Where Gold Is Headed in H2 2026 After a US$1,500 Crash

14 mins ago

A secured order book is not a pipeline. For a small-cap industrial stock still proving its post-acquisition integration thesis, that distinction is the entire story. FOS Capital (ASX: FOS) has disclosed a secured order book of approximately $10 million as of July 2026, with contract-backed contributions from both of its operating subsidiaries.

The figure gives investors something rare at this stage of a company’s development: a concrete, contract-backed anchor for forward revenue. But it also carries limits that the headline number alone does not communicate. No margin data has been disclosed. No revenue base comparison has been published. The order book tells you what may be recognised as top-line revenue in FY27; it cannot yet tell you what reaches the bottom line.

This analysis breaks down what the $10 million figure means structurally, where the thesis has a real foundation, and exactly where the gaps are that require further disclosure before forming a position. Think of it as a working investor’s tool for reading an ASX small-cap order book correctly, not a verdict.

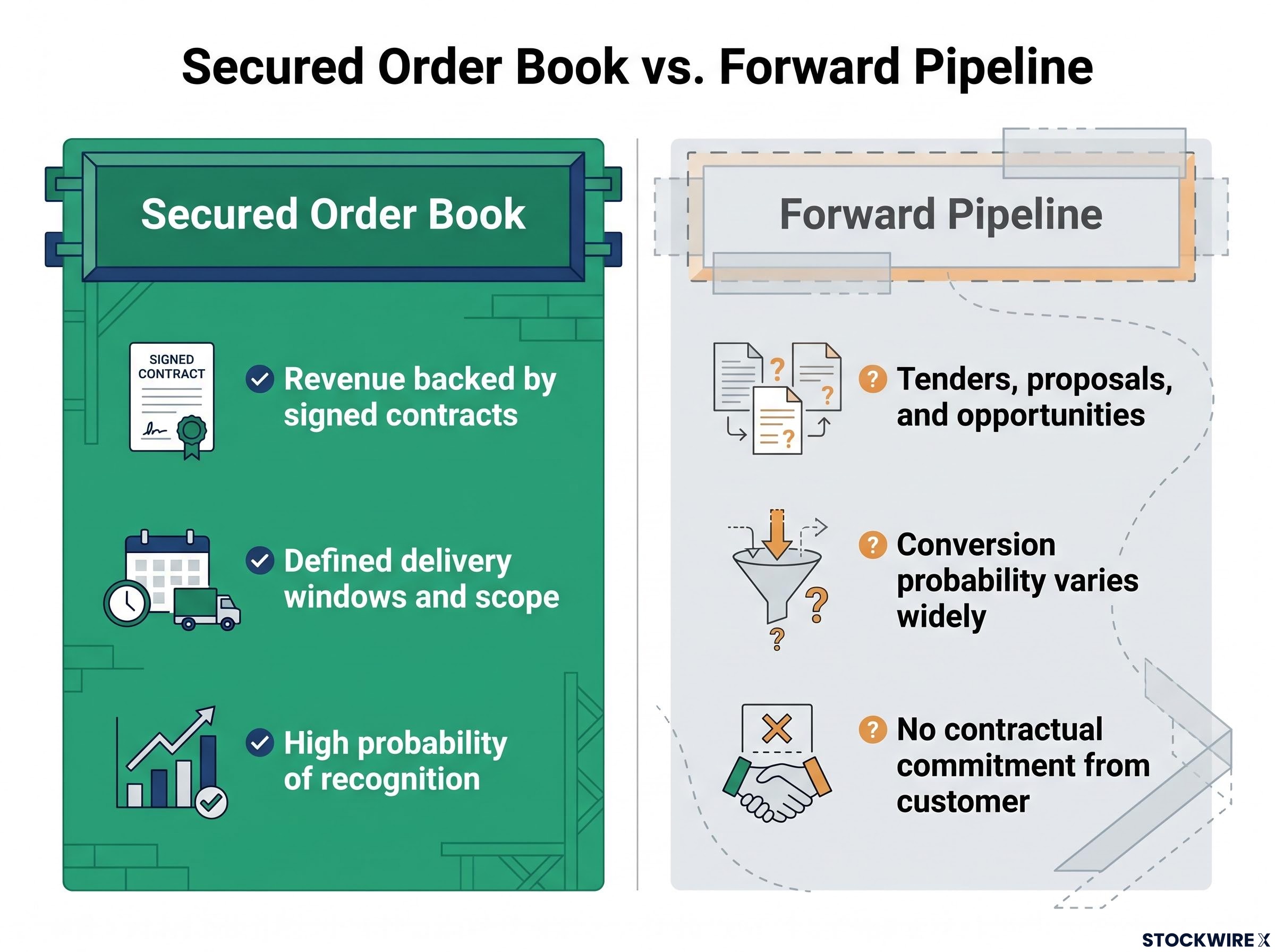

When a company discloses a “secured order book,” it is making a materially stronger claim than one reporting a “forward pipeline.” The difference is not cosmetic. It determines how much weight you can place on the number.

