Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

5 hrs ago

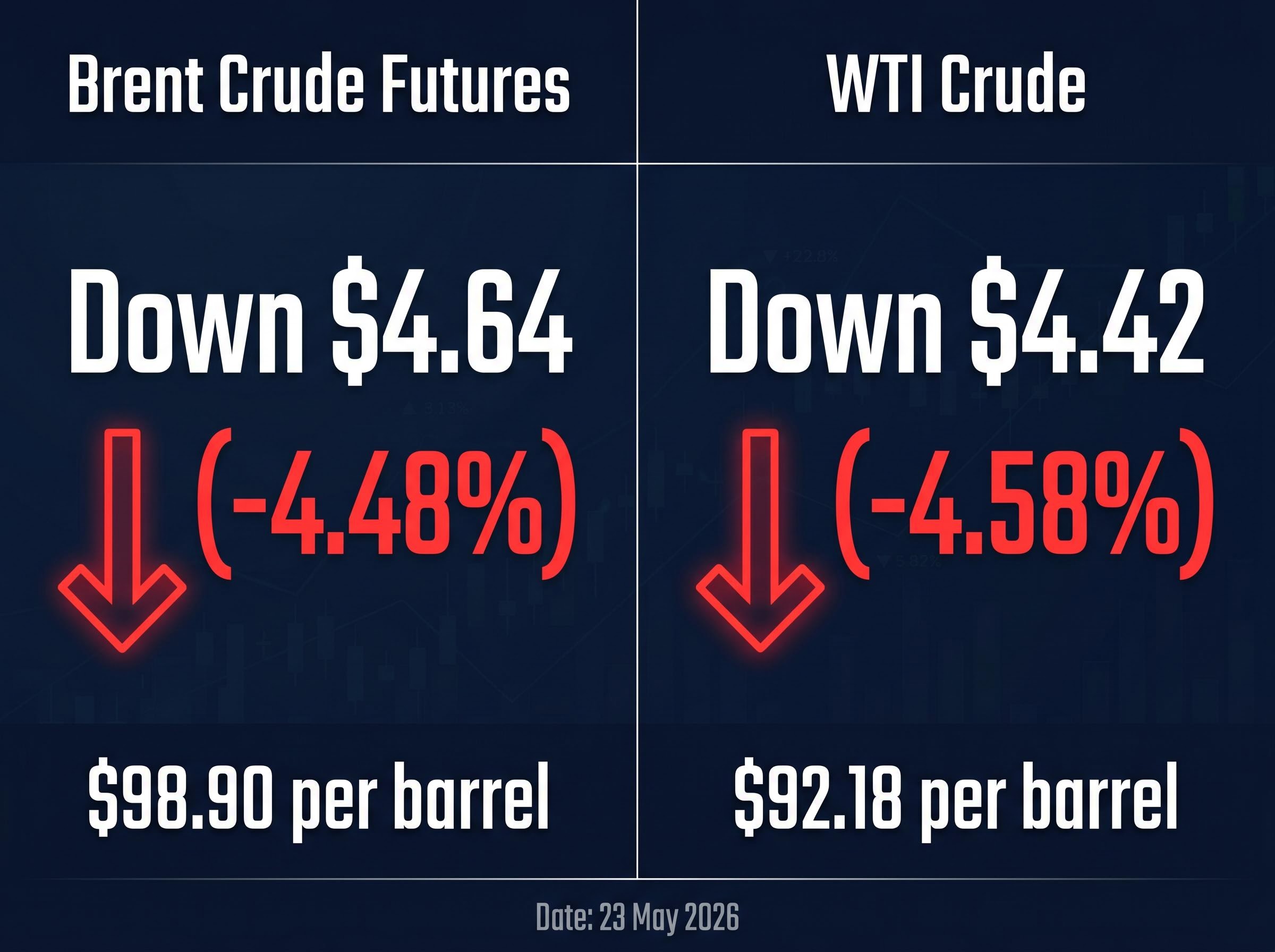

Brent crude fell $4.64 in a single session on 23 May 2026, a 4.48% drop to $98.90 per barrel, as hopes for a US-Iran nuclear agreement collapsed and fears over Middle East shipping risk surged back to the surface. The selloff represents more than one day of poor headlines. It captures a market forced to reprice the probability of a diplomatic resolution that traders had partially baked into oil prices over the preceding weeks. With the Strait of Hormuz handling roughly a fifth of the world’s seaborne crude, any signal of prolonged tensions carries outsized consequences for global supply chains.

