US Inflation Hits 4.2% but Core Data Tell a Calmer Story

1 hr ago

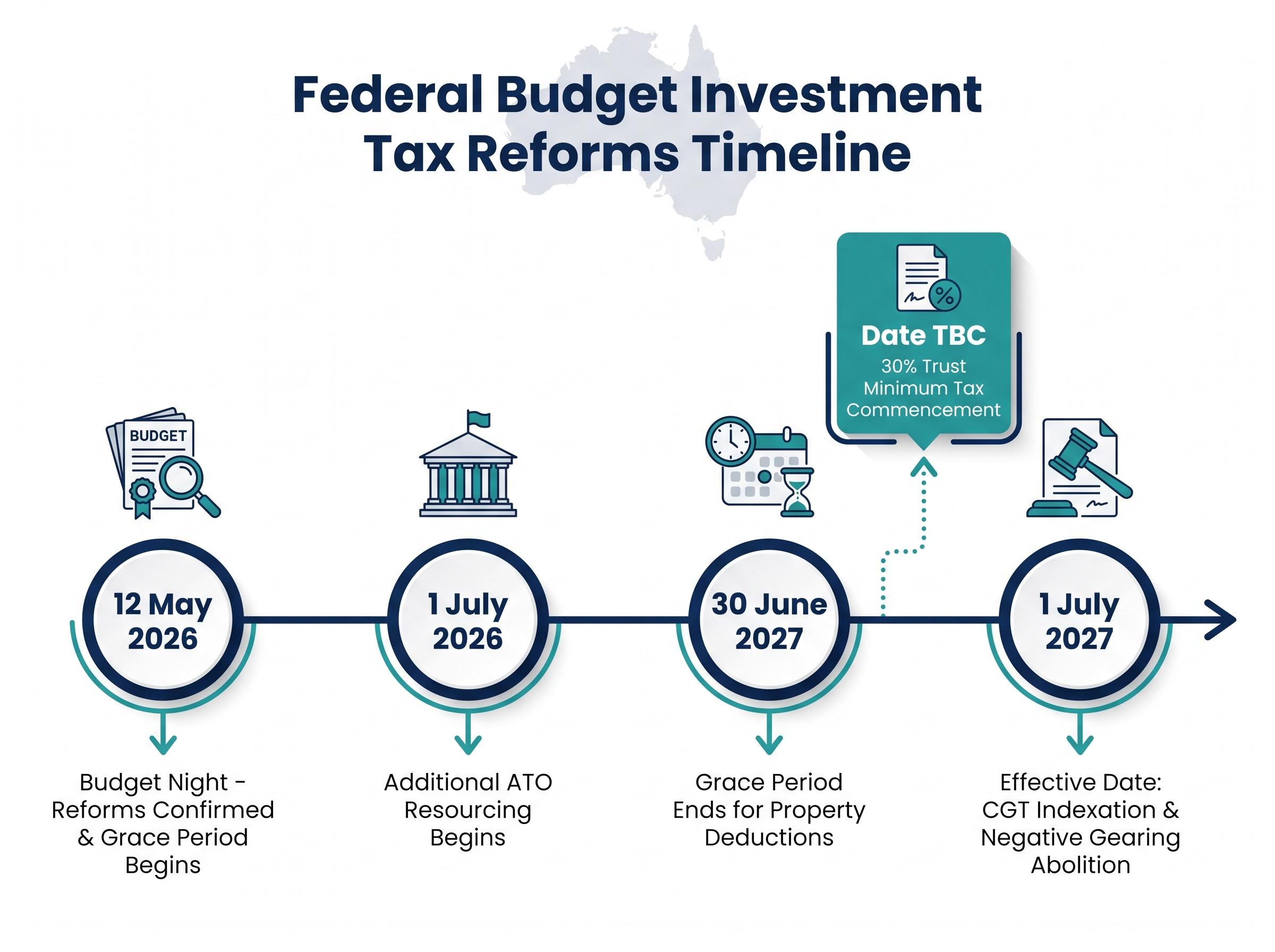

Three of the most significant investment tax changes in a generation were confirmed on a single budget night. On 12 May 2026, the Federal Budget replaced the 50% capital gains tax (CGT) discount with inflation indexation, abolished negative gearing for new investments, and introduced a 30% minimum tax on discretionary trust distributions to adult beneficiaries. The rules governing capital gains, rental property deductions, and family trust distributions are not what they were yesterday.

All three reforms target structures used by everyday Australian investors, property owners, and self-managed super fund (SMSF) trustees. Finance Minister Katy Gallagher has framed the package around housing affordability, intergenerational equity, and reducing tax minimisation through income-splitting arrangements.

What follows breaks down each reform in plain language: what changed, who is affected, what the grandfathering provisions mean in practice, and what questions investors should be asking before the detail is finalised.

The three measures are distinct policies, but they share a single underlying logic: reducing the tax advantage of passive investment income relative to labour income. That shared architecture is not accidental. Housing affordability researchers and Treasury modellers have advocated for this combination for years, and the 12 May budget confirmed that the government has accepted the direction.

