ASML shares jumped roughly 3.5% in Amsterdam by 09:00 GMT on Wednesday after UBS reinstated the Dutch lithography giant as its top European semiconductor pick, setting a price target of €1,900. That figure implies more than 50% upside from Tuesday’s close of €1,249 on Euronext Amsterdam.

The upgrade lands at a moment when ASML stock has underperformed most of its semiconductor equipment peers on a year-to-date basis, leaving its valuation premium versus U.S. rivals near a decade low. That divergence is precisely what UBS analyst Francois-Xavier Bouvignies and his team say makes the stock compelling right now.

What follows is a breakdown of the UBS price target, the three investment arguments behind it, and what the bank’s above-consensus earnings forecasts mean for investors tracking European semiconductor equities.

Why ASML’s valuation gap versus U.S. peers is flashing a buy signal for UBS

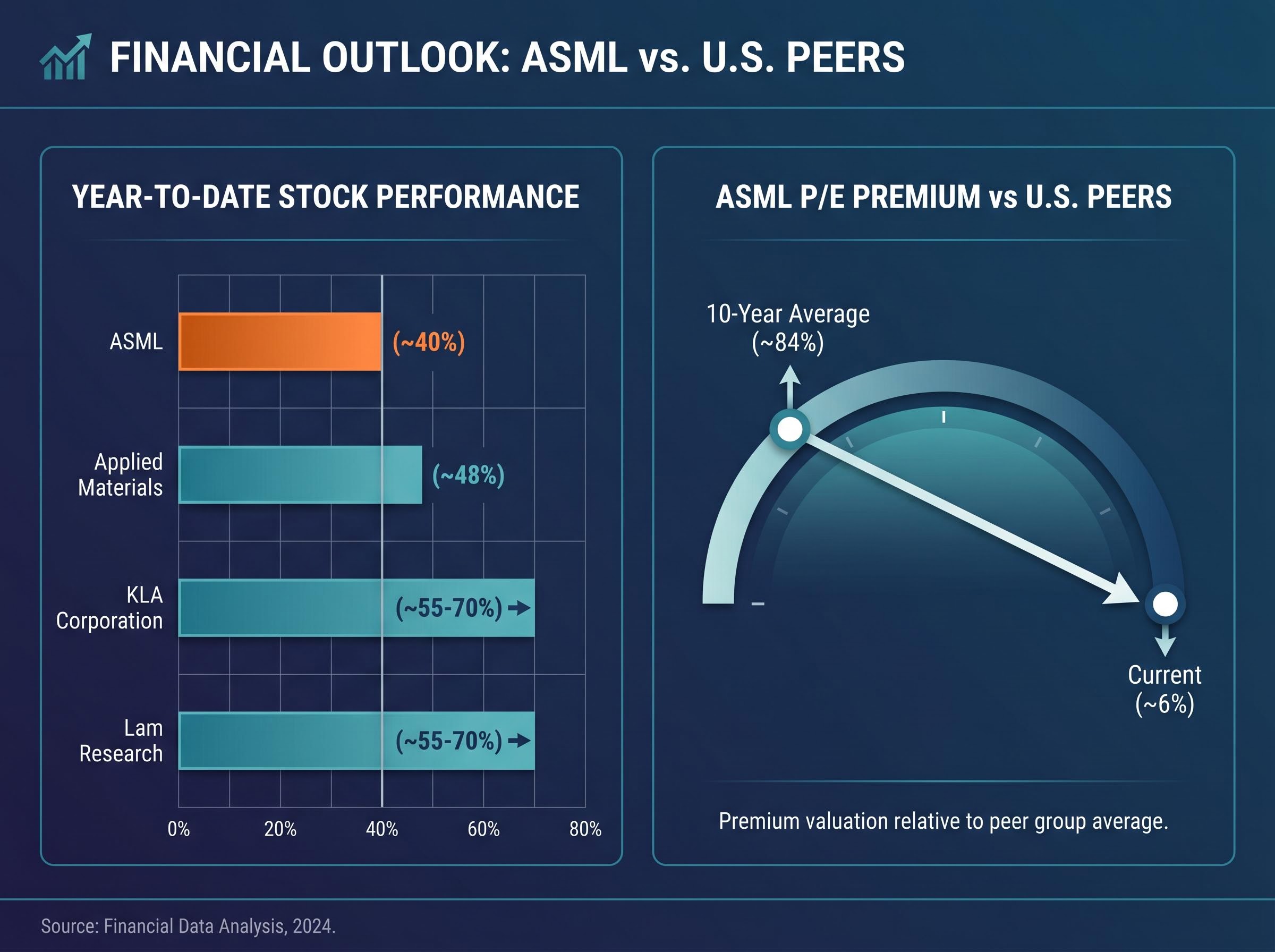

ASML has gained approximately 40% year to date. On its own, that looks strong. Set it against U.S. semiconductor equipment names, and the picture shifts:

