Australia’s most significant capital gains tax restructure in a generation takes effect on 1 July 2027, and for residential property investors who bought after Budget night, the numbers are already different. The 2026-27 Federal Budget, announced on 12 May 2026, introduced two interlocking reforms: the restriction of negative gearing on existing residential properties to new builds only, and the replacement of the 50% CGT discount with cost base indexation plus a 30% minimum tax on net capital gains. Neither measure is yet law, but the grandfathering cut-off has already passed, creating an immediate divide between existing and new investor positions.

What follows is an analysis of how these two levers interact, what they mean for after-tax returns on residential property, and which asset categories stand to benefit from the shift in relative attractiveness.

Two reforms, one structural shift in property’s after-tax appeal

These are not two separate policy tweaks. The negative gearing restriction and the CGT discount replacement activate on the same date, target the same asset class, and compress the same investor’s returns from both ends of the holding period: ongoing cash flow and eventual sale. Treated in isolation, either reform would alter the property investment calculus. Together, they compound.

The negative gearing ring-fence also catches family trust structures holding investment properties, with a 30% minimum tax on trust distributions from rental income taking effect on the same 1 July 2027 date, a third dimension of the reform that is absent from most investor commentary focused solely on individual landlords.

The reforms as announced:

- Negative gearing restriction: From 1 July 2027, rental losses on existing residential dwellings can no longer be offset against other income. New builds remain eligible. Properties held before the Budget night cut-off are grandfathered.

- CGT discount replacement: The existing 50% capital gains discount for individuals, trusts, and partnerships is replaced by cost base indexation (adjusting the purchase price for inflation) plus a 30% minimum tax on net capital gains. The new regime applies to gains accruing after 1 July 2027.

Both reforms were announced on 12 May 2026 and, as of 26 May 2026, neither has been tabled as legislation. The policy details remain subject to change, meaning the risk of amendment, delay, or defeat in Parliament is real. Investors should track the bill’s progress rather than treat these settings as settled.

The ATO tax explainer on negative gearing and capital gains confirms the 1 July 2027 commencement date, the 30% minimum tax on net capital gains, and the grandfathering cut-off of 7:30pm AEST on 12 May 2026 as the official parameters announced in the 2026-27 Federal Budget.

