Australia has no NVIDIA, no Microsoft, no Alphabet. The companies building and commercialising AI at scale are overwhelmingly listed overseas, which means the most consequential investment question for you as an Australian investor right now is not whether to own AI exposure, but how to access it without taking on more risk than you intended.

The ASX offers a growing menu of ETFs spanning broad index funds with embedded AI exposure through to concentrated semiconductor and robotics funds with triple-digit three-year returns and the volatility to match. The gap between these options is enormous. The wrong choice for your circumstances can mean either missing the theme entirely or sitting through a 40% drawdown you were not prepared for.

This guide maps the full spectrum of AI-accessible ETFs available to Australian investors across four distinct risk levels, explains the trade-offs at each tier, and gives you a practical framework for deciding which vehicle, or which combination, belongs in your portfolio. The goal is to match your conviction and risk tolerance to the right instrument, so the decision becomes a considered one rather than a reactive one.

Why AI investment today differs from the dot-com era

You have probably already made the comparison in your head. A new technology, breathless coverage, soaring share prices. It is natural to wonder whether this is the late 1990s again.

The structural difference is worth understanding, because it changes how you think about the risk you are taking. Listed AI ETFs today predominantly hold large, profitable companies already monetising AI across cloud, chips, software and services. Microsoft, Alphabet, NVIDIA and Amazon are not pre-revenue concepts chasing clicks. They are generating material AI-linked revenue from products millions of businesses and consumers already use.

AI ETFs today hold companies already monetising the technology at scale, not pre-revenue concepts reliant on narrative. That distinction changes your base case for loss, even if it does not guarantee gain.

That said, pockets of AI hype and overvaluation exist today, just as they did in the late 1990s. The correct macro thesis does not guarantee good timing or good outcomes. What happened with lithium and EV-linked ETFs on the ASX is instructive: investors who held concentrated thematic positions found that being broadly right about battery metal demand still left them exposed to severe losses once commodity prices fell back to earth.

The dot-com era parallel is instructive here: being correct about a transformative technology did not translate into correctly identifying the winning companies, and ASX investors who picked individual AI stocks in 2025 and 2026 were reminded of this when names like Appen fell nearly 30% in a single session.

The takeaway is not fearlessness or dismissiveness. It is calibration. The structural quality of today’s AI leaders lowers the floor compared to dot-com-era narrative stocks, but it does not remove the risk of overpaying or over-concentrating at the wrong point in a cycle.

When big ASX news breaks, our subscribers know first

Level 1: Broad index ETFs and the AI exposure you may already own

Here is something that catches many investors off guard: if you already hold a broad global or US index ETF, you have meaningful AI exposure right now without ever making a deliberate thematic bet.

Megacap AI leaders dominate global developed-market and US large-cap indices by market capitalisation. That means broad index ETFs carry substantial AI exposure through simple index mechanics, not through any deliberate thematic tilt by the fund manager.

- VGS-style global developed-market funds offer the broadest diversification, covering equities across the US, Europe, Japan, the UK and other developed markets. Top holdings include Apple, Microsoft, Alphabet and NVIDIA. AI is one growth driver among many.

- IVV-style S&P 500 trackers are more concentrated in the US economy, where most commercial AI investment is occurring. Market-cap weighting naturally tilts toward Microsoft, Apple, Alphabet, Amazon, Meta and NVIDIA. The AI exposure is heavier, but it is still embedded within a 500-company index.

The real question is whether the concentration of that exposure matches your conviction level. If your view is simply that AI will be economically important over the long run, a broad index ETF may already give you what you need without adding complexity.

| Characteristic | VGS-style (Global Developed) | IVV-style (S&P 500) |

|---|---|---|

| Focus | Global developed markets | 500 largest US companies |

| Diversification level | Very high (multi-country) | High (US-only, multi-sector) |

| AI exposure mechanism | Market-cap weighting includes AI leaders as part of broad mix | Market-cap weighting naturally overweights US tech giants |

| Suitable investor profile | Long-term core portfolio, AI as one driver among many | Core portfolio with a deliberate US tilt |

Level 2: NASDAQ and megacap technology ETFs for a deliberate AI tilt

When you step from a broad index ETF to a NASDAQ 100 tracker, you are making a deliberate decision to overweight technology. That is a different type of bet, and it comes with a different type of volatility.

