3 ASX Sector ETFs That Returned Up to 136% in One Year

2 hrs ago

The Australian ETF market is on track to reach A$380 billion in 2026, a roughly 400% increase in six years. Yet the three funds beginners actually need to understand can fit on a single page.

New investors face a genuine paradox: more ETF options than ever, but no clear framework for choosing between them. VDHG, IVV, and VAS appear consistently across beginner investing communities, brokerage top-10 lists, and finance podcasts because they solve different problems. Understanding what each one does, and does not do, is the most efficient starting point for anyone building a first portfolio in 2026.

This guide explains what each of the three funds holds, what it costs, how it has performed, and which type of investor it suits. It provides a clear basis for making an informed decision without requiring prior investing knowledge.

There are now hundreds of ETFs listed on the ASX. For a first-time investor, the sheer volume of choice creates more paralysis than opportunity.

The convergence on VDHG, VAS, and IVV is not a coincidence. These three funds appear among the most-held ETFs on Pearler, the most-traded on CommSec, and the most frequently recommended across platforms like Equity Mates, Rask, and Sharesies. They dominate because each one solves a structurally different beginner need:

The rest of this guide answers one practical question: which of these funds belongs in your portfolio, and why?

If you have ever bought shares in a company through a brokerage app, you already understand the mechanics. An ETF works the same way. Buying a single ETF unit gives proportional exposure to every company or asset the fund holds, in one transaction. Instead of choosing between 300 individual ASX stocks, for example, one unit of VAS covers all of them.