When big ASX news breaks, our subscribers know first

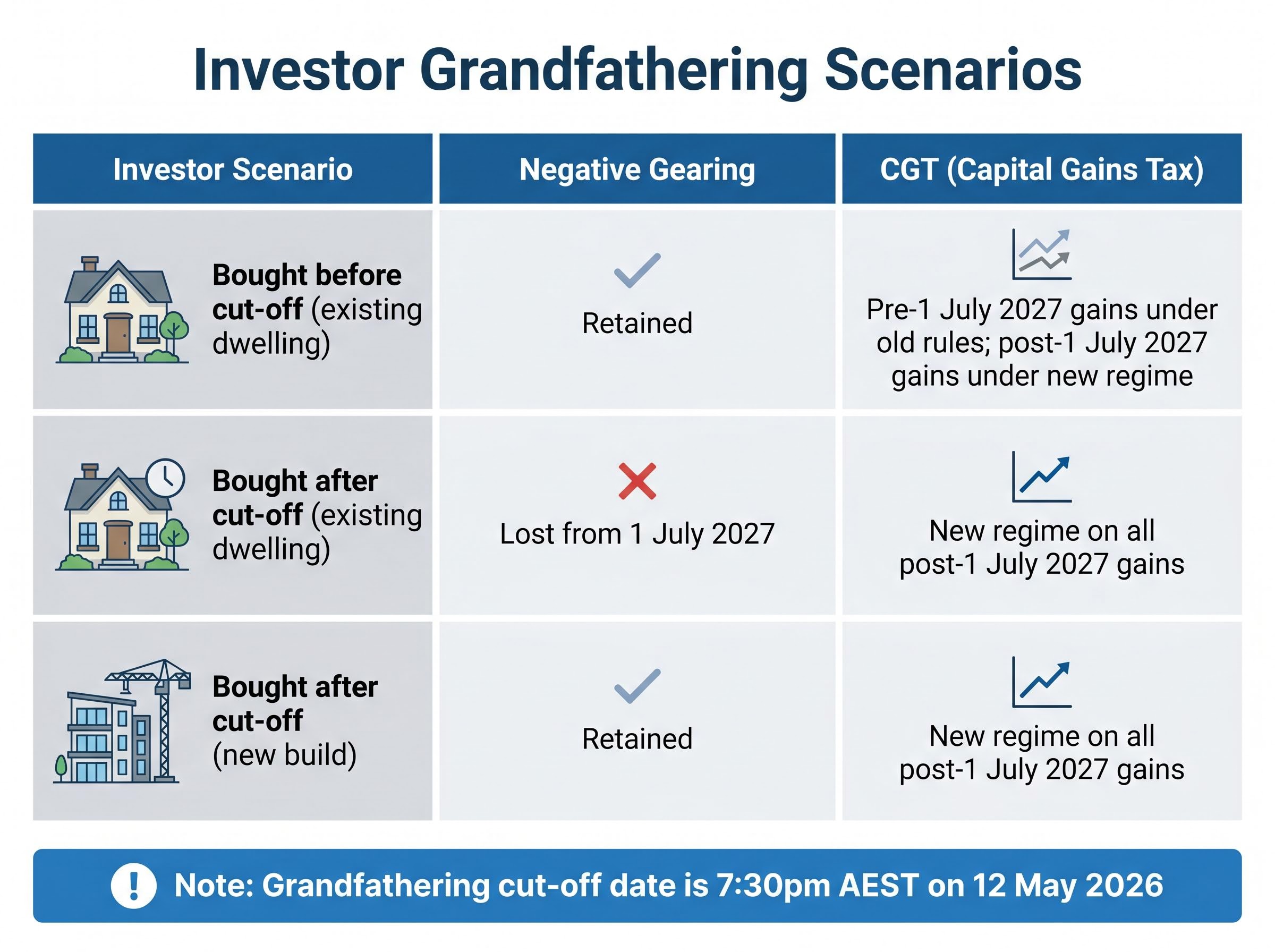

What the grandfathering rules actually mean for your position

The grandfathering structure determines whether an investor is protected or exposed, and the answer depends on two separate triggers operating on two different timelines.

For negative gearing, the line is purchase timing. Properties held before 7:30pm AEST on 12 May 2026 retain access to negative gearing deductions on existing dwellings. Properties purchased after that moment in existing dwellings do not, from 1 July 2027 onward. New builds remain eligible regardless of purchase date.

For capital gains tax, the line is when the gain accrues, not when the property was bought. Gains accruing before 1 July 2027 are not subject to the 30% minimum tax regime. Gains accruing after that date fall under the new treatment, regardless of the original purchase date.

These two grandfathering mechanisms operate independently, which creates complexity for investors straddling both timelines.

| Investor Scenario | Negative Gearing Access | CGT Treatment | Key Risk |

|---|---|---|---|

| Bought before cut-off (existing dwelling) | Retained under grandfathering | Pre-1 July 2027 gains under old rules; post-1 July 2027 gains under new regime | Erosion of exit returns on long-held properties if most gain accrues after 1 July 2027 |

| Bought after cut-off (existing dwelling) | Lost from 1 July 2027 | New regime on all post-1 July 2027 gains | Compounding effect: higher holding costs and higher effective CGT on sale |

| Bought after cut-off (new build) | Retained (new builds exempt from restriction) | New regime on all post-1 July 2027 gains | CGT change still applies; negative gearing partially offsets cash flow pressure |

