Every major broker covering Commonwealth Bank of Australia (CBA) has a Sell rating. Not one Buy. Not one Hold. Fourteen analysts, zero reasons to buy, and yet CBA shares are up roughly 15.8% in 2026 including dividends, comfortably lapping the ASX 200, which sits approximately -0.4% on the year. The disconnect between what the market is paying and what professional analysts think CBA is worth has rarely been this wide.

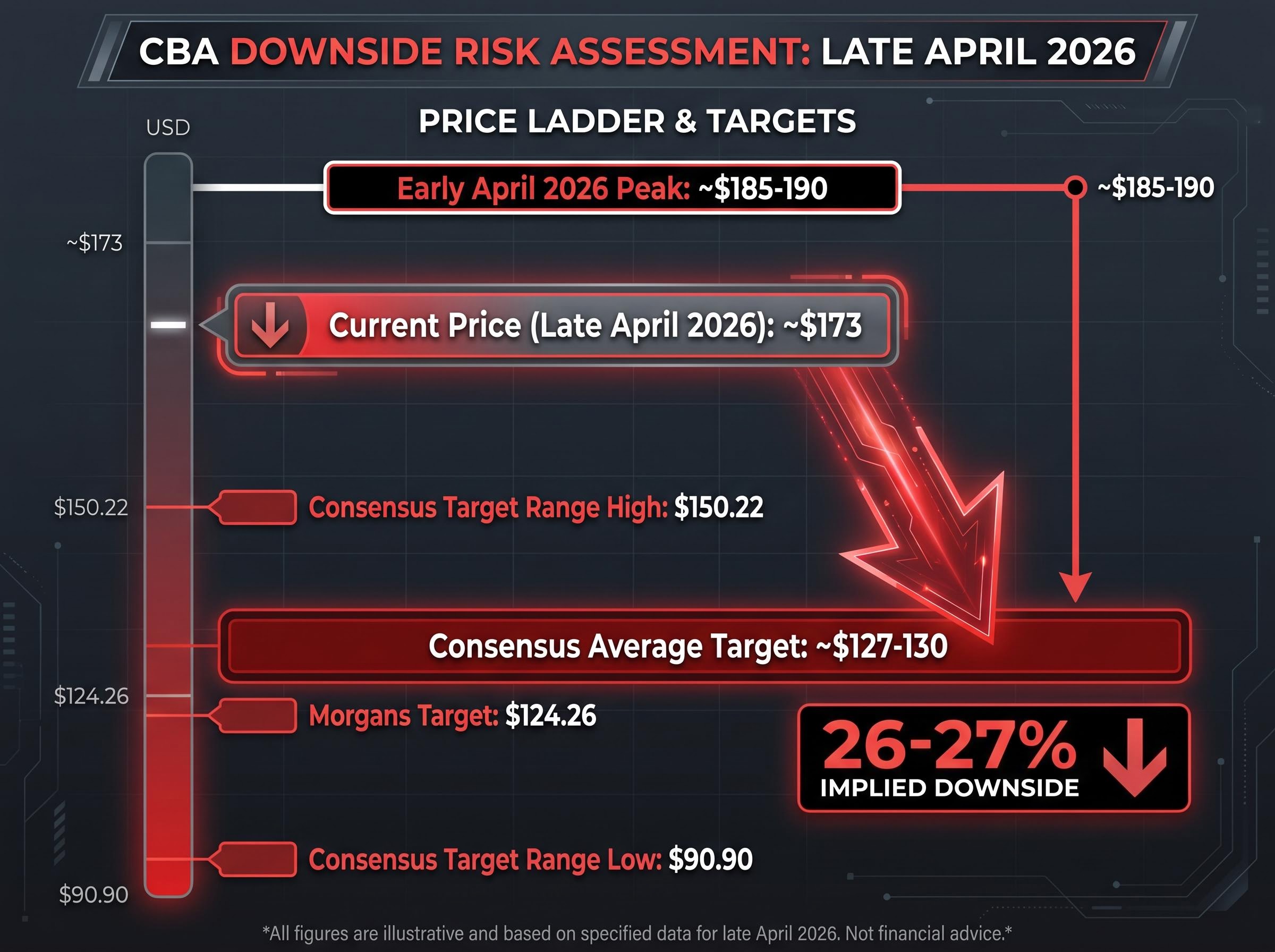

On 27 April 2026, Morgans analyst Damien Nguyen issued a Sell on CBA with a price target of $124.26, roughly 28% below where the stock was trading. His argument was not that CBA is a bad bank. It is that CBA is a great bank trading at a price that already assumes it stays great forever, leaving no room for anything to go wrong and very little room for the share price to compound meaningfully from here.

