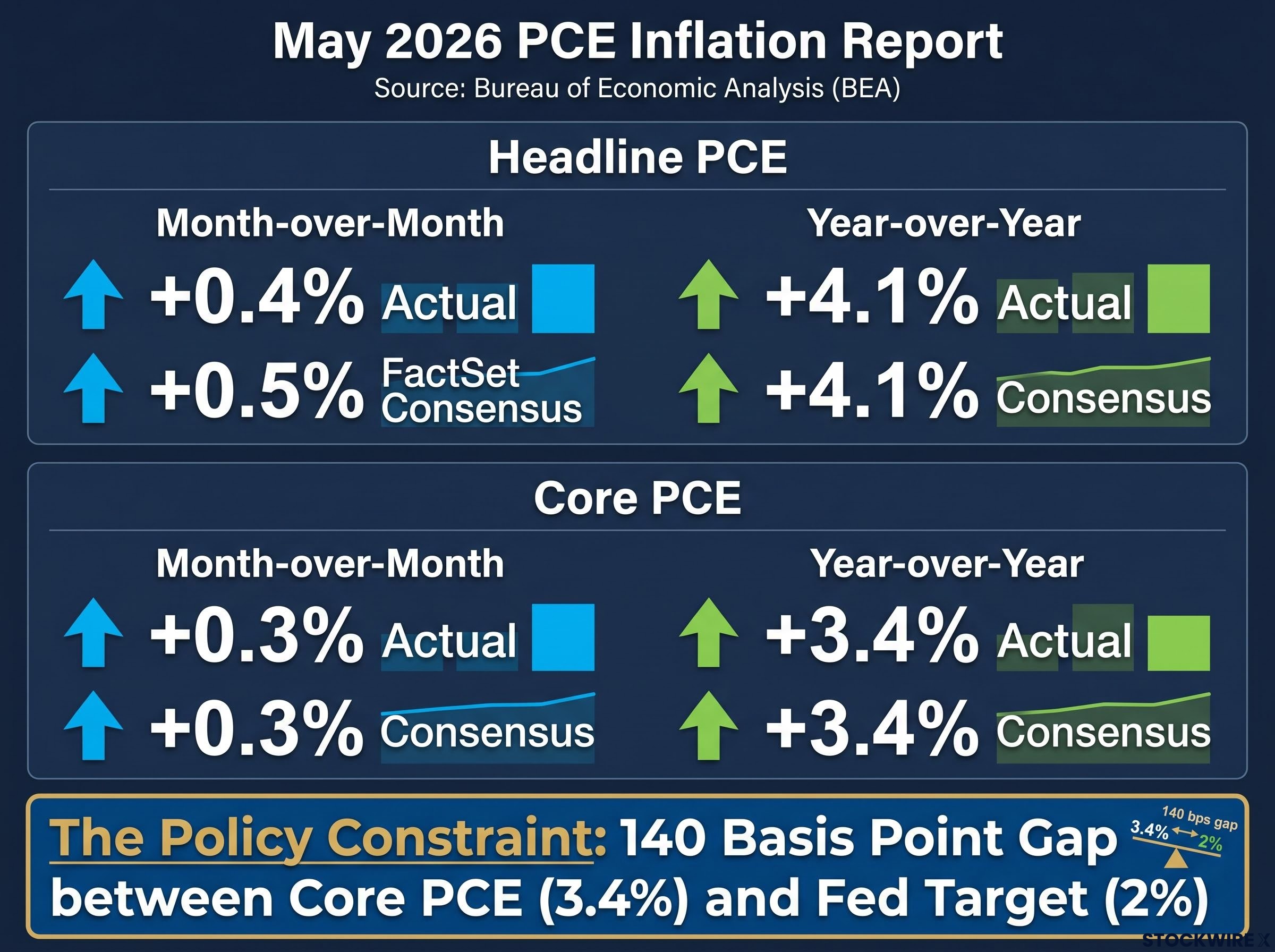

The headline PCE price index rose 0.4% month-over-month, slightly below the 0.5% consensus tracked by FactSet. On an annual basis, prices climbed 4.1%, matching forecasts precisely.

The core PCE measure, which excludes food and energy to capture the underlying direction of prices, posted a gain of 0.3% on the month and 3.4% on the year. Both figures landed precisely in line with analyst forecasts and came in slightly above where they stood in April.

| Measure | Actual | Consensus | Prior Month |

|---|---|---|---|

| Headline PCE (MoM) | +0.4% | +0.5% | Lower |

| Headline PCE (YoY) | +4.1% | +4.1% | Lower |

| Core PCE (MoM) | +0.3% | +0.3% | Lower |

| Core PCE (YoY) | +3.4% | +3.4% | Lower |

The number the Fed watches most closely: Core PCE at +3.4% year-over-year, the reading that strips away commodity noise and reveals the underlying inflation signal policymakers use to calibrate rate decisions.

A miss in either direction would have moved markets. A hot print would have forced traders to reprice rate expectations higher. A cool print would have sparked premature easing bets. The exact match is the news: price pressures are elevated but not accelerating, which is precisely the reassurance markets needed to avoid a repricing of rate expectations today.

April’s inflation shock, when monthly CPI printed at +0.6% against a +0.3% consensus and pushed the annual rate to 3.8%, established the baseline of anxiety that made May’s in-line PCE result feel like reassurance rather than a routine data release.