The BetaShares NASDAQ 100 ETF (NDQ) tracks approximately 100 of the largest NASDAQ-listed non-financial companies, heavily dominated by Microsoft, Alphabet, NVIDIA, Meta, Apple and Amazon. As at May 2026, NDQ was the largest AI-adjacent ETF on the ASX with approximately $8.96 billion in assets under management, a 0.48% management fee, and a three-year return of approximately +88.8%.

NDQ three-year return: approximately +88.8%. Past performance does not indicate future results. This figure reflects a period of exceptional technology outperformance that may not repeat.

That +88.8% figure is real, but it also tells you this fund can move sharply in either direction. Performance is closely tied to tech sentiment and earnings cycles. If the next cycle disappoints, drawdowns will be steeper than those in a broad index.

At the extreme end of this level sit highly concentrated megacap baskets, such as FANG-style ETFs holding roughly 10 major technology names including Alphabet, Microsoft and Tesla. Return profiles are more extreme in both directions, and Tesla’s inclusion adds EV and energy-transition risk alongside AI exposure.

Key differences between NASDAQ-level ETFs and broad index funds:

- Concentration: Fewer companies, dominated by technology

- Sector tilt: Deliberately overweights tech; underweights financials, healthcare, industrials

- Volatility profile: Higher drawdowns during tech-led selloffs

- Appropriate portfolio role: Satellite allocation around a diversified core, not a standalone holding

If you are entering now, do not anchor to recent history as a baseline for future expectations. The question is whether you have the risk tolerance for what these funds do during their bad periods, not just what they have delivered during their best ones.

Level 3: Pure-play AI, robotics and semiconductor ETFs

This is where the menu gets specific and the risk profile gets narrow. Three distinct sub-themes sit at this level, and understanding what each actually bets on matters more than the headline performance numbers.

AI and robotics thematic ETFs target companies whose revenue is tied directly to the AI and automation theme:

- RBTZ (BetaShares Global Robotics and Artificial Intelligence ETF) covers industrial robotics, humanoid technology, unmanned vehicles and drones.

- ROBO (Global X ROBO Global Robotics and Automation ETF) offers a broader basket of automation and robotics names, including mid and small caps.

- GXAI (Global X Artificial Intelligence ETF) focuses on companies that develop or directly benefit from AI technologies, with a strong information technology sector tilt.

Both GXAI and AINF are relatively new and lack long performance track records, which limits the historical data available to assess how they behave through different market conditions.

AI infrastructure and semiconductor funds

AINF (Global X AI Infrastructure ETF) targets the physical and cloud infrastructure required to run AI at scale: data centres, networking, chip fabrication and related services. Its performance is tied to capital expenditure cycles in AI and cloud, adding a cyclical layer on top of thematic risk.

Hyperscaler capital expenditure commitments from the four largest AI companies sit at approximately $725 billion for 2026, with 70-75% directed at infrastructure, which is the structural demand signal underpinning SEMI’s approximately 51% year-to-date return and AINF’s infrastructure-layer positioning.

SEMI (Global X Semiconductor ETF) is the most concentrated bet in this category. Dedicated to semiconductor manufacturers including NVIDIA, TSMC, ASML, AMD and Broadcom, SEMI delivered approximately +269.7% over three years from mid-2023 to May 2026, driven by explosive demand for AI chips.

