Why Panic Selling Costs You Most at the Moment It Feels Right

8 hrs ago

Not all $10 million order books are created equal. When a small-cap industrial announces a headline figure that size, the first question worth asking is whether the number represents signed contracts or a wish list dressed up in a table. The difference between the two shapes everything that follows.

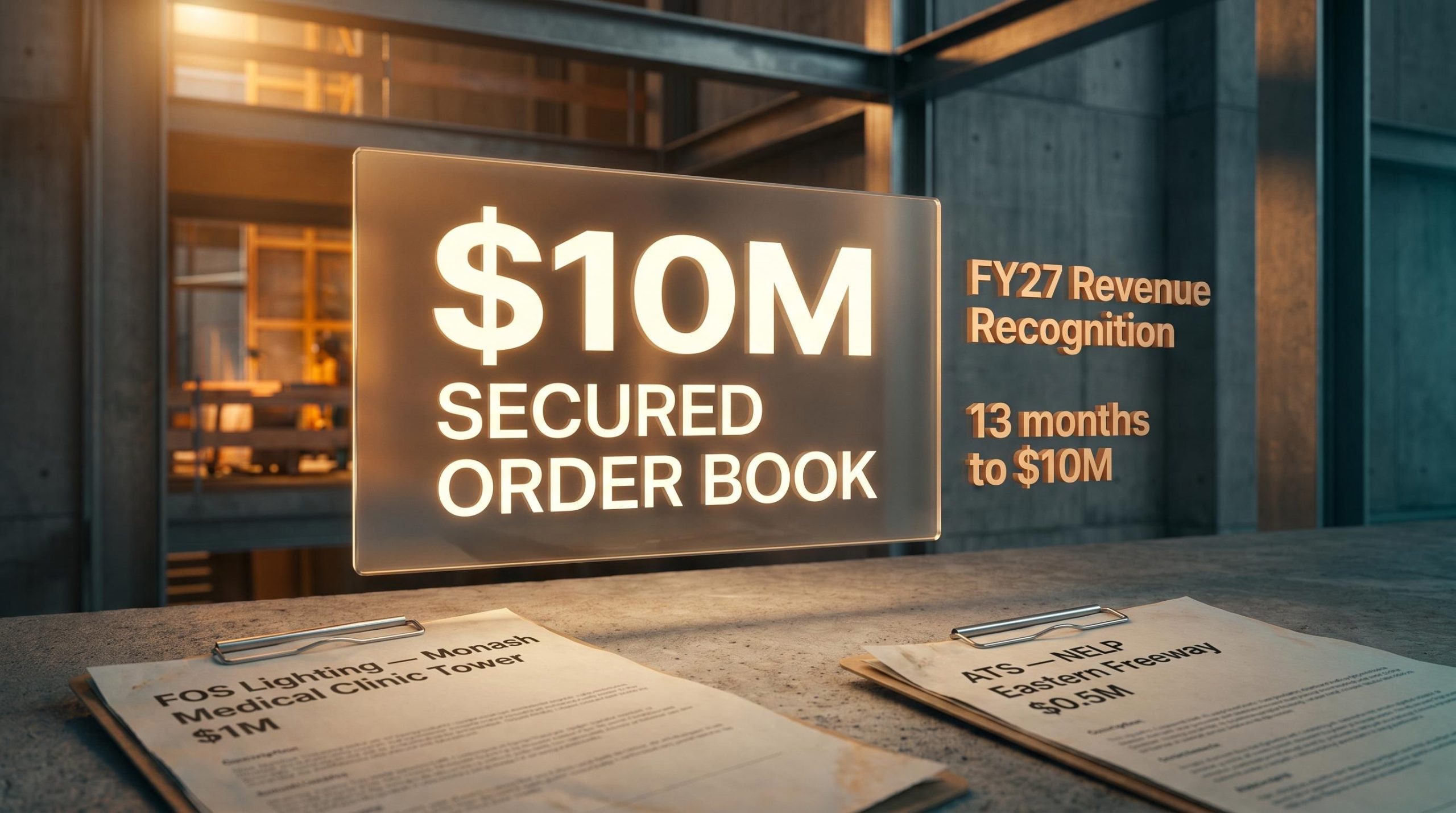

FOS Capital (ASX: FOS) reached the $10 million secured order book milestone in July 2026, following a $1 million healthcare lighting contract for the Monash Medical Clinic Tower expansion. Both of its operating subsidiaries, FOS Lighting Pty Ltd and Aldridge Traffic Systems (ATS), contributed to the figure. At small-cap scale, where a single contract can represent a material share of total forward revenue, the distinction between secured and speculative matters more than at any other point in the market-cap spectrum.

