Aristocrat Leisure shares surged 11.7% on 13 May 2026, adding more than $3 in share price value in a single session after the company delivered a slight earnings beat and announced a $1 billion expansion to its share buyback programme. The result lands at a moment when Australian investors are closely watching capital allocation decisions from large-cap ASX companies, and Aristocrat’s cumulative $2.5 billion buyback commitment now ranks among the largest active repurchase programmes on the exchange. What follows breaks down what the HY26 numbers actually showed, what the expanded buyback means for shareholders, and where management is steering the business through to FY29.

Shares surge 11.7% as results land above expectations

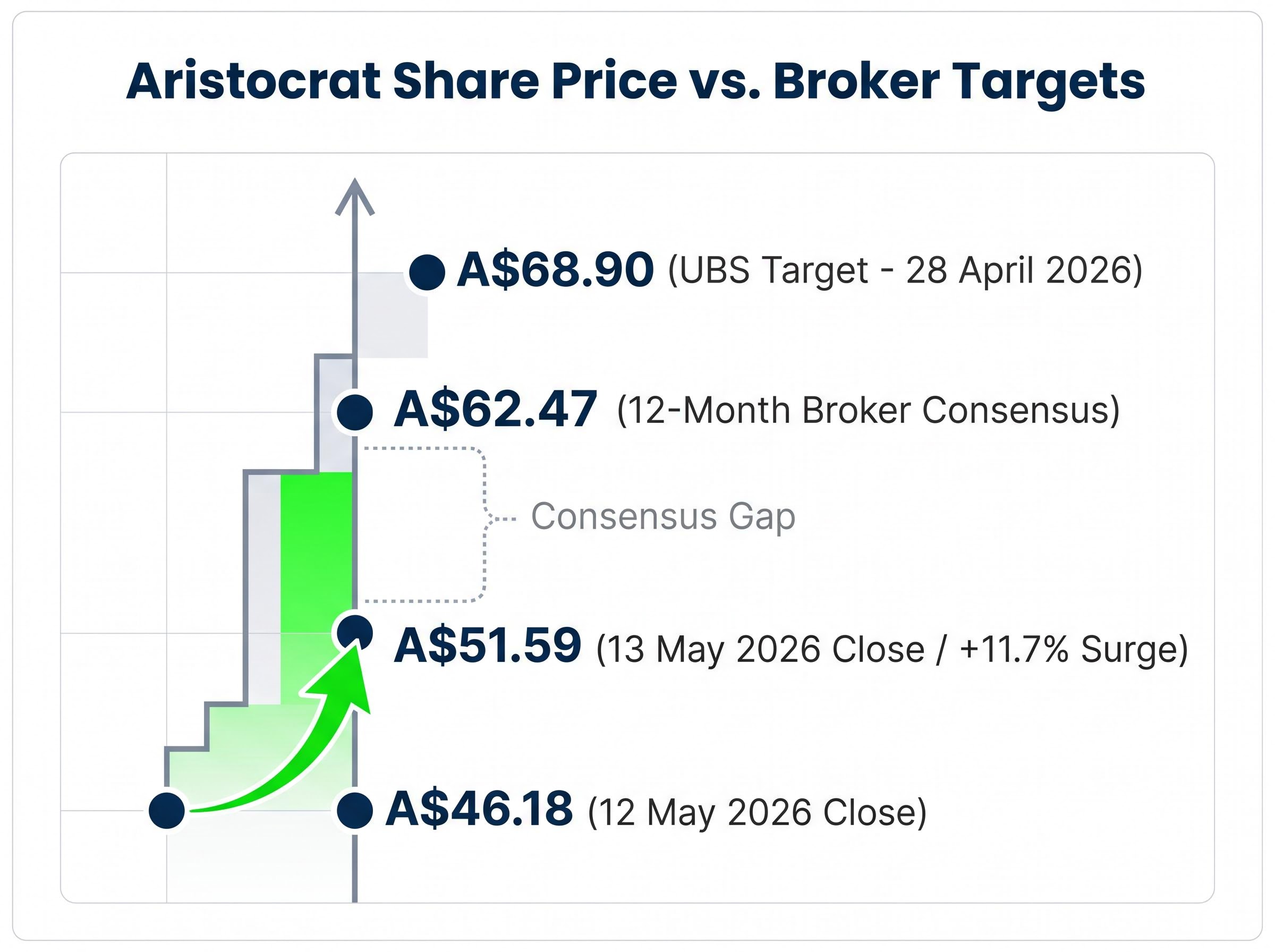

The market’s verdict arrived within minutes of the open. Aristocrat Leisure shares gapped higher at A$48.26, more than $2 above the prior close, and kept climbing through the session to finish at A$51.59. Against a 12 May 2026 close of A$46.18, that represented a gain of approximately 11.7%.