Finance Minister Katy Gallagher stated that the reforms are intended to address housing affordability, support intergenerational equity, and respond to the reality that young Australians are increasingly locked out of the housing market.

As recently as 30 January 2026, the Tax Institute noted uncertainty about whether announced-but-unenacted measures would proceed. The budget has now resolved that ambiguity. The three confirmed reforms, summarised:

Understanding the shared logic behind these reforms helps investors anticipate where future policy may develop, and why each individual change is unlikely to be reversed in isolation.

The superannuation tax advantage over personal investment has widened materially under the new settings: with personal investors facing a 30% minimum CGT floor and the end of negative gearing on new properties, the 10% effective CGT rate inside accumulation-phase super and the 0% rate in pension phase represent a structural gap that portfolio planning decisions will need to account for.

Most Australian investors are familiar with the existing 50% CGT discount. For any asset held longer than 12 months, half the nominal capital gain is excluded from taxable income. That structure is being replaced.

Under the new approach, effective 1 July 2027, the cost base of an asset is adjusted upward for inflation. Only the real gain above that adjusted base is taxable. The change applies to all asset classes, not just residential property.

The distinction matters most in two scenarios. For assets where inflation drove most of the nominal gain (a property that barely kept pace with CPI, for instance), the new method may result in a lower taxable amount than the old 50% discount. For assets with strong real capital growth well above inflation, the taxable gain under indexation may be similar to or higher than under the current rules.

CPA Australia has warned that the shift from a flat discount to indexation will add significant compliance complexity, as investors and their advisers will need to calculate inflation-adjusted cost bases rather than applying a simple percentage reduction.

The investor cost of the CGT overhaul becomes concrete when modelled against specific asset disposals: Stockspot analysis estimates a business founder selling a $1 million company could lose more than $225,000 in after-tax proceeds under the new regime compared with the current 50% discount rules.

| Scenario | Nominal Gain | Taxable Gain (Current 50%) | Taxable Gain (Indexation) | Outcome |

|---|---|---|---|---|

| Gain driven mainly by inflation | $200,000 | $100,000 | Lower (e.g. $60,000 if most gain was inflation) | Investor pays less tax under new rules |

| Gain driven mainly by real growth | $200,000 | $100,000 | Higher (e.g. $140,000 if inflation was modest) | Investor pays more tax under new rules |

Assets acquired before the effective date remain subject to the existing 50% discount rules when sold, regardless of when that sale occurs. No confirmed exemptions for new-build properties have been announced. Investors should monitor Treasury.gov.au for any carve-outs that may appear in the exposure draft.

For long-term investors holding shares or property purchased well before 2027, no immediate action is required.

The first point to clarify: this is not a blanket abolition of negative gearing. Existing negatively geared properties retain full deductibility indefinitely under grandfathering provisions. The change applies only to new investments.

The timing mechanics are where precision matters. Properties acquired after budget night (12 May 2026) but before 1 July 2027 fall within a one-year grace period. Investors can utilise negative gearing deductions on those properties only until 30 June 2027. From 1 July 2027, the deduction ceases for those properties. The abolition is full, not capped at a second property.

The SMSF Association has flagged that self-managed super funds acquiring direct property after the effective date will also lose access to negative gearing deductions, a consideration for trustees planning direct property acquisitions within their fund.

Pre-budget projections from CommBank estimated full abolition with grandfathering at approximately $2 billion over four years and $20 billion over 10 years. These figures are indicative pre-budget modelling, not confirmed Treasury costings.

The Real Estate Institute of Australia (REIA) estimates the combined CGT and negative gearing changes could apply 1-4% downward pressure on property prices. This is an industry projection rather than confirmed Treasury or independent modelling.

Three categories of investor face distinct treatment:

The grace period offers a narrow window, but investors making new purchases within it should recognise that the property becomes neutral or positively geared from the effective date.

Discretionary trusts have historically allowed families and business owners to distribute income to adult beneficiaries on lower marginal tax rates. A trust earning $200,000 could, for example, distribute portions to adult children or a spouse in lower tax brackets, reducing the overall family tax burden. The practice is legal, widely used, and has been a feature of Australian tax planning for decades.

The 2026-27 budget targets that structure directly. A 30% minimum tax rate will apply to distributions from discretionary trusts to adult beneficiaries, regardless of the beneficiary’s personal marginal rate. An adult beneficiary who would otherwise pay 19% or 0% on their share of trust income will now face a minimum 30% rate on those distributions.

Expert commentary reported by SmartCompany described the measure as a significant policy reversal that will materially affect family business succession and income planning structures.

The following groups face the most direct impact:

The full mechanics remain pending. Outstanding items include:

Authoritative updates will be available via Treasury.gov.au and ATO.gov.au as fact sheets and administrative guidance are released in the weeks following 12 May.

This section provides a quick-reference summary for readers encountering these reforms for the first time or looking to confirm where they stand.