That +269.7% return tells you this is the most AI-specific bet available on the ASX. It also tells you this is the most concentrated single-cycle risk. Chip demand and pricing can swing sharply, and sector-specific ETFs at this level can fall 30-50% in a downturn. The question is not whether the AI chip theme is real. It is whether a 50% drawdown in chips would cause you to sell.

| ETF | Sub-theme focus | Diversification within theme | Risk level |

|---|---|---|---|

| RBTZ | Industrial robotics, drones, humanoid tech | Moderate (global robotics names) | High |

| ROBO | Broad automation and robotics | Higher (includes mid and small caps) | High |

| GXAI | AI software and services | Moderate (IT sector tilt) | High (limited track record) |

| AINF | Data centres, networking, cloud infra | Moderate (infrastructure layer) | High (limited track record, cyclical) |

| SEMI | Semiconductor manufacturers | Low (concentrated in chip giants) | Very high (cyclical, single-sector) |

These products are designed as small satellite allocations for investors with specific sub-theme conviction. They are not core holdings and they are not a substitute for general AI exposure.

Level 4: Commodity and resource ETFs as indirect AI infrastructure plays

At this level, you are no longer betting on AI companies or their earnings. You are betting on the physical inputs AI requires, with commodity price cycles doing most of the work in between.

WIRE provides exposure to copper mining companies. Copper plays a role in data centre wiring, electricity grid upgrades and electrified transport, all of which expand as AI infrastructure scales. XME covers a basket of lithium, nickel, cobalt and related metals that support batteries, EVs and modern electrical grids, themes that overlap with AI’s growing energy demands.

When lithium prices collapsed after the early EV boom, Australian investors holding concentrated positions in battery metals funds were reminded that getting the underlying demand story right offers no protection when commodity cycles turn. A compelling technology narrative and a profitable investment are two different things.

If you are drawn to resource ETFs as an AI play, the honest framing is that you are making a commodity bet that benefits if AI infrastructure build-out drives materials demand. Commodity cycles have historically been indifferent to how compelling the underlying tech narrative is.

Four risk drivers specific to this level are absent from equity AI ETFs:

- Commodity price cycles: Supply and demand for the raw material, not the technology, drives returns

- Mining operational risk: Project delays, cost overruns and geological uncertainty

- Geopolitical factors: Trade policy, export controls and resource nationalism

- Currency movements: AUD/USD fluctuations affect returns on USD-denominated assets in both directions

These are speculative, theme-driven allocations suitable only for investors with a genuine view on resource demand and comfort with commodity volatility. They are not AI investments in the conventional sense.

Building your AI portfolio: the core-satellite approach for Australian investors

Knowing the products is one thing. Knowing how to combine them is where the decision actually gets made. The core-satellite structure gives you a practical framework for fitting these levels together.