What follows explains what broke down in the negotiations, why the Strait of Hormuz matters so much to energy pricing, what cross-asset signals reveal about how markets are interpreting the risk, and what leading analysts see ahead for crude under this geopolitical overhang.

The numbers landed hard. Both global crude benchmarks posted their largest single-session declines in months:

A move of that magnitude in a single session signals how much speculative optimism had already been built into the price. The proximate trigger was a statement from President Trump indicating Washington would not be rushed into finalising an agreement he described as not yet fully negotiated.

“Washington will not be rushed into a bad deal. No agreement is better than a weak agreement.” — President Trump, 24 May 2026

The implication was immediate. Traders who had positioned for a deal, one that would have eased sanctions on Iranian oil exports and structurally increased global supply, began unwinding those positions. Analysts at S&P Global Commodity Insights characterised the selloff as “a paring back of speculative length rather than a reassessment of long-term supply tightness.” The distinction matters: the market did not decide oil is less scarce. It decided a deal is less likely.

The deal premium built into crude was most visible on 7 May 2026, when Brent fell approximately 7.6% in a single session after reports of a US-Iran framework emerged, dropping from $116.55 to $101.88 per barrel and simultaneously driving a 7.73% surge in the Gold Miners ETF as falling Treasury yields triggered a broad commodity rotation outside energy.