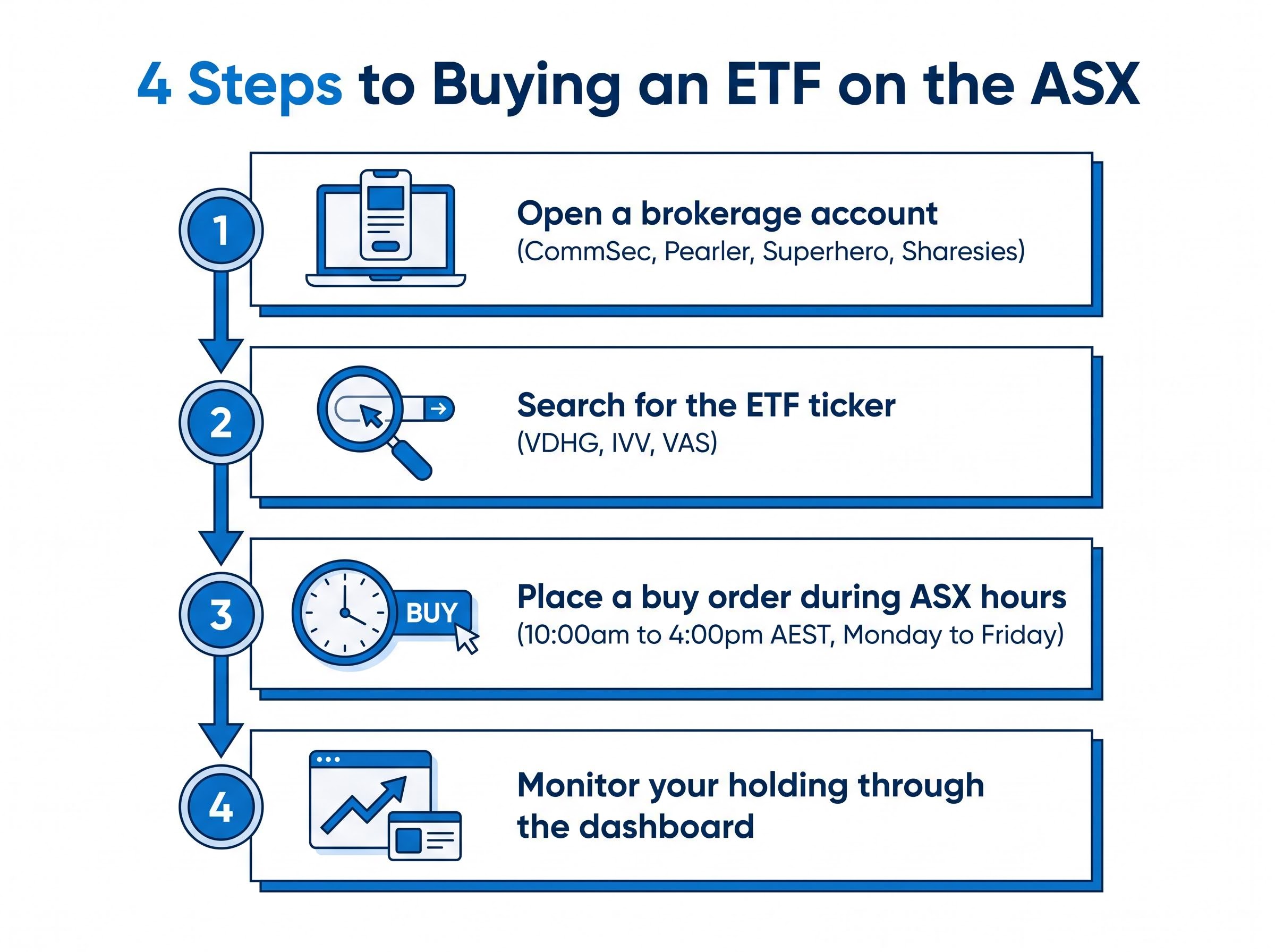

Purchasing an ETF on the ASX involves four steps:

Key benefits:

Key risks:

ASIC’s ETF consumer guide provides regulatory-level detail for beginners wanting independent verification of how these products work.

For readers wanting to go deeper before placing their first order, our full explainer on ETF structure and execution mechanics covers how ETF assets are held in a legally separate unit trust, why limit orders protect against wide bid-ask spreads, and which parts of the ASX trading session to avoid for better execution.

A managed fund pools investor money and is typically bought and sold through the fund issuer at end-of-day pricing. An ETF, by contrast, trades on the stock exchange throughout the day at live market prices, just like an ordinary share. This means ETF investors can see their holding’s value in real time and buy or sell during trading hours, whereas managed fund investors usually wait until the next business day for their transaction to settle.