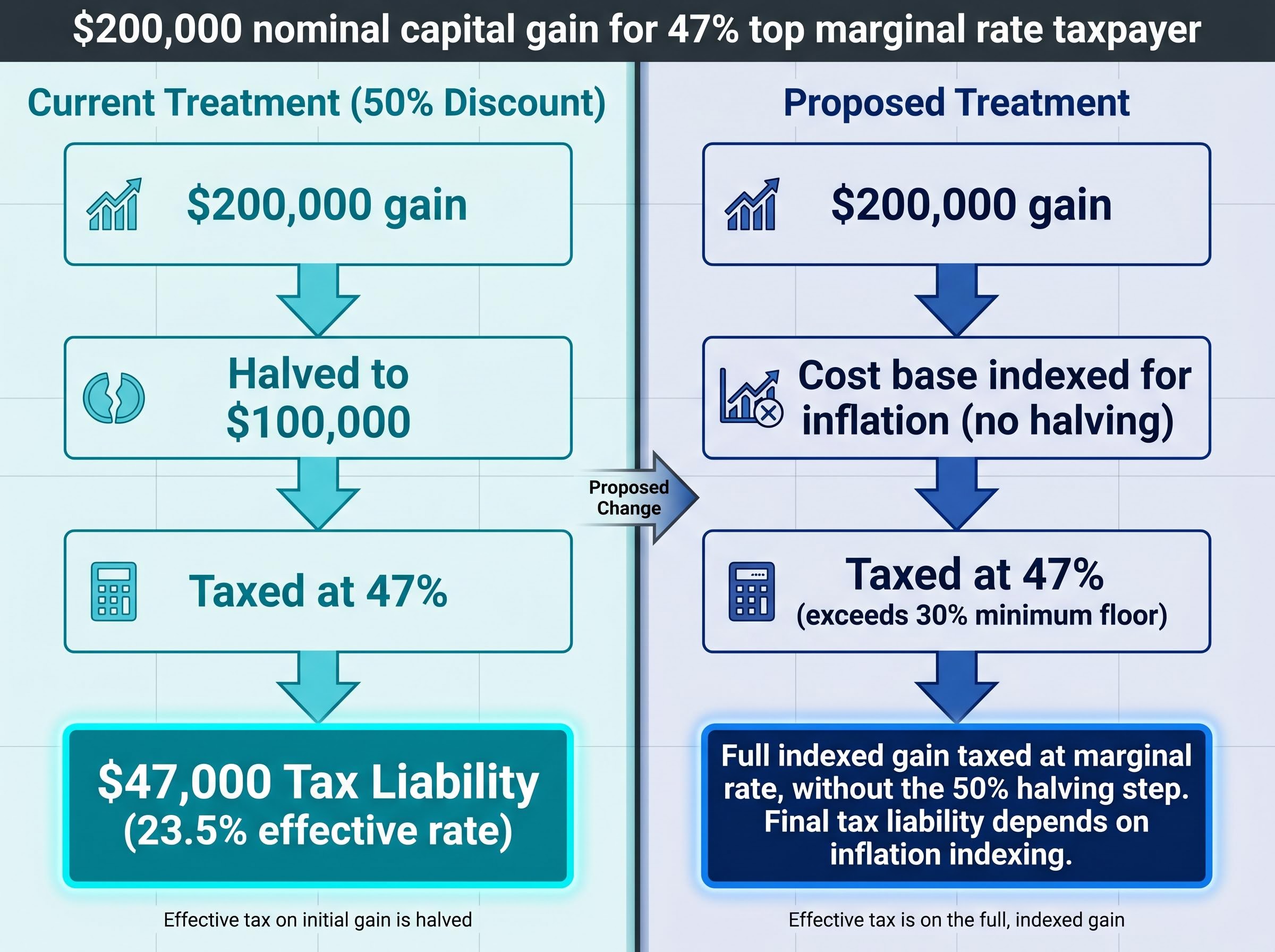

Understanding how the CGT discount worked and why its removal bites harder at higher incomes

The existing 50% CGT discount works by halving the nominal capital gain before it enters an individual’s taxable income. For an investor on Australia’s top marginal rate of 47% (including the Medicare levy), this means the effective tax rate on a qualifying gain is approximately 23.5%: half the gain is discarded, and the remaining half is taxed at 47%.

Under the proposed regime, the 50% discount disappears. In its place, the investor’s cost base is indexed for inflation (partially compensating for price rises over the holding period), and a 30% minimum tax applies to net capital gains.

The 30% minimum tax on net capital gains represents the new structural floor. It is not a flat rate; investors on marginal rates below 30% may see little change. The impact concentrates at higher income levels.

To illustrate the shift for a top-rate taxpayer on a $200,000 nominal capital gain:

- Current treatment: The gain is halved to $100,000, then taxed at 47%, producing a tax liability of approximately $47,000 (effective rate: 23.5%).

- Proposed treatment: The cost base is indexed for inflation, reducing the nominal gain (the reduction depends on the holding period and CPI movement). The remaining net gain is taxed at whichever is higher: the investor’s marginal rate or 30%. For a top-rate taxpayer, the marginal rate of 47% exceeds the floor, meaning the full indexed gain is taxed at 47%, without the halving step.

The cost base indexation partially compensates, but for high-income investors holding rapidly appreciating assets, it does not replicate the 50% discount’s effect. The gap between the old and new treatment widens as the gain grows.

City-level variation in CGT outcomes complicates any single-number modelling exercise: PropTrack analysis finds Melbourne investors are disproportionately likely to benefit from cost base indexation relative to the old 50% discount, while Brisbane investors face a higher effective tax bill under the same switch, reflecting the different growth trajectories those markets have experienced over the past decade.

The negative gearing arithmetic on existing properties, and where it breaks down

Negative gearing, as it currently operates, allows investors to deduct rental losses (where mortgage and holding costs exceed rental income) against their other income, reducing their overall taxable income. From 1 July 2027, this mechanism ends for existing dwellings purchased after the Budget night cut-off.

The interaction with the CGT change is where the compounding effect becomes visible. Consider the before-and-after cash flow position for a negatively geared existing property:

- Before reform: Rental shortfall of, say, $15,000 per year is deducted against salary income, reducing the investor’s tax bill. The investor accepts negative cash flow during the holding period because the eventual capital gain will be taxed at a concessional rate (approximately 23.5% effective for top-rate taxpayers).

