What 4 Wall Street Firms See Driving Markets in H2 2026

19 mins ago

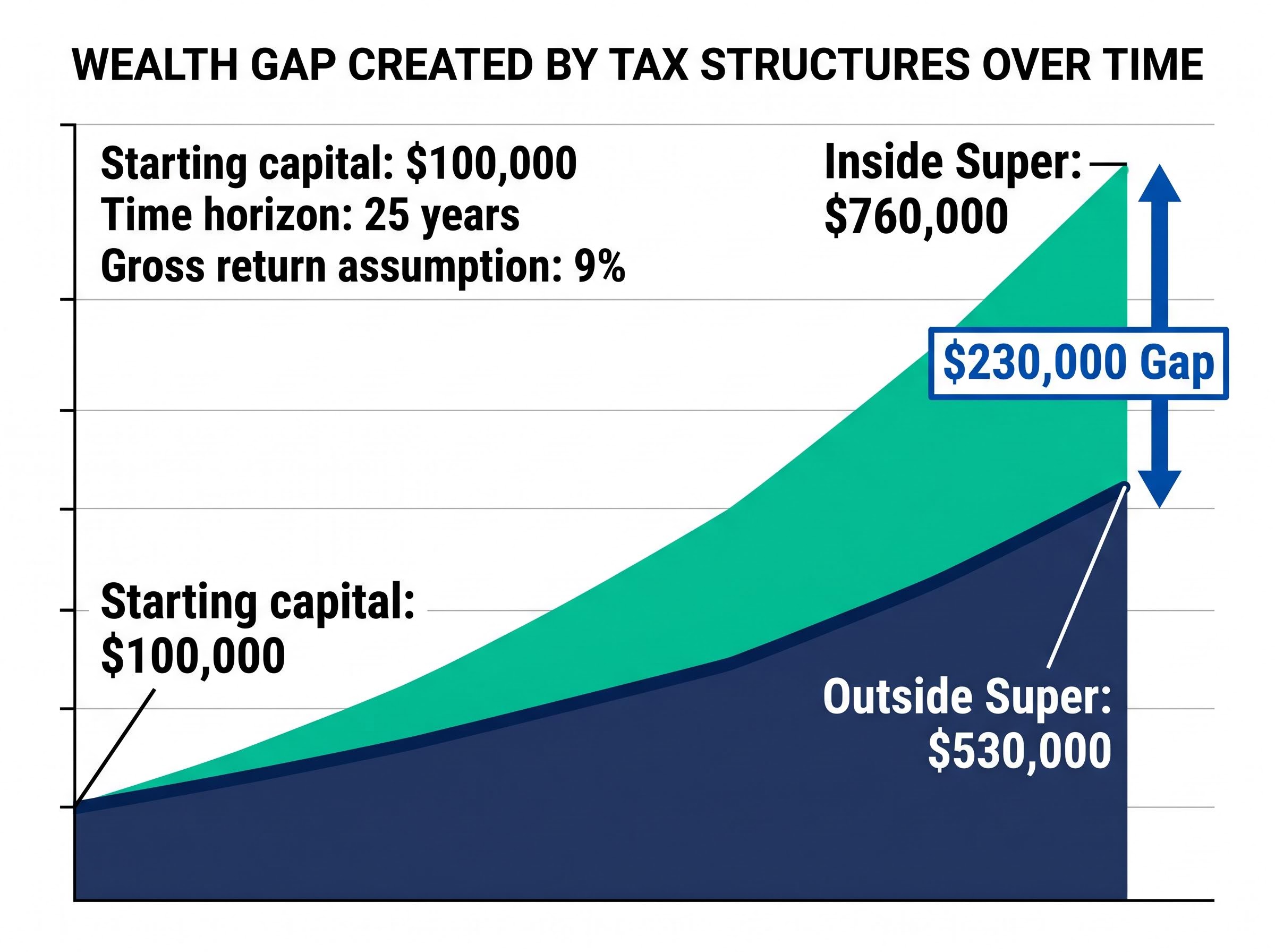

A 35-year-old Australian investor who places $100,000 into a low-cost ASX 200 index fund outside superannuation and another $100,000 into super, holding both for 25 years at the same gross return, does not end up with the same balance. The gap is roughly $230,000, and the market had nothing to do with it. The investment performance is identical. The tax wrapper is the entire difference.