Most investors will fall into one of four categories. The majority of those with established portfolios are protected by grandfathering provisions. The table below maps each investor type against the three reforms.

| Investor Type | CGT Impact | Negative Gearing Impact | Trust Tax Impact | Action Required |

|---|---|---|---|---|

| Share investor (existing portfolio) | None; existing assets grandfathered under 50% discount | Not applicable | Only if receiving trust distributions | Monitor for new acquisitions post-July 2027 |

| Property investor (existing negatively geared property) | None; existing assets grandfathered | None; full deductibility continues | Only if property held via trust | No immediate action required |

| Investor considering new property purchase | Indexation applies to assets acquired post-July 2027 | Grace period ends 30 June 2027; no deduction after | Only if purchasing via trust | Seek professional advice before purchasing |

| Discretionary trust trustee or beneficiary | Indexation applies to new trust-held assets post-July 2027 | Applies if trust acquires new property | 30% minimum rate; timing TBC | Review distribution strategy with tax adviser |

Grandfathering is confirmed for CGT and negative gearing. For the trust minimum tax, grandfathering status remains unconfirmed pending legislation. Effective dates are 1 July 2027 for CGT and negative gearing; to be confirmed for the trust measure.

Not all investment structures are equally exposed: passive ETFs, ASX-listed REITs, and superannuation are among the investment structures better positioned under the new tax settings, while leveraged residential property and high-turnover managed funds face the steepest combined impact from the CGT and negative gearing changes.

Professional advice from a qualified tax adviser or financial planner is strongly recommended for individual circumstances, particularly given the volume of legislative detail still pending. The ATO is expected to publish administrative guidance and Q&A documents via ATO.gov.au in the weeks following the budget.

Much of the legislative detail remains outstanding. The most useful near-term action is to identify which of the four investor categories applies to an individual’s situation: grandfathered, directly affected, or potentially affected by the trust changes.

The period between budget night and the 1 July 2027 effective date is a planning window. Investors who restructure based on partial information before exposure drafts are released risk acting unnecessarily. Those who wait passively may miss the implications of the grace period for new property acquisitions.

Five milestones to monitor in the months ahead:

Additional ATO resourcing from 1 July 2026 is expected to support administration of the new measures. Key sources to bookmark include budget.gov.au, Treasury.gov.au, ATO.gov.au, the SMSF Association, CPA Australia, and the Tax Institute.

Investors in affected categories, particularly those considering property acquisition within the grace period or those with discretionary trust distribution strategies, should consult a tax professional before the legislation is finalised.

Investors exploring how to adapt their share portfolios to the new regime will find our full explainer on CGT changes and ETF portfolio structure, which covers low-turnover fund selection, buy-only rebalancing strategies, and the widened CGT gap between superannuation and personal ownership that now runs to 20 percentage points.

The 2026-27 Federal Budget confirmed three directions: inflation indexation replacing the CGT discount, the end of negative gearing for new investments, and a 30% minimum tax on trust distributions. All three are now policy. None is yet fully legislated.

For the majority of existing investors with established portfolios, grandfathering provisions mean immediate restructuring is not required. That said, passive assumptions that current arrangements will continue to apply indefinitely are not warranted either, particularly for trust structures where the commencement date and exemptions remain unconfirmed.

The months between 12 May 2026 and the 1 July 2027 effective date are the window in which the real tax planning decisions will be made. The detail released via Treasury and the ATO will determine how much of the headline change translates into personal tax obligation. Authoritative updates will be published at budget.gov.au, Treasury.gov.au, and ATO.gov.au as legislation progresses.

The budget.gov.au 2026-27 Budget Papers provide the primary official source for the confirmed policy parameters across all three reforms, including the revenue assumptions underpinning the CGT indexation switch and the negative gearing abolition.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future policy implementation are subject to change based on legislative developments and government decisions.

The 2026-27 Federal Budget confirmed three major reforms: replacing the 50% CGT discount with inflation indexation, abolishing negative gearing for new property investments, and introducing a 30% minimum tax on discretionary trust distributions to adult beneficiaries. All three measures take effect from 1 July 2027, except the trust tax whose commencement date is still pending legislation.

No. Existing negatively geared properties are fully grandfathered, meaning current deductibility continues indefinitely regardless of when you sell. The abolition applies only to new property investments acquired after budget night on 12 May 2026, with a grace period allowing negative gearing deductions until 30 June 2027 for properties bought before that date.

From 1 July 2027, instead of excluding 50% of a nominal capital gain from taxable income, the cost base of an asset is adjusted upward for inflation so that only the real gain above that adjusted base is taxed. Investors holding assets with gains driven mainly by real growth may pay more tax under the new system, while those whose gains were mostly inflation-driven could pay less.

The 30% minimum rate applies to distributions from discretionary trusts to adult beneficiaries, regardless of the beneficiary's personal marginal tax rate. Family trust trustees, adult beneficiaries currently receiving distributions taxed at lower rates, family business owners using trusts for succession planning, and SMSF trustees using trust structures are among those most directly affected.

Investors should first identify which category applies to their situation: grandfathered, directly affected by the negative gearing grace period, or potentially affected by the trust minimum tax. Those considering new property acquisitions or running discretionary trust distribution strategies should seek professional tax advice before exposure drafts are released via Treasury.gov.au and ATO.gov.au, as acting on incomplete information carries its own risks.