What follows is an examination of the Morgans case, the valuation gap between CBA and its Big Four peers, the specific headwinds that could compress that premium, and what investors weighing a position in CBA shares should be asking themselves before committing capital at these levels.

The number that explains everything: CBA at 28 times earnings

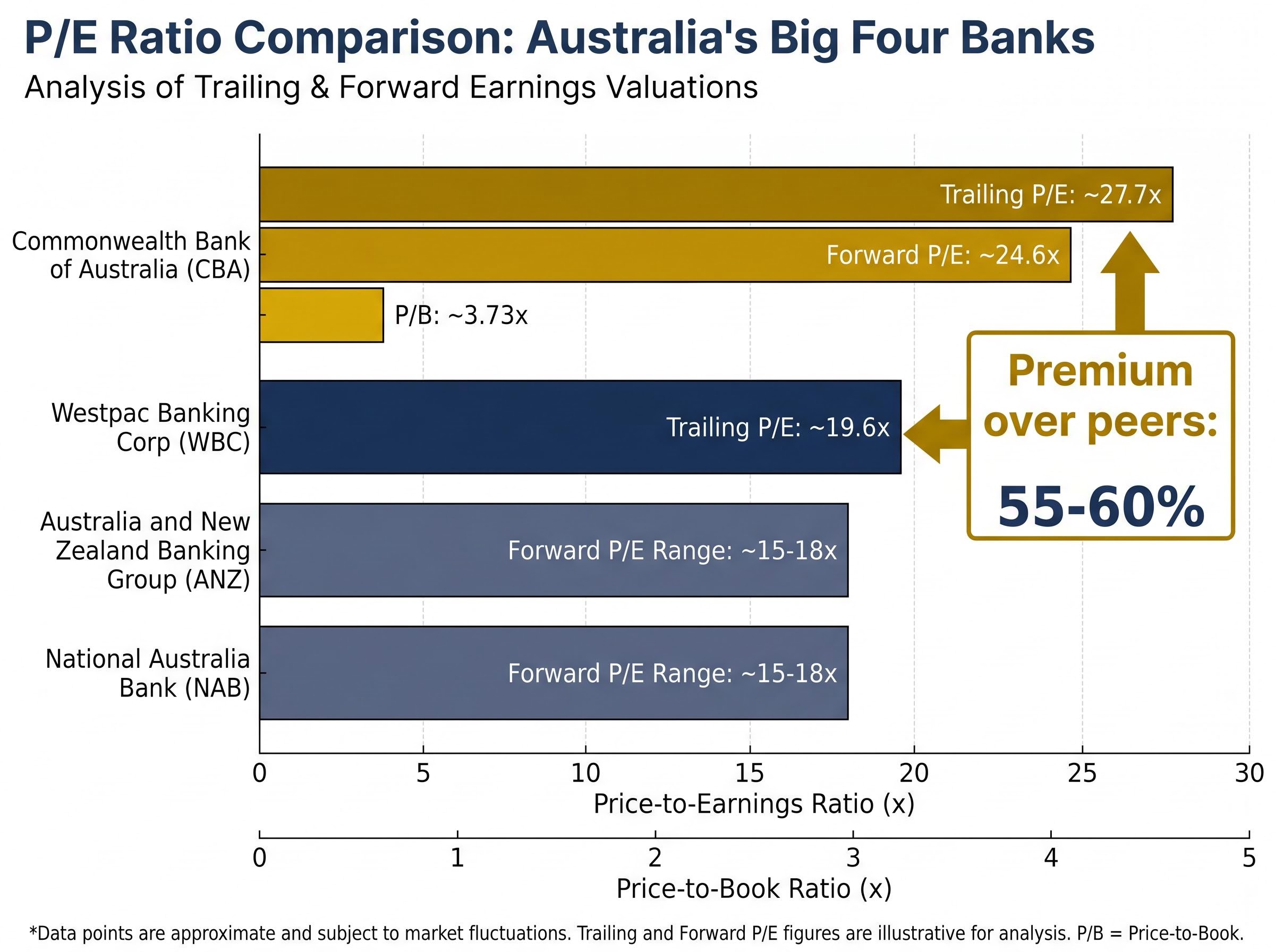

CBA trades at approximately 27.7x trailing earnings. That single number carries the full weight of the valuation debate, but it only becomes legible when placed beside the rest of Australia’s major banks.

