On 28 April 2026, VanEck listed three new diversified ETFs on the ASX, each carrying an active management mandate and a CPI-plus return target. The products, VBAL, VGRO, and VHGR, are the most explicitly inflation-aware single-ticket offerings in a category that has, until now, been defined entirely by passive index tracking.

The diversified ETF-of-ETFs segment has become the default starting point for Australian retail investors seeking multi-asset exposure in a single trade. BetaShares and Vanguard have built substantial followings in this space, but both rely on passive indexing to deliver market-level returns. VanEck’s entry reframes the category question: passive simplicity versus active ambition, and whether the fee premium attached to the latter is worth paying before any performance data exists.

What follows is a comparison of VanEck’s range against BetaShares’ DHHF and Vanguard’s diversified suite (VDCO, VDBA, VDGR, VDHG) across fee structure, asset class coverage, management approach, and risk-profile fit, so investors can evaluate which product suite genuinely matches their objectives.

A crowded category gets a new contender

The diversified ETF-of-ETFs segment is not a new idea on the ASX. BetaShares’ DHHF has accumulated approximately $1 billion in assets under management (a community-sourced figure, treated as indicative), and Vanguard’s four-product range spans conservative through high-growth risk profiles. Investor adoption is well established.

The ASX ETF market growth context matters here: assets under management are estimated at $340-$350 billion as of April 2026, with Betashares forecasting the figure to exceed $500 billion by end-2028, which helps explain why providers like VanEck view the diversified ETF-of-ETFs segment as worth entering with a differentiated product.

VanEck’s entry is a deliberate positioning move rather than a routine product release. The three new funds span the same balanced-to-high-growth risk spectrum as their rivals, signalling direct competitive intent. What distinguishes them from day one is the management approach: an explicitly active mandate with inflation-beating return objectives.

The three products launched at $20 per unit with the following targets:

- VBAL: targets CPI + 3% per annum

- VGRO: targets CPI + 4% per annum

- VHGR: targets CPI + 5% per annum

Those CPI-plus targets are the clearest signal of what VanEck is selling. Rather than competing on cost alone, the range positions itself as an active alternative for investors who want more than index-level returns from a single-ticket diversified product.

