Alphabet‘s Google DeepMind invented the Transformer architecture that makes ChatGPT, Claude, and every major large language model work. Yet Wall Street has largely priced the stock as if it were a search company facing disruption rather than the foundational layer of the AI era. With Q1 2026 revenues of $109.9 billion (up 22% year-over-year), Google Cloud surging 63% on AI demand, and a $180-190 billion capital expenditure programme underway, the Alphabet of mid-2026 looks structurally different from the company many investors think they own.

This analysis unpacks why 89% of covering analysts rate the stock a buy, what each of the company’s AI growth vectors represents in practice, and how the investment case differs from the semiconductor plays that dominate most AI portfolios.

The foundational AI argument most investors are missing

Google Brain, now merged into Google DeepMind, developed the Transformer architecture in 2017. That neural network design underpins GPT-4, Claude, and virtually every major large language model in commercial use today. The company that created the modern AI paradigm is still evaluated, by most of the market, primarily as an advertising business.

The Transformer architecture research from Google Brain, published in the 2017 paper “Attention Is All You Need” by Vaswani et al., introduced the attention mechanism that became the foundational design pattern for every major large language model in commercial use today, including GPT-4 and Claude.

The distinction matters for portfolio construction. Alphabet is not a pick-and-shovel semiconductor play in the mould of Nvidia or Broadcom. It is a vertically integrated AI company that trains its own models, designs its own chips (TPUs), runs its own cloud infrastructure, and deploys AI-native consumer products at scale across Search and Workspace. That structural position creates multiple simultaneous monetisation pathways rather than a single revenue dependency.

89% of covering analysts (59 of 66 surveyed by S&P Global) rate Alphabet a buy or strong buy, reflecting confidence in the breadth of that vertical integration.

At a market capitalisation of approximately $4.6 trillion and a gross margin of 60.43%, the stock’s 52-week range of $147.84 to $387.38 illustrates the market’s ongoing uncertainty about how to price the AI optionality embedded in the business. Investors who frame Alphabet purely as a search-at-risk company are evaluating the wrong denominator. Understanding the full vertical stack is the prerequisite for any serious position assessment.

