Two Vanguard ETFs sit on the ASX with growth-oriented mandates and familiar branding. But choosing between VDHG and VISM, or deciding whether to hold them together, is not a matter of picking the better fund. It is a matter of understanding what role each one plays and whether that role fits your portfolio.

Australian ETF investment flows are running at record pace in mid-2026, and VDHG remains one of the most widely held funds among long-term retail investors. VISM attracts a different kind of buyer: one already running a multi-ETF strategy and looking to add targeted small-cap international exposure. The practical question is not which fund is superior in isolation, but which structure suits the investor’s actual situation.

Here is a framework for placing each fund in its correct portfolio role, including the structural overlap most investors miss, so you can make a grounded allocation decision rather than defaulting to a vague “it depends.”

Two ETFs designed for different jobs

Before comparing fees, volatility, or holdings, the distinction that matters most is design intent. These two funds were built for entirely different purposes, and evaluating them side by side as if they occupy the same portfolio slot produces the wrong answer every time.

What VDHG holds

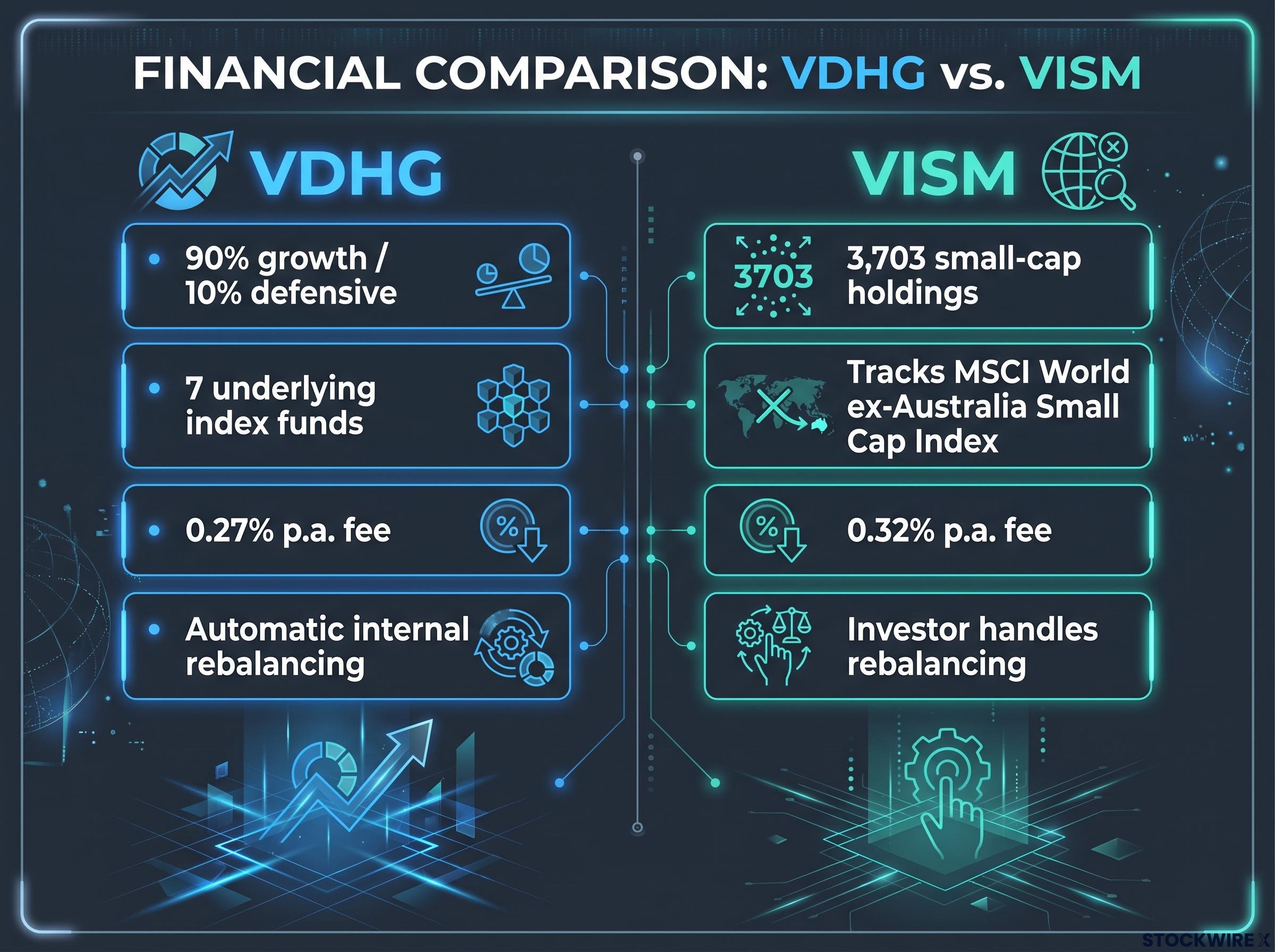

VDHG is a complete portfolio solution, not a building block. It holds seven underlying Vanguard index funds spanning:

- Australian shares

- International shares (hedged)

- International shares (unhedged)

- Emerging markets

- Global small companies

- Australian bonds

- Global bonds

At target weights, the fund allocates approximately 90% to growth assets (shares) and 10% to defensive assets (bonds). Vanguard handles all internal rebalancing, currency-hedging decisions, and capital allocation between sleeves. The investor’s only job is to buy and hold.

VDHG’s fund-of-funds structure means the 0.27% fee covers not just one index but seven underlying Vanguard funds, with Vanguard managing currency-hedging decisions and allocation drift across all sleeves simultaneously.