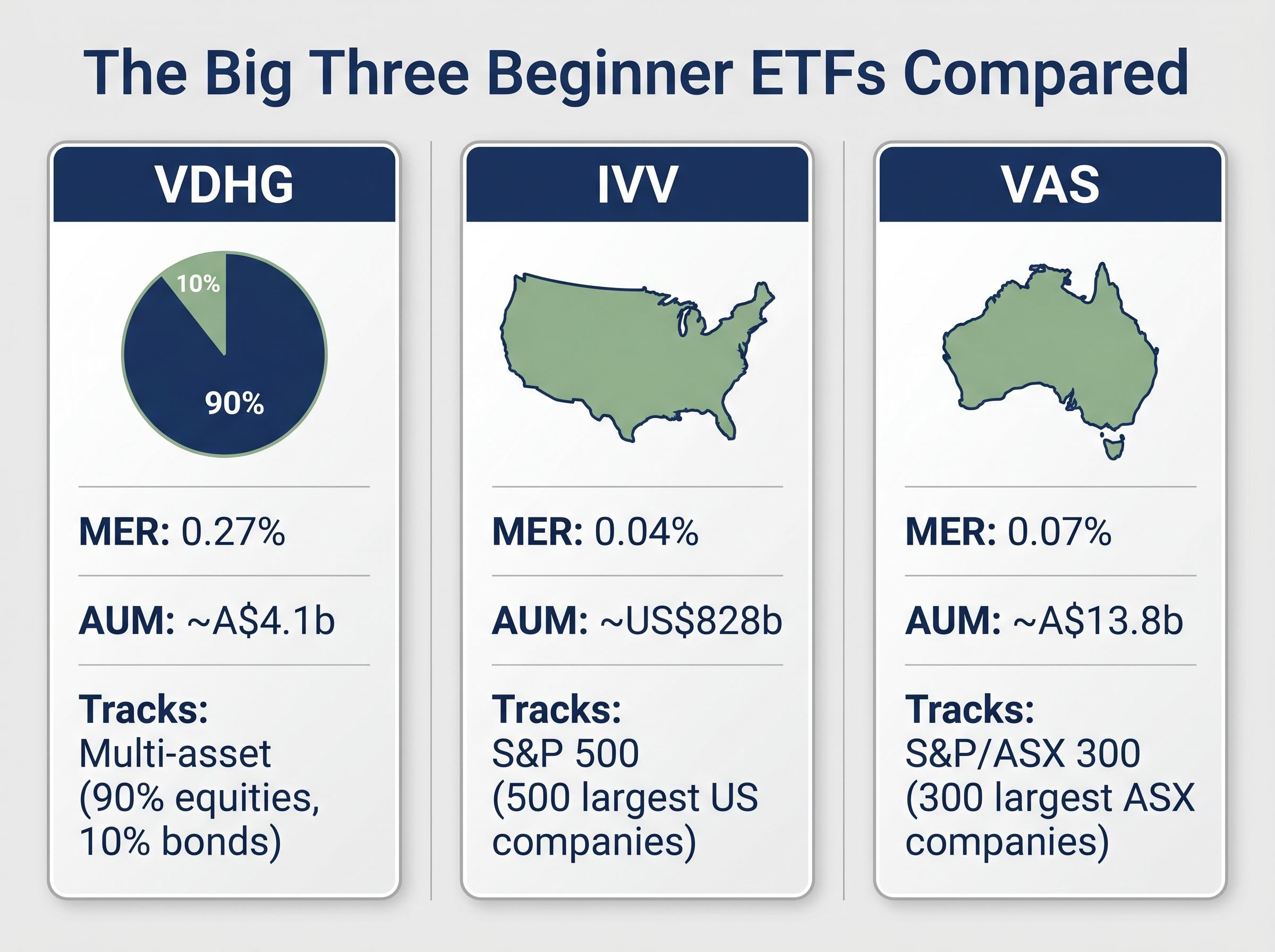

VDHG (Vanguard Diversified High Growth Index ETF) is a fund of funds. It holds multiple underlying Vanguard index funds, which means the investor gets automatic rebalancing across global equities, Australian equities, and a 10% defensive allocation of fixed income, without doing anything.

That convenience comes at a cost. At 0.27% p.a., VDHG’s management expense ratio is higher than holding VAS and IVV separately. The premium buys automatic rebalancing and asset allocation management: Vanguard adjusts the underlying fund weightings so the investor doesn’t have to.

The word “diversified” in the name deserves scrutiny. Approximately 90% of the fund sits in growth assets (global and Australian equities). That means VDHG will fall materially in a market downturn. Vanguard’s own Target Market Determination specifies a high risk tolerance and a long time horizon.

VDHG delivered a 1-year total return of 15.02% to 30 April 2026 (after fees, before tax), according to InvestSMART. This figure reflects the recovery from short-term volatility during early 2025 tariff-related market disruptions.

| Period | Total Return (% p.a.) |

|---|---|

| 1 year | 15.02% |

| 3 years (p.a.) | 12.75% |

| 5 years (p.a.) | 8.98% |

| 10 years (p.a.) | 10.05% |

The fund’s most recent distribution was 64.69 cents per unit (ex-dividend 1 April 2026), franked at 24.88%. Trailing income yield ranges from approximately 2.3% to 4.0% depending on the measurement period. AUM sits at approximately A$4.1 billion as at 31 March 2026.

For investors who want to start investing without designing a portfolio allocation, VDHG removes the most common beginner paralysis point entirely.

IVV (iShares S&P 500 ETF) tracks the S&P 500, giving Australian investors exposure to approximately 500 of the largest US-listed companies across technology, healthcare, financials, consumer goods, and industrials. The fund’s global AUM of approximately US$828 billion (as at 13 May 2026) signals institutional-grade liquidity and scale.

US exposure serves as a deliberate structural complement to the Australian market. The ASX is heavily concentrated in banks and miners. IVV adds sectors that barely exist domestically:

The management expense ratio is 0.04% p.a., the lowest of the three funds covered in this guide.

IVV’s 1-year AUD return to 31 March 2026 came in at approximately 23-25%, with 3-year annualised returns of approximately 14-16% and 5-year annualised returns of approximately 14-15%. Those figures reflect both strong US tech earnings and a period of AUD weakness.