Here is the analytical framework for reading a secured order book correctly, applied to a live ASX example. After this, you will know what the $10 million means, what it does not mean, and what three specific signals to watch before forming a view on where FOS Capital goes from here.

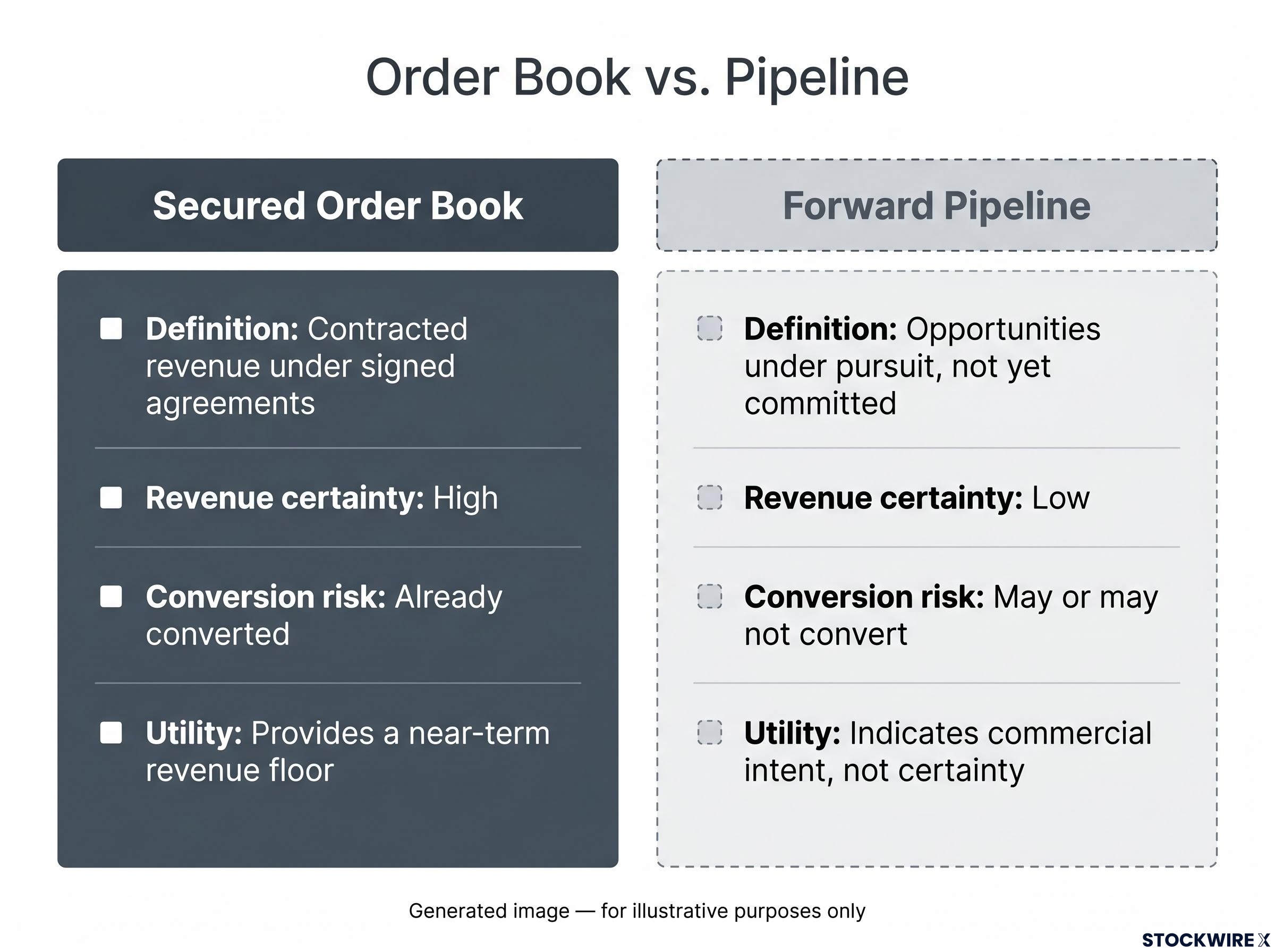

A secured order book is contracted revenue sitting behind signed agreements. The work is committed. It carries delivery risk and counterparty risk, but it does not carry commercial conversion probability, because the conversion has already happened. The buyer has signed.