Westpac trades at roughly 19.6x trailing earnings. ANZ and NAB sit around 15-18x on a forward basis. CBA’s premium over its closest peer is more than 55%. Over its cheapest peer, it approaches 60%.

| Bank | Trailing P/E | Forward P/E | Price-to-Book | Analyst Consensus |

|---|---|---|---|---|

| CBA | ~27.7x | ~24.6x | ~3.73x | Strong Sell (0 Buy, 0 Hold) |

| Westpac | ~19.6x | — | — | Sell |

| ANZ | — | ~15-18x | — | Trim (Morgans) |

| NAB | — | ~15-18x | — | Sell |

Paying a 55-60% premium over peers is only rational if CBA’s earnings growth will be meaningfully superior over time. The average analyst price target sits at approximately $127-130, implying roughly 26-27% downside from the late April price of $173.50.

Australian bank overvaluation is not confined to CBA; Morningstar’s analysis of the S&P/ASX 200 shows that the index’s modest 2026 year-to-date gain is almost entirely dependent on major bank performance, meaning a valuation re-rating across the sector would remove the index’s primary structural support and expose investors in domestic index funds to concentrated financial sector risk they may not have priced.

Morgans price target: $124.26, implying approximately 28% downside from CBA’s late April 2026 trading level. Analyst Damien Nguyen rates CBA a Sell, citing low single-digit earnings growth insufficient to justify the premium multiple.

That gap between where CBA trades and where analysts believe it belongs demands an explanation. It is not a rounding error.

When big ASX news breaks, our subscribers know first

What Morgans is actually arguing (and what it is not)

Nguyen’s Sell rating is not a call on CBA’s quality. It is a call on CBA’s price.

The distinction matters. CBA reported H1 FY26 cash net profit after tax (NPAT) of $5.45 billion, up approximately 2% year-on-year, and shares rose 6.8% on results day. By most operational measures, the result was solid. Morgans, however, described the half as “missing expectations” relative to what a 28x P/E implies. When a stock is priced for perfection, merely good results are a disappointment.

This is the concept of priced-in competitive advantage: when a stock’s valuation already reflects its moat, that moat stops generating returns for new buyers. CBA’s market leadership, its operational efficiency, its brand trust are all real. They are also already in the share price.

Morningstar’s Nathan Zaia described CBA as “materially overvalued” as recently as February 2026, noting that shares “remain materially overvalued” despite strong business fundamentals and recommending “better value elsewhere among Australian bank stocks.”

Nguyen’s position is not isolated. The broker consensus as of April 2026 shows 0 Buy ratings, 0 Hold ratings, and 9-14 Sell ratings across tracked brokers, with a price target range from approximately $90.90 to $150.22.

The three pillars of the Morgans bear case are:

- Valuation stretched beyond what earnings growth can justify

- CBA’s competitive advantages already priced into the current multiple

- Superior risk-adjusted alternatives available elsewhere in the sector

Why CBA commands a premium, and why that premium has limits

The bull case for CBA is not difficult to articulate, and it deserves its full due.

CBA holds dominant market share across Australian retail banking, mortgages, and deposits. Its AI-driven operational efficiency programme has been cited by multiple analysts as a medium-term earnings advantage. Brand trust, measured by customer retention and net promoter scores, sits above every domestic peer. And for Australian retail investors specifically, fully franked dividends carry real value: the franking credits attached to CBA’s payouts effectively boost the after-tax yield for domestic shareholders.

CBA’s Fitch credit rating upgrade to ‘AA’ in March 2026 underscored exactly the kind of institutional quality the bull case rests on, with Fitch citing earnings strength, balance sheet discipline, and a stable outlook that supports lower wholesale funding costs across international capital markets.

- Market leadership across retail banking and mortgages

- AI-driven efficiency gains supporting cost-to-income improvement

- Fully franked dividends providing enhanced after-tax yield for Australian residents

- Earnings resilience demonstrated in H1 FY26 despite broader pressures

CBA’s year-to-date 2026 total return sits at approximately 15.8%, including the $2.35 per share fully franked interim dividend paid 30 March 2026. The forward dividend yield is approximately 2.8% (full-year dividend of approximately $4.65 per share), with a payout ratio of roughly 78% considered sustainable.