IVV is unhedged, meaning Australian investors are fully exposed to AUD/USD currency movements. This is where IVV’s returns can look dramatically different from the underlying S&P 500 performance.

Illustrative example: If the S&P 500 returns 10% in USD and the AUD falls 5% against the USD over the same period, an Australian investor may see approximately 15% in AUD terms.

The AUD/USD rate ranged from approximately 0.63 to 0.72 across 2024-2025, with notable weakness in late 2025 (approximately 0.6648 average in December 2025) before recovering to approximately 0.7223 by mid-May 2026. Periods of AUD softness during tariff scares and global growth concerns coincided with strong US mega-cap performance, amplifying IVV’s AUD returns.

Currency works both ways. When the AUD strengthens against the USD, IVV’s AUD returns compress, even if the S&P 500 itself is rising. Beginners should treat currency exposure as a genuine two-way risk, not a reliable performance enhancer.

IVV’s underlying US dividend yield sits at approximately 1.3-1.5% in USD. US withholding tax applies to those distributions; completing a W-8BEN form reduces the rate from 30% to 15% under the Australia-US tax treaty. IVV distributions carry no franking credits.

The IRS guidance on Form W-8BEN confirms that foreign beneficial owners of US-sourced income, including Australian investors receiving IVV distributions, can use the form to claim a reduced withholding tax rate under an applicable tax treaty, bringing the standard 30% rate down to 15% for eligible Australian residents.

VAS (Vanguard Australian Shares Index ETF) tracks the S&P/ASX 300 Index, covering approximately 300 of the largest ASX-listed companies. The fund is heavily weighted toward financials (the major banks) and resources (large miners), reflecting the composition of the Australian market itself.

Notable holdings include Commonwealth Bank (CBA), BHP Group (BHP), and Woolworths Group (WOW).

VAS charges 0.07% p.a. and held approximately A$13.8 billion in net assets as at 31 March 2026, making it the largest of the three funds by Australian AUM.

The fund’s 1-year return to 31 March 2026 was approximately 9-10%, with 3-year annualised returns of approximately 8-9% and 5-year annualised returns of approximately 7-8%. Those figures are lower than IVV’s over the same periods, but the two funds are doing structurally different jobs. VAS delivers domestic market exposure with no currency risk.

The return gap between domestic and US equity ETFs reached its widest point in recent memory across the 12 months to May 2026, with IVV returning approximately 32% against VAS’s 10.59%, a divergence driven by RBA rate decisions, AUD movements, and the structural concentration differences between the two indexes.

VAS’s trailing 12-month cash yield sits at approximately 3.6-4.2%, plus franking credits on top. Distributions are typically 80-100% franked, making the effective after-tax yield materially higher for eligible investors, particularly those on lower marginal tax rates or holding within superannuation (taxed at 15%).

The franking credit mechanism works like this: Australian companies pay corporate tax before distributing dividends. The franking credit represents that tax already paid and reduces the investor’s personal tax bill on that income. For an investor in a lower tax bracket, the credit can result in a tax refund that effectively boosts the yield above the headline cash figure.

VAS carries no currency exposure. It is fully domestic. For Australian investors who pay tax, VAS’s franked distributions deliver genuine after-tax income that a USD-denominated fund like IVV cannot replicate.

For investors wanting to model what VAS’s franked distributions are actually worth in after-tax terms, our dedicated guide to franking credit calculations walks through the 30/70 formula with worked examples, including how a $1,000 fully franked dividend becomes $1,428.57 in total value for an SMSF in pension phase or an eligible low-income investor.