- Applied Materials (AMAT): approximately 48% year-to-date gain

- KLA Corporation: approximately 55-70% year-to-date gain

- Lam Research: approximately 55-70% year-to-date gain

The performance gap has compressed ASML’s valuation premium to a level UBS considers anomalous. On a 12-month forward price-to-earnings basis, ASML now trades at roughly a 6% premium to its U.S. large-cap peers. Over the past decade, that premium has averaged approximately 84%.

Semiconductor valuation frameworks applied to the current cycle reveal a fragmented picture: Micron trades below 9x forward earnings while Intel sits near 101x, a dispersion that illustrates why sector-level P/E comparisons can obscure more than they reveal when assessing whether any single name’s premium is justified or anomalous.

Valuation signal: ASML’s 12-month forward P/E premium has collapsed from a 10-year average of roughly 84% to approximately 6% versus U.S. large-cap semiconductor equipment peers.

UBS reads that compression as mispricing rather than a structural re-rating, and it forms the foundation of the reinstatement. The bank raised its price target from a prior €1,600 to €1,900, with the closing price on 19 May 2026 of €1,249 serving as the baseline for what UBS frames as an entry point investors rarely get on a monopoly asset.

When big ASX news breaks, our subscribers know first

How UBS constructs its bull case for the €1,900 price target

The UBS note is structured less as an endorsement and more as a rebuttal. Each of the three investment pillars addresses a specific concern that has held the stock back.