When big ASX news breaks, our subscribers know first

How Google Cloud became the article’s most important number

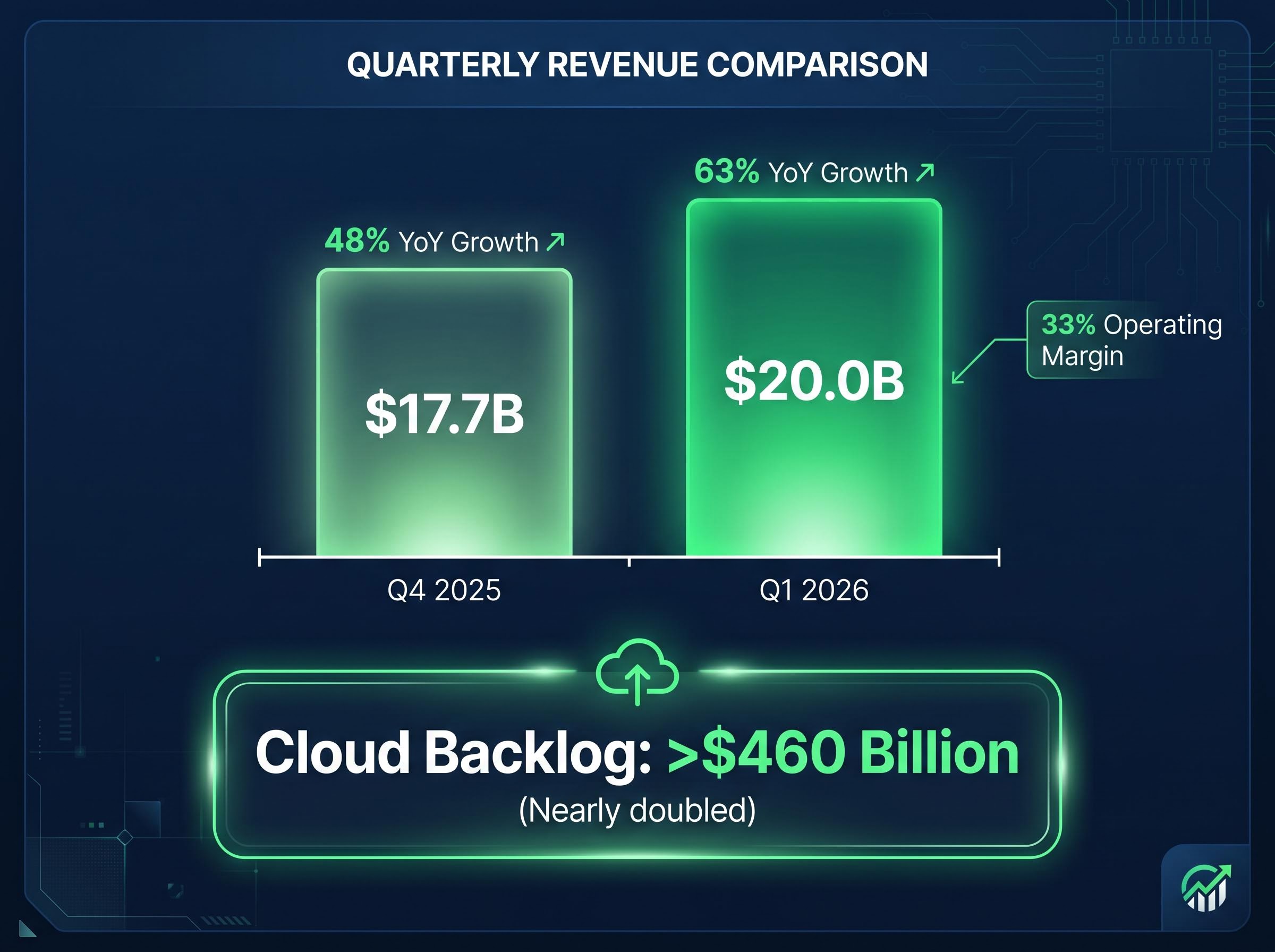

Google Cloud generated $20.0 billion in revenue during Q1 2026, up 63% year-over-year, with a 33% operating margin. No single figure in Alphabet‘s earnings report better captures the speed at which AI demand is reshaping the company’s revenue composition.

The growth is not a one-quarter anomaly. In Q4 2025, Cloud revenue reached $17.7 billion, representing 48% year-over-year growth. The sequential acceleration from 48% to 63% signals that enterprise AI adoption through Google’s infrastructure is compounding, not plateauing.

| Quarter | Cloud Revenue | YoY Growth | Operating Margin |

|---|---|---|---|

| Q4 2025 | $17.7B | 48% | N/A |

| Q1 2026 | $20.0B | 63% | 33% |

The engines behind this growth are Gemini model integrations across enterprise Workspace, Cloud AI infrastructure provisioning, and Gemini Enterprise licensing. Full-year 2026 capex guidance of $180-190 billion reflects the infrastructure investment required to sustain that trajectory.

What a $460 billion backlog actually signals

Cloud’s backlog, the value of contracted but not yet recognised revenue, nearly doubled to over $460 billion. This figure represents forward demand commitments from enterprise customers, not trailing performance.

A backlog doubling in roughly one year indicates that enterprise AI adoption is accelerating at the commitment level, not just the spending level. For investors evaluating AI cloud exposure, this forward-visibility metric positions Alphabet as a direct competitor to Amazon Web Services and Microsoft Azure in the enterprise AI buildout, with a growth rate currently exceeding both.

What Gemini is, what it is not, and why the distinction matters for the investment case

Gemini is Alphabet‘s family of multimodal AI models, developed by Google DeepMind and now integrated across multiple product surfaces. Understanding its role clarifies why Alphabet‘s AI monetisation is structurally different from OpenAI‘s or Anthropic‘s approach.