With three individual fund profiles established, the practical question becomes: which combination, if any, suits a beginner portfolio?

| Feature | VDHG | IVV | VAS |

|---|---|---|---|

| MER (annual fee) | 0.27% | 0.04% | 0.07% |

| AUM | ~A$4.1b | ~US$828b (global) | ~A$13.8b |

| What it tracks | Multi-asset (90% equities, 10% bonds) | S&P 500 (500 largest US companies) | S&P/ASX 300 (300 largest ASX companies) |

| Currency exposure | Unhedged international component | Fully unhedged (USD) | None (domestic only) |

| 1-year return | 15.02% | ~23-25% | ~9-10% |

| 3-year p.a. return | 12.75% | ~14-16% | ~8-9% |

| Distribution yield | ~2.3-4.0% | ~1.3-1.5% (USD) | ~3.6-4.2% + franking |

| Franking | Partial (varies) | None | High (80-100%) |

| Best suited for | One-fund simplicity; long horizon | Growth-oriented; comfortable with USD risk | Income/franking focus; domestic exposure |

The most common beginner question is direct: do I need all three, or do I pick one? The answer depends on how much management the investor wants to do.

One practical tax consideration: VDHG’s internal rebalancing can trigger annual capital gain distributions to investors, even if the investor has not sold any units. Holding VAS and IVV separately avoids this, giving the investor greater control over CGT timing.

To buy any of these funds, open a brokerage account (CommSec, Pearler, Superhero, or Sharesies), search by ticker code, and place a buy order during ASX trading hours.

The difference between investors who stick with their strategy through volatility and those who panic-sell at the worst moment often comes down to three pieces of knowledge, absorbed before the first purchase rather than learned the hard way after it.

Australia’s CGT changes and ETF portfolio structure decisions are becoming increasingly linked: from 1 July 2027, the 50% CGT discount is replaced by inflation indexation and a 30% minimum effective tax floor, making the structural advantage of holding low-turnover passive ETFs like VAS even more pronounced relative to actively managed alternatives.

The ATO’s CGT discount rules confirm that Australian resident individuals who hold an asset for at least 12 months before disposal are entitled to reduce the taxable capital gain by 50%, a structural incentive that meaningfully improves after-tax returns for patient ETF investors.

“Investors who hold ETF units for more than 12 months qualify for a 50% CGT discount, halving the taxable portion of any capital gain on sale.”

One additional note on tax: investors holding IVV should complete a W-8BEN form to reduce US withholding tax on distributions from 30% to 15% under the Australia-US tax treaty. Investors should seek personal tax advice regarding their specific circumstances.

The core distinction between the three funds comes down to two sentences. VDHG is the one-decision option: broad diversification, automatic rebalancing, and a single ticker for investors who want simplicity above all else. IVV and VAS are the building blocks for investors who want to construct their own allocation, minimise fees, and retain greater control over tax outcomes.

All three funds are accessible through standard Australian brokerages and require no prior investing knowledge to purchase.

Before committing capital, review each fund’s Product Disclosure Statement (PDS) and Target Market Determination on the relevant issuer’s website. Investors uncertain about which fund suits their specific tax situation, income needs, and risk tolerance should seek personal financial advice. ASIC’s MoneySmart (moneysmart.gov.au) also provides independent, free guidance on ETF investing for Australian retail investors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

VDHG, IVV, and VAS are the most consistently recommended ASX ETFs for beginners, appearing on top-traded lists across platforms like CommSec and Pearler because each one solves a different portfolio need: one-fund diversification, US market access, and domestic income respectively.

VDHG (Vanguard Diversified High Growth Index ETF) is a fund of funds that holds multiple underlying Vanguard index funds, giving investors automatic exposure to global equities, Australian equities, and a 10% bond allocation with built-in rebalancing for a management fee of 0.27% per year.

IVV is unhedged, meaning returns in Australian dollars are affected by AUD/USD movements; if the AUD falls against the USD, your AUD returns are amplified, but if the AUD strengthens, your returns are compressed even if the S&P 500 itself is rising.

VAS distributions are typically 80-100% franked, meaning the dividends carry tax credits for corporate tax already paid by the underlying companies, which can reduce your personal tax bill or generate a refund, making the effective after-tax yield materially higher than the headline cash yield of approximately 3.6-4.2%.

VDHG provides simplicity through automatic rebalancing in a single ticker at a 0.27% fee, while holding VAS and IVV separately lowers the blended fee to approximately 0.05-0.06% and gives investors direct control over their allocation and capital gains tax timing, since VDHG's internal rebalancing can trigger annual CGT distributions even if you have not sold any units.