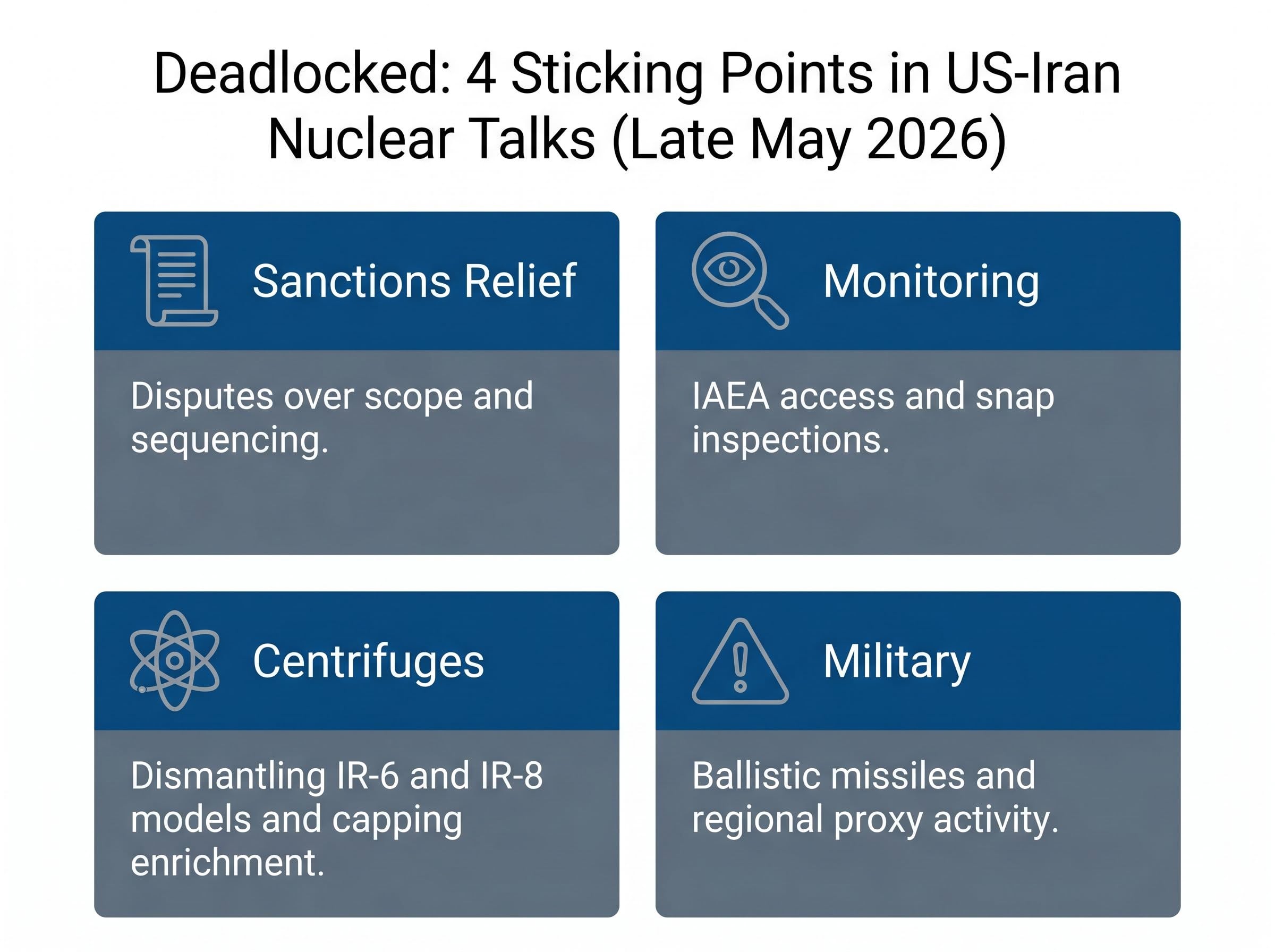

Negotiations between Washington and Tehran stalled on four structural disputes, each of which involves a genuine conflict of interest rather than a procedural delay. Understanding what is unresolved tells investors how far the market remains from the scenario, a signed deal and sanctions relief on Iranian oil exports, that would structurally reprice crude lower.

The four sticking points, as reported by Reuters, the Financial Times, and the Wall Street Journal in late May 2026:

Negotiators remain in contact, but no signing date has been set. The talks are described as “deadlocked” as of late May 2026. Each of these four disputes involves a dimension where the two sides’ core positions are structurally opposed, not simply unfinished. That is why the impasse feels earned, and why traders moved so aggressively to unwind their deal premium.

The Strait of Hormuz is a narrow waterway between Iran and Oman, roughly 33 kilometres wide at its narrowest navigable point. Approximately one-fifth of the world’s seaborne crude transits through it daily. There is no practical alternative route for most of that volume; pipelines that bypass the strait carry a fraction of what the tankers move, and they cannot be scaled quickly.

That geography is why Helima Croft, head of global commodity strategy at RBC Capital Markets, has described the strait as the “single most critical chokepoint in the global oil market,” noting that “risk premia can expand rapidly on any sign of Iranian interference with shipping.”

In recent weeks, several incidents have elevated the perceived threat without triggering an actual disruption to flows:

| Incident | Date | Source | Market Interpretation |

|---|---|---|---|

| Revolutionary Guard naval drills near Hormuz (missile and drone launches) | 21 May 2026 | Reuters | Signal of capability and intent; heightened risk perception |

| US Navy near-miss (Iranian fast boats made “unsafe and unprofessional manoeuvres”) | 22 May 2026 | Associated Press | Elevated military tension; miscalculation risk |

| Maritime security advisories for vessels transiting the strait | 23 May 2026 | Lloyd’s List | Insurance cost increases; potential route delays |

Physical flows remained broadly uninterrupted as of late May 2026. The IEA confirmed in its May 2026 Oil Market Report that there had been “no major disruption to physical supply flows.” The price drop, then, was about repricing risk rather than responding to an actual supply cut.

“Even a temporary disruption of Hormuz exports would be a shock far greater than any single OPEC+ decision.” — Amrita Sen, co-founder and head of research, Energy Aspects

That asymmetry, between the probability of disruption and its potential magnitude, is what keeps the geopolitical premium embedded in every barrel.

The Hormuz risk premium does not simply dissolve when physical flows are uninterrupted; VLCC daily hire rates tracking near $110,000 per day and the near-total withdrawal of commercial war-risk insurance suggest the market is pricing a structural elevation rather than a temporary spike, with the IEA projecting a two-year recovery timeline even under a best-case resolution.

The crude selloff did not happen in isolation. Across equities, safe havens, and fixed income, the Friday 23 May session produced a coherent risk-off signal. Each asset class moved in the direction consistent with a single underlying anxiety: rising geopolitical risk and retreating growth confidence.