| Pillar | Market concern addressed | UBS counter-argument | Key metric |

|---|---|---|---|

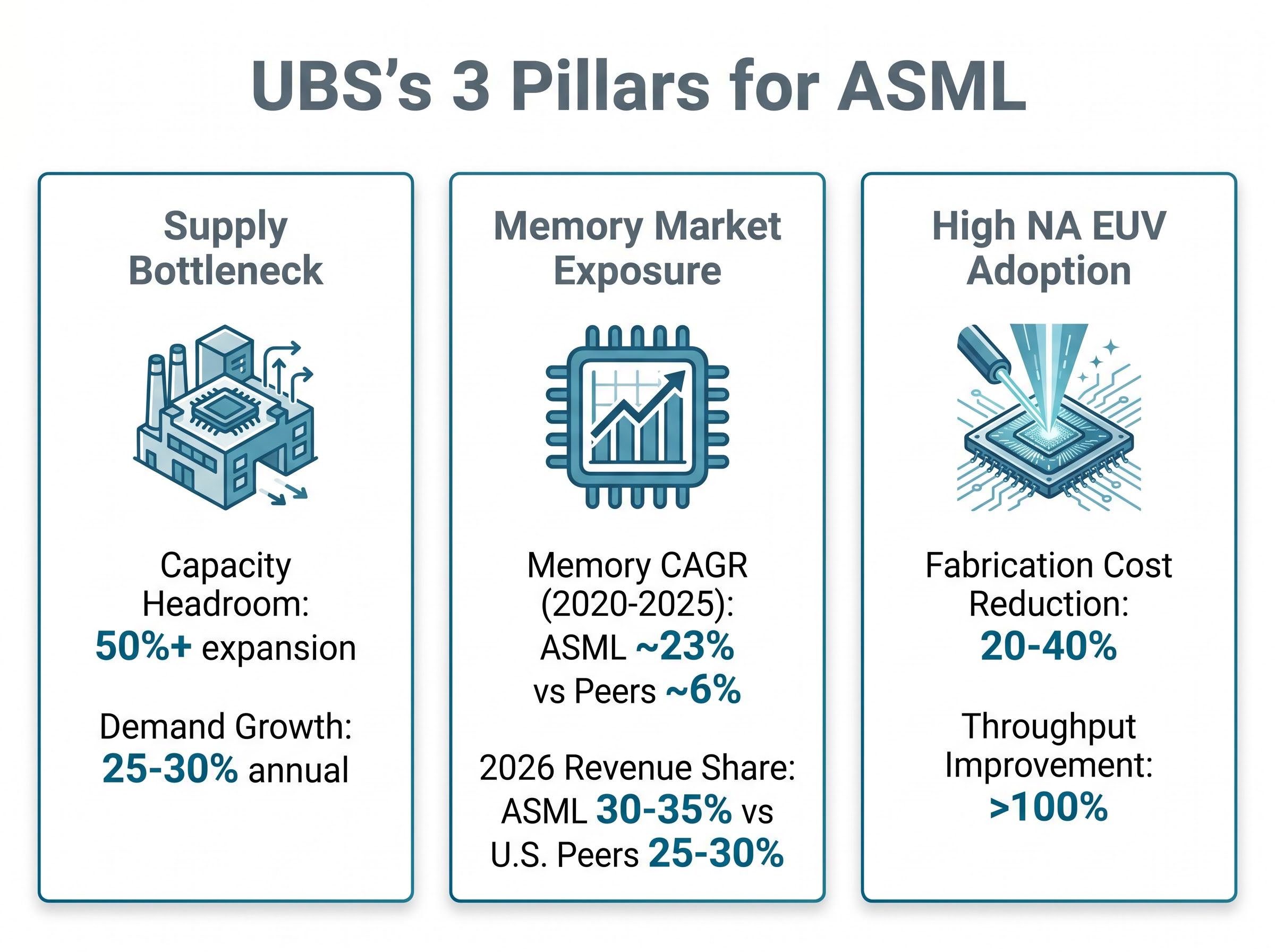

| Supply bottleneck dismissal | ASML cannot produce enough machines to meet demand | Projected 2027 production capacity can absorb more than 50% year-on-year expansion in leading-edge wafer output, well above anticipated demand growth | Capacity headroom: 50%+ expansion vs 25-30% annual demand growth |

| Memory market exposure | High memory revenue share is a cyclical risk | Rising EUV intensity in DRAM node shrinkage makes memory exposure an underappreciated tailwind | Memory revenue CAGR: ~23% (ASML, 2020-2025) vs ~6% for comparable peers |

| High NA EUV adoption | TSMC delays undermine the next-generation platform | Delays shift timing, not the eventual adoption curve; cost and throughput advantages are too large to bypass | Fabrication cost reduction: 20-40%; throughput improvement: exceeding 100% |

On the memory pillar, ASML’s memory segment accounted for approximately 30-35% of total revenues by 2026, compared with 25-30% for U.S. peers. UBS argues that this higher exposure positions ASML to capture a disproportionate share of the EUV-driven DRAM upgrade cycle, particularly as Samsung, SK Hynix, and Micron expand high-bandwidth memory capacity for AI workloads.

The AI-driven DRAM capex cycle that underpins ASML’s memory revenue thesis is structurally unlike previous upcycles: hyperscaler spending commitments now account for an estimated 70% of total memory shipment volumes, and new manufacturing capacity is not expected to reach mass production until after 2027, removing the supply-side pressure relief that historically shortened memory equipment spending windows.

High NA EUV throughput: UBS estimates the next-generation platform delivers throughput improvements exceeding 100% versus most alternative patterning approaches, alongside 20-40% cost reductions on critical fabrication layers.

The High NA pillar acknowledges TSMC’s cautious stance without treating it as thesis-breaking. UBS’s position is that the economics of High NA are too compelling for any leading-edge manufacturer to skip indefinitely.

What ASML actually does and why lithography machines are so hard to replace

At the core of every advanced semiconductor is a patterning step: light is projected through a mask onto a silicon wafer to print circuit features measured in nanometres. Extreme ultraviolet (EUV) lithography uses light with a wavelength of 13.5 nanometres to achieve the resolution required for the smallest transistors in production today.

ASML is the sole commercial supplier of EUV lithography systems. That monopoly position reflects decades of accumulated engineering complexity across optics, light sources, and precision mechanics. No competitor has demonstrated a commercially viable alternative, and the development timeline for a rival system would span years, if not longer. ASML trades on Euronext Amsterdam under ISIN NL0010273215 for investors seeking live price data.

