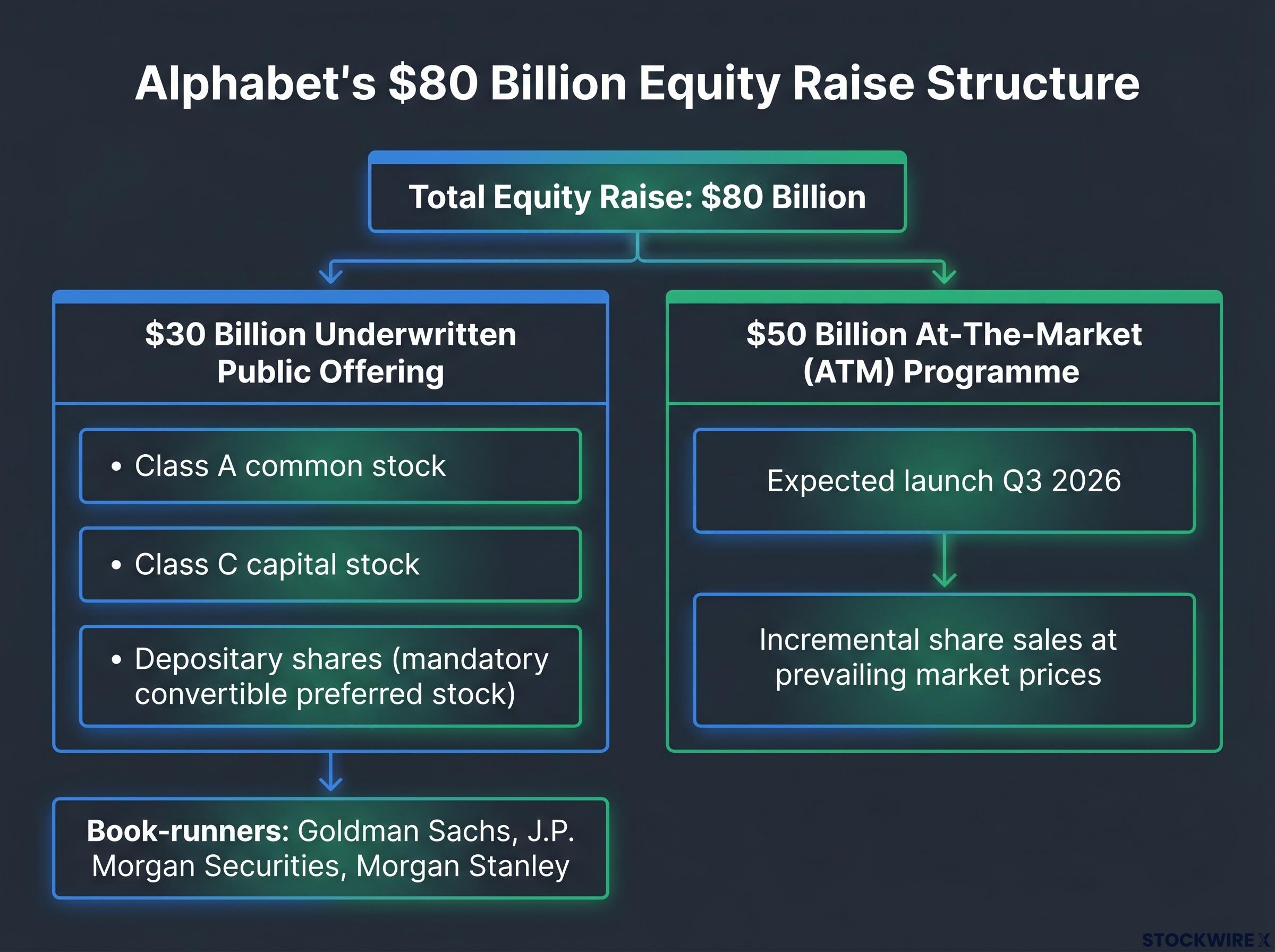

Alphabet announced on 1 June 2026 that it plans to raise $80 billion in equity capital, one of the largest equity fundraisings in United States corporate history, to close a compute supply gap the company says it cannot bridge fast enough with existing resources. The raise is structured in two parts: a $30 billion underwritten public offering and a $50 billion at-the-market programme expected to launch in Q3 2026. Goldman Sachs, J.P. Morgan Securities, and Morgan Stanley are acting as joint book-running managers. What follows breaks down how the deal works, why Alphabet chose equity over debt, what the capital will fund, and what the transaction signals about the scale of investment required to compete in AI infrastructure through the late 2020s.