For mid-career Australians, the instinct to pursue higher returns through direct share investing is understandable but routinely miscalculated. The comparison between superannuation and shares almost always focuses on gross returns and ignores the tax structure, which is where the real compounding divergence occurs. With voluntary concessional contributions growing sharply through FY2025 and financial planners consistently prioritising super for clients aged 30 to 50, this question has moved from theoretical to urgently practical. What follows unpacks exactly why the tax treatment of superannuation, not its investment performance, is the primary wealth-building lever for mid-career investors, and lays out the conditions under which each approach wins.

Consider an investor earning $150,000 per year. Every dollar of investment income earned outside super is taxed at 37%, plus the 2% Medicare levy. The same dollar earned inside a super fund is taxed at a flat 15%. That is not a rounding error. It is a 24 percentage point gap on every dollar, every year.

The asymmetry begins before the money even starts compounding. Concessional contributions (including salary sacrifice) are taxed at 15% on entry into super. For someone on the 37% marginal rate, that represents an immediate 22 percentage point saving compared to receiving the same income as salary. For those on the top 45% rate, the saving widens to 30 percentage points.

Capital gains inside super receive an additional concession. Assets held for more than 12 months attract a one-third discount on the standard 15% rate, producing an effective capital gains tax of 10%. Outside super, the same gain is taxed at the investor’s marginal rate, reduced only by the standard 50% CGT discount.

| Tax Category | Inside Super Rate | Outside Super Rate (37% Bracket) |

|---|---|---|

| Earnings tax | 15% | 37% + 2% Medicare levy |

| Capital gains (12+ months) | 10% effective | 18.5% (after 50% CGT discount) |

| Pension-phase earnings (post-60) | 0% | Marginal rate applies |

| Concessional contribution entry | 15% | N/A (taxed as income at marginal rate) |

The pension-phase advantage: Once a member reaches age 60 and transitions to pension phase, earnings inside super are taxed at 0%. No other domestic investment structure, whether trust, company, or investment bond, offers this rate. It is the single most powerful structural advantage in the Australian tax system for retirement savers.

The inputs are deliberately simple. Two portfolios, identical in every respect except tax treatment: $100,000 starting capital, a 35-year-old investor earning $95,000, a 25-year holding period, and a 9% gross annual return. No additional contributions after the initial amount. The same index fund. The same market.

The key assumptions are transparent:

Real investor outcomes will vary by marginal rate, fund choice, fee level, and actual market returns. The projection is illustrative of the tax mechanics, not a financial forecast.

The personal portfolio comes first. At a 9% gross return with approximately 2% annual tax leakage on dividends and capital gains events, the after-tax compounding rate settles around 5.7-7% depending on income level and franking credit recovery. After 25 years, the projected balance reaches approximately $530,000.

The super portfolio holds the same investment. But at a 10-15% effective earnings tax rate, the after-tax compounding rate sits closer to 7.65-8.1%. After 25 years, the projected balance reaches approximately $760,000.

The gap: approximately $230,000. The investment return was identical. The tax treatment was the sole variable. ASFA modelling directionally supports a $200,000+ advantage over 25 years at a 7% gross return, consistent with this projection.

The implication reframes the decision entirely. Investors who benchmark super against shares by comparing fund returns are solving the wrong equation. The relevant comparison is after-tax compounding, and the divergence is large enough to alter retirement outcomes by years of additional working life.

The scale of this compounding shortfall becomes more confronting when set against superannuation balance benchmarks by age, which show the average Australian aged 50-54 holding approximately $198,400 in super, more than $430,000 below the ASFA comfortable retirement threshold, a gap that the tax drag on personal portfolios compounds further with every passing year.

