Why T-Cell Exhaustion Defines the CAR-T Bet for ASX Biotech Investors

9 hrs ago

Most Australian investors arrive at the property versus ETFs question with their mind half-made up. They have heard that property always beats inflation, or that shares compound faster over time, and they want the data to confirm the view they already hold. The problem is that the data does not cooperate. During the 2022-2023 RBA hiking cycle, property prices fell across numerous Australian markets while inflation was still running hot, and investors who had concentrated into resources ETFs at the peak of the commodity spike watched those positions give back months of gains within weeks.

The question matters right now because inflation and the rate environment that follows it remain live concerns for every Australian household making borrowing decisions, choosing where to direct superannuation contributions, or deciding whether the next dollar goes into a deposit on an investment property or a brokerage account.

What follows gives you a clearer way to think about both asset classes under inflationary conditions, a framework for assessing which mix suits your own situation, and why the answer almost certainly involves holding more than one.

Inflation erodes the purchasing power of your money. When the cost of goods and services climbs, cash sitting in a savings account and income from fixed-rate investments like term deposits lose real value over time. That is why investors look to assets like property and equities in the first place: they want returns that at least keep pace with rising prices.

But inflation never arrives alone. The Reserve Bank of Australia (RBA) responds by lifting the cash rate, which is the benchmark interest rate that flows through to mortgage rates, business lending, and the pricing of almost every financial asset. The rate response is what actually reprices your holdings.

The RBA cash rate decision in May 2026 marked the third consecutive 25 basis point hike, lifting the benchmark to 4.35% with eight of nine Board members voting in favour, and forward guidance that left the door open to a fourth move depending on Q2 CPI and labour market data.

Higher rates produce three effects that hit simultaneously:

Most investors think about inflation as the threat. In practice, the bigger threat to your portfolio over any two-to-three year window is the central bank’s response to it. Positioning around inflation alone, without accounting for the rate hikes that follow, is an incomplete strategy that has caught many Australian investors off-guard.

Property has earned its reputation as a long-term inflation hedge for three reasons. First, rents tend to rise over time as incomes and living costs increase, which supports the income side of a property investment. Second, construction and replacement costs climb with inflation, pushing up the value of existing buildings. Third, land in desirable Australian locations remains scarce, and that scarcity supports prices even when broader economic conditions soften.

For you as a patient investor holding quality property with manageable debt, these forces can help preserve purchasing power relative to simply holding cash. Over decades, the evidence supports property as a store of real value.

When the RBA raises rates, the maximum loan a buyer can service at any given monthly repayment shrinks, pressing purchase prices downward. Property investors carrying variable-rate debt find their holding costs rising sharply, which compresses net rental yields. Where the cost pressure becomes severe enough, some investors are pushed to sell.

The 2022-2023 RBA hiking cycle, one of the sharpest in recent Australian history, put this dynamic on clear display. As borrowing costs climbed and purchasing power eroded, prices fell across many local markets even though inflation was still running above target and rents were increasing in numerous areas.

Property can fall in value during inflation if rate hikes move fast enough to crush affordability before price growth can reassert itself. The long-run hedge and the short-run risk are not contradictory; they operate on different timeframes.

What this means for you is that the property investment thesis depends heavily on your time horizon. Over a two-to-three year window of aggressive rate hikes, capital values can move against you even when you are technically holding an asset that hedges inflation over the long run.

ETFs are baskets of assets, usually shares, wrapped in a tradable structure you can buy and sell on the ASX. Their behaviour during inflation is determined by what sectors sit inside the basket, not by the ETF wrapper itself. This distinction matters more than most investors realise.

Sectors that tend to perform relatively better during inflation:

Sectors that face the most pressure from rate hikes:

The 2022 global rate-hiking episode demonstrated this split in real time. Many technology and growth stocks suffered sharp drawdowns while resource producers in Australia posted strong results on the back of elevated commodity prices.

When you hold a broad Australian ETF through an inflationary cycle, you are not making a single directional bet. Some holdings will benefit from the environment while others absorb the headwinds, and that built-in spread across sectors means your overall equity exposure is not riding on whichever part of the market is under the most pressure at any given moment.

Inflation-aware ETF selection at the fund level matters as much as the decision to hold equities at all: bond income ETFs like VBND are currently yielding above CPI, quality-factor international funds like QUAL target companies with pricing power and low leverage, and cash ETFs like AAA preserve flexibility at yields of roughly 3.90-4.24% while markets remain unsettled.

Across different inflationary episodes in Australia and globally, the asset class that outperforms is not consistent. Sometimes property leads. Sometimes equities lead. Sometimes neither delivers especially well in real terms. The research on historical comparisons yields no stable pattern that reliably identifies a single winning asset class.