A two-part deal: how Alphabet is structuring its $80 billion raise

The $30 billion underwritten public offering is the front-loaded component, structured across three securities:

- Depositary shares tied to mandatory convertible preferred stock

- Class A common stock

- Class C capital stock

Specific terms of the mandatory convertible preferred stock, including the dividend rate, conversion premium, and mandatory conversion date, were not disclosed in the offering announcement and would be detailed in Alphabet’s offering documentation.

The $30 billion underwritten offering operates in the primary market, where new shares are created and sold directly by the company to raise capital, a structurally different transaction from the secondary market trading activity that sets GOOGL and GOOG prices on any given day; the distinction between primary and secondary markets helps explain why even a large new issuance does not directly reprice existing shares through the exchange order book.

The second, larger tranche is a $50 billion at-the-market (ATM) programme expected to launch in Q3 2026. Unlike the underwritten offering, which prices and settles in a concentrated window, the ATM programme allows Alphabet to sell shares incrementally into the open market over time at prevailing prices. That flexibility means the company can match equity issuance to the pace of its infrastructure spending rather than raising the full amount upfront.

| Tranche | Key terms |

|---|---|

| $30B underwritten offering | Three components: depositary shares (mandatory convertible preferred), Class A common stock, Class C capital stock. Joint book-runners: Goldman Sachs, J.P. Morgan, Morgan Stanley. |

| $50B ATM programme | Incremental share sales at prevailing market prices. Expected launch Q3 2026. Flexible drawdown tied to infrastructure spending timeline. |

For investors tracking GOOGL and GOOG, the two-tranche structure matters because dilution is not concentrated in a single event. The underwritten offering delivers immediate dilution; the ATM spreads additional dilution across quarters.

When big ASX news breaks, our subscribers know first

What is an at-the-market offering and why do companies use it

An at-the-market offering is a registered programme that allows a company to sell new shares directly into the open market, in smaller increments, at whatever price the stock is trading at the time of each sale. There is no single pricing date and no block discount negotiated with institutional buyers.

The trade-offs between ATM programmes and traditional underwritten block offerings break down as follows:

- ATM programmes reduce execution risk by avoiding a single large block sale that can pressure the share price. They also eliminate the pricing discount typically required to attract buyers in a block deal. The trade-off is that dilution arrives gradually and unpredictably, making it harder for shareholders to model the exact impact on earnings per share in any given quarter.

- Traditional underwritten offerings concentrate dilution in one transaction, providing certainty for both the company and investors. The cost is a negotiated discount to the prevailing share price, which can be material for large raises.

Alphabet’s decision to use the ATM structure for the larger $50 billion portion of the raise, with a Q3 2026 launch, gives the company flexibility to draw down capital as its infrastructure spending accelerates rather than sitting on a $50 billion cash pile earning less than its cost of equity.

The demand problem Alphabet is trying to solve

Alphabet has stated that demand for its AI products from enterprise and consumer customers currently exceeds available computing capacity. That gap between what customers want and what the company can deliver is the named driver behind the $80 billion equity raise.

Google Cloud’s revenue trajectory provides the commercial justification for the capex commitment: the division reported $20 billion in quarterly revenue in Q1 2026, up 63% year-over-year, with a backlog exceeding $460 billion, figures that suggest the compute demand Alphabet is citing is already materialising in contracted enterprise revenue rather than sitting as speculative future demand.