When big ASX news breaks, our subscribers know first

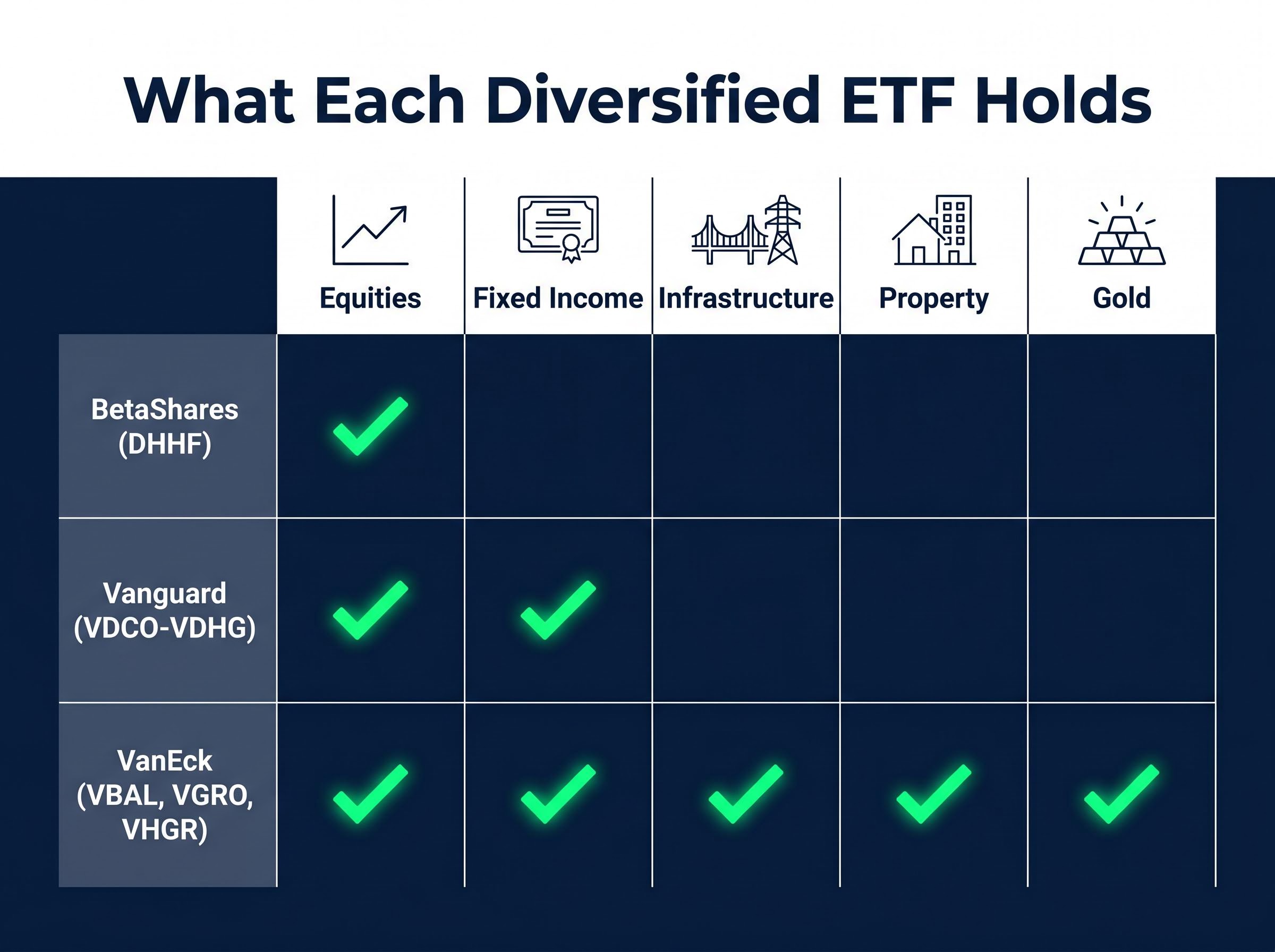

What each fund actually holds

All three providers use the ETF-of-ETFs structure, where a single listed fund holds a portfolio of underlying funds to deliver multi-asset exposure. The structural similarity ends there.

VanEck invests exclusively through its own products, including MVW (the VanEck Australian Equal Weight ETF) for domestic equities, alongside international equity, fixed income, and three asset classes its passive rivals do not include: listed infrastructure, property, and gold. The growth-to-defensive balance shifts across the range, with VHGR holding a higher weighting to Australian equities via MVW and VBAL a lower weighting, though exact percentage allocations should be confirmed via VanEck’s product disclosure statement.

BetaShares’ DHHF takes a structurally different approach. It allocates 100% to growth assets across diversified global and Australian equities, with no defensive allocation. There is no fixed income, no infrastructure, no gold. It is a pure equity growth bet.

Vanguard’s range sits between the two. Its four products move from VDHG at 90% growth and 10% defensive through to VDCO at the conservative end, with allocations split across equities and fixed income according to each fund’s risk profile. Exact per-asset-class weights are available in Vanguard’s product disclosure statements.

| Provider | Tickers | Structure | Asset Classes Held | Growth/Defensive Split |

|---|---|---|---|---|

| VanEck | VBAL, VGRO, VHGR | ETF-of-ETFs (VanEck products only) | Equities, fixed income, infrastructure, property, gold | Balanced through high growth |

| BetaShares | DHHF | ETF-of-ETFs (multi-provider index ETFs) | Equities only | 100% growth |

| Vanguard | VDCO, VDBA, VDGR, VDHG | ETF-of-ETFs (Vanguard index funds) | Equities and fixed income | Conservative through high growth |

The additional asset classes VanEck includes beyond standard equities and bonds are worth noting:

- Listed infrastructure

- Property

- Gold

These asset classes behave differently across economic cycles. For investors choosing DHHF, the commitment is to pure equity growth. For those considering VanEck, the multi-asset approach introduces inflation-sensitive holdings that passive rivals do not offer.