A premium P/E is logically defensible for this kind of franchise. The question is where that premium tips from reasonable to speculative.

Where the premium becomes a problem

At 28x earnings, CBA needs to deliver earnings per share growth that justifies the entry price. Current consensus points to low single-digit EPS growth. The arithmetic is unfavourable: paying 28x for 2-3% growth means the stock needs the multiple itself to hold or expand for the investment to generate acceptable returns.

A price-to-book of 3.73x leaves limited buffer. If earnings disappoint, there is no margin of safety to absorb the re-rating. The franking credit value is real, but a 2.8% grossed-up yield does not close a 55-60% valuation gap over peers on its own.

The headwinds that could make the premium compress

The valuation debate moves from abstract to concrete when specific mechanisms come into view.

- Rate cycle fading: The RBA raised the cash rate to 4.10% on 17 March 2026, with forward estimates pointing to a peak of approximately 4.7-4.85% by mid-2026 via further 25bps moves expected in May, June, and August 2026. Higher rates have supported net interest margins, but that tailwind fades as the cycle peaks and eventually reverses.

- Competitive pressure narrowing: Peers are pursuing operational improvement programmes of their own. As Westpac, ANZ, and NAB close the efficiency gap with CBA, the premium the market pays for CBA’s operational edge narrows. Analyst commentary from Morgan Stanley and Citi references “self-help” stories at multiple competitors.

- Credit quality risk: As Australia’s largest home lender, CBA’s loan book carries concentrated exposure to mortgage stress. Analyst commentary has described “benign credit quality” as a partial offset to valuation concerns, but benign conditions may not persist if rate hikes continue to slow household spending and borrower serviceability.

APRA’s quarterly ADI statistics for the December 2025 period show Australian major banks carrying elevated residential mortgage concentrations, with asset quality metrics that analysts describe as benign but sensitive to further rate increases and slowing household income growth.

Morgan Stanley and Citi analysts have flagged CBA as “most vulnerable among the majors” due to its prior outperformance and higher multiples, noting that roughly 25% downside to fair value persists even after recent declines from peak levels.

These headwinds do not need to be catastrophic for CBA’s business. They only need to compress a 28x P/E toward the 20-24x range, which would represent a significant capital loss for investors who bought near record prices.

Relative value: what you get if you look at CBA’s peers instead

Relative valuation is one of the most practical tools available to investors comparing stocks within the same sector. At its simplest, the price-to-earnings (P/E) ratio measures how much an investor pays for each dollar of a company’s annual profit. A stock trading at 20x earnings is cheaper per dollar of profit than one at 28x, assuming earnings quality is comparable. Price-to-book compares the share price to the net asset value on the balance sheet, providing a measure of how much premium the market places on the business above its accounting value.

With that framework, the Big Four comparison becomes clearer.

| Bank | Approximate P/E | 2026 YTD Return | Dividend Yield | Morgans Rating |

|---|---|---|---|---|

| CBA | ~28x trailing | ~+15.8% (incl. dividends) | ~2.8% | Sell ($124.26) |

| Westpac | ~20x trailing | ~+13% | Higher relative to price | Sell |

| ANZ | ~15-18x forward | ~+4.5% | Higher relative to price | Trim |

| NAB | ~15-18x forward | Mixed | Higher relative to price | Sell ($31.46) |

Morgans issued Sell ratings across the Big Four, but with materially different implied downside. ANZ received a milder “Trim” rather than an outright Sell, indicating a spectrum of risk even within the sector. Morningstar’s Nathan Zaia has pointed to “better value elsewhere among Australian bank stocks” as the practical conclusion.

Relative valuation does not indicate that peers are strong buys. It does clarify what investors give up by concentrating in CBA at its current premium:

Investors comparing value across the domestic banking sector have concrete alternatives to consider; Bank of Queensland’s capital return and restructuring, anchored by a $3.7 billion asset sale to Challenger and an 11% dividend increase in 1H26, represents the kind of self-help story that can drive re-rating from a lower valuation base precisely when premium-multiple stocks like CBA are most exposed.