ASML’s 100% EUV market share, confirmed by independent industry analysis as of mid-2025, underpins the monopoly premium that UBS argues has been incorrectly eroded by recent underperformance relative to U.S. peers.

High NA EUV: the next platform shift ASML is already selling

High NA EUV represents the next generation of the platform, using a wider-aperture lens to print even finer features with fewer patterning steps. UBS estimates commercial adoption within approximately two to three years, with broader high-volume manufacturing uptake extending into the 2030s.

Intel is the lead High NA customer. TSMC and Samsung have also placed orders, though TSMC has adopted a more cautious timeline, evaluating High NA for nodes beyond its current N2 generation. UBS views the delays as a timing shift rather than a challenge to the eventual adoption curve.

How far UBS’s earnings estimates depart from consensus and why it matters

The numbers themselves are the starting point. UBS projects ASML earnings per share of €48.42 for 2027 and €59.73 for 2028. Both figures sit approximately 15-20% above prevailing analyst consensus.

| Year | UBS EPS estimate |

|---|---|

| 2027E | €48.42 |

| 2028E | €59.73 |

| Both estimates approximately 15-20% above consensus | |

Three drivers underpin the gap: a more constructive view on memory capex durability, faster High NA adoption contributing to revenue mix uplift, and dismissal of the bottleneck risk that has weighed on Street forecasts. The €1,900 price target is internally consistent with these estimates, meaning it is not credible unless the earnings forecasts prove directionally correct.

Analyst view: Francois-Xavier Bouvignies of UBS has characterised ASML as offering the most favourable risk-to-reward profile in semiconductor equipment.

The scale of the departure matters. A target that sits 15-20% above consensus on earnings is not incremental optimism; it is a deliberate, argued bet that the market is underestimating ASML’s earnings power over the next two to three years.

The next major ASX story will hit our subscribers first

ASML’s path to €1,900 depends on getting these assumptions right

The UBS thesis is specific enough to monitor and specific enough to fail. Three assumptions must hold for the price target to track:

- High NA EUV adoption must stay on schedule. If TSMC’s timeline slips beyond the two-to-three-year window UBS projects, the mix uplift that drives above-consensus EPS does not materialise on time.

- Memory capex must remain durable. The earnings forecasts assume DRAM manufacturers sustain elevated equipment spending through the AI infrastructure cycle. A slowdown in AI-related capital expenditure would compress ASML’s memory revenue growth.

- Export controls must not escalate further. Any tightening of restrictions targeting ASML’s EUV shipments, particularly to China, would directly reduce the addressable market UBS’s revenue estimates assume.

China revenue exposure is the export-control risk most directly linked to ASML’s addressable market assumptions; a sector-wide analysis published in May 2026 estimated ASML’s China revenue share at approximately 29%, materially higher than Nvidia’s roughly 15%, making any tightening of BIS equipment restrictions a disproportionate earnings headwind relative to most U.S. semiconductor peers.

ASML traded at approximately €1,290 intraday on 20 May 2026, reflecting the day’s move. Reaching €1,900 from that level implies roughly 47% upside, an outcome that requires the earnings upgrade cycle UBS is projecting to materialise over the next 12 to 18 months.

UBS’s bet on ASML is ultimately a bet on the decade’s chip buildout

The reinstatement on 20 May 2026, with a price target lifted from €1,600 to €1,900, is not a narrow call on one quarter’s order book. It is a position on where the semiconductor equipment cycle goes for the rest of the decade: that ASML is the infrastructure provider that every leading-edge fab depends on, and that a valuation compression to near-peer levels represents a structural mispricing rather than a justified discount.

Price targets in semiconductor equipment often attract follow-on commentary from other banks within days. Investors tracking this thesis should monitor ASML’s quarterly order intake and High NA EUV delivery milestones (ASML trades on Euronext Amsterdam, ISIN: NL0010273215) as the most reliable forward indicators of whether UBS’s conviction is well placed.

Investors evaluating UBS’s conviction on ASML against broader market scepticism about semiconductor valuations will find our full explainer on the semiconductor bubble rebuttal, which examines Bank of America’s free cash flow yield data, the 20% earnings revision momentum across the sector, and why active long-only positioning at half the 2017 cycle peak undermines the speculative-excess argument that has kept some institutional investors on the sidelines.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.