A secured order book represents revenue that has been confirmed through executed agreements. Delivery scope and terms are set, and the company holds a contractual entitlement to recognise that revenue once it meets the relevant completion conditions. A forward pipeline, by contrast, is a collection of potential opportunities: tenders submitted, proposals awaiting decisions, and prospects at various stages of conversion likelihood, none of them committed by the customer.

ASX Guidance Note 8 on continuous disclosure sets out when a listed entity must release material contract and earnings information to the market, including the specific exceptions under Listing Rule 3.1A that permit temporary withholding of commercially sensitive information, a framework directly relevant to how FOS Capital manages its order book communications.

For small-cap growth stocks, getting this distinction right is what separates meaningful analysis from noise. Revenue visibility is scarce by default at this company stage, and a contract-backed figure gives investors a concrete anchor that pipeline language simply does not provide. Many ASX small-cap industrials report pipeline sizes and total addressable market estimates. Those figures are speculative. A secured order book is a more conservative and more credible form of forward communication.

Secured order book characteristics:

Forward pipeline characteristics:

When evaluating any small-cap stock, the first question to ask is not how large the pipeline is, but what fraction of that pipeline has converted to signed contracts. Only the latter provides genuine top-line visibility.

Quality screening within the ASX small-cap universe matters precisely because broad exposure to the asset class systematically dilutes the size premium by including unprofitable and speculative names; investors who apply quality filters before sizing a position are working with a structurally different risk profile than those buying broad small-cap exposure.

The $10 million figure did not arrive as a single event. It accumulated through a sequence of decisions and outcomes that, read together, tell a more important story than the dollar amount alone.

FOS Capital acquired Aldridge Traffic Systems (ATS) in June 2025. What followed was a rebuild phase, the kind of post-acquisition integration work that absorbs management bandwidth and delays commercial output. That phase is where many small-cap acquisitions stall.

ATS did not stall. By May 2026, the subsidiary had secured the NELP Eastern Freeway contract, pushing the cumulative order book to approximately $9 million. Then in July 2026, a second subsidiary, FOS Lighting Pty Ltd, won the Monash Medical Centre contract, adding approximately $1 million and lifting the total to $10 million.

The structural signal here is not the individual contract wins. It is the shift from one active subsidiary plus one in rebuild to two subsidiaries winning contracts in parallel. That progression, from acquisition to rebuild to dual-subsidiary traction in under 13 months, suggests the integration thesis is converting into a functioning operating model rather than remaining a single-unit story.

Management execution in the post-acquisition phase is one of the harder variables to quantify from public disclosures alone; per-share return analysis and milestone delivery tracking are the most reliable observable proxies, and professional investors weight the consistency between public statements and filed outcomes heavily when forming a view.

| Date | Event | Order Book Impact |

|---|---|---|

| June 2025 | ATS acquisition | Acquisition phase begins |

| May/June 2026 | NELP Eastern Freeway contract win | Order book reaches ~$9 million |

| July 2026 | Monash Medical Centre contract secured | Order book reaches ~$10 million |

For small-cap investors, the build sequence matters more than the headline figure. It tells you whether the order book reflects repeatable commercial activity or a single contract concentration event.

A $10 million secured order book is not $10 million in reported revenue. The two are separated by delivery, completion, and the accounting standards that govern when revenue can be recognised.

The approximately 12-month delivery windows associated with the current contracts link the work to FY27 as the primary revenue recognition period. That gives investors a timing anchor: the contracted work is positioned for recognition within the next financial year, not sitting in an indefinite future pipeline.

The analytical tool to apply here is the order book-to-prior-year-revenue ratio. If $10 million represents 1.0x to 1.5x prior-year revenue, the backlog is highly material to the investment thesis. If it represents 0.3x, the signal is more modest. The problem is that this ratio is not calculable from current public disclosures alone. Investors would need to access FY24 and FY25 financials, plus any pro-forma ATS revenue figures, to complete the calculation.