A forward pipeline is something different entirely. It represents opportunities under active pursuit, at varying stages of commercial discussion, with no binding commitment attached.

Conflating the two is one of the most common analytical errors investors make when evaluating small-cap industrials. Many ASX small caps present pipeline figures alongside order book data without clearly distinguishing between them. FOS Capital’s $10 million is confirmed contracted work, not pipeline. That distinction tells you the near-term revenue floor has a structural basis that a pipeline figure of the same size simply would not provide.

Rigorous ASX small-cap research starts with the announcement feed before any secondary interpretation is applied: the primary source document carries the definitional precision, such as whether a figure is contracted or indicative, that secondhand summaries routinely flatten or omit.

| Attribute | Secured Order Book | Forward Pipeline |

|---|---|---|

| Definition | Contracted revenue under signed agreements | Opportunities under pursuit, not yet committed |

| Revenue certainty | High (subject to delivery and counterparty risk) | Low (subject to conversion probability) |

| Conversion risk | Already converted | May or may not convert; rates rarely disclosed |

| Investor utility | Provides a near-term revenue floor | Indicates commercial intent, not commercial certainty |

Pipelines represent commercial intentions, not obligations. Conversion rates are rarely disclosed, and a pipeline figure can remain static or even grow without any commercial progress occurring underneath it. For an investor, the risk is mistaking directional ambition for contracted momentum.

Both of FOS Capital’s operating subsidiaries contributed to the $10 million order book concurrently as of July 2026. That is not a coincidence of timing worth glossing over; it is a structural signal worth examining.

For a business at FOS Capital’s scale, two distinct revenue streams generating contracted work simultaneously is a more favourable structural signal than one segment carrying the entire book, even if the absolute figures were identical. Single-sector dependence is one of the primary risks in small-cap industrial investing, and concurrent contribution from both segments reduces that concentration.

Two contracts across two subsidiaries constitutes the beginning of a diversification thesis, not confirmation of it. Sustained concurrent activity across multiple reporting periods would be required before the structural claim can be made with confidence. This is a favourable early signal, not a proven advantage.

The story starts not with a contract win, but with an acquisition. FOS Capital completed the purchase of Aldridge Traffic Systems on 24 June 2025, bringing traffic and infrastructure capabilities into the group. ATS then underwent a significant rebuild period before becoming commercially active.

Total secured order book: approximately $10 million as of 7 July 2026.

The trajectory from acquisition to $10 million in roughly 13 months tells you that ATS was rebuilt and commercially active faster than the timeline of many small-cap M&A integrations. That is relevant context for assessing management execution. And the build itself, a series of incremental wins across two subsidiaries rather than one large contract inflating a headline figure, is a structurally different commercial story.

Management execution at small-cap scale is assessed through observable behaviour over time: milestone delivery rates, consistency between public statements and filed outcomes, and whether capital raises are signalled in advance or arrive as distressed surprises are all measurable signals available to investors working from public documents.

A secured order book tells you revenue is coming. It does not tell you when it arrives on the income statement. Revenue recognition, the accounting process that determines when contracted revenue appears in reported earnings, follows delivery milestones rather than contract signing dates.

Infrastructure and institutional contracts typically recognise revenue over the delivery period via milestones or percentage-of-completion accounting. For FOS Capital, with primary contract awards falling in the May-July 2026 window and approximately 12-month delivery periods, the associated revenue recognition is positioned primarily in FY27.

AASB 15 performance obligations satisfied over time form the accounting basis for milestone and percentage-of-completion revenue recognition, which is why infrastructure and institutional contracts spread their revenue contribution across reporting periods rather than recognising the full contracted amount at signing.