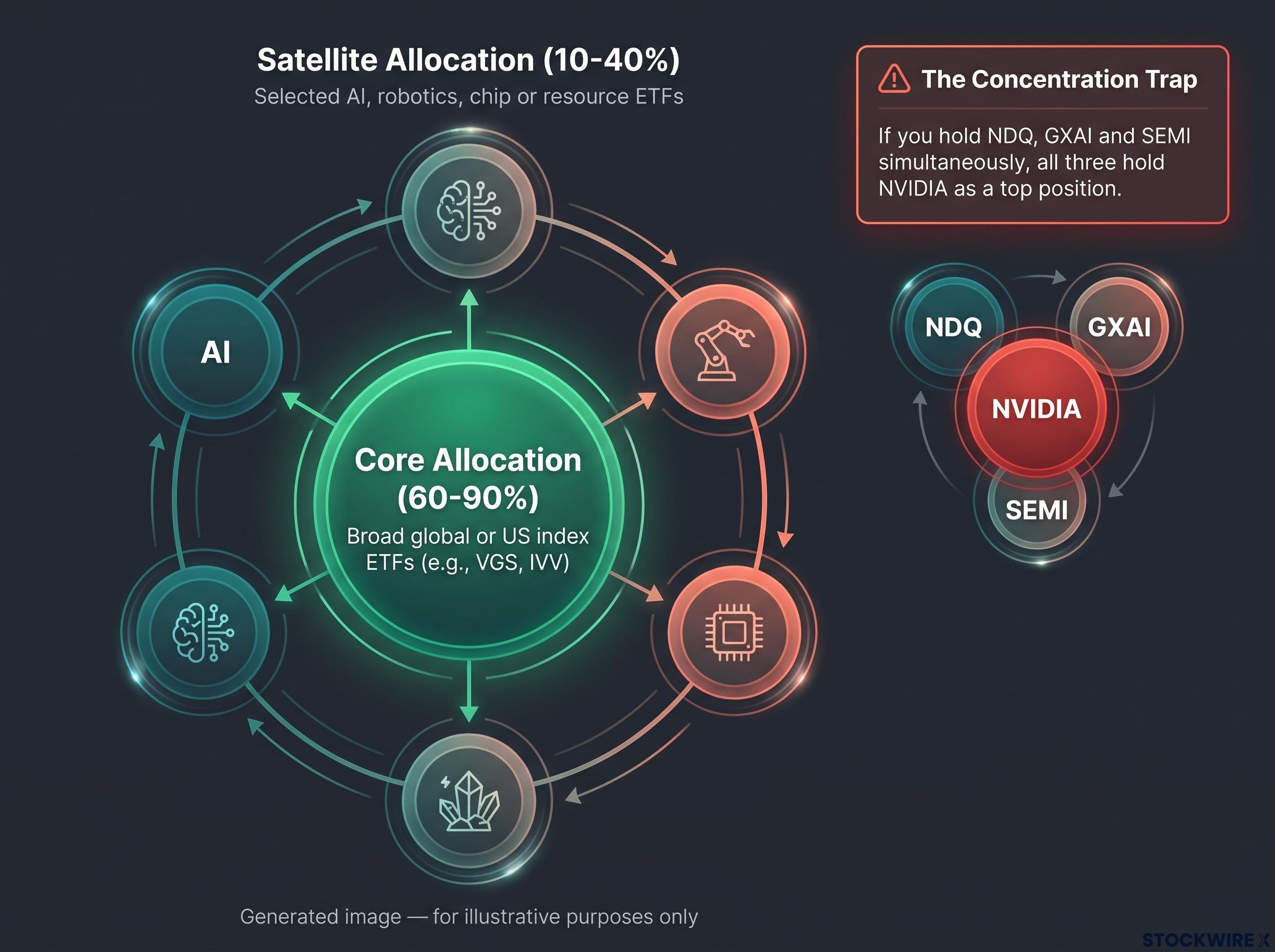

The core-satellite framework allocates 70-90% of the portfolio to broadly diversified, low-cost ETFs and reserves 10-30% for targeted, thesis-driven satellite positions, a structure that also requires answering three discipline questions for every satellite: what thesis does it express, why does the core not already capture it, and over what time horizon must the thesis play out.

- Assess your conviction level. If your view is simply that AI will matter economically over the long run, Levels 1-2 are typically sufficient. If you have a specific thesis about chips, robotics or infrastructure, Level 3 satellites can express that view more precisely.

- Match your risk tolerance to the drawdown test. Ask yourself whether you would hold through a 40% drawdown. If not, limit exposure to concentrated themes and stay closer to Levels 1-2.

- Define your core-satellite split. A common approach is 60-90% in broad global or US index ETFs as the core, with 10-40% spread across selected AI, robotics, chip or resource ETFs aligned with your thesis. The same thematic ETF has very different portfolio implications at 5% versus 50% of your holdings.

- Address Australian-specific mechanics before executing.