The key price levels for the session:

- Prior close (12 May 2026): A$46.18

- Opening price: A$48.26

- Intraday high and close: A$51.59

- Session gain: approximately 11.7%

Double-digit single-day moves on ASX large-caps are uncommon. This was not a routine post-results drift; two catalysts fired simultaneously. The earnings result came in slightly above consensus expectations, and the $1 billion buyback expansion signalled a capital return commitment that the market had not fully priced.

Broker consensus target: The 12-month consensus price target sits at approximately A$62.47, with UBS holding the high at A$68.90 (dated 28 April 2026). Even after the surge, the stock trades well below consensus.

When big ASX news breaks, our subscribers know first

What the HY26 numbers actually showed

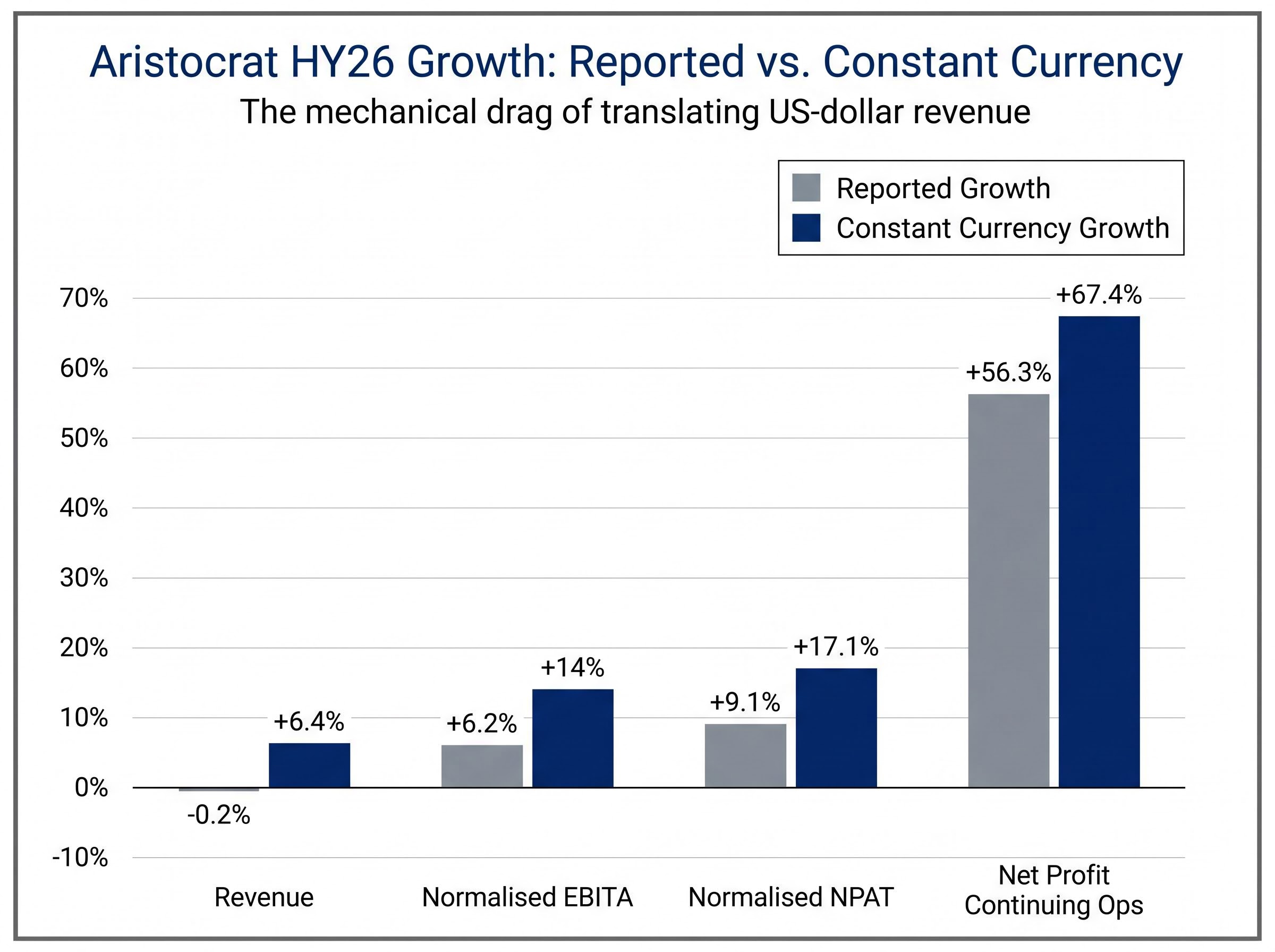

The headline revenue figure looked soft. Aristocrat reported total revenue of $3.03 billion for the half-year to 31 March 2026, down 0.2% on a reported basis. Read in isolation, that number suggests a business treading water.