What VISM holds

VISM is a single-purpose exposure. It tracks the MSCI World ex-Australia Small Cap Index, holding approximately 3,703 smaller-capitalisation companies across developed markets outside Australia. There are no bonds, no Australian shares, and no large-cap anchor.

- Targeted exposure to international small caps only

- Excludes Australian-listed companies entirely

- Requires an existing diversified portfolio to function as intended

Using VISM without a diversified core already in place creates significant concentration risk. That is the framing to carry into every section that follows: this is a portfolio-architecture question, not a performance horse race.

When big ASX news breaks, our subscribers know first

Risk profiles and what volatility actually looks like for each fund

Both funds carry meaningful equity risk, but they do not carry the same amount of it.

VDHG behaves like a high-growth diversified fund. Investors should expect equity-style drawdowns during bear markets, partially cushioned by the approximately 10% bond allocation. That bond sleeve does not eliminate losses; it softens them at the margins.

VISM carries higher volatility again. Smaller companies tend to react more sharply to tightening credit conditions, deteriorating growth expectations, and swings in market risk appetite. Price swings can be sharper than those seen in broad large-cap global ETFs, and drawdowns tend to cut deeper before recovery.

VISM does not reduce portfolio volatility relative to VDHG. It increases it. Adding VISM to a portfolio that already holds VDHG raises total equity risk and sharpens sensitivity to the small-cap segment specifically.

Both funds require a long time horizon for the growth premium to emerge. VISM particularly suits a 7-10 year minimum horizon, giving small-cap cycles enough room to play out. If recent equity drawdowns made you uncomfortable, VISM amplifies that experience rather than diversifying away from it.

The overlap most VDHG investors do not know about

Here is the nuance that changes the “should I add VISM?” question entirely.