- Is the P/E premium justified by proportionally higher earnings growth?

- Does CBA’s dividend yield, after franking, compensate for the valuation gap?

- What is the margin of safety at each bank’s current price if conditions deteriorate?

- Where is earnings growth most likely to surprise on the upside over the next 12 months?

The quality trap: why being the best bank does not make CBA the best buy right now

CBA is the best-run major bank in Australia by most operational measures. That quality is precisely why the market has bid the stock to a level where future returns are likely constrained even if everything goes right.

This is the tension the entire Morgans case rests on. A $173 share price already compensates investors for CBA’s dominant position, its efficiency, its brand, and its dividend reliability. What it does not compensate them for is any future disappointment, however minor.

The bear case could weaken under specific conditions:

- CBA delivers earnings materially above the low single-digit growth currently projected

- Rate tailwinds persist longer than modelled, sustaining net interest margins above consensus

- New growth catalysts, such as AI efficiency gains, deliver ahead of schedule and expand the earnings trajectory

CBA’s share price as of 29 April 2026 sat at approximately $172.29 intraday, down from a historical peak of approximately $185-190 reached in early April 2026. The stock remains roughly 6-9% off peak, yet the consensus price target range of $90.90 to $150.22 (average approximately $127-130) implies the pullback has barely begun if analyst models prove correct.

Morgans’ Damien Nguyen has pointed to “superior value opportunities elsewhere” as the practical conclusion for investors evaluating CBA at current levels.

The quality trap is the most common way retail investors destroy value in strong companies: paying for quality twice, once in the business fundamentals and once in the valuation multiple, with no room left for the investment itself to compound meaningfully.

What should actually drive your decision on CBA shares right now

The question is not whether CBA is a good company. It is whether the current price offers an adequate return for the capital deployed.

That distinction turns the decision into a structured evaluation rather than a sentiment call. Before buying, holding, or trimming CBA at these levels, the following checklist captures the variables that matter:

- Entry price versus analyst targets: CBA trades at approximately $173, against a consensus target of $127-130 and 14 Sell ratings with 0 Buy or Hold. Implied downside sits at 26-27%.

- Income need versus growth expectation: A fully franked yield of approximately 2.8% serves income-focused portfolios, but does not offset a potential 26-27% capital loss.

- Time horizon: A 20-year holder may ride through a re-rating. A 3-year holder may not recover entry cost in that window.

- Portfolio concentration: Overweighting a single bank at a premium valuation amplifies sector-specific risk.

- Specific disagreement with consensus: Ignoring 14 Sell ratings requires an articulated reason to believe the consensus is wrong, not simply admiration for the business.

If you already hold CBA shares

The Morgans case supports reducing exposure. A trim, rather than an exit, acknowledges CBA’s income value while adjusting position size to reflect the valuation risk. Tax implications and reliance on franked income may argue for holding with eyes open, but the analytical case for maintaining a full-weight position has weakened materially.

If you are considering buying CBA shares for the first time

A buyer at $173 needs to believe CBA will sustain earnings outperformance above what peers deliver, that the premium P/E will hold rather than compress, and that the operational moat will widen rather than narrow as competitors execute their own efficiency programmes. Fourteen analyst Sell ratings suggest the probability-weighted outcome is less favourable than the share price implies.

CBA is a great bank. That is no longer enough to make it a great buy.

Quality and value are different dimensions of the same investment decision, and CBA scores highly on one while scoring poorly on the other at current prices. The business remains Australia’s strongest retail banking franchise. The share price, however, has moved well beyond what that franchise can justify on current earnings and growth projections.

What would change the outlook is specific: a material earnings beat in H2 FY26, a significant price pullback toward the $130-150 range, or new catalysts that genuinely justify premium expansion. Until one of those conditions materialises, the gap between CBA’s quality and its valuation remains the defining feature of this stock.

Investors holding or considering CBA would benefit from checking whether their position size reflects conviction on both business quality and valuation, not just the former. The H2 FY26 results and any RBA rate decision surprises in the months ahead are the two triggers most likely to shift the balance of probability.

For investors who have worked through the valuation case and want a framework for acting on it, our comprehensive walkthrough of ASX portfolio positioning during inflation covers how to allocate across cash ETFs, quality equity exposures, and fixed income instruments in a tightening cycle, with specific attention to the risks of reactive decision-making when CPI headlines are elevated.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—