An inflation-resilient portfolio allocation framework typically assigns weight to alternatives including gold and listed infrastructure precisely because these assets behave differently from equities and bonds during inflationary cycles, which is the same logic underpinning VanEck’s decision to include those asset classes in VBAL, VGRO, and VHGR.

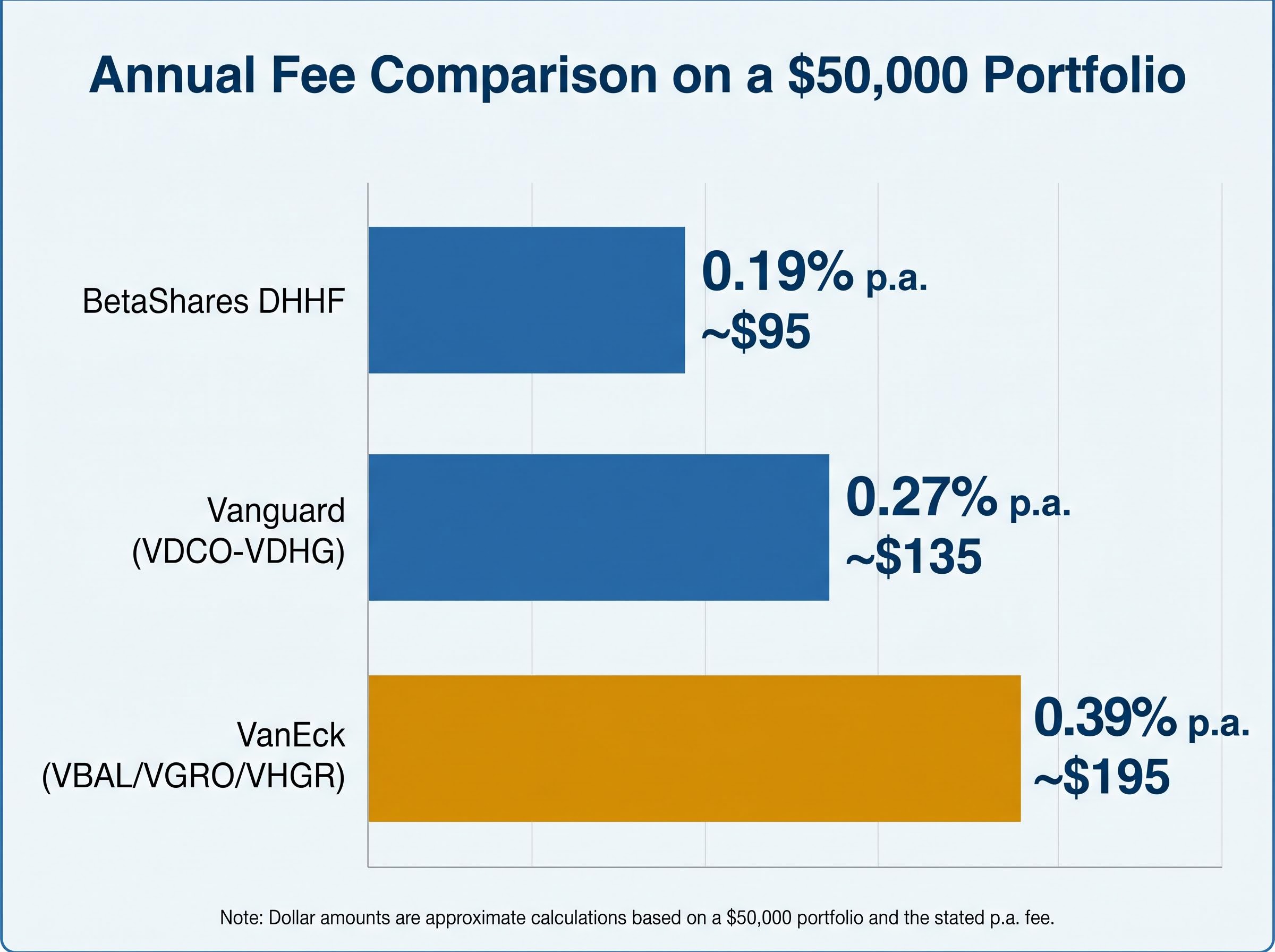

The fee gap and what it buys

The fee structure across the three providers forms a clear hierarchy.