Australian-specific mechanics that affect every ETF choice:

- Currency exposure: Most ASX AI and technology ETFs hold USD-denominated assets; AUD/USD movements affect your returns in both directions

- Tax treatment: Distributions are generally taxable as income; capital gains apply when you sell units; international ETFs rarely provide franking credits

- Execution platforms: Major brokers including CommSec, SelfWealth and Stake provide access to BetaShares, Global X, Vanguard and iShares ETFs on the ASX

- Dollar-cost averaging: Regular, fixed-amount investing can reduce the risk of allocating a lump sum at a local peak in a volatile theme

The size of your AI satellite allocation matters as much as the vehicle you choose. A highly volatile ETF at 5% of your portfolio is a considered bet. The same ETF at 40% is a concentrated risk that can define your outcomes regardless of how the rest of your holdings perform.

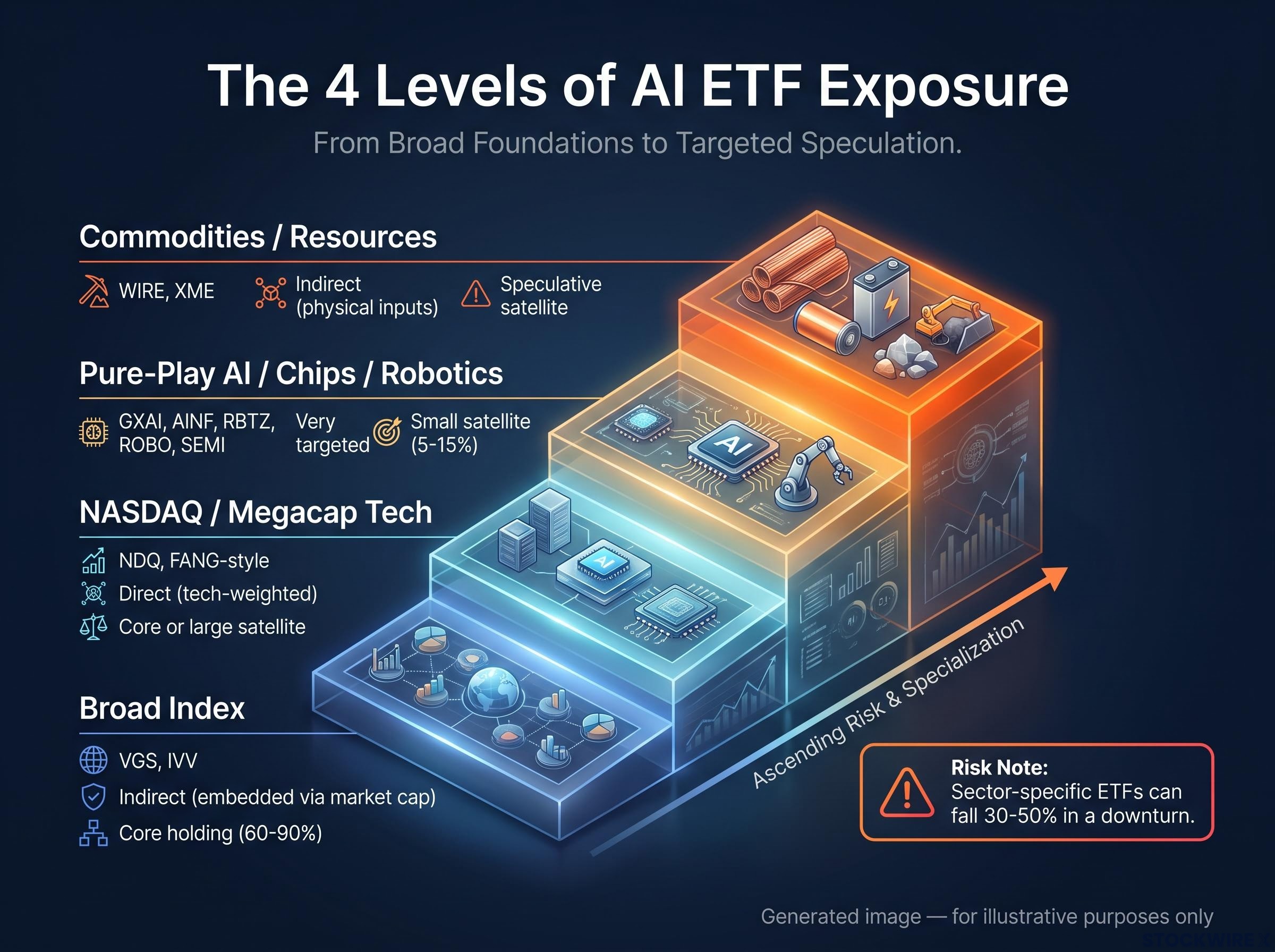

| Level | Typical ETF examples | AI specificity | Suggested portfolio role |

|---|---|---|---|

| 1. Broad Index | VGS, IVV | Indirect (embedded via market cap) | Core holding (60-90%) |

| 2. NASDAQ / Megacap Tech | NDQ, FANG-style | Direct (tech-weighted) | Core or large satellite |

| 3. Pure-Play AI / Chips / Robotics | GXAI, AINF, RBTZ, ROBO, SEMI | Very targeted | Small satellite (5-15%) |

| 4. Commodities / Resources | WIRE, XME | Indirect (physical inputs) | Speculative satellite if thesis-driven |

The next major ASX story will hit our subscribers first

What to avoid: leveraged ETFs, pre-IPO vehicles and the concentration trap

Before you execute, three categories of products deserve explicit caution, not because they are inherently bad, but because they carry a different risk profile than they appear to advertise.

- Leveraged and inverse AI/technology ETFs are trading tools, not investment instruments. Products offering 2x leverage or inverse exposure carry path-dependent compounding risk, meaning returns compound in ways that can diverge significantly from the underlying index over time. A 2x leveraged product can lose substantially more than twice the index decline over a multi-week drawdown.

- Pre-IPO and private AI company vehicles offering exposure to names like OpenAI or other unlisted AI startups are typically illiquid, hard to value and highly speculative. They are unsuitable as foundational allocations for retail investors regardless of how appealing the underlying company name sounds.