- After reform: The $15,000 shortfall is no longer deductible. Holding costs rise in after-tax terms. At sale, the gain faces the new CGT regime with no 50% discount. Returns compress at both ends.

Rob Wilson, Director of Investment Strategy at Selfwealth by Syfe, noted in Bloomberg reporting on 13 May 2026 that the combined effect of tighter negative gearing rules and reduced CGT concessions makes investment property a comparatively weaker proposition.

The supply incentive logic

The exemption for new builds is not incidental. It represents an explicit policy mechanism to redirect investor capital toward housing supply. Properties that add to the dwelling stock retain negative gearing eligibility, creating a differential return profile between new and existing dwellings that did not previously exist at this scale.

Where investor capital is likely to rotate, and what the relative return case looks like

The same tax arithmetic that weakens property’s after-tax returns actively strengthens the case for income-producing equities, particularly Australian dividend-paying stocks with franking credits.

The logic is structural. The 50% CGT discount gave growth-oriented assets (including property) a tax advantage over income-producing assets, because dividend income was never sheltered by the discount. With the discount removed, that relative advantage narrows. Franking credits, which function as a pre-paid tax credit against the investor’s marginal rate, make after-tax income from quality dividend stocks more competitive once capital gains treatment tightens.

ASX dividend portfolio construction for investors rotating out of residential property requires particular attention to payout ratio sustainability and the 45-day holding rule, since a rising dividend yield driven by a falling share price can mask an imminent cut that erodes the income replacement thesis entirely.

Rob Wilson of Selfwealth by Syfe told Bloomberg on 13 May 2026 that the reformed tax rules alter the balance between high-growth shares and income-producing investments, with franked dividend stocks reinforced as a preferred category under the new settings.

| Asset Category | Negative Gearing Impact | CGT Treatment Change | Relative After-Tax Position |

|---|---|---|---|

| Existing residential property | Lost for post-cut-off purchases | 50% discount removed; 30% minimum tax applies | Weakened at both cash flow and exit |

| New build residential | Retained | 50% discount removed; 30% minimum tax applies | Partially shielded; negative gearing offsets holding costs |

| Australian dividend equities (franked) | Not applicable | CGT change applies to capital gains component only | Strengthened; franking credits unchanged, relative advantage widens |

The reforms are not yet law, and that uncertainty is itself a risk factor

As of 26 May 2026, no bill has been tabled. No Exposure Draft or Treasury consultation paper has been released. The policy details derive entirely from Budget night announcements and secondary reporting, meaning specifics remain subject to change before legislation is introduced.

This creates a specific risk for investors who restructure portfolios in anticipation of reforms that are later amended, delayed, or defeated. Transaction costs, stamp duty, and capital gains triggered by pre-emptive sales cannot be reversed if the legislation does not proceed as announced. The proposed commencement date of 1 July 2027 is approximately 13 months away, a window that will narrow as Parliamentary debate begins, but that remains wide enough for material amendment.

The grandfathering cut-off, however, has already passed. Its practical effect on market behaviour is already in motion regardless of whether the broader reforms become law.

Three actions warrant consideration:

- Track the bill’s progress through Parliament, including any Senate committee review or crossbench negotiations that could alter the final settings.

- Obtain specific advice on where existing holdings sit relative to the grandfathering cut-off, and what that means under both the proposed and current regimes.

- Model portfolio returns under two scenarios: one where the reforms proceed as announced, and one where they do not.

The investment property calculus has shifted, even before the law changes

The combined removal of negative gearing on existing dwellings and the replacement of the 50% CGT discount creates a structural repricing of residential investment property returns. That repricing does not require the legislation to pass before it affects investor behaviour; the grandfathering cut-off is already shaping purchase decisions, and the expectation of reform is already filtering into valuation assumptions.

The relative attractiveness of property versus income-producing equities has shifted. Franked dividend stocks, which were never sheltered by the CGT discount, now occupy a stronger position in the after-tax return hierarchy. New build residential, with negative gearing intact, represents the remaining property sub-category where returns are less impaired.

The 13 months between now and the proposed commencement date represent a window for portfolio assessment, not a reason to defer analysis. Investors who stress-test their positions against both scenarios will be better calibrated than those who wait for legislative certainty.

For investors who want to stress-test the indexation-plus-floor model against alternative structures, our deep-dive into the CGT reform design models a tapered discount alternative over a 20-year holding period and quantifies the tax differential, finding the government’s chosen approach produces a materially higher bill than a holding-period-sensitive taper would for long-term investors with consistently compounding assets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding proposed tax reforms are based on Budget announcements as of 12 May 2026 and are subject to change based on legislative developments.