The constant-currency lens tells a different story. Strip out the mechanical drag of translating US-dollar revenue into a stronger Australian dollar, and underlying revenue grew 6.4%. The same effect runs through the profit lines: normalised EBITA of $1.12 billion rose 6.2% on a reported basis but 14% in constant currency. Normalised net profit reached $725.4 million, up 9.1% reported and 17.1% in constant currency. Net profit from continuing operations surged 56.3% on a reported basis to $511 million.

| Metric | Reported Result | Reported Growth | Constant Currency Growth |

|---|---|---|---|

| Revenue | $3.03B | -0.2% | +6.4% |

| Normalised EBITA | $1.12B | +6.2% | +14% |

| Normalised NPAT | $725.4M | +9.1% | +17.1% |

| Net Profit (Continuing Ops) | $511M | +56.3% | +67.4% |

The constant-currency framing is not spin. Aristocrat generates the majority of its revenue in US dollars. The translation drag is a mechanical accounting effect, not a reflection of operational performance. Investors who read only the reported revenue line risk misreading the underlying business.

The gap between reported and constant-currency figures illustrates a broader analytical challenge with reported versus adjusted earnings: two companies can post identical underlying performance and produce dramatically different headline numbers depending on currency mix, accounting treatment, and what each chooses to normalise away.

Dividend lifted 13.6% alongside the buyback

The interim dividend rose to $0.50 per share, a 13.6% increase. That increase runs alongside the buyback expansion rather than in lieu of it, indicating management is running both income and capital return levers simultaneously.

Understanding Aristocrat’s business before the numbers make sense

Most casual observers associate Aristocrat with poker machines in Australian pubs. The reality is a US-weighted, multi-division technology business. Before the divisional performance makes sense, the structure matters.

Aristocrat operates through three divisions:

- Aristocrat Gaming: Land-based slot machines and casino management systems. Revenue comes through two channels: outright machine sales and gaming operations, a recurring lease and participation fee model where Aristocrat retains ownership of the machine and earns a share of its revenue.

- Product Madness: Free-to-play social casino mobile games. Revenue is generated through in-app purchases rather than real-money wagering.

- Aristocrat Interactive: Online real-money gaming and iLottery. This is the high-growth division with a stated revenue target of US$1 billion by FY29.

The reporting period covered the six months ending 31 March 2026. Because the majority of revenue is earned in US dollars, the AUD/USD exchange rate creates translation effects that separate reported results from underlying business performance. This is why constant-currency reporting is central to interpreting every result Aristocrat publishes.

A $2.5 billion buyback and what it returns to shareholders

The buyback programme has been increased by $1 billion to a cumulative total of up to $2.5 billion, extended through to 12 May 2027. This is not a theoretical pledge. To date, $981 million has already been returned to shareholders through a combination of dividends and on-market buybacks.

ASIC’s share buyback rules govern the conditions under which ASX-listed companies may repurchase shares on market, including the 10/12 limit that caps on-market buybacks at 10% of shares on issue within any rolling 12-month period without separate shareholder approval.

$2.5 billion: The cumulative buyback programme represents one of the largest active repurchase commitments on the ASX.

For shareholders unfamiliar with the mechanics, a buyback programme works in three steps:

Investors unfamiliar with how on-market buybacks work will find the mechanics straightforward: the company enters the market as a buyer through its broker, purchases shares at prevailing prices, and cancels them, with each cancellation permanently reducing the shares on issue and lifting earnings per share for remaining holders.

- The company purchases its own shares on the open market at prevailing prices.

- Purchased shares are cancelled, reducing the total number of shares on issue.

- With fewer shares outstanding, earnings per share rise for remaining holders, all else being equal.

The extension through May 2027 provides a multi-year capital return floor. The programme creates a persistent source of demand for shares on the open market, which is relevant context for understanding downside support at current price levels.

Divisional performance and where growth is coming from

The established engine performed. Aristocrat Gaming delivered market share gains in outright machine sales across both North America and Australia, supported by ongoing expansion of the gaming operations installed base. This division remains the earnings anchor.