The cross-asset transmission from Iran talks follows a consistent sequential pattern: energy price moves arrive first, long-duration bond yields reprice as inflation expectations shift, and rate-sensitive equity sectors react last, a sequence that played out with particular clarity in mid-May 2026 when 30-year Treasury yields retreated from 19-year highs in a single session.

| Asset | Friday Move | Monday Move |

|---|---|---|

| Brent crude | Down 4.48% to $98.90 | Session data pending |

| S&P 500 | Down 0.7% | Up 0.3% |

| Gold | Up approx. 0.9% to ~$2,420/oz | Little changed |

| Silver | Up approx. 1.6% | Data pending |

| US 10-year Treasury yield | Down ~4 bps to ~3.95% | Up 2 bps to 3.97% |

Monday’s partial reversal, the S&P 500 up 0.3%, the Nasdaq up 0.5%, the 10-year yield recovering 2 basis points, was technical in character rather than a genuine shift in sentiment. Gold held its gains rather than giving them back, and equities recovered only a fraction of Friday’s decline.

“The geopolitical premium is likely to remain sticky as long as U.S.-Iran tensions stay elevated.” — Bob McNally, president, Rapidan Energy Group

That stickiness is the signal. When gold holds, yields stay low, and equities only partially bounce, the market is telling investors it has not moved past the risk. It has absorbed one session of it and is waiting for the next headline.

The spectrum of institutional views ranges from contained volatility to historic disruption. That spread itself is the story: no consensus exists, which is precisely why crude remains difficult to price with conviction.

The IEA, EIA, and J.P. Morgan positions converge on a shared assumption: physical flows continue, OPEC+ spare capacity provides a structural buffer, and prices trade within a volatile but bounded range. The geopolitical risk premium is acknowledged as justified but is not expected to produce a sustained breakout absent an actual supply curtailment.

Goldman Sachs and Ed Morse at Citigroup occupy the other end of the distribution. No major institution is treating a Hormuz closure as a base case. But Morse warned that “any attack on tankers or key export infrastructure could change the balance of risks overnight.” The asymmetry of the tail risk, low probability, extreme magnitude, is what keeps the premium alive even when physical flows continue unimpeded.

For investors wanting to map each institutional projection to specific Hormuz reopening timelines, our dedicated guide to oil price forecast scenarios covers the Goldman Sachs $110-$142 range, the EIA reopening baseline, and the probability weights Goldman assigns to normalisation by mid-June, with worked comparisons across the base case and prolonged closure outcomes.

The oil price drop on 23 May 2026 is a rational repricing. Traders had built a deal premium into crude on the assumption that negotiations were progressing toward sanctions relief on Iranian oil exports. That assumption collapsed when the specific sticking points, centrifuge caps, inspection access, sanctions sequencing, ballistic missiles, proved too structurally difficult for a near-term resolution.

The alternative to a deal is not stability. It is heightened confrontation in and around the Strait of Hormuz, where the Iranian Revolutionary Guard and the US Navy are already exchanging provocative manoeuvres. Amrita Sen at Energy Aspects captured the tension precisely: the market is “oscillating between relief over uninterrupted Hormuz flows and anxiety over miscalculation in the Gulf.”

Brent closed at $98.90. The centrifuge and sanctions-sequencing disputes are the proximate indicators to watch. Movement on either would signal whether talks are heading toward resolution or deeper deadlock.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments.

Crude oil prices fell sharply because hopes for a US-Iran nuclear deal collapsed after President Trump signalled Washington would not rush into an agreement, prompting traders to unwind speculative positions that had priced in sanctions relief on Iranian oil exports.

The Strait of Hormuz is a narrow waterway between Iran and Oman, roughly 33 kilometres wide at its narrowest navigable point, through which approximately one-fifth of the world's seaborne crude passes daily, making it the single most critical chokepoint for global oil supply.

The four unresolved disputes are: the scope and sequencing of sanctions relief, monitoring and inspection access for the IAEA, the dismantlement of advanced centrifuges and enrichment caps, and whether Iran's ballistic missile programme and regional proxy activity should be included in the nuclear agreement.

The selloff triggered a broad risk-off move: the S&P 500 fell 0.7%, gold rose approximately 0.9% to around $2,420 per ounce, silver gained around 1.6%, and the US 10-year Treasury yield dropped roughly 4 basis points to approximately 3.95%.

Major institutions including the IEA, EIA, and J.P. Morgan expect crude to trade in a volatile but bounded range with no sustained breakout as long as physical flows remain uninterrupted, while Goldman Sachs and Citigroup warn that any actual disruption to the Strait of Hormuz could produce an extreme upside price shock.