Two Index Changes on 29 June, Two Very Different Flow Stories

1 hr ago

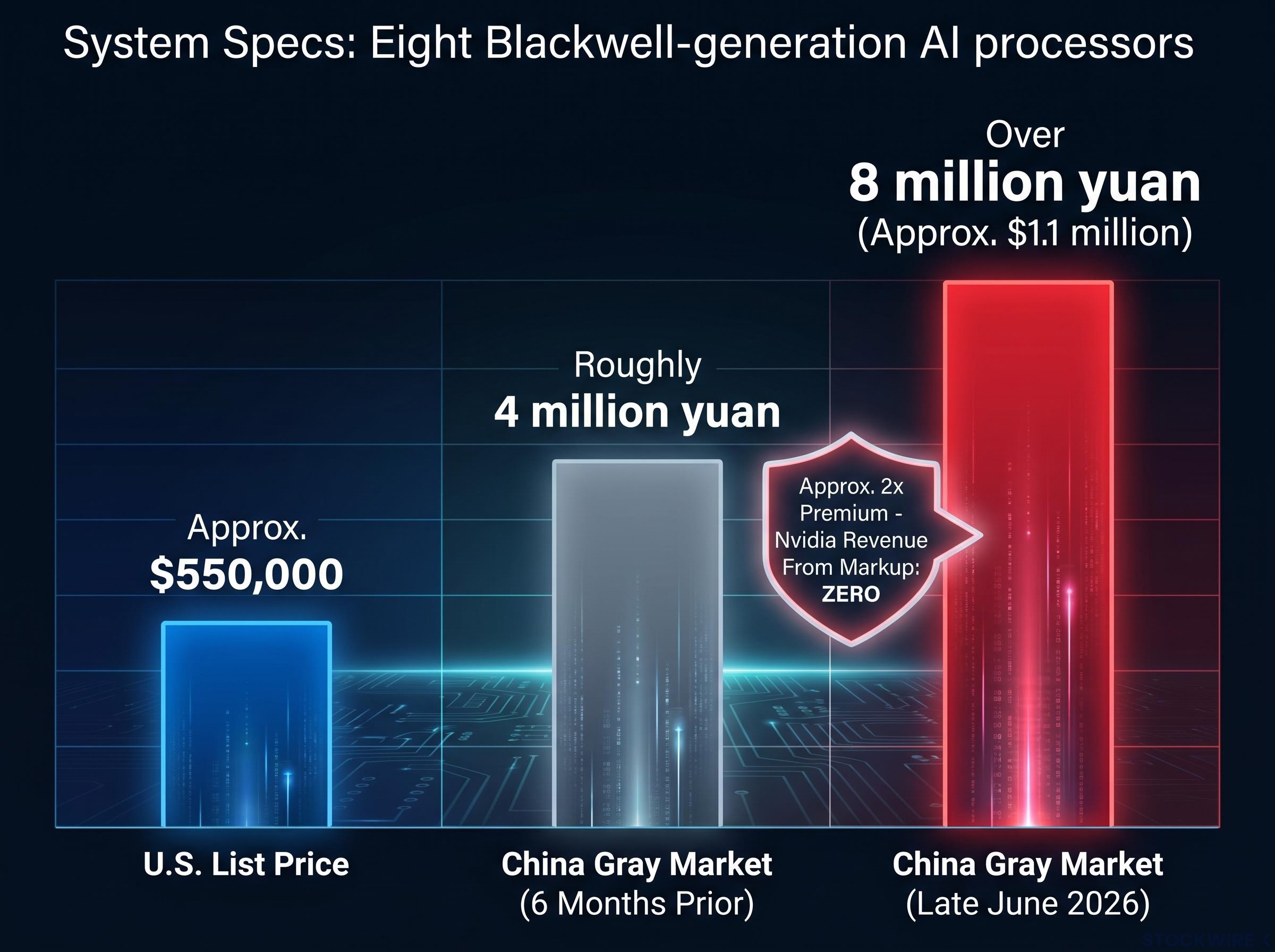

China’s gray market put a precise price tag on restricted AI hardware: the Nvidia DGX B300, a top-tier AI server, has seen its unofficial asking price climb to more than 8 million yuan (roughly $1.1 million) from around 4 million yuan just six months prior. That is close to double the approximate $550,000 U.S. list price for a single system.