The common framing treats tax as a deduction: the government takes a slice, the investor keeps the rest. That framing understates the damage. Tax leakage outside super does not just reduce each year’s return. It reduces the base on which future returns are calculated.

At a 37% marginal rate, a 9% gross return on dividends and realised gains becomes approximately 5.7% net. Inside super, the same 9% gross return becomes approximately 7.65% after the 15% earnings tax. The difference between compounding at 5.7% and 7.65% over 25 years on a $100,000 base is not a minor gap. It is the gap between $530,000 and $760,000.

The mechanics are straightforward. Inside super, the full pre-tax earnings are retained within the fund each year. The 15% tax is applied to earnings, but the remaining 85% of each year’s gain rolls into the base for the following year. Outside super, the marginal rate strips a larger portion before reinvestment, permanently shrinking the compounding base.

Three stages define super’s structural tax advantage:

The 0% earnings tax in pension phase applies from age 60 under current legislation, confirmed in the 2026 Labor Budget. This means the compounding rate effectively increases at the precise point in an investor’s life when balances are at their largest and each percentage point of return difference carries the most dollar impact. No equivalent benefit is available through trusts, companies, or investment bonds. Super fund returns, as reported by industry data providers, are already net of the 15% earnings tax and fees (approximately 0.5-1% per annum), meaning published performance figures reflect the accumulation-phase tax treatment.

The tax advantage is only useful to the extent an investor can get capital into the structure. The contribution rules are the levers.

The concessional contributions cap sits at $30,000 for the 2025-26 financial year. This includes employer Superannuation Guarantee payments and any salary sacrifice amounts. For a salaried employee earning $120,000 who salary sacrifices $15,000, the tax saving is approximately $4,800 in income tax, calculated as the difference between their marginal rate and the 15% concessional contributions tax.

The carry-forward rule is where the real opportunity sits for mid-career investors. Individuals with a super balance below $500,000 can access unused concessional caps from the previous five financial years. For someone who has not maximised contributions in prior years, this can enable a single-year contribution of $100,000 or more, particularly useful following a bonus, a business sale, or a high-income year.

The ATO contributions caps and carry-forward rules confirm that individuals with a total superannuation balance below $500,000 on 30 June of the previous financial year can access up to five years of unused concessional cap space, meaning a single-year contribution well above the standard $30,000 limit is achievable in the right circumstances.

Carry-forward opportunity: An investor who has not fully utilised their concessional cap over the past five years, and whose super balance sits below $500,000, may be eligible to contribute well above the standard $30,000 annual cap in a single financial year.

The non-concessional cap provides a second vehicle. At $120,000 annually, with the bring-forward rule allowing up to $360,000 over three years for those under 75, investors can deploy after-tax capital into super’s lower-tax environment.

| Contribution Type | Annual Cap (2025-26) | Key Rule | Best Use Case |

|---|---|---|---|

| Concessional | $30,000 | Includes employer SG and salary sacrifice | Ongoing salary sacrifice for 32.5%+ earners |

| Non-concessional | $120,000 (bring-forward: $360,000 over 3 years) | After-tax contributions; no tax deduction | Lump-sum deployment from savings or asset sales |

| Carry-forward | Up to 5 years’ unused concessional caps | Balance must be below $500,000 | High-income year; bonus; business sale proceeds |

Super is preserved until age 60 for those born after 1964. For a 35-year-old investor, that is approximately 25 years of capital lock-up. ASX-listed shares, by contrast, settle within two business days. The liquidity gap is real and should not be softened.

Specific goals that require capital before age 60 cannot be served by super:

These are not edge cases. They are the financial events that define a mid-career decade.

The rules governing super have changed multiple times over the past two decades, and investors should account for this.

The pattern is worth noting: the core advantages (the 15% accumulation rate and the 0% pension-phase exemption) have survived multiple government changes and remain intact under the 2026 Labor Budget. Legislative risk is a factor to monitor and plan around, not a reason to forgo the structure entirely.