| Provider / Ticker | Annual Fee | Dollar Cost on $50,000 |

|---|---|---|

| BetaShares DHHF | 0.19% p.a. | ~$95 |

| Vanguard (VDCO-VDHG) | 0.27% p.a. | ~$135 |

| VanEck (VBAL/VGRO/VHGR) | 0.39% p.a. | ~$195 |

On a $50,000 portfolio, the difference between the cheapest and most expensive option is $100 per year. That figure looks modest in a single year. Over a longer horizon, it compounds.

Over a 20-year investment period, the cumulative fee difference between 0.19% and 0.39% on a $50,000 portfolio, assuming reinvestment and market growth, can amount to thousands of dollars in foregone returns. The question is whether active management generates enough additional return to offset that drag.

VanEck’s stated justification for the premium is the active management mandate and the CPI-plus return objectives. The range is positioned as a “Core+” offering drawing on institutional investment frameworks, where the fund manager makes deliberate allocation decisions rather than tracking an index mechanically.

The fee premium is a forward-looking cost certainty against an unproven return objective. VanEck’s funds launched on 28 April 2026 and carry no ASX performance track record. Whether the active approach delivers returns above the fee drag remains to be seen.

Active vs passive: what the distinction actually means for retail investors

Most retail investors in the ETF-of-ETFs space have defaulted to passive products without explicitly choosing passive over active. VanEck’s entry forces that choice into the open.

What passive management means in practice

Passive management in this context means index replication. The fund holds what the index holds, in the proportions the index dictates. Rebalancing is driven by index rules rather than manager discretion. Both BetaShares and Vanguard operate on this basis.

The outcome is predictable: the fund delivers market returns minus fees. There is no manager making calls about whether to overweight Australian equities or rotate into gold. The investor gets the market, for better or worse, at a low cost.

What active management commits you to

Active management introduces manager discretion as a variable. VanEck’s range is designed to target real returns above CPI, not a market benchmark. The fund manager can shift allocations between asset classes based on their assessment of market conditions.

VanEck positions this as “Core+” management, drawing on institutional frameworks. The CPI-plus targets (VBAL at CPI + 3%, VGRO at CPI + 4%, VHGR at CPI + 5%) provide the specific benchmarks against which the manager’s performance can be measured.

The ABS Consumer Price Index data provides the official inflation baseline against which VanEck’s CPI-plus return targets, ranging from CPI + 3% for VBAL to CPI + 5% for VHGR, will be measured in practice, making current and historical CPI figures directly relevant to evaluating whether active management adds real value over time.

Those targets are objectives, not guarantees. With no performance history on the ASX, VanEck’s active mandate is being taken on trust at this stage. Active management can work for or against the investor, and the manager’s skill becomes the variable that passive products eliminate.

Investors weighing VanEck’s CPI-plus targets against a passive alternative may also want to consider inflation-sensitive ASX ETFs that sit outside the diversified ETF-of-ETFs structure entirely, particularly fixed income and quality-factor equity funds that can be combined to target real returns without committing to a single active manager.

Before choosing active over passive, three questions are worth considering:

- How long is the investment time horizon? Active management typically requires longer periods to demonstrate whether it adds value.

- What is the tolerance for periods of underperformance relative to a passive alternative?

- Are the investor’s financial goals sensitive to inflation in a way that makes CPI-plus targeting specifically relevant?

Matching the fund to the investor: risk profiles and practical fit

The choice of provider is partly determined by which risk profile the investor needs. Vanguard offers four options spanning conservative through high growth. VanEck offers three, from balanced through high growth. BetaShares offers one: all growth, all equities.