Gemini 3 and its variants, including Deep Think and Flash, rolled out in February 2026 with an emphasis on reasoning, multimodal processing across text, video, and audio, and enterprise AI integration. The model family is not a standalone product competing for benchmark supremacy. It is an integration-and-distribution play, embedded across:

- Search: AI-enhanced query processing and results generation

- Workspace: Enterprise productivity tools with native AI capabilities

- Google Cloud: Infrastructure-level AI services for enterprise customers

- Gemini Enterprise licensing: Direct subscription revenue through Cloud

Alphabet reports Gemini processes over 16 billion tokens per minute (note: self-reported and not independently verified), indicating the operational scale of deployment across its product surfaces.

The competitive distinction matters for the investment case. Where OpenAI and Anthropic compete primarily on model capability benchmarks, Alphabet‘s advantage is integration depth and distribution scale across products that already have billions of users. Gemini monetisation flows directly into the Cloud growth story: every Gemini Enterprise licence is Cloud revenue.

Cloud remaining performance obligations across Alphabet, Microsoft, and Amazon tripled from $596 billion in Q1 2025 to $1.5 trillion in Q1 2026, the forward demand signal that prompted BCA Research to upgrade Communication Services to overweight and name Alphabet as one of its two preferred stock-level expressions of the AI capex thesis.

Waymo and quantum computing as long-horizon optionality the market may be underpricing

Neither Waymo nor Google Quantum AI features in most analyst consensus models. For investors with a multi-year holding period, that absence represents asymmetric upside: any material commercialisation of either positions adds value that current pricing does not account for.

Waymo’s ride volume trajectory

Waymo reached approximately 500,000 rides per week in early 2026, roughly doubling from approximately 250,000 a year prior. The company’s stated target is 1 million weekly rides by the end of 2026, which would make it the only autonomous ride-hailing service operating at that scale in the United States.

Waymo investments contributed to a slight operating margin dip in Q4 2025. That near-term cost reflects the capital required to scale fleet operations and geographic coverage while the service approaches commercial self-sufficiency.

Quantum AI’s path from research to commercial access

Google Quantum AI is accepting proposals for early access to its Willow quantum processor, with a submission deadline of 15 May 2026. This moves the programme from pure research into structured commercial and academic engagement with the hardware.

The broader quantum computing market is projected at approximately $3 billion. Google Quantum AI has expanded its hardware approach into neutral atom computing alongside superconducting qubits, and has published a six-milestone roadmap covering hardware and software development. That structured roadmap signals a commercialisation intent, not indefinite research spending.

- Waymo: Operational scale doubling annually, targeting 1 million weekly rides by year-end. Near-term margin drag reflects scaling costs for a future revenue stream.

- Quantum AI: Willow early access programme signals transition from research to commercial engagement. Six-milestone roadmap provides measurable development checkpoints.

Reading the Q1 2026 earnings with clear eyes: the adjusted picture underneath the headline numbers

Alphabet reported Q1 2026 net income of $62.58 billion, a headline figure that demands immediate context. Approximately $36.9-$37.7 billion of that total came from a one-time gain on non-marketable equity securities, a non-operating windfall that inflated the reported number well beyond what core operations produced.

The gap between reported and adjusted earnings per share tells the real story.

| Metric | Reported Figure | Analyst Consensus | Delta |

|---|---|---|---|

| Revenue | $109.9B | $107.2B | +$2.7B beat |

| Reported EPS | $5.11 | N/A (includes one-time gain) | N/A |

| Adjusted EPS | $2.62 | $2.63 | –$0.01 miss |

Adjusted EPS of $2.62 marginally missed consensus of $2.63, a result that reflects solid but not spectacular core performance once the equity gain is stripped out. The capex guidance adds further nuance: $35.7 billion in Q1 alone and $180-190 billion for the full year compresses near-term free cash flow and represents the primary source of analyst caution.

The Q1 2026 earnings divergence across the hyperscaler group illustrated precisely why capex guidance now moves individual stock prices more than revenue beats: Meta fell more than 9% on the same day Alphabet surged to an all-time high, despite both companies posting strong top-line growth.

Bank of America raised its price target to $430 (from $370) following the Q1 report, while CMB International maintained its Buy rating with a $425 target. The consensus average 12-month price target sits at approximately $351.73.