Why? Because outcomes depend on five variables that rarely line up the same way twice:

Performance leadership rotates. Resources or property may lead in one phase and lag in the next. The investor who concentrated into the winning asset class last cycle often finds themselves holding the lagging one in the next.

By the time outperformance is obvious, it may largely be in the rear-view mirror. Markets tend to price in expected outcomes before they fully materialise.

The practical takeaway: asking “which one wins?” is the wrong question, because the answer changes with every cycle, and the cost of being wrong with a concentrated position is steep.

After all the macro analysis, the variables that most practically determine the right mix of property and ETFs in your portfolio are the ones you can actually assess about your own situation. Individual circumstances often outweigh macro conditions when it comes to which allocation serves you best.

| Factor | Property | ETFs |

|---|---|---|

| Capital requirements | Large upfront deposit plus ongoing maintenance, insurance, and management costs | Can be purchased in small increments and scaled gradually over time |

| Liquidity | Slow and costly to sell; settlement takes weeks and agent fees apply | Can be sold on the ASX within minutes at minimal cost |

| Concentration risk | A single property is a large, concentrated bet on one location and one asset | A broad ETF spreads exposure across dozens or hundreds of companies and sectors |

| Leverage | Readily accessible through standard mortgages at relatively low interest rates | More complex in share markets and carries higher risk if misused |

| Tax considerations | Negative gearing and the CGT discount can reduce the effective cost of holding | CGT applies on disposal; superannuation rules can shift net outcomes significantly |