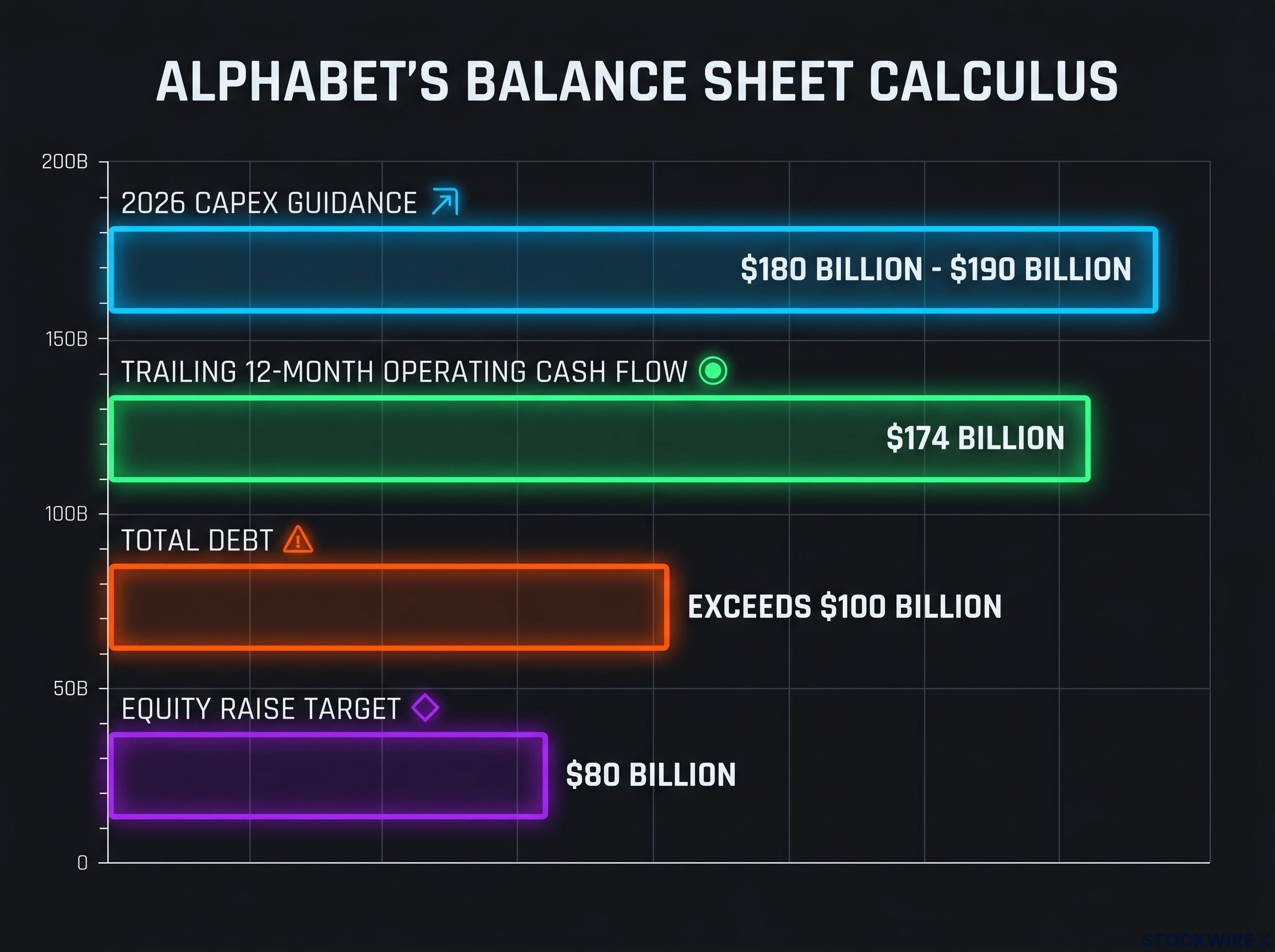

The scale of spending required to close that gap is substantial. Alphabet has guided 2026 capital expenditure to fall between $180 billion and $190 billion, with further increases projected for 2027, though a specific figure for the following year has not been disclosed.

2026 capital expenditure guidance: $180 billion to $190 billion. The equity raise represents one funding source within a multi-year infrastructure programme that extends into 2027 and beyond.

The $80 billion raise, then, is not the total cost of Alphabet’s AI buildout. It is one component layered on top of operating cash flow and existing resources to fund a programme whose total price tag runs into the hundreds of billions.

Where Alphabet’s spending sits in the hyperscaler arms race

Earnings-season coverage from 2023 to 2025 across Reuters, the Wall Street Journal, the Financial Times, and CNBC documents a broad AI infrastructure investment cycle among large U.S. cloud and social media platforms. Microsoft, Amazon, and Meta have all publicly guided to rising AI-driven capital expenditure across that period, with GPU data-centre spending increasing materially year on year.