The doubling is not a curiosity. It is the clearest available signal of what happens when demand for frontier AI hardware runs headlong into a regulatory wall. Since October 2022, Washington has progressively restricted China’s access to top-end AI chips and systems. Official supply channels are shut. The premium exists because demand has nowhere legal to go, and Nvidia captures none of the gray-market markup.

Here is what the data actually tells you about Nvidia’s China exposure: demand is proven, access is the constraint, and U.S. export policy is the single variable most capable of repricing the company’s China segment faster than any product cycle or earnings release.

The numbers speak first. The Financial Times reported that the DGX B300’s price in unofficial channels surpassed 8 million yuan by late June 2026, having started the preceding six-month period at roughly 4 million yuan, a rise of more than 100%. Each of these systems is built around eight Blackwell-generation AI processors.

DGX B300 gray-market price: over $1.1 million, approximately double the U.S. list price of $550,000.

Gray-market premiums of this magnitude only persist when buyers see a product as both scarce and effectively irreplaceable. Not merely expensive; irreplaceable. The buyers paying double are not bargain hunters. They are:

The doubling tells you that Chinese demand for top-tier Nvidia systems has not softened under export pressure. It has been forced into informal channels. The suppressed revenue is a policy decision, not a market one, and that distinction reshapes how Nvidia’s upside should be modelled.

The gray-market premium did not appear from nowhere. It is the direct and predictable consequence of a policy escalation that has progressively narrowed every door:

Extraterritorial enforcement was extended in May 2026 through a Commerce Department directive requiring export licences for any Chinese-headquartered entity purchasing advanced AI chips regardless of where that entity physically operates, directly closing the third-country subsidiary workaround that had been the primary remaining legal channel.

The intent is specific. Washington aims to slow China’s frontier AI progress by capping access to the highest-end chips and systems, not to halt all Chinese AI activity. But each tightening step has directly reduced Nvidia’s addressable market in China while simultaneously increasing the gray-market premium. That relationship is likely to continue in whichever direction policy moves.

The BIS export controls on advanced computing, first imposed in October 2022 and expanded through 2023, established the performance thresholds that define which chips and systems are restricted from sale to Chinese buyers, and those thresholds have directly shaped the supply gap the gray market now prices at a 2x premium.

Nvidia has designed downgraded “China-safe” variants of its chips with performance dialled below export thresholds. The H20, an H-series variant, was one precedent. More recently, the company has developed cheaper Blackwell-architecture SKUs aimed at compliant price points.

The persistence of the gray-market premium despite these alternatives is telling. Chinese buyers perceive a meaningful performance gap between the compliant SKUs and the full DGX B300 systems, and that gap is exactly what the premium is pricing.

Here is where the analytical tension sits. The gray-market price surge looks bullish at first glance. It is not, at least not for near-term earnings.

Every DGX-class system sold through gray channels represents foregone high-margin revenue for Nvidia: no direct sale price, no software attach, no support contract. The company collects nothing from the markup. As controls have tightened, Nvidia has shifted toward lower-spec, lower-ASP (average selling price, the average revenue per unit sold) compliant products for China, compressing revenue per unit relative to unconstrained markets.

Nvidia’s Q1 FY2027 results, which showed data centre revenue of $75.2 billion representing approximately 92% of total revenue, were built almost entirely on U.S. and allied market demand, with China data centre compute revenue excluded from guidance entirely.

The gray-market premium is best understood as “demand left on the table” rather than a bullish catalyst for near-term earnings.

| Metric | Value |

|---|---|

| DGX B300 U.S. list price | Approx. $550,000 |

| DGX B300 China gray-market price | Over $1.1 million |

| Gray-market premium | Approx. 2x |

| Nvidia revenue from gray-market units | Zero |

| China data-centre revenue (pre-controls) | Significant contributor |

| China data-centre revenue (post-controls) | Structurally reduced |

For investors tracking Nvidia’s revenue line, the gray-market premium quantifies the China upside that is currently locked out. It functions as an option value indicator, not a current earnings driver.

You know chips matter. What you may not have fully internalised is that advanced AI hardware now sits in the same strategic category as dual-use defence technology, and that changes how its prices and supply chains should be read permanently.