- Overlapping thematic ETF combinations create a concentration trap. If you hold NDQ, GXAI and SEMI simultaneously, check the underlying holdings. All three hold NVIDIA as a top position. What looks like thematic diversification across three products may actually be a single concentrated position in a handful of chip and platform companies expressed through multiple wrappers.

ASIC RG 282 guidance on complex ETPs specifically addresses products that use leverage or derivatives, requiring issuers to use clear naming conventions and disclosures that alert retail investors to the path-dependent compounding risk these instruments carry.

If you find yourself holding several AI and technology ETFs at once, map the underlying holdings across all of them. The overlap is often larger than it appears, and genuine diversification requires looking through the product labels to the actual companies you own.

Satellite allocation discipline matters most when a theme is performing strongly, because that is precisely when the temptation to increase concentration beyond a pre-set limit is highest; SPIVA data consistently shows that the majority of active tilts underperform their benchmark over the long run, reinforcing the case for pre-committed sizing rules rather than reactive ones.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Matching your conviction to the right level

The four levels map a clear spectrum from broad market participation to narrow thematic bets. Where you sit on that spectrum comes down to two questions:

- What is your specific AI conviction? If it is general, a broad index gives you what you need. If it is specific to chips, robotics or infrastructure, a targeted satellite can express that view. If it is about physical resource demand, you are making a commodity bet that happens to overlap with AI.

- What drawdown can you genuinely tolerate? Thematic and sector ETFs can fall 30-50% in a downturn. If that would cause you to sell, the allocation is too large for your circumstances.

The right AI ETF is not the one with the highest recent return. It is the one whose risk profile you will still be comfortable with when the theme faces its next correction, because that moment will test every allocation decision made during the optimistic phase. The core-satellite structure gives you a way to hold both conviction and discipline at the same time.

This information is general in nature and does not constitute personal financial advice. You should consider your own objectives, financial situation and needs, and seek guidance from a licensed financial adviser before investing.

—