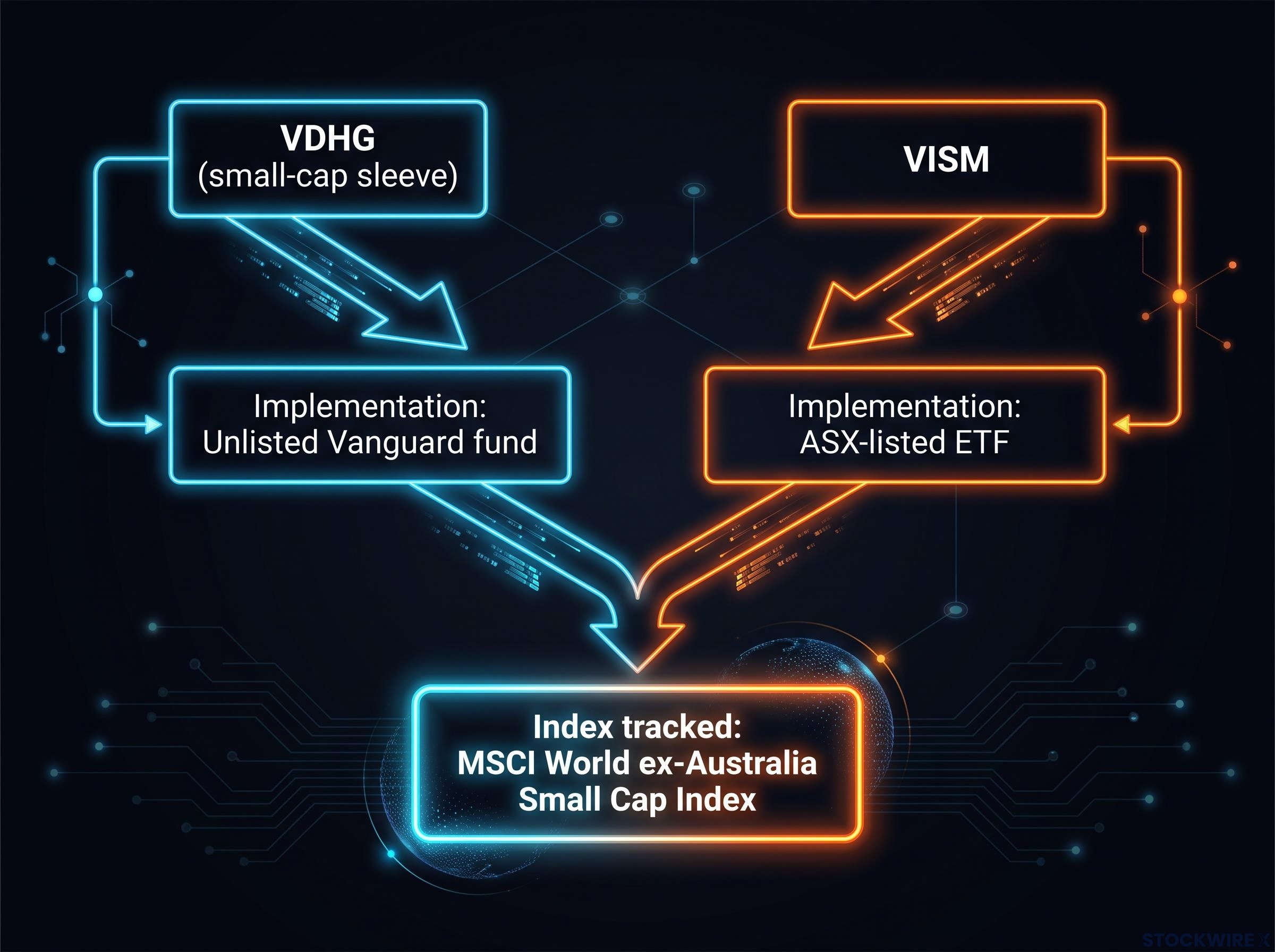

VDHG’s “global small companies” sleeve is not some vaguely related allocation. It is implemented through the Vanguard MSCI International Small Companies Index Fund (an unlisted fund), which tracks the same MSCI World ex-Australia Small Cap Index that VISM itself tracks.

VISM the listed ETF is not a direct holding inside VDHG. But the underlying index exposure is equivalent. The two products access the same small-cap universe through different wrappers.

| ETF | Index tracked by small-cap sleeve | Implementation |

|---|---|---|

| VDHG (small-cap sleeve) | MSCI World ex-Australia Small Cap Index | Unlisted Vanguard fund |

| VISM | MSCI World ex-Australia Small Cap Index | ASX-listed ETF |

What this means in practice: an investor adding VISM on top of VDHG is increasing concentration in the same index segment, not adding an uncorrelated new asset class. For VDHG holders considering VISM, this is not a free diversification upgrade. It is a deliberate decision to overweight a specific factor that VDHG already expresses at a moderate level.

The quality factor is the critical variable investors miss when evaluating passive small-cap indexes: broad small-cap benchmarks carry a structural tilt toward unprofitable companies, meaning the index VISM tracks does not automatically deliver the size premium that academic research describes.