That gap in BetaShares’ range matters. DHHF suits investors who want 100% equity exposure and are comfortable accepting no defensive allocation. For some investors, particularly those with long time horizons and high risk tolerance, that is appropriate. It is not, however, a default for all investor profiles.

The investor profile most suited to VanEck’s range has specific characteristics:

- A preference for active management over passive index tracking

- A priority on inflation-beating return targets rather than market-matching returns

- Willingness to pay a higher fee in exchange for broader asset class coverage

- An interest in exposure to infrastructure, property, and gold alongside equities and fixed income

| Investor Profile | Best-Fit Provider | Recommended Ticker(s) | Key Reason |

|---|---|---|---|

| Cost-focused, high growth tolerance | BetaShares | DHHF | Lowest fee, 100% equity exposure |

| Passive, moderate risk | Vanguard | VDBA or VDGR | Proven passive range, balanced allocations |

| Passive, conservative | Vanguard | VDCO | Only provider offering a conservative option |

| Active, inflation-sensitive goals | VanEck | VBAL, VGRO, or VHGR | CPI-plus targets, multi-asset including gold |

| Passive, high growth | Vanguard or BetaShares | VDHG or DHHF | Low cost, high equity weighting |

The right product is not the cheapest or the most sophisticated in isolation. It is the one whose risk profile, asset class mix, and management approach matches what the investor actually needs from a core portfolio holding.

Three providers in, one decision to make: how to approach the choice today

The three-way comparison distils to a cost-versus-coverage-versus-conviction decision:

- BetaShares DHHF offers the lowest cost at 0.19% p.a. and pure equity growth exposure

- Vanguard’s range offers proven passive diversification across the full risk spectrum at 0.27% p.a.

- VanEck’s range offers the broadest asset class coverage and active management at 0.39% p.a., with no ASX performance history

VanEck’s active mandate means the comparison will become more meaningful in 12-24 months once a performance track record against CPI-plus targets begins to form. The ETF-of-ETFs structure itself is validated across all three providers; the decision ultimately comes down to what the investor believes a diversified core holding should do: replicate the market, or attempt to beat inflation.

VanEck’s CPI-plus return targets are objectives, not guarantees. The funds launched on 30 April 2026 and carry no ASX performance history. The active management premium will be testable only once sufficient performance data accumulates.

Three practical questions can help frame the decision:

- What level of annual fees is acceptable for the expected holding period?

- Which risk profile (conservative, balanced, growth, or high growth) matches the investor’s circumstances?

- Is there a specific conviction that active management can add value above the additional cost?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The verdict depends on what you ask your portfolio to do

This is not a comparison where one product wins outright. The decision depends on what the investor believes a diversified core ETF should accomplish.

For cost-focused investors comfortable with pure equity exposure, DHHF remains the lowest-fee option in the segment. For those seeking passive multi-asset coverage across the full risk spectrum, Vanguard’s four-product range provides the widest selection. For investors willing to pay more for active management, broader asset class exposure including gold and infrastructure, and explicit inflation-beating targets, VanEck’s new range presents a distinct proposition.

The forward-looking question is straightforward. VanEck’s CPI-plus targets will either validate the fee premium over the coming 12-24 months or give investors reason to re-evaluate. That makes the ASX diversified ETF category worth revisiting as performance data accumulates.

Investors considering any of these products should consult the product disclosure statements for VBAL, VGRO, VHGR, DHHF, and the Vanguard diversified range before investing, and consider their specific financial goals and risk tolerance in the context of professional financial advice.

For investors who find none of the three single-ticket providers a perfect fit, our dedicated guide to building a quality-focused ASX ETF portfolio walks through how QUAL, IVV, and AQLT can be combined into a self-directed multi-asset allocation with a blended fee well below any of the diversified ETF-of-ETFs options assessed here.

ASIC’s exchange traded product obligations require ETF issuers to provide product disclosure statements covering fees, asset class exposures, and management approaches, which is why comparing PDS documents across VanEck, BetaShares, and Vanguard remains the appropriate first step for any investor evaluating these products.