The core distinction: The secured order book represents contracted forward work, not revenue already recognised. The two should not be conflated in investment analysis. Until an investor calculates the backlog against FOS Capital’s reported revenue base, including any ATS pro-forma figures, they cannot determine whether $10 million is a transformative forward load or a meaningful but incremental one.

The order book confirms forward revenue visibility. It does not confirm forward profitability. FOS Capital has disclosed no margin or profitability data as of July 2026, which means the $10 million figure tells you what may appear on the top line in FY27 but nothing about what survives to the bottom line.

That gap is not a footnote. It is the central risk in the current thesis.

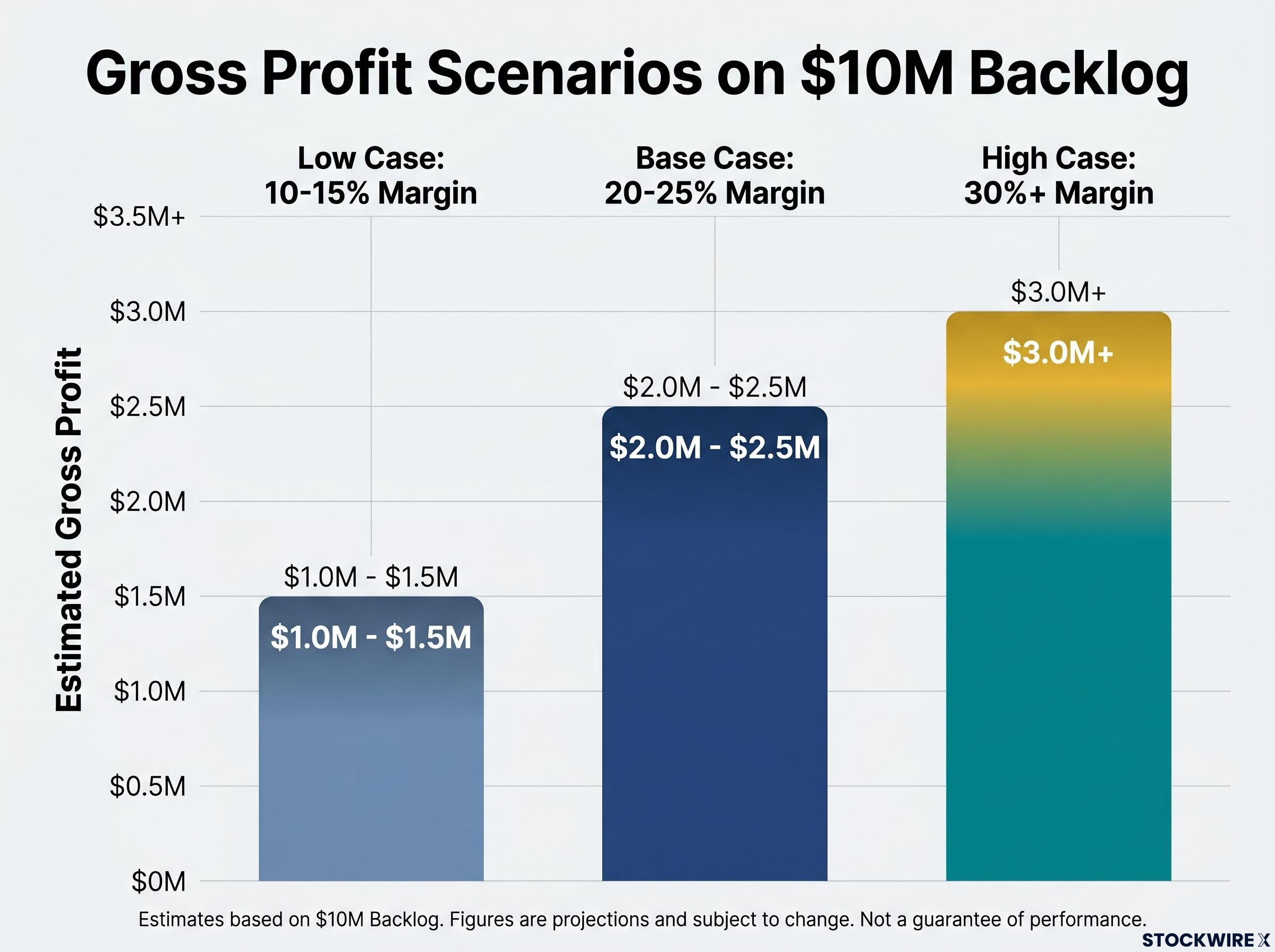

To illustrate the sensitivity, consider three gross margin scenarios applied to the $10 million backlog. These are not predictions; they are informed by typical margin ranges for comparable ASX-listed lighting and traffic infrastructure small caps.