The market appears to be resolving its uncertainty in Alphabet‘s favour. Shares rose 23.03% year-to-date as of 30 April 2026, outperforming the Nasdaq. Investors who evaluate only the headline EPS will either overpay on euphoria or dismiss the operational strength. The adjusted picture shows a company with strong core momentum executing an expensive but arguably necessary infrastructure bet.

Why Alphabet sits in a different category from Nvidia and Broadcom for AI investors

The most common portfolio error in AI investing is treating all AI exposure as interchangeable. Alphabet, Nvidia, and Broadcom occupy fundamentally different positions in the AI value chain, and understanding that distinction determines whether adding one duplicates or diversifies an existing AI allocation.

| Company | Market Cap | Gross Margin | Analyst Buy Rating | Primary AI Revenue Driver |

|---|---|---|---|---|

| Alphabet | ~$4.6T | 60.43% | 89% (59/66) | Cloud, Gemini, Search, Waymo |

| Nvidia | ~$4.8T | 71.07% | 95% (56/59) | GPU silicon, CUDA ecosystem |

| Broadcom | ~$2.0T | N/A | 94% (44/47) | Custom ASICs, AI networking |

Nvidia and Broadcom are infrastructure-layer plays. Their revenue depends on other companies building AI systems. Alphabet both builds AI infrastructure and deploys it in revenue-generating products at scale. This carries different risk exposures: less dependence on hyperscaler capex cycles, more exposure to search revenue competitive pressure, but also greater positioning to benefit from AI-enhanced search and productivity monetisation.

Nvidia’s valuation discount relative to its Magnificent Seven peers sits at roughly half the forward P/E of the group average despite projected free cash flow exceeding $400 billion across 2026-2027, a gap that Bank of America analysts attribute to a capital return policy that structurally excludes income-mandate funds from the register rather than to any deficiency in the underlying AI growth story.