The conditions under which super is the dominant vehicle are specific. The investor is aged 30-55. Their marginal tax rate is 32.5% or above. Their time horizon extends to age 60 or beyond. Cash flow allows maximising the concessional cap without financial strain. When all four conditions hold, the tax compounding advantage is difficult to replicate through any other structure.

Direct shares are preferable under a different set of conditions: capital is needed before age 60; the investor earns below $45,000 (reducing super’s tax advantage); specific liquidity-dependent goals exist; or the investor has already maximised both concessional and non-concessional caps.

| Investor Profile | Recommended Primary Vehicle | Rationale |

|---|---|---|

| High earner (37%+ rate), under 55 | Super (maximise concessional cap) | 22-30 ppt contribution saving; 15% earnings tax vs 39%+ |

| Mid-earner (32.5% rate), aged 30-50 | Super first, shares for surplus | Meaningful tax saving; liquidity preserved via shares |

| Low earner (under $45,000), any age | Direct shares or split | Tax advantage narrows; liquidity value increases |

| Investor with pre-60 liquidity needs | Direct shares for those goals | Super cannot serve sub-60 capital requirements |

| Investor who has maximised both caps | Direct shares / ETFs | No additional super capacity; shares are the next-best vehicle |

The split strategy is the practical consensus among financial planners: maximise salary sacrifice to the concessional cap first, then direct surplus savings into an ETF portfolio for liquidity and flexibility. This is not a compromise. It captures the tax compounding advantage for the bulk of long-term wealth while preserving the flexibility that direct shares provide for life events that do not wait until age 60.

The super and ETF split strategy is where the tax compounding argument meets practical implementation: directing a fixed monthly amount across salary sacrifice and a low-cost ASX ETF portfolio captures the 15% accumulation tax rate on the super portion while keeping a liquid buffer outside the preservation age barrier for goals that arrive before 60.

Three immediate actions for a mid-career investor:

Active versus passive fund performance data adds a compounding layer to this decision: SPIVA figures show 74% of Australian equity managers failed to beat the S&P/ASX 200 in 2025, which means the default balanced option inside super is doubly penalised, carrying both a higher fee drag and a higher probability of underperforming the index that a low-cost ETF would simply replicate.

For mid-career Australian investors on a 32.5% marginal rate or above, the tax differential between superannuation and a personal share portfolio is the dominant determinant of long-term wealth outcomes. Not the fund manager. Not the stock selection. Not the market cycle. The wrapper.

The trade-offs are genuine. Liquidity is constrained until age 60. Legislative settings can change. The lock-up period is long. Direct shares address all three of those limitations and remain the appropriate vehicle for capital needed before preservation age.

With pension-phase tax exemption intact under the 2026 Budget and voluntary contributions rising, the structural case for maximising super within contribution caps remains as strong as it has been, for investors whose time horizon extends to age 60. The next contribution decision is not about chasing a better return. It is about choosing which tax rate compounds alongside the return already being earned.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Inside superannuation, investment earnings are taxed at a flat 15%, while the same earnings outside super are taxed at the investor's marginal rate, which can be 37% or higher plus the 2% Medicare levy, creating a gap of 24 percentage points or more on every dollar earned each year.

Based on illustrative projections using a $100,000 starting balance, a 9% gross annual return, and a 25-year holding period, the superannuation portfolio reaches approximately $760,000 versus $530,000 for a personal portfolio, a gap of roughly $230,000 driven entirely by the difference in tax treatment.

The carry-forward rule allows Australians with a superannuation balance below $500,000 to access up to five years of unused concessional contribution cap space, potentially enabling a single-year contribution well above the standard $30,000 annual limit, which is particularly useful in a high-income year, following a bonus, or after a business sale.

Once a member reaches age 60 and transitions to pension phase, earnings inside superannuation are taxed at 0% under current legislation, confirmed in the 2026 Labor Budget, making it the most tax-efficient investment structure available to Australian retirement savers.

Financial planners broadly recommend maximising salary sacrifice to the concessional cap first to capture the 15% accumulation tax rate, then directing surplus savings into a low-cost ETF portfolio outside super to preserve liquidity for financial goals that arise before the preservation age of 60.