Fees, complexity, and what each fund actually costs the investor

The headline fee difference between these two funds is modest. What is not modest is the difference in ongoing management effort they demand.

| ETF | Management fee | Rebalancing responsibility |

|---|---|---|

| VDHG | 0.27% p.a. | Vanguard (internal, automatic) |

| VISM | 0.32% p.a. | Investor (manual, ongoing) |

The five basis point gap is largely irrelevant to the decision. What matters is the total cost of ownership, and for VISM holders that cost extends well beyond the management fee.

VDHG’s 0.27% fee covers all internal rebalancing across seven underlying funds, including currency-hedging decisions between hedged and unhedged international sleeves. The investor pays once and Vanguard handles the ongoing structural work.

VISM at 0.32% covers only the small-cap exposure itself. The investor must then decide how much to allocate, how VISM fits alongside other ETFs such as VGS, VGAD, VGE, and VAS, and when to rebalance. That is an ongoing time and decision cost that compounds over years. Investors who underestimate the complexity of a multi-ETF strategy often end up with a fragmented portfolio that underperforms a simpler approach, not because the funds were wrong but because rebalancing inertia or emotional decision-making during drawdowns eroded the structural advantage.

Portfolio rebalancing in a multi-ETF structure is not a one-time event: investors holding VISM alongside a core fund must define a drift threshold, select a tax-efficient execution order, and commit to reviewing the split at least quarterly to prevent the small-cap satellite from growing outside its intended weight.

The next major ASX story will hit our subscribers first

Matching each fund to the investor profile it was built for

Every section so far has built toward a single practical question: which profile fits you? Here are three distinct investor scenarios, each with a clear set of defining characteristics.

- The VDHG investor

- Prioritises simplicity and wants a single instrument to hold for decades

- Accepts Vanguard’s fixed 90/10 growth-to-defensive allocation without wanting to customise individual sleeves

- Prefers automatic rebalancing and currency-hedging decisions handled internally

- Values time saved over granular portfolio control

- The VISM investor

- Already holds broad global equity exposure through a core ETF or multi-fund structure

- Has a high risk tolerance and is comfortable with sharper small-cap drawdowns

- Is investing over a 7-10 year minimum horizon, giving the small-cap growth premium time to emerge

- Is willing and able to manage allocation decisions, rebalancing, and trimming actively

- The “both funds” investor

- Uses VDHG as the diversified core and adds VISM as a deliberate small-cap satellite tilt

- Understands this increases total equity risk and concentrates exposure in the international small-cap segment VDHG already covers at a moderate level

- Has defined a target split (for example, 80% VDHG and 20% VISM) and commits to maintaining and rebalancing that split over time

- Treats the combination as a conscious factor overweight, not a diversification upgrade

The “both” scenario is not an upgrade for VDHG holders by default. It is a deliberate increase in small-cap concentration and total equity risk that suits only investors who understand and accept that outcome.

What the data tells you before committing to either fund

The choice between VDHG and VISM is not a competition between two products. It is a choice between two portfolio architectures. VDHG offers a fully managed solution: 90% growth assets, 0.27% p.a., seven-fund diversification, and internal rebalancing included. VISM offers a targeted building block: 3,703 small-cap holdings across developed markets outside Australia, 0.32% p.a., and investor-managed allocation.

The index overlap between VDHG’s small-cap sleeve and VISM’s tracked index means that holding both is a factor tilt, not a diversification event. That distinction should shape how you think about it.

Before committing, assess these variables against your own situation:

- Your tolerance for portfolio complexity and ongoing rebalancing work

- Whether you already hold broad equity exposure or are starting from scratch

- Your genuine capacity to sit through small-cap drawdowns without selling

- Your investment time horizon, particularly whether it extends beyond seven years

If you would not confidently explain the difference between VDHG’s small-cap sleeve and VISM’s index to another investor, VDHG alone is the right starting point.

For investors new to VDHG who want a side-by-side fee, return, and tax treatment comparison before committing, our dedicated guide to VDHG for beginners sets out how it compares to IVV and VAS across the variables that matter most in the first years of building a portfolio.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

For investors whose situation involves existing concentrated holdings, tax considerations, or retirement planning, a licensed financial adviser can help tailor the decision to your specific circumstances.

—