12-month delivery windows position the majority of the $10 million order book as FY27 revenue recognition.

Recognition may extend across reporting periods depending on project milestone schedules. The $10 million will not appear as a single-period event. What this means for your assessment is straightforward: the order book is a forward visibility asset for FY27, not a current-period earnings catalyst. That changes how you should weight it in any near-term valuation view.

As of 9 July 2026, FOS Capital has released no margin or profitability data alongside its order book announcements. That absence is the most significant gap remaining in the analytical picture for investors.

Consider a general conceptual illustration: two contracts of identical order book value can deliver dramatically different earnings outcomes depending on their margin profiles.

| Contract characteristic | Contract A (higher margin) | Contract B (lower margin) |

|---|---|---|

| Order book contribution | $1 million | $1 million |

| Gross margin (illustrative) | 40% | 12% |

| Gross profit contribution | $400,000 | $120,000 |

Note: This table is a conceptual illustration of how margins affect earnings outcomes. It does not represent implied or actual margin ranges for FOS Capital.

The order book establishes how much contracted revenue is coming. What it cannot establish is how much of that revenue will translate into profit. Revenue visibility and earnings visibility are two separate things, and without margin data from FOS Capital, you are working with only one of them. The $10 million tells you where revenue is coming from but not what the business will earn from it.

Revenue visibility and earnings visibility diverge most sharply when margin data is absent, a gap that the earnings report analytical framework addresses directly: free cash flow alignment, gross margin direction, and the GAAP/non-GAAP gap are the three cross-checks that convert a revenue-level headline into something resembling an earnings thesis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The analytical work above gives you the framework. These three signals give you the forward-monitoring toolkit.

Margin disclosure is the pivotal variable: it is the data point that converts a revenue map into an earnings thesis.

These three signals are not equally weighted. Margin disclosure matters most because it is the one that transforms what you know about revenue into something you can use to assess earnings trajectory. Its absence remains the single largest outstanding uncertainty in the current FOS Capital picture.

Investors ready to build a systematic framework around the forward monitoring approach described above will find our deep-dive into ASX small-cap investing disciplines useful; it covers practitioner methods for identifying thesis invalidation criteria before entering a position, so that future contract announcements and margin disclosures can be assessed against pre-set benchmarks rather than reacted to in isolation.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Two threads run through this analysis. The first is company-specific: FOS Capital has built a contracted $10 million order book across two operating subsidiaries in roughly 13 months, with revenue recognition positioned primarily in FY27. The second is structural: the distinction between secured and speculative, between revenue certainty and earnings certainty, applies to every small-cap industrial order book disclosure you will encounter.

The $10 million is a structurally credible milestone for a small-cap industrial at FOS Capital’s stage. The analytical framework above allows you to hold that view without overstating what the number confirms.

The three forward signals, additional NELP lots, margin disclosure, and sustained dual-subsidiary activity, are the mechanism by which you can revisit and sharpen your assessment as new disclosures arrive, rather than reacting to headline figures in isolation.

—

A secured order book is contracted revenue backed by signed agreements, meaning commercial conversion has already occurred. A pipeline represents opportunities under active pursuit with no binding commitment, and conversion rates are rarely disclosed, making it a measure of commercial intent rather than commercial certainty.

The $10 million secured order book, reached in July 2026, includes contributions from both FOS Lighting Pty Ltd and Aldridge Traffic Systems (ATS), with recent wins including a $1 million healthcare lighting contract for the Monash Medical Clinic Tower and a $0.5 million contract for the NELP Eastern Freeway Upgrades.

With primary contract awards falling in the May-July 2026 window and approximately 12-month delivery periods, the majority of the $10 million order book is positioned for revenue recognition in FY27, spread across reporting periods via milestone or percentage-of-completion accounting rather than recognised in a single period.

As of July 2026, FOS Capital has released no margin or profitability data alongside its order book figures, meaning investors have revenue visibility but not earnings visibility; two contracts of identical order book value can produce dramatically different profit outcomes depending on their margin profiles.

The three forward signals are: additional contract lots awarded within the North East Link Project, any gross margin or cost structure disclosure from management, and sustained concurrent contract wins from both FOS Lighting and ATS across subsequent reporting periods, with margin disclosure carrying the most analytical weight.