Export controls on AI hardware follow the logic of defence-related technology restrictions, where strategic considerations override normal trade economics. The pricing signals, risk factors, and policy variables are now structurally equivalent. When a government decides who can buy a product, that product’s economics shift from commercial to geopolitical.

Advanced AI hardware should be analysed with the same framework investors apply to defence procurement: policy-driven access, sticky premiums, and structural supply constraints.

China’s response has been to invest heavily in domestic alternatives:

For investors, this framing explains why gray-market premiums are sticky and why the competitive threat from domestic Chinese alternatives is real but not imminent for the most demanding AI workloads.

The variable that matters most is not product performance or competitive positioning. It is Washington’s next move. Three scenarios frame the range.

| Scenario | Key Trigger | Nvidia China Impact | Gray-Market Implication |

|---|---|---|---|

| Status quo | No material policy change | Compliant lower-ASP products continue; strong demand in U.S. and Europe offsets China constraints | Gray-market activity persists at current premiums |

| Further tightening | Wider extraterritorial enforcement or stricter system-level controls | Legal sales into China compress further; compliance costs rise; accelerated Chinese domestic investment | Premiums could rise further as supply narrows |

| Partial relaxation | Narrowly tailored exemptions or higher performance thresholds | Significant pent-up demand could be unlocked rapidly | Current premium serves as a pricing floor indicator for what buyers will pay |

Across all three scenarios, U.S. policy decisions matter more for Nvidia’s China trajectory in the near term than competitive dynamics or product cycles. Export-control policy should be on every Nvidia investor’s primary monitoring list, not as background context, but as the single variable most capable of repricing the China segment faster than any earnings release.

The structural durability of these restrictions comes from their national-security law backing, with bipartisan Congressional support placing chip controls outside the jurisdiction of trade negotiators, meaning they cannot be unwound through the same diplomatic channels that have produced tariff agreements.

The DGX B300 gray-market surge distils into four specific takeaways:

The DGX B300 price spike is not a buy signal on its own. It is a precise measure of how much upside remains locked behind a regulatory door. Investors who understand that distinction are better positioned for whatever policy shift comes next.

For investors wanting to model what China upside recovery would actually mean across Nvidia’s full revenue stack, our full explainer on Nvidia’s platform investment thesis covers how Goldman Sachs, Morgan Stanley, and William Blair decompose data centre revenue into four distinct layers, including the networking and software attach rates that would accompany any compliant China sales resumption.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding policy scenarios and competitive dynamics are speculative and subject to change based on regulatory developments and market conditions.

The doubling of DGX B300 prices on China’s gray market is not a story about smuggling or arbitrage. It is a precise market signal about where effective AI hardware dominance resides, and which variable determines whether that dominance translates into realised revenue.

Demand is confirmed. Access is the constraint. Policy is the lever. That relationship held through every tightening cycle since October 2022, and it will hold through whatever comes next.

Gray-market pricing will remain a live indicator worth watching, because it encodes, in real time, both the scale of unmet demand and the direction of buyer desperation. The price is the signal.

—

The Nvidia DGX B300 is a top-tier AI server built around eight Blackwell-generation AI processors, priced at approximately $550,000 in the U.S. It is restricted in China under U.S. export controls that have progressively blocked access to frontier AI hardware since October 2022, with system-level restrictions on DGX-class units added in 2025-2026.

By late June 2026, the DGX B300 was selling in China's unofficial channels for more than 8 million yuan (over $1.1 million), having risen from approximately 4 million yuan six months earlier, a premium of roughly 2x the U.S. list price.

No. Every DGX-class system sold through gray-market channels represents foregone revenue for Nvidia: the company collects nothing from the markup, no software attach, and no support contract, meaning the gray-market premium reflects demand left on the table rather than a current earnings driver.

A partial relaxation of U.S. export controls, such as narrowly tailored exemptions or higher performance thresholds, could rapidly unlock significant pent-up demand and compress the gray-market premium, making policy evolution the single variable most capable of repricing Nvidia's China segment.

Domestic Chinese alternatives from Huawei and Cambricon are still assessed as lagging Nvidia at the frontier in both performance and software ecosystem maturity, with meaningful competitive catch-up for the most demanding AI workloads remaining a multi-year prospect despite sustained state investment.