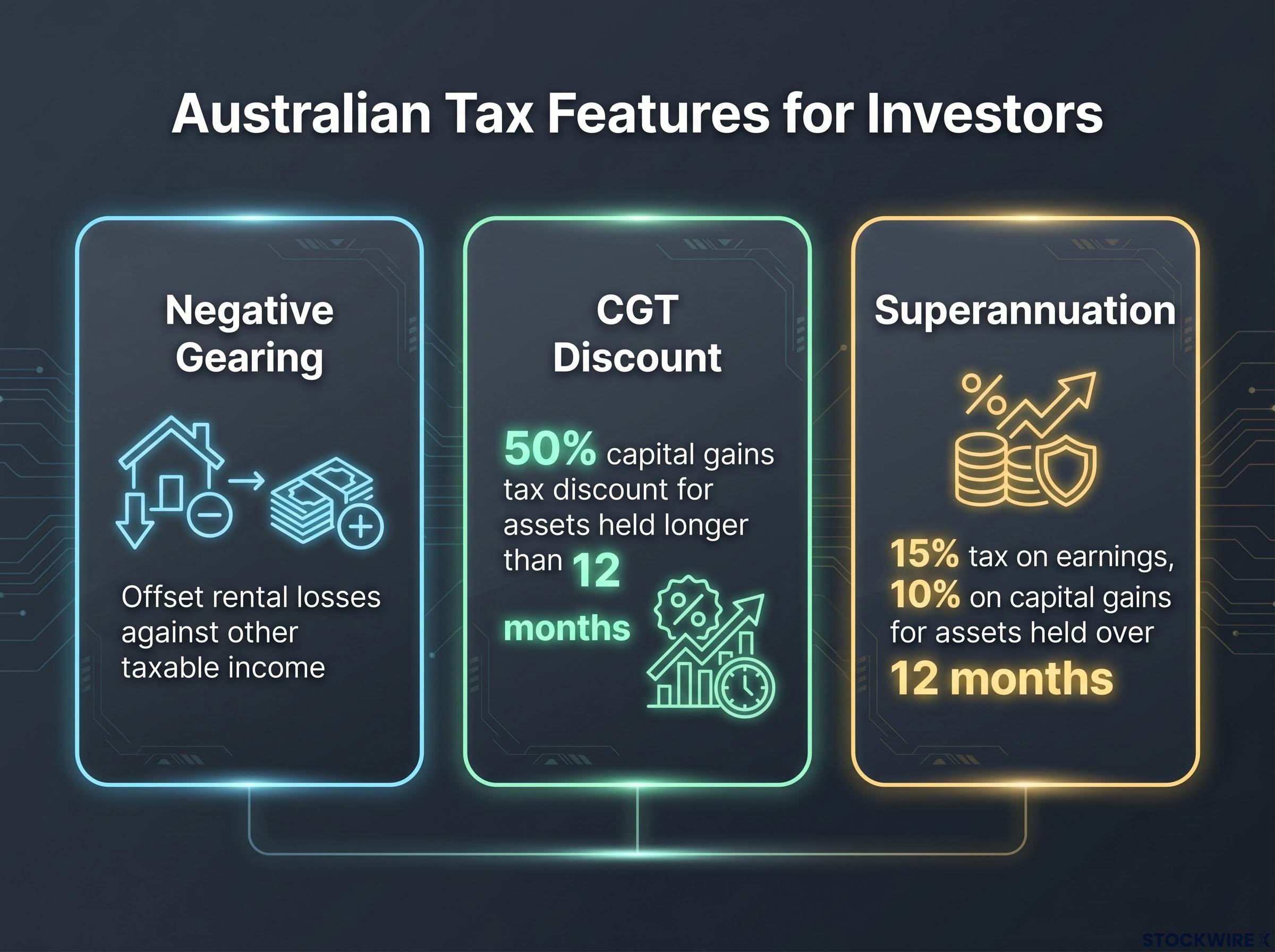

Three Australian tax features can meaningfully tilt the economics between property and ETFs, and they work differently for different investors.

Negative gearing allows property investors to offset rental losses (where holding costs exceed rental income) against other taxable income, reducing the overall tax bill. This benefit is most valuable to higher-income earners in higher tax brackets. It does not apply to ETFs in the same way.

The negative gearing removal for existing residential dwellings took effect at 7:30pm AEST on 12 May 2026 for new purchases, meaning investor positions are already divided between grandfathered and exposed regardless of whether the legislation ultimately passes, and the effective after-tax return on newly acquired investment properties has already shifted for top-rate taxpayers.

The 50% capital gains tax (CGT) discount applies to both property and ETF investments held for longer than 12 months, halving the taxable portion of any capital gain on disposal. This benefits both asset classes equally in principle, but the larger absolute gains typical of leveraged property can make the discount more impactful in dollar terms.

Superannuation rules allow Australians to hold ETFs and listed property trusts within their super fund at concessional tax rates (15% on earnings, 10% on capital gains for assets held over 12 months). Direct property within superannuation is possible but operationally complex and subject to strict borrowing rules.

The right blend of property and ETF exposure for you personally is not determined by reading the macro environment correctly. It is determined by honestly assessing your capital base, your need for liquidity, your tax position, and how long you can stay invested.

The case this article has built is straightforward: because inflation and rate cycles produce rotating winners, diversification across both asset classes is the structurally sound response, not a failure to pick correctly. Holding both property and ETFs, and potentially bonds, cash, and commodities alongside them, spreads your exposure across categories that respond differently to the same macro forces.

That spread serves a practical purpose. It avoids catastrophic loss from a single concentrated bet. It allows you to participate in gains across multiple categories. And it accepts one uncomfortable truth: not every holding in your portfolio will outperform at the same time, and that is by design.

The investor behaviours that evidence consistently supports are simpler than most commentary suggests:

The practical step is deciding on a mix that fits your personal circumstances, then holding it with discipline through the cycles that will inevitably favour one part of your portfolio and pressure another. That is not a passive shrug. It is the evidence-backed response to a macro environment where the winning asset class genuinely cannot be identified in advance.

For readers wanting to move from the allocation framework to specific fund selection and positioning tactics, our dedicated guide to investing during inflation covers six ASX-listed ETFs across preservation, income, and growth roles, a dollar cost averaging approach calibrated to current conditions, and portfolio tilt logic for the distinct phases of an inflationary cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

—

Neither asset class consistently outperforms across every inflationary episode. Property protects purchasing power over decades through rising rents and land scarcity, but rate hikes can push capital values down in the short term, while ETFs holding resources and infrastructure tend to benefit from inflation even as growth stocks suffer.

The 2022-2023 RBA hiking cycle was one of the sharpest in recent Australian history, and prices fell across many local markets even while inflation was still running above target and rents were rising in numerous areas, because the surge in borrowing costs crushed buyer affordability faster than price growth could reassert itself.

Rising rates hit ETF sectors unevenly: growth and technology stocks lose value as higher rates discount their future earnings more heavily, while resources, energy, and infrastructure holdings can hold up or outperform because their revenues move with commodity prices and regulated contracts rather than cheap capital.

Negative gearing lets property investors offset rental losses against other taxable income, a benefit most valuable to high-income earners that does not apply to ETFs in the same way. The removal of negative gearing for new residential purchases, effective 12 May 2026, has already shifted the after-tax return calculation for investors buying now.

Capital requirements, liquidity needs, concentration risk, tax position, and time horizon typically matter more than the macro environment when determining the right mix. Property demands a large upfront deposit and is slow to sell, while ETFs can be purchased incrementally and exited on the ASX within minutes at minimal cost.