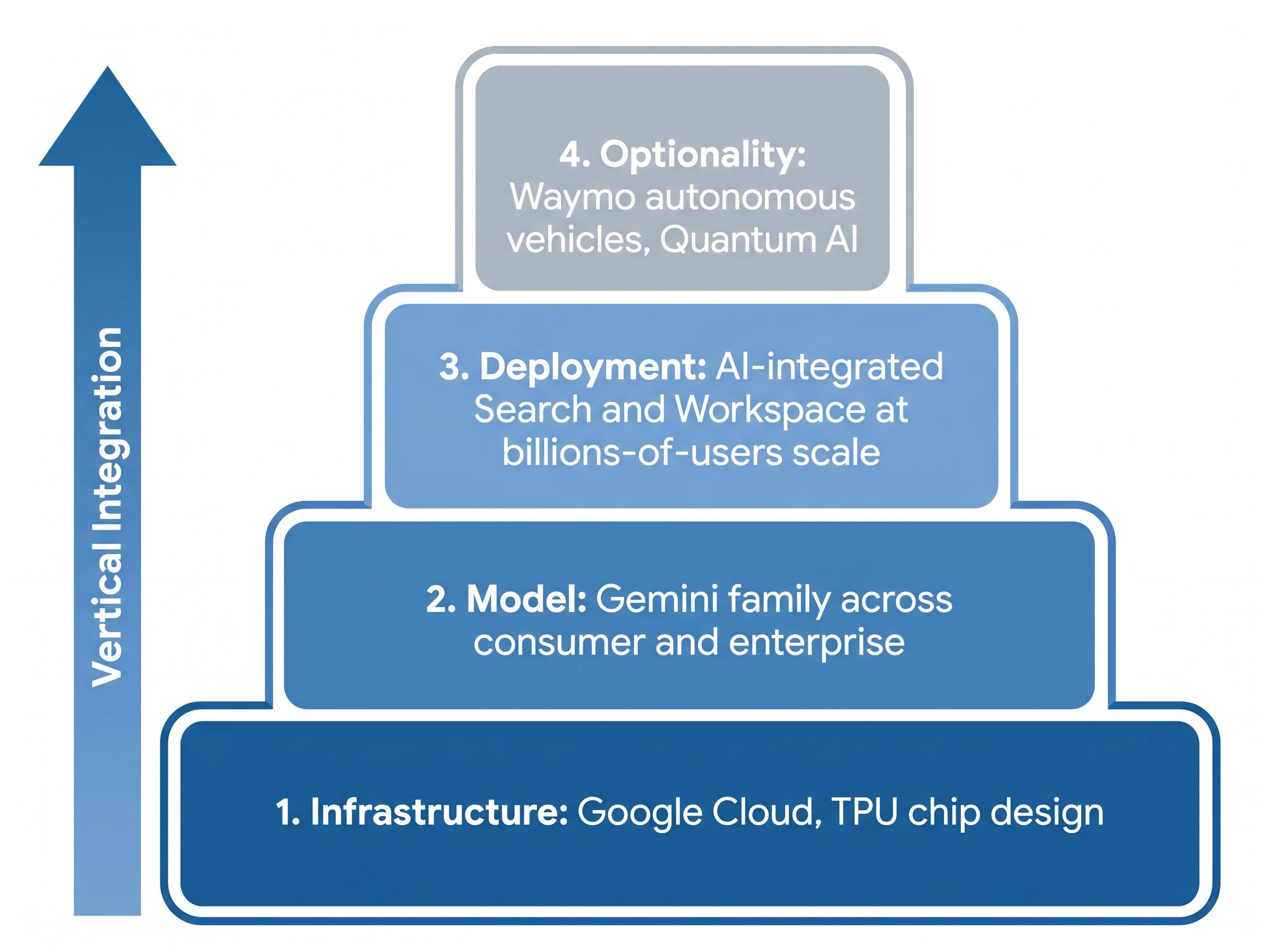

Within a single stock, Alphabet offers four distinct AI exposure categories:

- Infrastructure: Google Cloud, TPU chip design

- Model: Gemini family across consumer and enterprise

- Deployment: AI-integrated Search and Workspace at billions-of-users scale

- Optionality: Waymo autonomous vehicles, Quantum AI

The 89% analyst buy rating and 0.22% dividend yield reflect Wall Street’s current view. That consensus is context, not a conclusion. The reader’s own assessment of whether the capex trajectory and competitive risks align with their time horizon and risk tolerance determines whether the positioning argument translates into an allocation decision.

The investment verdict: a stock that rewards investors who understand what they own

The Q1 2026 results validate the structural argument that Alphabet is being re-rated from a search company to a multi-vector AI company. Cloud growth of 63%, a backlog that nearly doubled, and a revenue beat of $2.7 billion over consensus represent tangible evidence, not forward speculation.

The primary risks are equally tangible:

- Capex ROI uncertainty: $180-190 billion in annual infrastructure spending with a return timeline that is not yet fully visible

- Search revenue competitive pressure: AI-native competitors could erode the core advertising business that still funds the broader AI investment

- Regulatory exposure: Antitrust and data privacy scrutiny across multiple jurisdictions

The sustainability question around hyperscaler debt-funded capex intensified after the four major cloud operators collectively issued $121 billion in debt during 2025, approximately four times their five-year average, with a further $100 billion projected in 2026, raising structural questions about whether the infrastructure build-out can be sustained without material balance sheet deterioration.

The DOJ antitrust remedies against Google, confirmed in September 2025 following the August 2024 monopolisation ruling, represent the most concrete regulatory risk in Alphabet’s current profile, with structural remedies potentially affecting the search distribution agreements that underpin its core advertising revenue.

For investors evaluating where Alphabet fits in an AI-weighted portfolio, the differentiation from semiconductor peers is the actionable insight. This is not another infrastructure-layer bet. It is a vertically integrated operator with exposure across every layer of the AI value chain, from foundational research to consumer deployment, trading at a 60.43% gross margin.

The 89% analyst consensus reflects broad institutional confidence, but it is not a substitute for assessing whether the company’s risk profile and capex trajectory align with individual time horizons and portfolio objectives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.