The ATO small business benchmarks for electrical services provide publicly accessible gross profit ratio data for electrical contractors in Australia, offering a reference point that broadly supports the base-case gross margin assumption of 20-25% applied to the backlog scenarios above.

| Scenario | Gross Margin Assumption | Estimated Gross Profit from $10M Backlog |

|---|---|---|

| Low case | 10-15% | $1.0 million – $1.5 million |

| Base case | 20-25% | $2.0 million – $2.5 million |

| High case | 30%+ | $3.0 million+ |

Actual EBIT would be further reduced after overhead allocation and integration costs in each scenario. The spread between low and high case gross profit is $1.5 million to $3.0 million or more, which tells you the thesis is highly sensitive to an assumption investors currently have no data to anchor.

The risk statement: Secured order book data tells investors what may be recognised as revenue in FY27. It does not tell you what will reach the bottom line. The risk-reward assessment cannot be completed without margin disclosure.

Order books can strain small-cap balance sheets. Project-based work often requires upfront capital for inventory, labour, and mobilisation before revenue is recognised, particularly when billing is completion-based rather than milestone-based.

FOS Capital has not publicly disclosed whether its contracts feature milestone payments or completion-based billing, nor its net cash or net debt position, nor any undrawn credit facilities. These are the specific data points investors should seek before assessing whether the balance sheet can fund the delivery of the current backlog without dilutive capital raising.

The analysis cannot go further without additional disclosure. But it can specify exactly what information, when it arrives, would either strengthen or qualify the thesis as currently constructed.

For investors actively monitoring FOS Capital, these three signals are the specific triggers that would justify revisiting the risk-reward assessment rather than waiting passively for a quarterly update.

The $10 million secured order book is a meaningful proof point. It confirms post-acquisition integration traction, demonstrates dual-subsidiary commercial activity, and provides concrete FY27 revenue visibility backed by signed contracts. For an ASX small-cap industrial at this stage of development, that is a credible foundation.

What remains unresolved is whether that revenue translates into earnings. No margin data, no revenue base comparison, and no working capital clarity have been disclosed. The investment thesis is structurally incomplete from an earnings perspective, and formal valuation work using earnings-based multiples is premature until the margin disclosure milestone occurs.

The upgrade path for this analysis is specific: connect the $10 million backlog to FOS Capital’s reported revenue history to establish scale, construct margin scenarios with actual disclosed figures once available, and assess balance-sheet capacity against project mobilisation requirements. Until that data arrives, revenue certainty is the ceiling of what can be concluded with confidence. That ceiling is meaningful, but it is not the same as investment conviction.

The broader framework for secured order book analysis, including how to calculate the backlog-to-revenue ratio and why delivery windows determine which financial year captures the recognition event, is developed in a companion piece that strips the FOS-specific narrative and presents the methodology in reusable form.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The margin scenarios presented are illustrative only and should not be treated as forecasts. Past performance does not guarantee future results.

—

A secured order book represents revenue confirmed through executed contracts, with defined delivery scope and a contractual entitlement to recognise revenue once completion conditions are met. A forward pipeline, by contrast, includes tenders, proposals, and unconfirmed opportunities where no customer commitment exists, making it a far less reliable indicator of future revenue.

The approximately 12-month delivery windows on FOS Capital's current contracts position the contracted work for recognition primarily in FY27, making the $10 million figure a concrete top-line anchor for that financial year. However, without margin disclosure, investors cannot determine how much of that revenue will survive to the bottom line.

The standard tool is the order book-to-prior-year-revenue ratio: if the backlog represents 1.0x to 1.5x prior-year revenue, it is highly material; if it represents 0.3x, the signal is more modest. For FOS Capital, this ratio cannot yet be calculated because comparable revenue base figures from FY24 and FY25, including ATS pro-forma data, have not been published.

The three most important signals are: additional NELP programme contract wins by ATS (which would confirm the infrastructure client relationship is repeatable), the release of margin or profitability data (which would allow the analysis to move from revenue certainty to earnings certainty), and continued dual-subsidiary contract wins from both ATS and FOS Lighting (which would confirm the dual-unit operating model is durable).

A formal earnings-based valuation requires margin data, a revenue base comparison, and balance sheet clarity on working capital and billing structure, none of which FOS Capital has disclosed as of July 2026. The $10 million order book establishes top-line visibility but leaves gross profit estimates ranging from $1 million to over $3 million depending on the margin scenario applied, too wide a range to anchor a credible valuation multiple.