The most direct channel is the one consumers see at the petrol station. Oil prices declined through the May 2026 period and into mid-June, feeding straight into lower gasoline costs. AAA gasoline price data referenced in analyst commentary confirmed that pump prices eased during the reporting window, pulling the headline PCE reading lower than it would have been under stable energy prices.

But the effect runs deeper than pump prices. Cheaper crude suppresses costs across three interconnected channels:

Analyst commentary noted that inflation worries had “broadly diminished” in conjunction with the sharp oil decline. That framing is accurate, but it contains a vulnerability.

The disinflationary effect from falling oil is real but borrowed. If crude reverses course, all three channels flip from tailwind to headwind, and the headline print will reflect it quickly. Today’s relatively contained number is partly a function of a favourable energy environment that the Fed cannot control and that markets cannot count on persisting.

PCE stands for Personal Consumption Expenditures. It is the BEA’s measure of the prices Americans pay across a wide basket of goods and services, from healthcare to housing to haircuts. The Federal Reserve formally targets PCE inflation at 2% annually, making every decimal move in this reading a direct input to rate decisions.

The BEA’s PCE price index data covers the full methodology behind how the agency constructs its spending basket, including the treatment of imputed costs like employer-sponsored healthcare that make PCE a broader measure than the CPI.

So why does the Fed use PCE instead of the more widely cited Consumer Price Index (CPI)? Two differences matter:

Core PCE goes one step further by excluding food and energy prices entirely. Those categories are volatile, driven by weather, geopolitics, and commodity markets rather than underlying demand. Stripping them out gives the Fed a cleaner signal of where inflation is headed, not just where it is today.

An in-line print does three things simultaneously, and they pull in different directions.

Kevin Warsh’s confirmation in May 2026 landed at a moment when April CPI had already shocked markets with a +0.6% monthly print, and his early signals — including a preference for trimmed mean PCE over headline readings and a willingness to accelerate balance sheet runoff — shaped the cautious institutional posture the Fed carried into the May data release.

The gap that defines the constraint: Core PCE at 3.4% versus the Fed’s 2% target. That 140-basis-point difference is the clearest reason the central bank has to stay restrictive, and anyone expecting rate cuts in the near term should treat today’s data as evidence against that thesis, not support for it.

For bond and equity investors, the policy takeaway is stability rather than resolution. Today’s data keeps current rate expectations intact, which means volatility risk shifts forward to upcoming inflation releases rather than arriving today.

Today’s in-line print delivers reassurance rather than resolution. Inflation is not reaccelerating, but the Fed’s task is unfinished. The cumulative signal from four inputs over the remainder of 2026 will determine whether the current policy pause extends, hardens, or reverses.

Tracking these four indicators gives you an early read on whether the current policy pause extends or reverses before the year is out, and today’s calm PCE print is the baseline from which all of those subsequent readings will be judged.

For readers wanting to track how today’s PCE data feeds into the Fed’s most recent decision, our dedicated guide to Warsh’s June rate decision covers the FOMC hold at 3.75%, Warsh’s inaugural press conference signals, and how a pending US-Iran memorandum of understanding is shifting the energy inflation picture in real time.

May 2026 PCE confirms what the market suspected but needed the data to verify: inflation is easing gradually but remains too high for the Fed to declare progress complete or shift policy direction. The slight monthly softness in the headline was welcome, but part of that softness was borrowed from falling oil prices, a tailwind that could reverse.

The second half of 2026 is when the ambiguity resolves. If core PCE begins to drift toward 3% and the labour market cools, the Fed’s next move will be an easing cycle. If core stays sticky and crude rebounds, the holding pattern hardens. Today’s data keeps every option on the table, which is exactly the kind of non-event that carries more weight than it first appears.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

PCE (Personal Consumption Expenditures) is the Bureau of Economic Analysis's measure of prices across a broad basket of goods and services. The Fed prefers it over CPI because it captures a wider range of spending, including costs paid on behalf of consumers like employer-sponsored health insurance, and it adjusts for substitution effects when consumers shift spending in response to price changes.

Headline PCE rose 0.4% month-over-month and 4.1% year-over-year, while core PCE (excluding food and energy) gained 0.3% on the month and 3.4% on the year. All four readings matched or slightly undershot analyst consensus tracked by FactSet, removing any upside shock that could have forced a hawkish Fed reassessment.

The in-line result removes the immediate trigger for renewed rate hikes but gives no green light for cuts either. With core PCE at 3.4%, sitting 140 basis points above the Fed's 2% target, policymakers are locked into a cautious, data-dependent holding pattern and are unlikely to ease until core inflation shows a durable move toward 2%.

Cheaper crude lowered gasoline prices directly for consumers, reduced transport and freight costs, and compressed manufacturing input costs, all of which pulled the headline PCE reading below where it would have been under stable energy prices. This disinflationary effect is conditional: if oil prices reverse, all three channels flip to headwinds and the headline print will rise quickly.

The four key inputs are: June CPI and PCE releases (to confirm whether May's softness is a trend or a plateau), Fed communications (for tone shifts between inflation concern and growth concern), oil price direction (the variable that most directly shifts the headline print), and labour market reports (since persistent wage growth feeds services inflation, the stickiest component of core PCE).