No directly comparable single-year 2026 equity raise by Microsoft, Amazon, or Meta has been confirmed through available sources. Alphabet’s transaction stands out for both its scale and its structure within the current AI capital formation environment.

Hyperscaler capital expenditure across Amazon, Microsoft, Alphabet, and Meta collectively reached $130 billion in Q1 2026 alone, with combined full-year 2026 guidance approaching $725 billion, a figure that contextualises Alphabet’s $180-190 billion annual programme as one large but not outlying component of an industry-wide infrastructure commitment that analysts are projecting to approach $1 trillion annually by 2027.

Why equity and not more debt: Alphabet’s balance sheet calculus

Alphabet generates $174 billion in operating cash flow on a trailing twelve-month basis. That figure alone might suggest the company could fund its AI buildout internally, or borrow to cover the gap.

The constraint is the other side of the balance sheet. Alphabet carries total debt exceeding $100 billion. Adding further borrowings to an already substantial load would compound leverage risk, increase interest obligations, and potentially tighten covenant flexibility at a time when the company is committing to multi-year infrastructure spending with uncertain return timelines.

Alphabet stated that the equity offering is structured to support expansion while keeping the balance sheet in sound condition. Equity funding preserves financial flexibility without layering additional fixed costs onto a business that is simultaneously increasing capital expenditure by tens of billions of dollars per year.

NBER research on optimal financing for capital-intensive firms finds that companies combining high R&D intensity with uncertain long-duration project outcomes systematically favour equity over debt to preserve financial flexibility, a framework that maps closely onto Alphabet’s stated rationale for structuring the raise as it has.

| Metric | Figure |

|---|---|

| Operating cash flow (trailing twelve months) | $174 billion |

| Total debt | Exceeds $100 billion |

| Equity raise target | $80 billion |

The combination of strong cash generation and elevated debt explains why a company of Alphabet’s scale still needs to raise $80 billion externally: the infrastructure ambition outscales even substantial internal cash generation, and the existing debt load limits borrowing headroom.

What Alphabet’s $80 billion bet signals for the AI infrastructure era

An $80 billion equity raise to close a compute supply gap carries a signal that extends beyond Alphabet’s individual funding needs. AI infrastructure has crossed into a capital intensity regime where even the largest technology companies, generating hundreds of billions in annual cash flow, cannot self-fund the buildout from internal resources alone.

For investors tracking the AI infrastructure cycle, the implication is structural. Compute supply gaps at hyperscaler scale are now large enough to drive primary equity issuances of this magnitude, a development with consequences for share dilution, market supply of equity, and the competitive dynamics of the AI compute market. Capital formation at this scale was, until recently, associated with energy, mining, and telecommunications infrastructure rather than technology platforms.

AI capital intensity has crossed a threshold not seen in prior technology cycles: US IT hardware and software spending reached 4.9% of GDP in Q1 2026, surpassing the dot-com era peak of approximately 4.2%, a comparison that reframes the current buildout not as an extension of the cloud investment cycle but as a structurally distinct capital formation event with broader macroeconomic consequences.

What remains to be seen is whether the execution matches the ambition. The pace of ATM drawdowns from Q3 2026, the scale of 2027 capital expenditure when a specific figure is disclosed, and whether the resulting compute capacity additions actually close the demand gap Alphabet has described are all variables that will determine the return on this capital commitment. The $80 billion is committed. The compute is not yet built.

The bottom line on Alphabet’s AI capital raise

Alphabet is raising $80 billion in equity across two tranches, a $30 billion underwritten offering and a $50 billion ATM programme, to fund an AI infrastructure buildout driven by a compute supply gap. Capital expenditure for 2026 is guided at $180 billion to $190 billion, with further increases expected in 2027.

The decision to raise equity rather than additional debt reflects a balance sheet already carrying more than $100 billion in total debt alongside $174 billion in annual operating cash flow. Equity preserves flexibility; more borrowing would not.

The variables to watch from here are the ATM drawdown pace beginning in Q3 2026, the specific 2027 capex figure when disclosed, and whether the resulting infrastructure delivers enough compute capacity to close the gap that prompted this raise in the first place.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding capital expenditure, infrastructure deployment, and compute capacity are subject to change based on market developments and company performance.