Product Madness outperformed the broader social casino market, with user acquisition investment and a growing direct-to-consumer conversion strategy contributing to market share gains. The shift toward direct-to-consumer is a margin-improvement play, reducing reliance on third-party app store economics.

- Aristocrat Gaming: Market share gains in outright sales; gaming operations installed base expansion

- Product Madness: Social casino market share outperformance; direct-to-consumer conversion growth

- Aristocrat Interactive: iLottery and content revenue growth, partially offset by deliberate white label withdrawal

Interactive’s white label exit and what it means for the US$1 billion target

Aristocrat Interactive grew iLottery and content revenue, but the headline growth rate was partially compressed by a deliberate withdrawal from white label operations. Management described this as a strategic decision rather than a performance deterioration, prioritising higher-quality revenue over volume.

The division carries a stated FY29 revenue target of US$1 billion. The white label exit is part of a quality-over-volume approach to reaching that figure. iLottery expansion in North America and Europe is the primary growth vehicle: the Portugal SCML contract extension (announced approximately 7 May 2026, extending a 13-year relationship) and the Massachusetts iLottery contract (announced August 2025) provide verified evidence of momentum.

FY26 guidance and the targets investors should track

Management guided for underlying net profit growth for the full year to 30 September 2026, on a constant-currency basis. The most granular operational metric in the guidance is the gaming operations net unit growth target: the higher end of the 4,000 to 5,000 unit range for FY26.

Across the three divisions, the committed growth trajectory runs as follows: Aristocrat Gaming targeting continued revenue and market share gains; Product Madness focused on market share growth with rising direct-to-consumer contribution; and Aristocrat Interactive actively scaling toward US$1 billion by FY29.

Currency remains the variable that separates constant-currency guidance from reported outcomes. If the Australian dollar strengthens relative to the US dollar, it would translate into a headwind on reported numbers even if underlying growth is delivered.

Three metrics shareholders should monitor through to the next result:

- Gaming operations net unit count: Whether the company exits FY26 at or above the 5,000-unit end of its target range.

- Aristocrat Interactive revenue trajectory: Progress toward the US$1 billion FY29 target, with iLottery contract activity as the lead indicator.

- Reported versus constant-currency profit divergence: The gap between these two figures signals how much currency is helping or hurting the reported result.

The buyback floor, the broker gap, and the longer-term build

Even after today’s 11.7% surge, Aristocrat trades at approximately A$51.59, well below broker consensus.

Consensus gap: The 12-month broker target of approximately A$62.47 implies roughly 21% further upside from the post-results price, with UBS targeting A$68.90 at the top end (dated 28 April 2026).

The buyback extension through May 2027 provides a structural capital return programme that creates ongoing demand for shares. For investors assessing downside risk, a $2.5 billion repurchase commitment is a meaningful consideration.

The thesis carries identifiable risks:

The US state-level iGaming legalisation tracker maintained by CasinoBeats identifies eight states where online casinos are currently legal and regulated, with several additional states actively weighing legislation, a pipeline that will directly shape the addressable market available to Aristocrat Interactive over the FY27-FY29 window.

- Currency translation: USD revenue dominance means AUD strength compresses reported earnings regardless of underlying performance.

- Interactive execution: Scaling a division to US$1 billion by FY29 involves multi-year execution risk across contract wins, market access, and regulatory approvals.

- US iGaming regulatory timeline: The pace of state-level iGaming legalisation in the United States will directly affect Aristocrat Interactive’s addressable market.

Aristocrat after May 13: capital discipline meets a long-horizon growth bet

The HY26 result carries a dual character. On one side sits capital discipline: a buyback programme expanded to $2.5 billion, an interim dividend up 13.6% to $0.50 per share, and nearly $1 billion already returned. On the other sits a long-horizon growth commitment: Aristocrat Interactive scaling toward US$1 billion by FY29, backed by verified contract wins in Europe and North America.

The franking credit value for Australian investors adds a layer to the dividend calculus that reported yield alone does not capture: a fully franked 50-cent interim dividend grosses up to a materially higher pre-tax equivalent depending on the investor’s marginal rate, which is relevant context for comparing Aristocrat’s income return against other ASX large-cap dividend payers.

The full-year FY26 result, expected in November 2026, will be the next major test of whether constant-currency guidance translates into reported earnings growth.

The question that will determine whether today’s share price surge looks prescient or premature in two to three years is whether Aristocrat can sustain the discipline of returning capital while investing enough in Interactive to hit the FY29 target, without one ambition compromising the other.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.